SHI 10.25.23 – We Are Not Alone

SHI 10.18.23 – Food and Drinking Places

October 18, 2023

SHI 11.22.23 — Velocity: Money and Food

November 22, 2023

No, today’s blog is not about little green men from other worlds.

But we will start today’s blog discussing the actions of some probably-not-green men (and women) and the long-term financial and economic implications of those actions. Ready?

“

US interest rates are at decade highs.”

“US interest rates are at decade highs.”

But we are not alone. As you’ll see in the ‘Blog’ below, with the only exception being the central bank of Japan, known as the BOJ, the central banks in every developed nation in the world have all hiked rates dramatically.

Is it coincidence? No. Remember, all these men (and women) are members of the same club where, I’m sure, they talk, share ideas, and coordinate actions. Which club, you ask? It’s called the BIS, or the ‘Bank for International Settlements,‘ located over in Basil, Switzerland. Every systemically-important central bank is a member … and I guarantee you it is no coincidence they have all interest rates in lock-step. And in doing so, while they may have (in theory) “solved” one problem, they have created a new one. And it might be worse.

Oh … and the ‘preliminary’ GDP numbers just came out this morning and they are HOT! Real GDP grew at the annualized rate of 4.9% in Q3. This number is sizzling. Even hotter: Current dollar GDP increased 8.5 percent at an annual rate, or $560.5 billion, in the third quarter to a level of $27.62 trillion. Considering the interest rate headwinds, this outcome is absolutely staggering in my opinion.

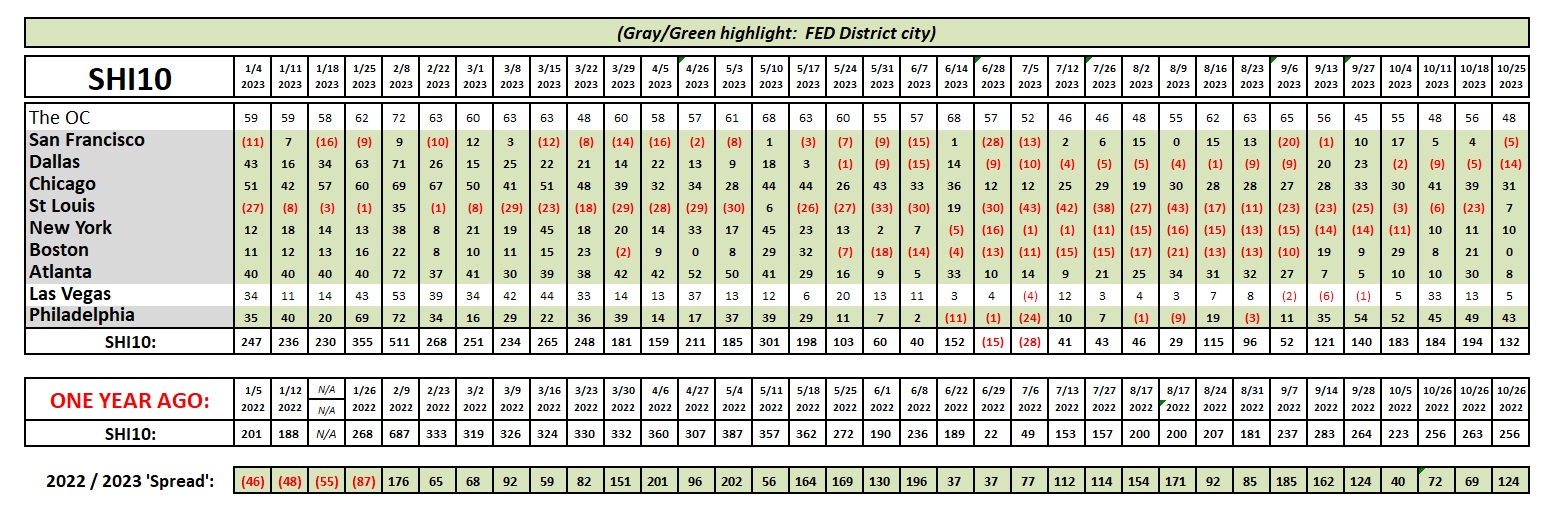

Welcome to this week’s Steak House Index update.

