SHI 10.26.22 – The Fast, The Slow, and The Downright Sloth-Like

SHI 10.5.22 – Chaos in the Kitchen

October 7, 2022

SHI 11.2.22 — May You Live In Interesting Times (Part 6)

November 2, 2022

Central banks spent most of last year telling us inflation would fade. Quickly.

No longer. That message is as dead as Ye’s deal with Adidas.

33 of the 38 central banks monitored by the Bank for International Settlements (BIS) have raised interest rates in 2022. That equates to 87%. As a result, short-term interest rates across the globe have skyrocketed when compared to 2021. What impacts has this coordinated move had on the US and global economies? Which “parts” were quickly impacted by the rate hikes; which segments will respond slower; and, where will the impact be almost invisible?

“

How do increased rates impact the economy?”

“

How do increased rates impact the economy?”

It’s an interesting question. The answer to the “fast” part is easy: Housing and mortgages. Housing sales plummeted. Mortgage rates skyrocketed — at last count, 30-year fixed rates had climbed over 7%. There’s your “fast” part. The balance of the answer, as you’ll see below, is a bit more complex.

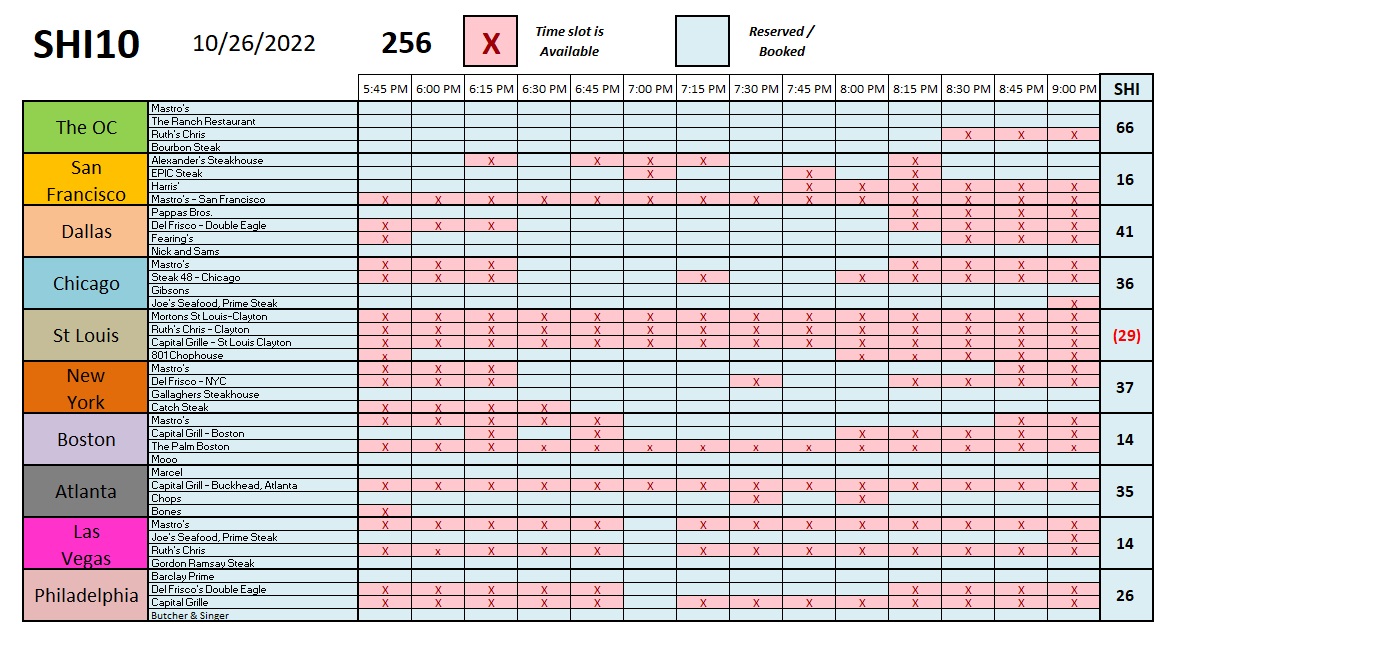

Welcome to this week’s Steak House Index update.

