SHI 10.2.19 – Chew on This, Beyond Meat!

SHI 9.25.19 – Recession Talk

September 25, 2019

SHI 10.9.19 – Cracks in the Foundation

October 9, 2019

“Steak is GOOD FOR YOU!”

Well, at the very least, it’s not bad for you. According to the NY Times on Monday, consumption of red meat is fine is not a health hazard. Which is really good news for our expensive steakhouses, given the growing battle between the ‘red meat’ folks and the ‘plant-based’ meat substitutes like Beyond Meat and the Impossible burger.

In fact, according to an international collaboration of medical researcher, reported it the Annals of Internal Medicine, the advice to limit consumption of red meat (because it is linked to heart disease and cancer) is not backed by good scientific evidence. Their findings are based on:

- Three years of work by a group of 14 researchers in seven countries, along with three community representatives, directed by Dr. Johnston. The investigators reported no conflicts of interest and did the studies without outside funding.

- The group reviewed 61 articles reporting on 55 populations, with more than 4 million participants.

- The researchers also looked at randomized trials linking red meat to cancer and heart disease (there are very few), as well as 73 articles that examined links between red meat and cancer incidence and mortality.

In each study, the scientists concluded that the links between eating red meat and disease and death were small, and the quality of the evidence was low to very low. OK … happy days are here again for our steakhouses! 🙂

Welcome to this week’s Steak House Index update.

If you are new to my blog, or you need a refresher on the SHI10, or its objective and methodology, I suggest you open and read the original BLOG: https://www.steakhouseindex.com/move-over-big-mac-index-here-comes-the-steak-house-index/

Why You Should Care: The US economy and US dollar are the bedrock of the world’s economy. This has been the case for decades … and will be true for years to come.

But is the US economy expanding or contracting?

According to the IMF (the ‘International Monetary Fund’), the world’s annual GDP is about $85 trillion today. US ‘current dollar’ GDP now exceeds $21.3 trillion. In Q2 of 2019, nominal GDP grew by 4.7%. The US still produces about 25% of global GDP. Other than China — in a distant ‘second place’ at around $13 trillion — the GDP of no other country is close. The GDP output of the 28 countries of the European Union collectively approximates US GDP. So, together, the U.S., the EU and China generate about 70% of the global economic output.

The objective of the SHI10 and this blog is simple: To predict US GDP movement ahead of official economic releases.

Historically, ‘personal consumption expenditures,’ or PCE, has been the largest component of US GDP growth — typically about 2/3 of all GDP growth. In fact, the majority of all GDP increases (or declines) usually results from (increases or decreases in) consumer spending. Consumer spending is clearly a critical financial metric. In all likelihood, the most important financial metric. The Steak House Index focuses right here … on the “consumer spending” metric. I intend the SHI10 is to be predictive, anticipating where the economy is going – not where it’s been.

Taking action: Keep up with this weekly BLOG update. Not only will we cover the SHI and SHI10, but we’ll explore related items of economic importance.

If the SHI10 index moves appreciably -– either showing massive improvement or significant declines –- indicating growing economic strength or a potential recession, we’ll discuss possible actions at that time.

The BLOG:

The fun aside, here’s my problem with this “meaty” debate: Who’s right? Is this “fake news” or factual? How do we know which data are accurate?

A few years ago a similar debate bubbled up over coffee. For years, perhaps even decades, we were told more than a cup or two of coffee, daily, was bad for you. But recent studies concluded that “people who drink three to four cups of coffee a day are more likely to see health benefits than harm, experiencing lower rates of premature death, cardiovascular disease and liver disease.”

And now, while eating more steaks may not have health benefits, apparently it doesn’t do any harm. So eat those T-bones and enjoy your coffee! It’s A-OK! Maybe. Depending on who you believe.

And this is why I write the Steakhouse Index. Without deeply digging into the economic headlines, I feel I might miss the essence … or the truth of the matter. And so I cut into the meat of each issue, chew intently on the data, and only after I’ve thoroughly digested everything, do I share my thoughts with you! Selfless, I know, but hey, that’s who I am. (And modest too!) 🙂