If you are new to my blog, or you need a refresher on the SHI10, or its objective and methodology, I suggest you open and read the original BLOG: https://www.steakhouseindex.com/move-over-big-mac-index-here-comes-the-steak-house-index/

Why You Should Care: The US economy and US dollar are the bedrock of the world’s economy.

But is the US economy expanding or contracting?

Expanding … FED rate increases notwithstanding! At the end of Q3, 2023, in ‘current-dollar‘ terms, US annual economic output rose to an annualized rate of $27.62 trillion. America’s current-dollar GDP increased at an annualized rate of 8.5% during the third quarter of 2023. Even the ‘real’ GDP growth rate was hot… clocking in at the annual rate of 4.9% during Q2.

The world’s annual GDP first grew to over $100 trillion in 2022. According to the IMF, in June of this year, current-dollar global GDP eclipsed $105 trillion! IMF forecasts call for global GDP to reach almost $135 trillion by 2028 — an increase of more than 28% in just 5 years.

America’s GDP remains around 25% of all global GDP. Collectively, the US, the European Common Market, and China generate about 70% of the global economic output. These are the 3 big, global players. They bear close scrutiny.

The objective of this blog is singular.

It attempts to predict the direction of our GDP ahead of official economic releases. Historically, ‘personal consumption expenditures,’ or PCE, has been the largest component of US GDP growth — typically about 2/3 of all GDP growth. In fact, the majority of all GDP increases (or declines) usually results from (increases or decreases in) consumer spending. Consumer spending is clearly a critical financial metric. In all likelihood, the most important financial metric. The Steak House Index focuses right here … on the “consumer spending” metric. I intend the SHI10 is to be predictive, anticipating where the economy is going – not where it’s been.

Taking action: Keep up with this weekly BLOG update. Not only will we cover the SHI and SHI10, but we’ll explore “fun” items of economic importance. Hopefully you find the discussion fun, too.

If the SHI10 index moves appreciably -– either showing massive improvement or significant declines –- indicating growing economic strength or a potential recession, we’ll discuss possible actions at that time.

The Blog:

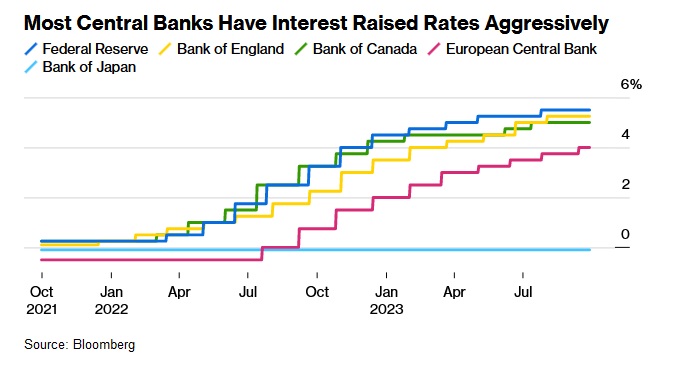

Consider this image clipped from a Bloomberg article:

Aggressively is right. In early 2021, the ECB “overnight funds rate” stood at a negative 0.5%. Do you remember that? Negative interest rates? It seems like so long ago. Today, the ECB rate stands at 4.0% … and the central banks in Canada, England and here in the US have all pegged short term rates much higher. The US is the highest at 5.5%.

And we all know the purpose: To crush the post-pandemic inflation surge. Whether the rate hikes did the trick, or the surge was, in fact, ‘transitional,’ inflation does appear to be heading back down toward the FED‘s long-term 2% goal.

But the rate hikes have left us with another, uncomfortable problem: High interest rates.

High interest rates aren’t a big deal for a debtor with small debt balances. The problem, of course, is that few have small debt balances today. America’s national debt now tips the scales at or near $33 trillion. Am I exaggerating? No. Check this out (right click, open in new Tab):

https://www.usdebtclock.org/index.html?taxpayer

From the Treasury’s website called “Debt the the Penny” the number for “Total Public Debt Outstanding” as of 10/24 was:

$33,684,219,111,864.76

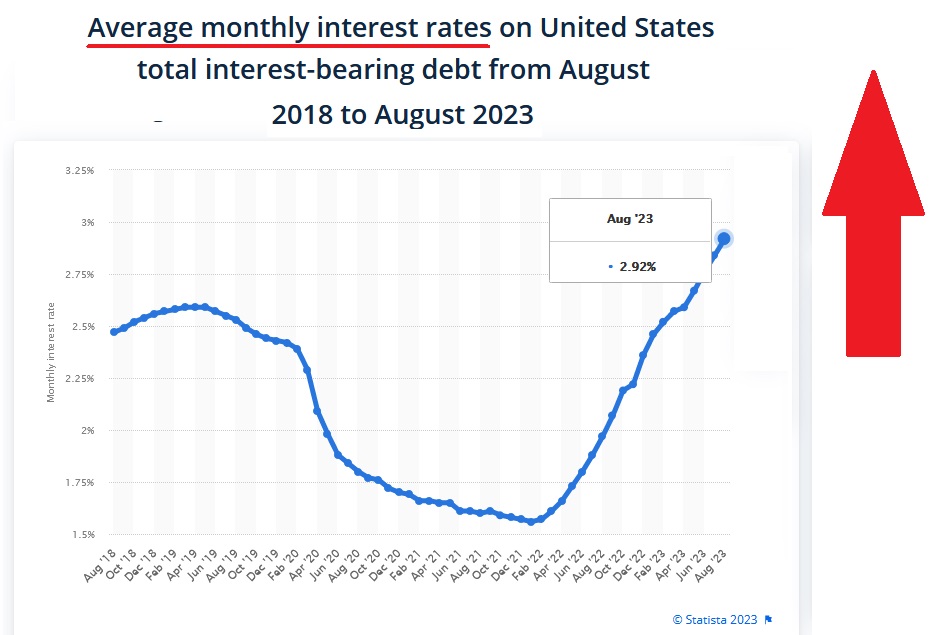

When short-term US rates were close to zero, and the 10-year Treasury dipped to 0.318% in early 2020, financing America’s debt was relatively cheap. Even with the 10-year Treasury was 2% or 2.5%, financing our debt was fairly inexpensive. But no longer. Take a look at the chart below:

The average monthly interest rate on US Treasury debt is skyrocketing. Averaging 2.92% just a couple of months ago, the average interest rate is up by almost 1.5% in just 1.5 years. Assuming rates do, in fact, stay “higher for longer” the average cost of US debt will go up … and up … and up, month after month. Consider this question:

How much does a 1% increase in US Treasury debt cost us in a year?

The answer: $330 billion. Remember, this is simply the annual increase to the interest cost. The Congressional Budget Office (CBO) is forecasting the US Treasury will pay about $750 billion of interest during fiscal 2024. During Fiscal 2024, the CBO is forecasting that the US Treasury will collect about $4.8 trillion … and pay out $3.8 trillion in “mandatory” payments and about $760 billion in “mandatory” interest. The math is simple: Mandatory payments and interest payment eat up almost 100% of all tax and other revenue collections. In addition, the CBO projects 2024 “discretionary” expenses of over $1.8 trillion.

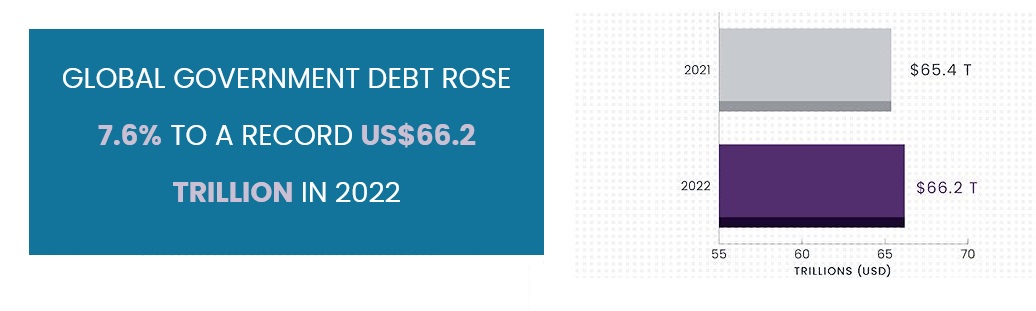

And we are not alone: Every developed nation has the same problem. A mountain of debt … and right now that debt is really expensive. According to Janus Henderson, a financial consultant, interest paid by all nations on sovereign debt reached almost $1.4 trillion in 2022. And the sovereign debt mountain increased considerably:

Reasonable questions might be these: In the face of such a staggering interest burden, why have the central banks raised rates so high? And why do they leave them there — “higher for longer” — forcing the average debt interest rate higher month-after-month, when every additional 1% rate increase cost these governments about an additional $700 billion each and every year.

