SHI 10.13.21 – Coming Soon: A Housing Crash?

SHI 10.6.21 – Change is the Only Constant

October 6, 2021

SHI 10.20.21 – Let the Good Times Roll!

October 20, 2021

No, not here in America. Relax. All good here. China is the problem. Here in the US, in spite of a record setting 18.1% Y-O-Y nationwide home price growth rate, according to CoreLogic (August, 2021), our housing market is solid as a rock. But in China, the chickens are finally coming home to roost, so to speak. Their housing market has run amuck for years – much like, well, much like a chicken with its head cut off. Ironically, the source of both problems is the same: China’s senior political leadership.

“

The changing landscape in China is troubling.“

“The changing landscape in China is troubling.“

Yes, things are very different today. I suspect you’ve noticed the same thing. Which, for me, triggers a host of questions: Just how crazy are Chinese home prices? Can the Chinese market actually crash? Is this leadership’s goal … to punish the ‘capitalist speculators’ in China? And finally, what impacts might this have on the rest of the world economies? Could a ‘crash’ in China trigger another global recession, much like the Great Recession of 2008?

Great questions.

Welcome to this week’s Steak House Index update.

If you are new to my blog, or you need a refresher on the SHI10, or its objective and methodology, I suggest you open and read the original BLOG: https://www.steakhouseindex.com/move-over-big-mac-index-here-comes-the-steak-house-index/

Why You Should Care: The US economy and US dollar are the bedrock of the world’s economy.

But is the US economy expanding or contracting?

The short answer? Expanding. By a staggering measure. In fact, during Q1 and Q2, annualized 2021 ‘real’ growth averaged about 6.4%. In nominal terms, our US economy averaged almost 12% growth — adding $1.245 trillion of economic activity during the first half of the year. The world’s annual GDP is expect to end 2021 near about $93 trillion. Annualized, America’s GDP settling in at almost $23 trillion by mid-year — still around 25% of all global GDP. Collectively, the US, the euro zone, and China still generate about 70% of the global economic output. These are your big players.

The objective of this blog is singular.

It attempts to predict the direction of our GDP ahead of official economic releases. Historically, ‘personal consumption expenditures,’ or PCE, has been the largest component of US GDP growth — typically about 2/3 of all GDP growth. In fact, the majority of all GDP increases (or declines) usually results from (increases or decreases in) consumer spending. Consumer spending is clearly a critical financial metric. In all likelihood, the most important financial metric. The Steak House Index focuses right here … on the “consumer spending” metric. I intend the SHI10 is to be predictive, anticipating where the economy is going – not where it’s been.

Taking action: Keep up with this weekly BLOG update. Not only will we cover the SHI and SHI10, but we’ll explore “fun” items of economic importance. Hopefully you find the discussion fun, too.

If the SHI10 index moves appreciably -– either showing massive improvement or significant declines –- indicating growing economic strength or a potential recession, we’ll discuss possible actions at that time.

The Blog:

If China’s housing market crashes, it will be self-inflicted. Do I expect it to actually crash? No, I don’t. But they are playing with fire.

For close to 15 years, the political leaders of the People’s Republic of China (PRC) have been more laissez faire than controling.

But that changed with the flip of a switch in February of this year. Government officials have now decided to take a firmer hand, attempting to limit housing speculation and keep prices under control. The most aggressive plan is in the city of Shenzhen, where under new regulation, an 84-page rule book lists maximum prices for more than 3,500 property developments citywide. Buyers can pay more – if they wanted to – but the ‘overage’ cannot be financed. Several large online property-listing platforms also removed advertised prices on existing homes and replaced them with the government’s guidance prices.

We’ve all heard the stories of China’s problems with rampant home speculation, their “see-thru” apartment buildings, and torrid value increases. Just months ago, a “modest sized apartment” in Shenzhen cost more than $1 million. Clearly, in 2021, this has become an affront to the PRCs political leaders. After all, China is a communist country, right? ?

Not really … and certainly not for the past 15 years or so, anyway … but now Xi Jinping appears to have rediscovered his party membership card that was tucked away in his sock drawer, gathering dust, for more than a decade. All of a sudden China is going communist! Whether they want to or not!