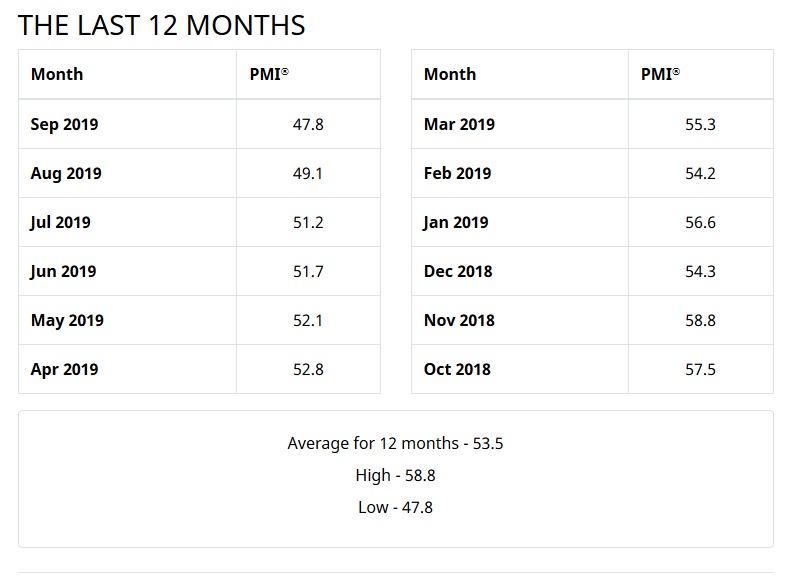

The stock markets are unhappy this week. The weight of negative economic news is clearly growing with each passing day, and the October 1st ‘Purchasing Managers’ Index’ — or PMI — tabulated by the Institute for Supply Management (ISM), showed increasing manufacturing weakness. An index reading of “50” is considered neutral, neither expansive or contracting, and we’re now at 47.3, down 1.3 points from last month’s reading. The ISM has been producing this report since 1948, so they likely have the bugs out of the survey by now. Of the 18 industries they survey monthly, 15 of them experienced a contraction in September. For context, here a chart showing the PMI readings for last 12 months:

About a year ago, the PMI Index stood above 58 — clearly expansionary. Today we’re almost 20% lower … and we’re in contraction territory. Not good. Let me finish with this quote from the October 1st report:

“Comments from the panel reflect a continuing decrease in business confidence. September was the second consecutive month of PMI® contraction, at a faster rate compared to August. Consumption (measured by the Production and Employment indexes) contracted at faster rates, again primarily driven by a lack of demand, contributing negative numbers (a combined 3.3-percentage point decrease) to the PMI® calculation. Global trade remains the most significant issue, as demonstrated by the contraction in new export orders that began in July 2019. Overall, sentiment this month remains cautious regarding near-term growth.”

There you have it. Business confidence continues to erode, at an increasing pace … and the trade wars seem to be the primary cause. Both here and abroad. Fact.

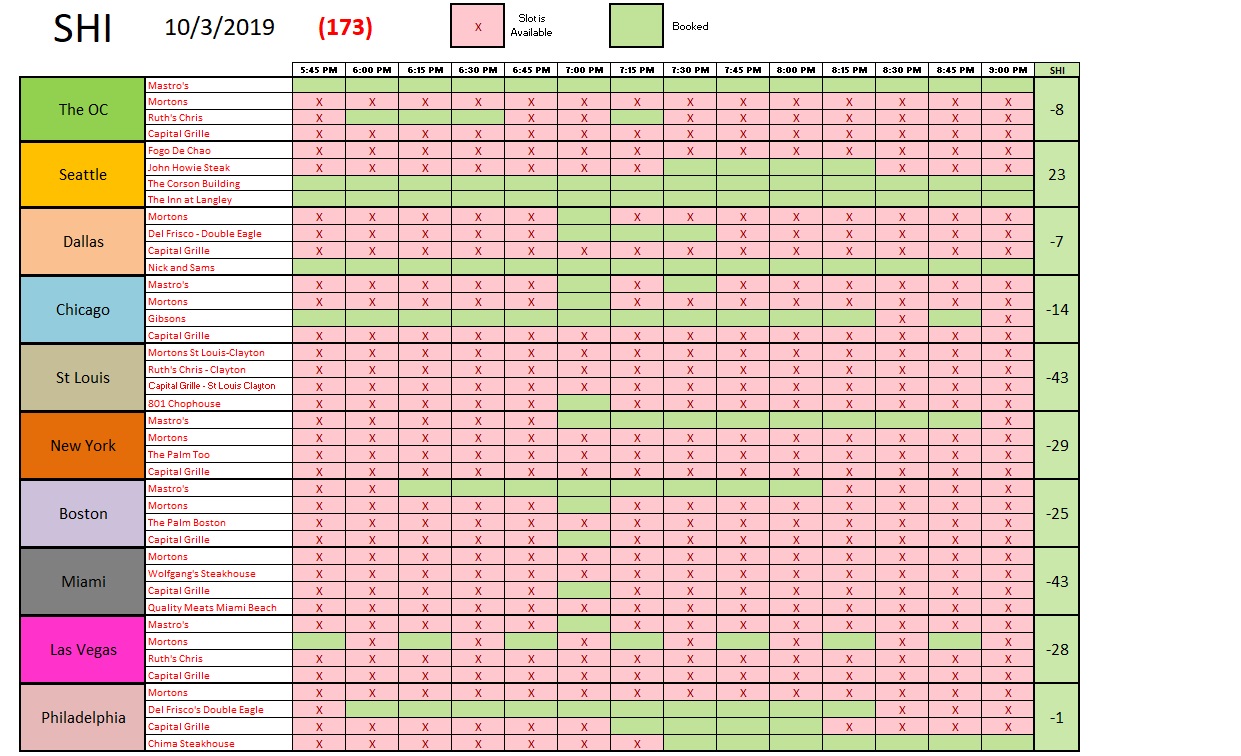

So its a good thing beef got a good report card from the Annals of Internal Medicine this week. Our expensive eateries probably needed the shot in the arm! Let’s see if it helped:

Well, not really. This weeks SHI10 is not good … but its not horrible. Once again, Philly is punching back from it’s typical weak pricey steak demand. And even stalwart Seattle seems to be feeling the pinch. Reservation demand is fairly well distributed across the country, however, with no one or two markets showing exceptional strength or weakness. On the restaurant level, once again reservations at Mastros are in high demand. Here’s the longer term trend:

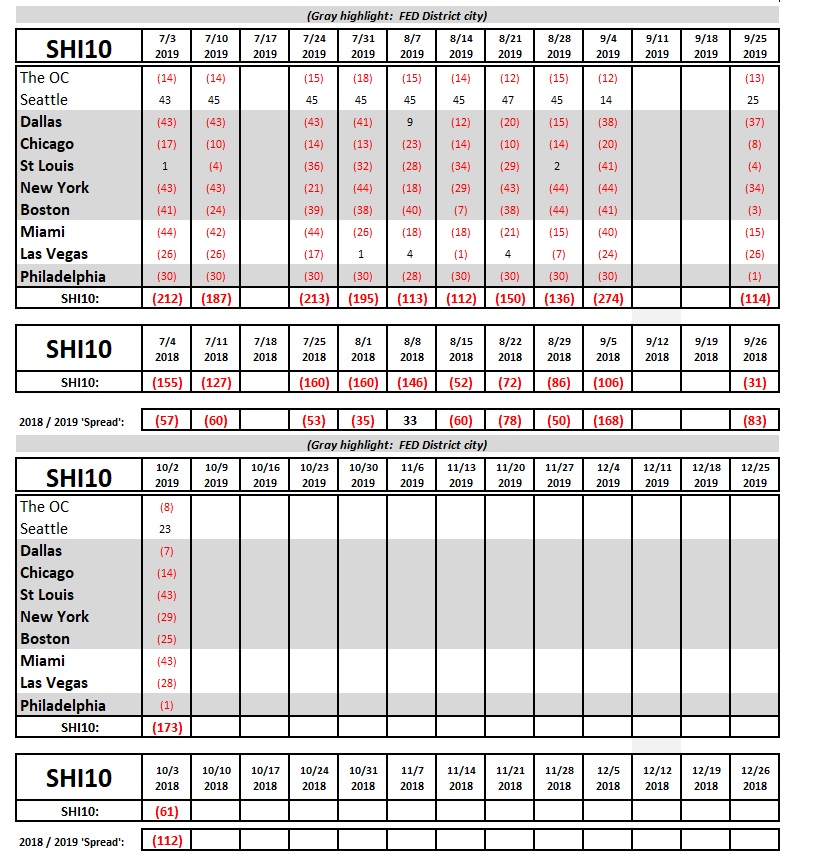

As this is a new calendar quarter, I’ve included Q3 and this first entry in Q4 on the trend chart. Big picture: Reservation demand at our extravagant steakhouses is lukewarm at best, much like the center of a ‘rare’ Filet Mignon. Either our well-heeled consumers with deep pockets and a hankering for a beautifully prepared steak are sharing the same feeling the manufacturing folks have, or the report on the health effects of steak hasn’t yet fully circulated across the internet. 🙂

As the US fiscal year ended on September 30th, I thought I’d offer a quick comment on the full year deficit. However, the Treasury data currently reflects just the first 11 months — thru the end of August. At that time, total ‘receipts’ by the Treasury equaled $3.088 trillion and total ‘outlays’ were $4.155 trillion, giving us an 11 month deficit of $1.067 trillion. Wow. Ouch.

If you’re interested to see where the US is spending it’s earned and borrowed money, click this link:

https://fiscal.treasury.gov/reports-statements/mts/current.html

Clearly the folks in Washington are doing all they can to keep the economy growing. Spend, spend, spend. On the other hand, the consumer seems to be showing signs of fatigue. As more economic challenges pile on, I grow more convinced we have a recession in our future. But not too soon. The US economy is huge. It can carry the weight for a fairly long time. Q3 will likely show positive GDP growth … but I feel it will be at the low end of the range. Over the longer-term, our economy is definitely showing signs of slowing.

- Terry Liebman