Central banks would say their decisions are independent. Sure, high rates create a problem for US and other developed nations … but that’s not their problem.

Which brings us full circle to this essential, existential question:

Does the US spend too much … or are tax collections too low?

Ahhh … now we’re there. In my view, America’s financial sustainability is at risk. After decades of ignoring the underlying problems, it is now obvious the United States either spends too much, or takes in too little revenue, or both. There is no debate over this fact. In fiscal 2024, America is expected to spend about $6.4 trillion, according the CBO. Total collections are forecast at under $4.9 trillion. Add in the annual increasing interest burden and this deficit quickly gets out of control. Even worse, current conditions have created their own systemic negative feedback loop. In other words, the higher the interest rate, the larger the deficit; the larger the deficit, the greater the systemic risk, and bondholders thus demand a higher interest rate to compensate for the risk; and so on, and so on.

Can America grow out of the problem? Will a rapidly GDP help increase tax collections?

No and yes. GDP grew like a weed in the third quarter. According to the BEA, our American GDP increased by $560 billion, at the annualized rate, in Q3. That’s fabulous. However, as this increase is likely to add only about 18% of that amount in new tax collections — or about $100 billion — the deficit remains massive. This helps, but doesn’t solve the problem. But the other problem with higher interest rates is this: High rates are like a weighted blanket laying over the economy. It’s heavy. And over time, the weight alone will slow economic activity. The sale of big ticket items houses, cars, and refrigerators will slow. This is inevitable. It simply takes time. And over time, as deficits accrue and add to the growing mountain of debt, the interest burden grows larger and larger.

And thus, in years to come, far more than 100% of all Treasury tax and other collections will be spend on “mandatory” expenses and interest. Mandatory expenses are mandated by law. Interest payments are mandated by law. Only “discretionary” expenditures are, well, discretionary.

The bottom line: America needs to raise taxes to generate more income. Unless we change the laws and modify the amounts and methodologies of mandatory spending, I believe we need to increase tax collections. We can argue until the cows come home about whether or not we should cut mandatory spending in future years, but what we cannot argue about is this simple fact:

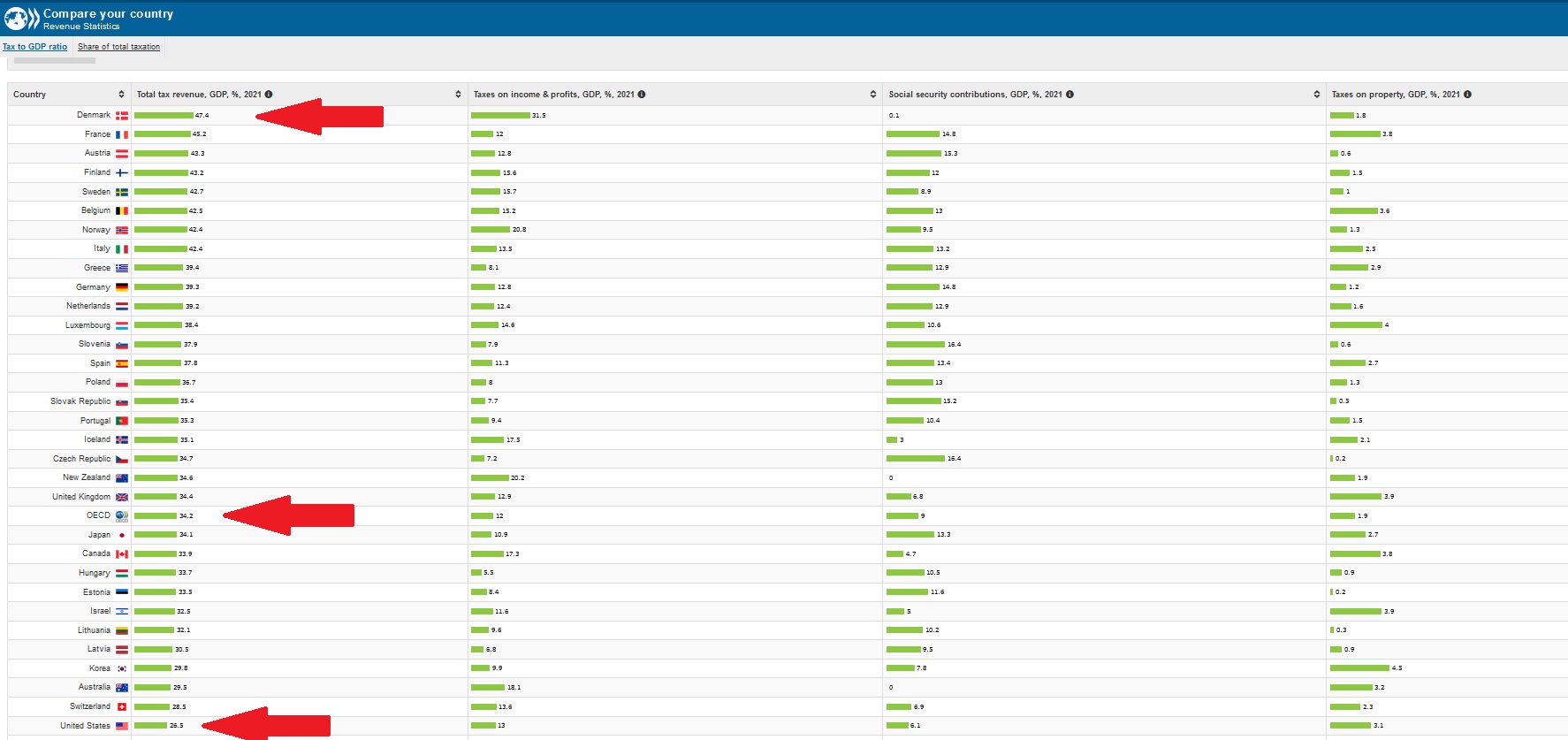

America has the smallest tax burden among all developed nations.

Yes, it’s true. In France, Austria, Italy, Denmark, Sweden … and the list goes on … their tax revenue collections are all north of 42% of GDP. What is that percentage here in the US? Only 26%. The OECD average tax collection rate, as you can see below, is 34.2% — more than 8% higher than the rate in the US. By how much would US tax collections increase with an 8% of GDP boost? More than $2 trillion … more than enough to eliminate the US deficit.

I know the image is small and hard to read. Feel free to go to the website and review the data there:

http://compareyourcountry.org/tax-revenues/en/

Of course, gaining an 8% of GDP tax boost overnight is patently unrealistic. Absurd even. But we need to begin to solve this problem somewhere. In my opinion, the US Treasury needs more income. We need to raise taxes. I know: Now EVERYONE hates me.

But if we plan to have an America for our children to enjoy, isn’t this the most important issue for the experts in Washington to resolve? It seems a far more important debate than which pronoun I wish to be known by.

America has danced around this issue for years … and now, in my opinion, it has now become existential.

The issue, I believe, is not whether or not to raise taxes … it is which taxes we should raise. We could debate this issue for days … so I’ll make it very simple. In my opinion, here is the tax that the United States should raise: The VAT.

Oh. Right. We don’t have one yet. We should get one. Every other developed nation in the world does. Every. Other. One. The United States does not. Yes, some states charge sales tax … other’s do not. But we do not have a national VAT. According to KPMG, over 14o countries across the globe have a VAT.

America does not. America has a massive deficit problem. The majority of developed nations does not. And consider this benefit: The VAT is a tax everyone in America will hate! No one likes the VAT … but it does help pay for the massive social safety nets all developed nations have built for their citizens.

I’ll end here. Hate the message … but don’t hate the messenger. 🙂

To the steakhouses!

As mentioned above, earlier this morning, we got the ‘preliminary’ reading for Q3, 2023 GDP: Real gross domestic product (GDP) increased at an annual rate of 4.9 percent in the third quarter of 2023 (table 1), according to the “advance” estimate released by the Bureau of Economic Analysis. Current dollar GDP increased 8.5 percent at an annual rate, or $560.5 billion, in the third quarter to a level of $27.62 trillion.

What an amazing economic performance. One I fear will not repeat anytime soon. No, expect our expansion to continue … only at a slower rate. Time will tell, but I believe the SHI is predicting a slower paced economy … and I agree.

Oh, by the way, my next blog post will be almost a month from now – on November 22nd. Why? Long story. I’ll tell you then. 🙂

Thanks for tuning in.

<:> Terry Liebman