If you are new to my blog, or you need a refresher on the SHI10, or its objective and methodology, I suggest you open and read the original BLOG: https://www.steakhouseindex.com/move-over-big-mac-index-here-comes-the-steak-house-index/

Why You Should Care: The US economy and US dollar are the bedrock of the world’s economy.

But is the US economy expanding or contracting?

Expanding. Sort of. At the end of Q2, 2022, in ‘current-dollar’ terms, US annual economic output rose to $24.85 trillion. Yes, during Q1, the current-dollar GDP increased at the annualized rate of 7.8%. The world’s annual GDP rose to about $95 trillion at the end of 2021. America’s GDP remains around 25% of all global GDP. Collectively, the US, the euro zone, and China still generate about 70% of the global economic output. These are the 3 big, global players.

The objective of this blog is singular.

It attempts to predict the direction of our GDP ahead of official economic releases. Historically, ‘personal consumption expenditures,’ or PCE, has been the largest component of US GDP growth — typically about 2/3 of all GDP growth. In fact, the majority of all GDP increases (or declines) usually results from (increases or decreases in) consumer spending. Consumer spending is clearly a critical financial metric. In all likelihood, the most important financial metric. The Steak House Index focuses right here … on the “consumer spending” metric. I intend the SHI10 is to be predictive, anticipating where the economy is going – not where it’s been.

Taking action: Keep up with this weekly BLOG update. Not only will we cover the SHI and SHI10, but we’ll explore “fun” items of economic importance. Hopefully you find the discussion fun, too.

If the SHI10 index moves appreciably -– either showing massive improvement or significant declines –- indicating growing economic strength or a potential recession, we’ll discuss possible actions at that time.

The Blog:

I just returned from about a 2-week trip to the east coast. Of course, the entire trip was focused on the Steak House Index. Field work. For you. My dedicated readers. You’re just gonna have to trust me on this. 🙂

For example, in Boston, I visited the typically booked SHI steakhouse, ‘Mooo‘ in the Beacon Hill area. I made the reservations many weeks before traveling to Boston; you’ll recall from the SHI grid (below) that Mooo is almost always fully booked. I wanted to see what all the hype was about.

So let me start here. I have to say, Mooo is one of the best steakhouses I’ve had the pleasure of enjoying in many years. Sure, their wine list was exemplary; but more importantly, their menu choices were plentiful and opulent. The food was perfectly prepared. Even the prices were reasonable, for a steakhouse of its level and elegance. The evening was a complete success. I can see why they are consistently fully booked for Saturday when I survey the SHI steakhouses Wednesday mornings at 11 AM.

But as you know, this is an economic blog. I am not a restaurant critic. Alas. Beyond my praise above, what struck me was this: I was at Mooo on a week-night — not a Saturday. And the place was packed. To the gills. Not one table was vacant while we were there … until later in the evening. Home values and mortgages may have been quickly and adversely impacted by the FED‘s interest rate increases but 6-months into one of the fastest FED rate-hike cycles in history, Mooo is doing just fine.

Home sales, home values and mortgage rates were all immediately impacted by the large and quick FED rate increases. The same scenario is unfolding in all developed countries where their central bank is increasing interest rates at unprecedented speeds. And in countries where most home loans are variable-rate loans, home values are actually falling — in some countries, by a significant amount. Here in the US, the majority of home loans are fixed rate loans. Are home values “softening” here in the US too? Sure, but not in all geographic markets. Today more than any time in the recent past, location matters. Current statistics show the extent of the pain:

<> New home sales fell 11% M-O-M in September (from August).

<> According to Freddie Mac, the “average” 30-year mortgage rate today is 7.16%

<> Refinance demand is down 86%.

<> Home-buyer demand for a mortgage is down 42%.

Big moves over just a few months. The FED — and other central banks — should be proud: They have done what the markets could not do. They have effectively ended the “multiple-offer” scenario playing out in housing markets across the country, and they silenced the home sales and mortgage industries. Was that their intent? Yes. It was. If any marketplace was out of balance, it was the single-family home market. The post-Covid ‘irrational exuberance’ in housing has been a global phenomenon. Central bankers had to slow or stop this run-away freight train. They had to slow home value appreciation across the globe. The fight against inflation offered central banks a great opportunity to kill two birds with one stone, as the old expression goes. By their actions, they are able to talk tough on inflation and, at the same time, take the froth out of the housing markets. For central banks, this is a win-win scenario.

