SHI 9.25.19 – Recession Talk

SHI 9.4.19 – Global Government Debt

September 4, 2019

SHI 10.2.19 – Chew on This, Beyond Meat!

October 2, 2019

“Welcome home, Terry!”

Thank you. Much appreciated. I have returned from Europe where I did all I could to help the economy of France. Eating and drinking my way thru the wine regions of ‘Champagne’ and ‘Burgundy’, I feel I did my part to pump up Europe’s economy. One bottle of wine at a time. But was it enough?

Welcome to this week’s Steak House Index update.

If you are new to my blog, or you need a refresher on the SHI10, or its objective and methodology, I suggest you open and read the original BLOG: https://www.steakhouseindex.com/move-over-big-mac-index-here-comes-the-steak-house-index/

Why You Should Care: The US economy and US dollar are the bedrock of the world’s economy. This has been the case for decades … and will be true for years to come.

But is the US economy expanding or contracting?

According to the IMF (the ‘International Monetary Fund’), the world’s annual GDP is about $85 trillion today. US ‘current dollar’ GDP now exceeds $21.3 trillion. In Q2 of 2019, nominal GDP grew by 4.6%. The US still produces about 25% of global GDP. Other than China — in a distant ‘second place’ at around $13 trillion — the GDP of no other country is close. The GDP output of the 28 countries of the European Union collectively approximates US GDP. So, together, the U.S., the EU and China generate about 70% of the global economic output. This is worth watching carefully, right?

The objective of the SHI10 and this blog is simple: To predict US GDP movement ahead of official economic releases — an important objective since BEA (the ‘Bureau of Economic Analysis’) gross domestic product data is outdated the day it’s released. Historically, ‘personal consumption expenditures,’ or PCE, has been the largest component of US GDP growth — typically about 2/3 of all GDP growth. In fact, the majority of all GDP increases (or declines) usually results from (increases or decreases in) consumer spending. Consumer spending is clearly a critical financial metric. In all likelihood, the most important financial metric. The Steak House Index focuses right here … on the “consumer spending” metric. I intend the SHI10 is to be predictive, anticipating where the economy is going – not where it’s been.

Taking action: Keep up with this weekly BLOG update. Not only will we cover the SHI and SHI10, but we’ll explore related items of economic importance.

If the SHI10 index moves appreciably -– either showing massive improvement or significant declines –- indicating growing economic strength or a potential recession, we’ll discuss possible actions at that time.

The BLOG:

I’m asked every day: “Is a recession coming soon?” The Economist magazine sums it up nicely:

“Recessions are synchronised declines in economic activity; weak demand typically shows up in nearly every sector in an economy.

Spot on. In a normal economy, now and then, one or more business segments experiences a downturn. This is common even during economic expansions. So for an economic contraction to gets legs, many (or even most) economic components must simultaneously weaken or slow. That same article goes on to say:

“Housing is often among the first sectors to wobble; as rates on mortgages go up, this chokes off new housing demand. In a paper published in 2007 Edward Leamer, an economist at the University of California, Los Angeles, declared simply that ‘housing is the business cycle.’ Recent history agrees.”

That makes sense. But here’s a question for Professor Leamer: Can a recession start if home loan rates are down? To complicate matters, can a recession start when home sales are accelerating?

Herein lies the complexity of our current economic puzzle. Some segments of our economy are showing weakness now: ‘Recreational vehicle’ sales are languishing, threatening thousands of jobs in Indiana. Recently, Lowes suggested they plan to slash thousands of jobs, and Haliburton plans to do the same. But are these signs of weakness? Or are they a reflection of shifts in shopping habits (a move to e-commerce) and the employment of new technology in the oil patch?

Looking at the bigger picture, we see an inverted yield curve, shrinking auto sales, increasing home sales, declining home loan interest rates, (relatively low) oil prices, a FED cutting rates, increased consumer savings rate, a US ‘household balance sheet’ with the highest net worth ever recorded, the lowest unemployment rate in more than 50 years, an increasing rate of existing home sales, shrinking demand for temporary workers, and a dramatically declining PMI (purchase managers index) both here and in Europe.

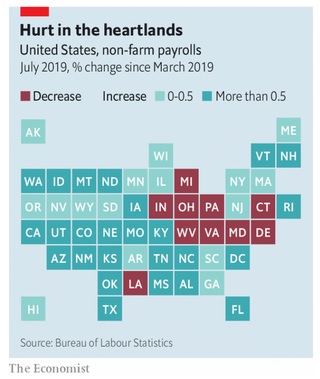

The bottom line: The economic picture is spotty. Some US industries — like construction — are still going gangbusters. Others, take manufacturing for example, are not. Geography seems to be playing a part too. Take a look at this graphic, courtesy of The Economist magazine:

While job growth across the US, in the aggregate, has been fairly consistent, not every geography is having the same experience. As we see above, the “rust belt” states are lagging behind. The list of states with falling employment is growing, and includes Ohio, Pennsylvania and Michigan. The “coasts” on the other hand are doing quite well. Job growth is strong here, and jobs are plentiful.