Reading the tea leaves, so to speak, it my opinion “anti-capitalist” policy shifts at the highest levels of the Chinese autocracy have triggered the problem. We’ve seen the same in government actions against the founders of Alibaba and a host of other large and successful Chinese companies. What impact will the policy shift have on the Chinese economy? And perhaps a more important question for the rest of us non-Chinese folks, how will this affect the US and global economies?

China’s actions are grave … and concerning. Both here in the US and inside of China. True or not, a “home buyer forum” in Guangzhou said they had learned that “Evergrande placed the money from their down payments in a private bank account and not the one stipulated by the local authority and monitored closely.” Ooops. That doesn’t sound good. Here in the US of A, we might call that ‘fraud’ or ‘commingling.’ Big no-nos.

China’s actions also seem to suggest that China’s home prices are rising unsustainably, achieving higher-and-higher highs, far surpassing home price increases in other developed economies around the globe. But, ironically, that is untrue.

In fact, according to a ‘Global house prices’ interactive tool, courtesy of The Economist magazine, home values (inflation adjusted) in China have increased about the same as home values here in the US: About 35% in the past 10 or so years. In fact, US and China 10-year home value appreciation is fairly tame when compared to some developed nations like New Zealand, up 61% since 2010, and Israel (55%), and Austria, Canada and Switzerland, all up about 50%.

However, after we convert from “real” prices to “nominal”, it turns out that China’s prices have zoomed up quite a bit. (China’s inflation rate has been running pretty hot since 2018). So, nominally, home prices in China are up 75% in the past 10 years, compared to about 59% (nominal) here in the US. Iceland “wins” the 10-year nominal-price appreciation contest, however: Their 10-year nominal price increase is 120%. 🙂

And since we humans actually live in a nominal world, China’s prices look pretty steep. To regulators and to buyers. But thru the “price to rents” lens, home value inflation in China is fairly tame:

Regardless, Xi has decided that China needs a new strategy. We’ve all watched the Evergrande debacle unfold … I don’t need to revisit it. And we’ve all seen how other large Chinese property developers are also defaulting, or threatening to default, on their dollar-denominated debt.

But why now?

I think this is part of a larger, multi-faceted message from the Chinese communist party leadership. First, I think PRC leaders are telling their citizens, “Stop speculating! We’re communists, damn it! You are screwing up the country for everyone else!” OK, that seems obvious. Clearly new policy, new lending guidelines, and a tougher stance from their banks and the PBOC — the “Peoples Bank of China,” their equivalent to the FED — again make that an obvious conclusion.

Secondly, the bond defaults by China’s housing giants appears to be in dollar-denominated bonds. By defaulting on these dollar bonds, China seems to be saying to the world that (1) we are unhappy with America right now, and (2) you should not invest in Asia high-yield, US dollar bonds.

The value of this group of bonds is down precipitously … and is currently yielding about 13%. Risk of permanent default is very high … and I suspect China is pulling this lever, too, in an attempt to reduce funding, and therefore, excesses, within their housing markets.

Can the Chinese market actually crash? Is this leadership’s goal … to punish the ‘capitalist speculators’ in China? And finally, what impacts might this have on the rest of the world economies? Could a ‘crash’ in China trigger another global recession, much like the Great Recession of 2008?

Even so, I expect the PBOC to prevent a crash and meltdown. The central bank has been been making market-supporting comments, suggesting that they are simply “fine tuning” their housing market. So while the holders of billions of dollars of junk bonds may not get paid … at least, not in full … China’s central bank vowed to ensure a “healthy property market” and protect home buyers’ rights. This way their citizens are protected while, at the same time, they punish those money-grubbing capitalists in the US and elsewhere!

I do not expect we will see any larger US or global stock or debt market contagion, beyond what has already occurred. And no, I do not expect a US or global recession as a result. The sub-prime crisis of the mid-2000s was a very different problem issue, much larger in scope.

To the steakhouses!