So, in the “Fast” category, we have home sales, home values, and mortgage rates. And P/E ratios too! Higher interest rates have the immediate effect of reducing P/E ratios. And bond values. Frankly, just about any financial instrument with a yield has been impacted. As short-term rates rapidly increased, the value of these assets quickly moved in the opposite direction. Which, again, was precisely what the FED was hoping to do: Take some froth out of the stock, bond, commercial real estate and “alternative” asset markets. As P/E ratios fall, so do stock prices. Everyone with a 401K has experienced this personally.

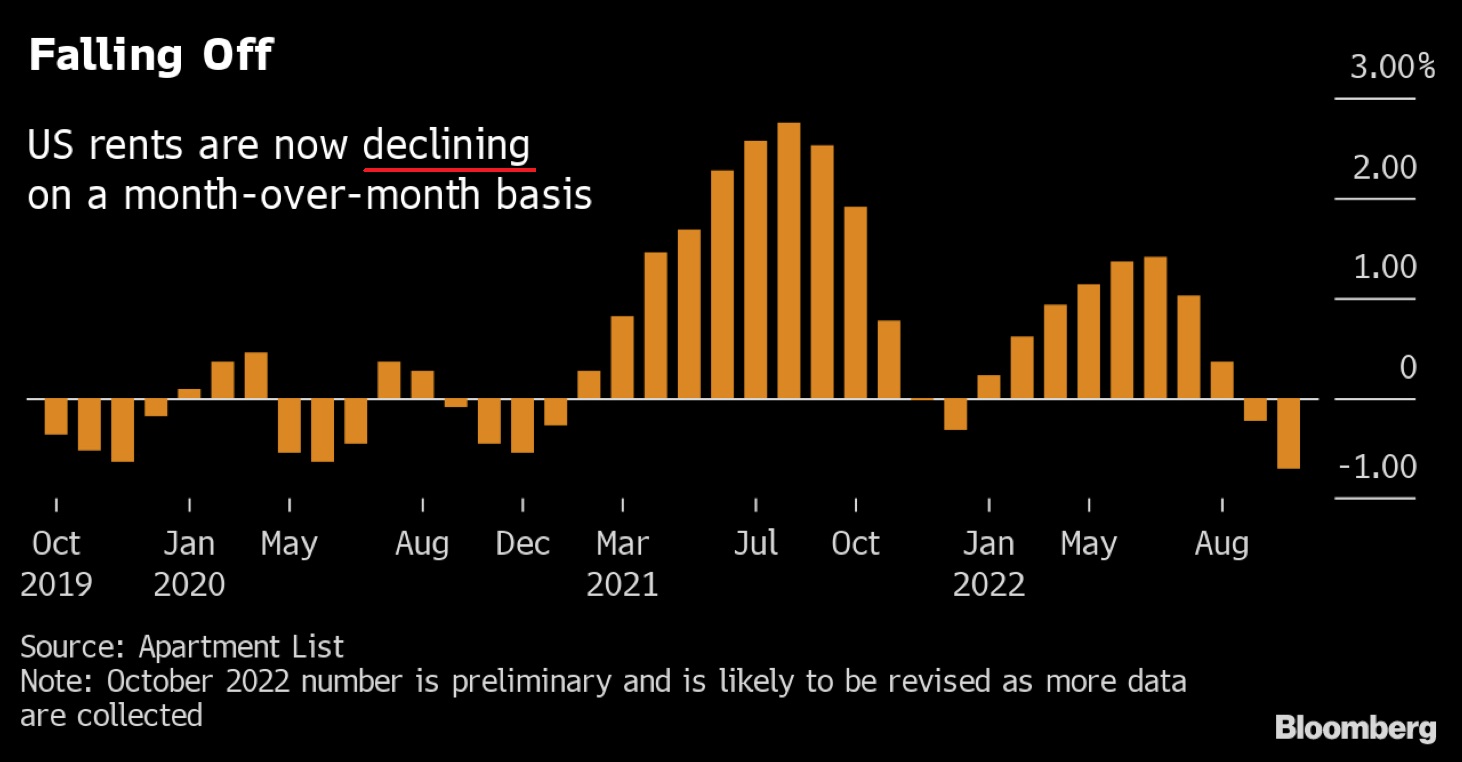

Apartment rental rates have shot to the moon and beyond in recent years. Check out the monthly data below:

As the headline says, apartment rents now appear to be declining month over month (M-O-M). Perhaps. The trend in the chart above is certainly down, down, down. But we have to keep in mind the same thing happened in Q4 of 2019, 2020, and 2021 (see chart). So is this a seasonal trend, or part of a larger change in the direction of rental rates? Time will tell. It’s too early to know now.