Part of the “rust belt” weakness is likely wreckage from the languishing trade war. US manufacturing in this region has been hit hard; Europe, on the other hand, has been absolutely decimated. This image, provided by TradingEconomics, shows the precipitous decline in ‘Euro Area’ manufacturing:

The speed of the 2019 decline in the euro area manufacturing is surprising. Manufacturing is now at levels not seen since 2012. Equally concerning, Germany saw output fall for the first time since April 2013, the rate of decline the steepest since October of 2012.

Chris Williamson, the Chief Business Economist at IHS Markit (the company that aggregates PMI data) made these comments:

“The eurozone economy is close to stalling as a deepening manufacturing downturn shows further signs of spreading to the services sector. The survey data indicate that GDP looks set to rise by just 0.1% in the third quarter, with momentum weakening as the quarter closed. The goods-producing sector is going from bad to worse, suffering its steepest downturn since 2012, but a further worrying trend is the broadening-out of the malaise to the service sector, where the rate of growth has now slowed to one of the weakest since 2014.

The details of the survey suggest the risks are tilted towards the economy contracting in coming months. Most vividly, new orders for goods and services are already falling at the fastest rate since mid-2013, suggesting firms will increasingly look to reduce output unless demand revives. Furthermore, hiring is being scaled back due to the order book slowdown, with jobs growth now down to the lowest since the start of 2015. A worsening labor market adds to the risk that households could trim their spending.

He concluded with this comment:

“The overall picture of an economy on the cusp of sliding into decline is underscored by a further deterioration in firms’ pricing power, with average prices charged for goods and services barely rising in September.”

Ouch. Clearly I didn’t buy enough wine or consume enough Michelin ‘star’ meals to help bolster the French economy. I’m sorry, France! 🙂

Manufacturing here in the US is faring better, so far, but even here the trade war has taken a toll. And it’s taken a toll on the consumer, too, as seen in the most recent confidence numbers: “Consumer confidence declined in September, following a moderate decrease in August,” said Lynn Franco, Senior Director of Economic Indicators at The Conference Board. “Consumers were less positive in their assessment of current conditions and their expectations regarding the short-term outlook also weakened. The escalation in trade and tariff tensions in late August appears to have rattled consumers.”

The bottom line is this: No, we’re not in a recession. Yet. But we’re moving that direction. Europe may already be contracting. And it’s clear that US consumers are “rattled” by all the trade rhetoric, to quote Ms. Franco.

Even if the trade war ends soon, a US recession could be on its way.

Are consumers still buying expensive steaks? Let’s take a look.