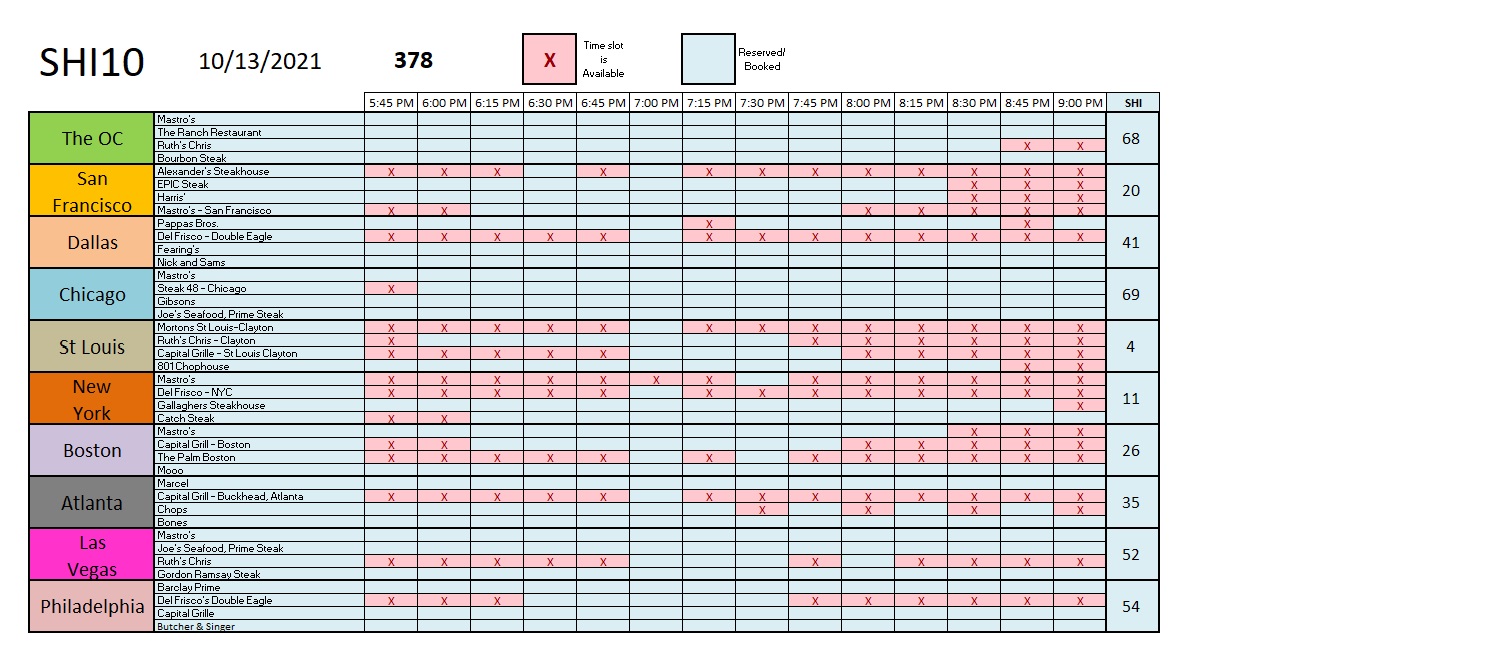

Numbers are little changed this week … steaks are grilling … reservations are in high demand:

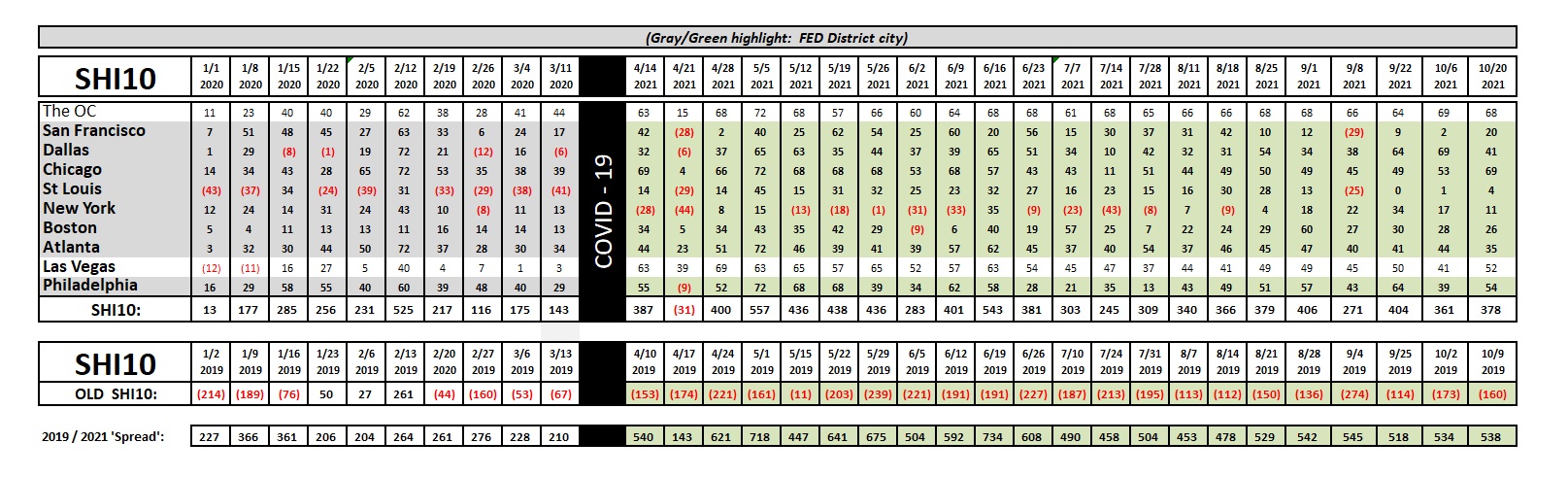

Check out Chicago! At 11:00 am this morning, the four SHI restaurants we track had only one (1) time slot remaining — at 5:45 pm! The grills are smoking in Chicago! Here’s the longer term trend chart:

Consistent … not much change week-over-week. Reservation demand remains elevated. Good.

The FED released the minutes from their September 21-22 meeting earlier today. If you’ve never looked at them before, I suggest you take a peek. It’s neither overly lengthy nor complex. They work hard to “dumb down” their language; I think they accomplish that goal. I’ll include a link below should you want to take a gander.

If not, permit me a few brief comments on three (3) topics:

China:

Quoting the FED, “… concerns had grown recently about the possible implications of developments in China.” They are watching … and like us, they are concerned too.

Inflation:

“Inflation, as measured by either the PCE price index or the consumer price index (CPI), had been boosted by a surge in demand as the economy reopened further, along with the effects of production bottlenecks and supply constraints. Total PCE price inflation was 4.2 percent over the 12 months ending in July, and core PCE price inflation, which excludes changes in consumer energy prices and many consumer food prices, was 3.6 percent over the 12 months ending in July. In contrast, the trimmed mean measure of 12‑month PCE inflation constructed by the Federal Reserve Bank of Dallas was 2.0 percent in July. In August, the 12-month change in the CPI was 5.3 percent, while the core CPI rose 4.0 percent over the same period.”

Finally, on this topic:

“In the third quarter of 2021, the staff’s common inflation expectations index, which combines information from many indicators of inflation expectations and inflation compensation, was little changed relative to the second quarter and was near its average over the decade before the pandemic.”

Interesting. This is why the FED is sticking to their guns on their belief in the “transitory” nature of inflation. Transitory or not, it’s also worth noting that earlier today the Social Security Administration (SSA) said that “… higher inflation will trigger a 5.9% increase in Social Security benefits….” This is the single largest increase in over 40 years.

The Taper: Here we get the true essence of the FEDs intentions. At present, they are targeting either a November or December start date. They plan to reduce their monthly purchases by about $15 billion per month. Recall that currently they are buying about $120 billion each month … so the taper will shrink bond buying over the 8 months after they begin down to zero. It’s worth mentioning that at present, assets on the FED balance sheet total is near $8.5 trillion. 🙂

Here’s that link:

https://www.federalreserve.gov/monetarypolicy/fomcminutes20210922.htm

<|> Terry Liebman