But there’s no doubt home prices are under pressure. Even here in the US. According to the “S&P CoreLogic Case-Shiller National Home Price Index” — that’s a mouthful — average home prices in major cities fell by 1.1% during August over July. This is the second M-O-M decline. This is the first 2-consecutive month decline in over 10 years.

The bottom line: The rapid, sizable FED rate increases have quickly turned around housing. At best, average price increases are flat. Worst case, home values in some locations are falling. Will this trend continue? It depends on the FED. Will they continue to raise rates? Probably. We’ll know a week from today. The futures market recently reduced the odds of another 75 basis point hike from 75% down to 45%. Regardless, while we may not see a 75 bp hike, I feel it’s a lock right now for a 50 basis point increase. I don’t believe the FED is done raising rates. Not yet. But the next increase may be the last increase we see for a while.

It’s worth noting that the central bank of Canada unexpectedly raised their interest rates by only 50 basis points earlier today. Back in July they had raised rates by a full percentage point. Not today. Today they slowed the increases to only 1/2 a percent. Canada’s policy shift suggests that central banks around the world might be closer to the end of the tightening cycle. Might. We’ll see.

OK, what’s in that “Slow” bucket? Which areas of the economy react slower to FED rate increases?

Expensive eateries, apparently. Clearly the crowd at Mooo isn’t reacting to FED rate hikes. By my personal experience, they were all having a wonderful time, spending gobs of money. But this is not to say that Mooo won’t eventually be impacted by the FEDs actions. They might. If and when the FEDs actions significantly increase unemployment, Mooo will be impacted. But, for now, Mooo is doing just fine.

Consumer spending is holding up fine, too. But like expensive eateries, consumer spending will be more directly impacted by increases in unemployment. Remember that each 1% increase in unemployment puts about 1.6 million people out of work. You’ve heard that old joke: What’s the difference between a recession and a depression? A recession is when your best friend loses his job … a depression is when you do. 🙂

Unemployment increases will certainly adversely affect consumer spending. But until rate increases filter thru the economy, causing layoffs and job losses, the consumer will probably keep spending. Apparently, we’re already seeing rate impact on computer chip sales. Just months ago, chips were in short supply. Today, we apparently have a glut. Who knows. But recent political decisions and supply chains probably play a roll. Either way, the rate increases will impact these segments, but it will be a much slower response. In fact, there are numerous well know economic publications that suggest the lag time from tightening to economic slow-down can be as long as 2 to 3 years. Yikes.

Mondelez is the company that makes Oreos, an American treasure! And Ritz crackers! Another treasure! On the other hand, they also produce ‘Sour Patch Kids’ candy. Yuck. Mondelez sells their products in about 150 countries around the world and has “operations” is more than 80. In a world with about 190 countries in total, these are impressive numbers. Annual revenues are almost $30 billion. So if you want to talk “global supply chains,” talk to Mondelez. Which is precisely what the Wall Street Journal did. Sandra MacQuillan is the “chief supply-chain” officer for Mondelez. In her words:

“We’ve never seen inflation like this. We’ve never seen disruption like this, certainly all the time that I’ve worked. We’re dealing with all sorts of shortages, all sorts of economic hits that you need to be agile and flexible in managing.”

and …

“We’re still fragile. We’ve had Covid. Covid is still going on, but we’ve had the aftermath of Covid, with people making choices in terms of where they want to work and how they want to live their lives. Some of them have decided not to work, particularly people that we would like to keep, women and diverse groups. We’ve now got inflation. Suppliers can only do so much before they have to push it through (to their customers) like we have with pricing.”

Interesting.

What about those sloths? Sloths are exceptionally slow-moving animals. They react to the outside world … but very, v e r y , slowly. If at all.

