SHI 1.31.18: Pirates in China

SHI 1.24.18: The Rate of Return on Everything

January 24, 2018

SHI 2.7.18: Bonds, Bunds and Gilts

February 7, 2018

When is debt not debt … and, in fact, is treated as equity?

When the debt in question is the result of selling a “perpetual bond.” What is a perpetual bond, or “perp,” you ask? It is a bond with no maturity date.

Perpetual bonds are not new. The first was issued in Holland in 1648. Ironically, it remains outstanding, in the possession of Yale University, and paid interest in 2015. But today, companies rarely issue perpetual bonds.

Except in China. Where, in my opinion, perps have become the latest and greatest scheme to defraud unwitting investors. Here’s how the duplicity works.

Welcome to this week’s Steak House Index update.

If you are new to my blog, or you need a refresher on the SHI10, or its objective and methodology, I suggest you open and read the original BLOG: https://www.steakhouseindex.com/move-over-big-mac-index-here-comes-the-steak-house-index/

Why You Should Care: The US economy and US dollar are the bedrock of the world’s economy. This has been the case for decades … and will continue to be true for years to come.

Is the US economy expanding or contracting?

According to the IMF (the ‘International Monetary Fund’), the world’s annual GDP is almost $80 trillion today.

During the calendar year 2017, US nominal GDP increased by $833 billion … by an amount approximately equal to the market capitalization of Apple. At the end of 2017, US ‘current dollar’ GDP was about $19.749 trillion — about 25% of the global total. Other than China — a distant second at around $11 trillion — no other country is close.

The objective of the SHI10 and this blog is simple: To predict US GDP movement ahead of official economic releases — an important objective since BEA (the ‘Bureau of Economic Analysis’) gross domestic product data is outdated the day it’s released.

Historically, ‘personal consumption expenditures,’ or PCE, has been the largest component of US GDP growth — typically about 2/3 of the total. In fact, the majority of all US GDP increases (or declines) usually result from (increases or decreases in) consumer spending. This is clearly an important metric. The Steak House Index focuses right here … on the “consumer spending” metric.

I intend the SHI10 is to be predictive, anticipating where the economy is going – not where it’s been. Thereby giving us the ability to take action early.

Taking action: Keep up with this weekly BLOG update. Not only will we cover the SHI, but we’ll explore related items of economic importance.

If the SHI index moves appreciably -– either showing massive improvement or significant declines –- indicating growing economic strength or a potential recession, we’ll discuss possible actions at that time.

The BLOG:

In 2017, Chinese companies sold more than $50 billion of perpetual bonds. Known as ‘perpetuals’ or ‘perps,’ these little beauties are unique. Unique how, you ask? Here’s how: Believe it or not, international accounting rules permit the seller of a perp to book the bond as equity on their balance sheet. Not debt. Yep. True.

How does a Chinese company struggling under a large debt load “reduce” the weight of over-leverage? Simple: Sell perps that are counted as equity. In theory and by accounting standards, since the perp bond is never due and payable, it’s not considered a debt on the issuing company’s balance sheet. In fact, the proceeds from the bond sale are counted as equity on the balance sheet. Meaning, of course, that the issuing company likely has quite a bit more debt on its books than it appears.

“Chinese issuers love perpetual bonds because they are under great pressure to deleverage,” said Wang Ying, a senior director at Fitch Ratings in Shanghai. “Sophisticated investors should do their homework and shouldn’t be misled by the numbers in accounting books.”

Right.

So, who’s selling these things? Here you go:

You have probably heard of Greentown. They are developing real estate in downtown LA. They are heavily leveraged. About 6 months ago, they went deeper into debt when they sold $450 million of ‘perps’ — but, of course, this debt was booked as equity on their balance sheet. They pay 5.25% — a good yield for a Chinese government-backed company — until 2020 when the debt payment (I’M SORRY, I meant ‘equity’) floats 500 basis points over Treasuries. And this bond is never due. Never. The issuing company can pay it off early. After a minimum of 5 years. If they wish … but the bond itself has no due date. 🙂

The first problem here is the lack of transparency. Unless an investor is really sharp and is able to discern from public filings if a company has issued perps, he or she would never know. The second: With debt on the books, a company must pay interest. Not so for traditional equity. But if that ‘equity’ is actually a ‘perp,’ it DOES require an interest payment. For its $450 mm perp, Greentown will pay over $23.6 million each year. For the next 5 years minimum.

Here’s a quote from Shuli Ren in an article he wrote back in July when Greentown floated their perp:

“China’s state-backed enterprises are playing a game of cat-and-mouse with Beijing. Investors should be aware that if there’s a way around regulators’ efforts to clamp down on excess leverage, they’ll find it.”

Ouch. Perps are not equity. International accounting standards notwithstanding. In my book, this treatment is pure financial duplicity. And another reason to stay far, far away from all Chinese equities. You really don’t know what you’re buying … or what’s really on their balance sheet.

My opinion only. But, to quote my pirate friends, “Ye be warned!”