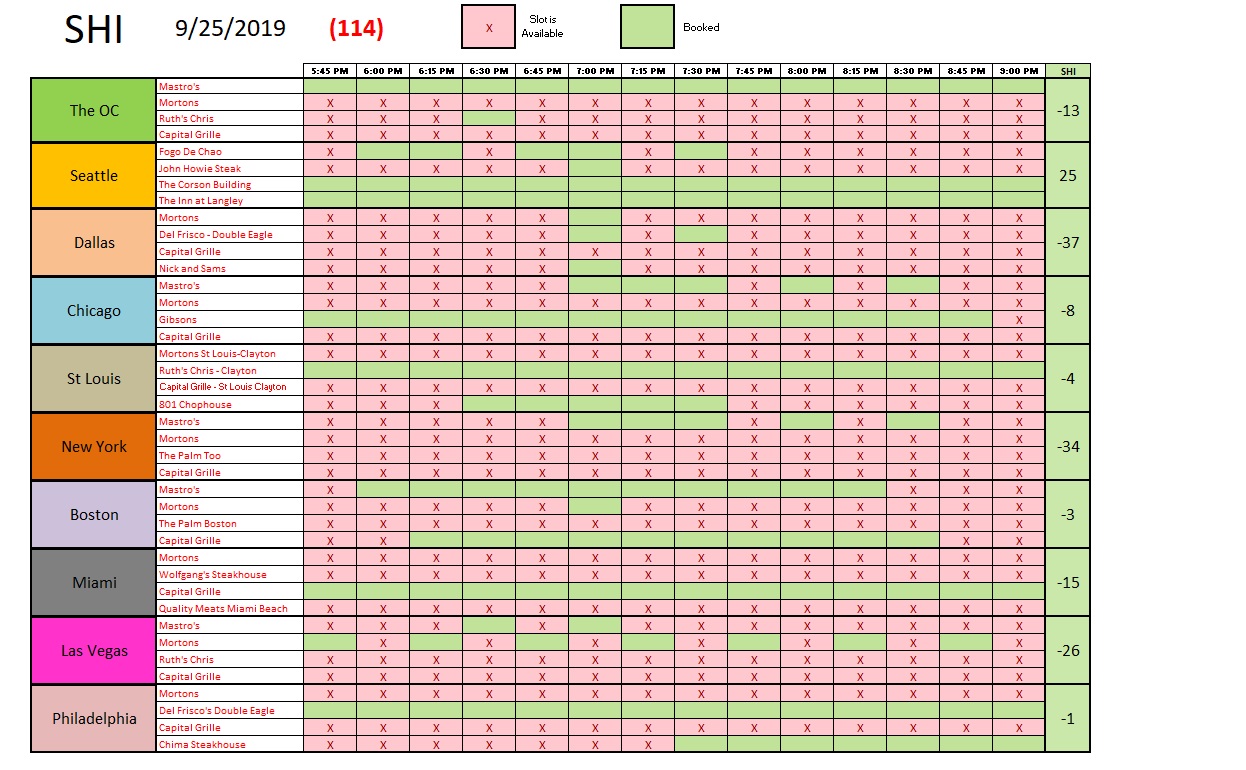

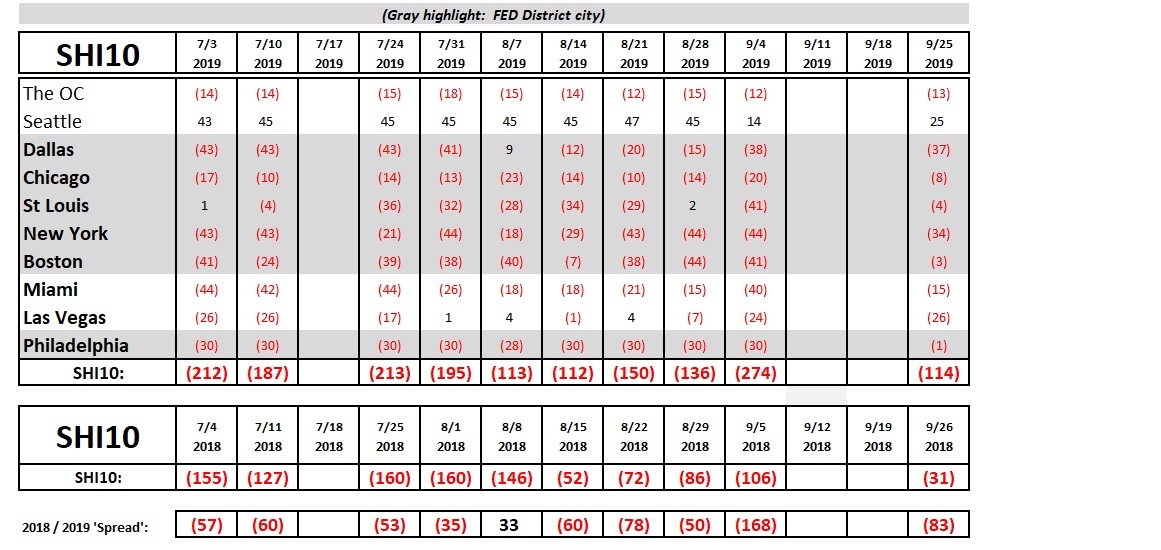

Interesting. Returning to the SHI after my 2 week hiatus, I see reservation demand at our pricey eateries has rebounded. Significantly. I see a lot more ‘green’ this week. Chicago, St Louis, Boston, Miami and Philly are all experiencing meaningful reservation demand increases this week. Here’s the longer term trend comparison:

Here we get a clearer picture of this week’s reservation demand improvement. The “spread” back on 9/4 was 168 points. This week, at 83 points, the spread is much more aligned with the historic trend. Piping hot NY strips are in demand, and the restaurants that serve the most expensive cuts are filling up this Saturday.

So while many data points suggest a recession is around the corner, an equally large number suggest the US economy continues to chug along. Make no mistake: I do not believe US GDP growth will offer an upside surprise this quarter. If anything, it will surprise to the downside. But GDP growth should remain positive, as our economy settles in, working hard to overcome the clear and dangerous obstacles thrown in its path by the trade wars.

– Terry Liebman