In the sloth category, we have oil, gasoline, and commercial R/E capitalization rates. Will FED rate hikes impact oil/gas prices? Naaaa. Well, maybe: to the extent that the “Slow” group begin to painfully adjust to the higher rates, and the unemployment rate moves appreciably higher, thereby pushing the world economy into recession, the demand for petroleum products will decline. And, in response, oil prices may decline. But any suggestion that oil prices are highly correlated with interest rate levels or moves is simply inaccurate.

Commercial real estate capitalization rates (“cap rates”) are more interesting. On one hand, one might expect that interest rate increases would immediately raise cap rates. After all, what are cap rates but essentially the cash-on-cash ROI an investor can expect from a commercial real estate investment. If yields on alternative investment choices — such as a 10-year Treasury — are up significantly one could logically expect cap rates to increase as well. But so far, we’ve seen little, if any, reaction. I suspect this muted response is more related to the short-duration of the rate hikes. If rates stay high for a longer period of time, I suspect cap rates will eventually generally move higher. But if the FED rate increase cycle ends with this next move, cap rates may remain entrenched. Again, time will tell. Regardless, cap rates are in the sloth camp. 🙂

OK, shall we see how the steakhouses are holding up this week?

Just fine is the answer. And once again, Mooo in Boston is fully booked for this coming Saturday. Until about 9:45 pm, anyway. Amazing.

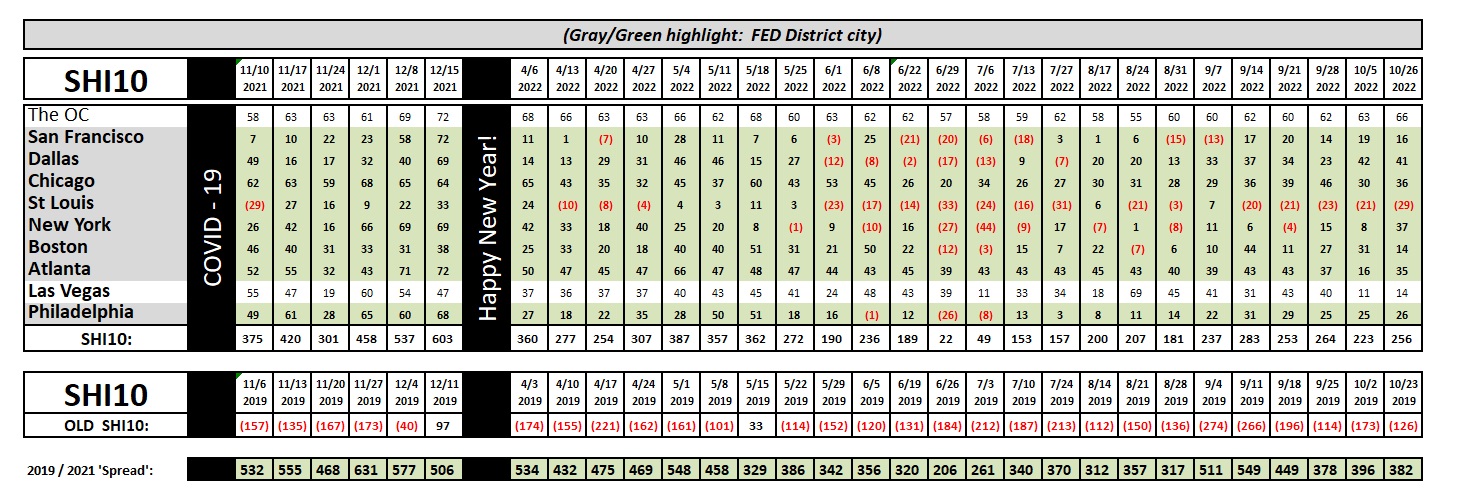

Here’s the longer term trend chart:

Steady as a rock. Opulent eateries in St Louis continue to struggle, week after week, but every other SHI market seems to be holding up just fine. Reservation demand even improved meaningfully in Chicago and Atlanta. Using our SHI as an alternative metric to measure US consumer spending, and by extension, our GDP as a whole, the economy looks steady to me. On the other hand, I have no doubt FED rate increases will eventually cause unemployment increases, adversely impacting everything. But like our sloth crossing the road in today’s blog image header, this might take a while.

<:> Terry Liebman