OK…let’s return to a much safer place: THE STEAK-HOUSE! A place where you might get burned, but only because you popped a morsel of that sizzling T-Bone into your mouth before it cooled. Ye be warned! 🙂

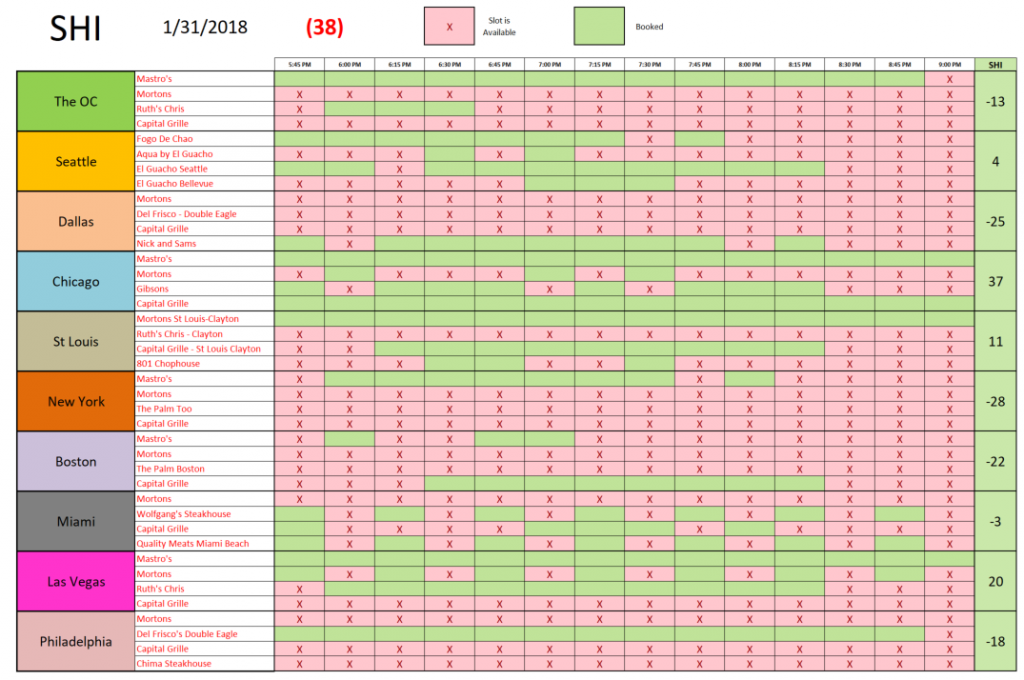

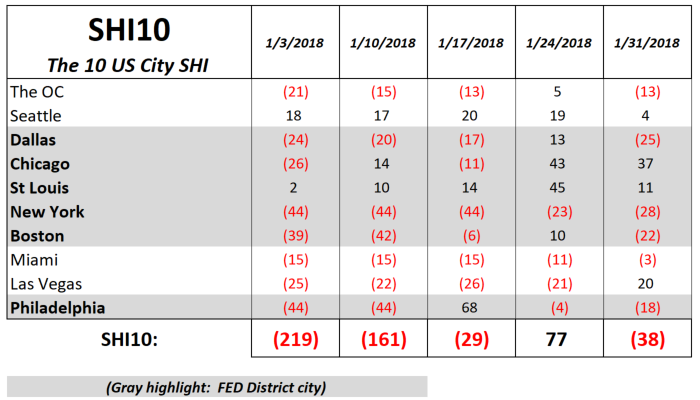

Well, this week our SHI10 index reading is a bit weaker than last. Here’s today’s grid for reservations on Saturday, February 3rd:

Once again, folks in Chicago are heading to the steakhouse this weekend. But the high-water mark last week — St. Louis — is a bit weaker this week. Steaks are much more popular in Las Vegas this coming Saturday — again, Mastros is fully booked in this market. Here’s the comparison grid:

With the exception of Las Vegas, consumer demand fell this week. Of course, since we kicked off the new SHI10 on 1/3, opulent eatery demand has improved significantly. As we would expect with a well functioning economy.

Let me finish with comments on a couple of meaningful issues: The Q4 ‘advance’ GDP number and the 10-year Treasury.

Per the Bureau of Economic Analysis (BEA) the first assessment of 2017 Q4 GDP growth is 2.6%. While this number is, in itself, a very positive outcome, looking at the numbers behind the headline we see something even more interesting: Q4 GDP growth would have been MUCH higher except for a huge spike in imports. Here are the individual contributions of the four (4) GDP sectors:

- PCE: 1.76% Once again, PCE is responsible for almost 70% of all GDP growth.

- Gross Investment: 0.6%

- Government: 0.5%

- Net Exports: a negative <1.13%>

Breaking ‘net exports’ down further, we find gross exports added a strong 0.82% to GDP for the quarter. But ‘net imports’ subtracted a whopping 1.96%! Wow. Expect this outcome to reverse this quarter as the dollar grows weaker against foreign currencies. Our exports will become cheaper for other countries; their exports to us, much more expensive.

Finally, as I write this blog the 10-year Treasury is north of 2.7% — a significant increase over about a month ago. Rest assured I’ll be diving deeper into this move in future blogs … but for now, permit me this comment: Current interest rates reflect expectations about the future. A recent change in future expectation — at least from the perspective of US investors — is the result of the new tax act. The potential for significant increases in US budget deficits is much greater than a month or two ago. If our deficit increases, the US Treasury must issue and sell more bonds. Adding supply to the marketplace. It’s quite possible, perhaps even likely, recent 10-year yield increases reflect this concern. We’ll talk more about this issue in future blogs. Thanks for tuning in.

- Terry Liebman