SHI 11.2.22 — May You Live In Interesting Times (Part 6)

SHI 10.26.22 – The Fast, The Slow, and The Downright Sloth-Like

October 26, 2022

SHI 11.9.22 — Be Happy You You Didn’t Buy This.

November 9, 2022

Yes, I know. I’ve used that ‘title’ many times before.

But come on! Economically speaking, these are “crazy times!”

In addition to our nutty employment marketplace, consider this:

Real GDP grew in Q3! That’s right — it went up! Did you notice? Probably not. Why not?

Well, probably for a few reasons. First, the BEA report on Q3 GDP came out the day after my last blog. Second, there’s been so much hand-wringing, worrying and whining over FED rate hikes, the collapse in home sales, and stock market losses, every other economic data point seems to have been pushed to the sidelines, unobserved. So let me repeat:

Real GDP grew in Q3!

That’s right! After two consecutive down quarters, real GDP actually increased in Q3. Significantly. The annualized rate of real GDP growth was 2.6%. Crazy, right?

“

GDP expanded by 2.6% annualized in Q3.”

“

GDP expanded by 2.6% annualized in Q3.”

What’s more, the ‘current dollar’ — or nominal — GDP grew by another $414.8 billion during Q3. Our American GDP (again, current dollar) is now running at the annual clip of $25.66 trillion! Further, while ‘real’ GDP fell during both Q1 and Q2, nominal GDP has grown significantly. Consider this: Q4, 2021 ‘nominal’ GDP was $24.349 trillion. The current run-rate is $25.66 trillion. Which means …

Nominal GDP growth has exceeded $1.31 trillion in 2022!

Where is that recession economists have been promising us? 🙂

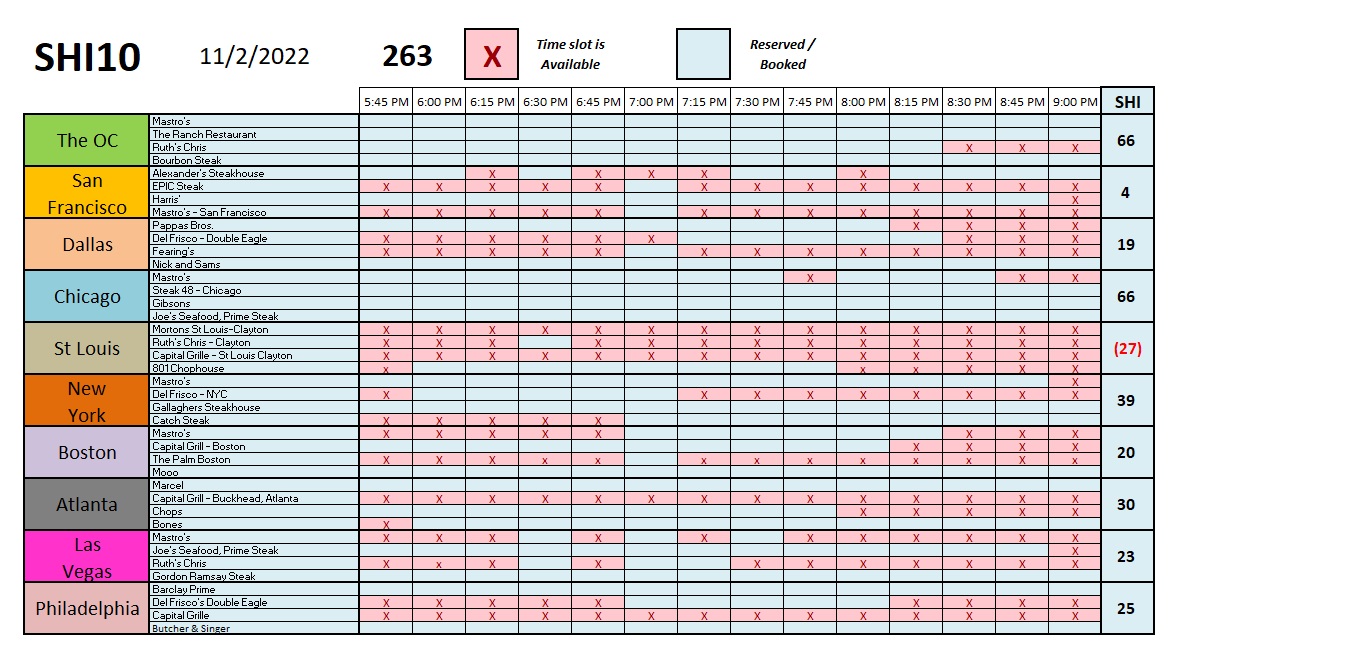

Welcome to this week’s Steak House Index update.

If you are new to my blog, or you need a refresher on the SHI10, or its objective and methodology, I suggest you open and read the original BLOG: https://www.steakhouseindex.com/move-over-big-mac-index-here-comes-the-steak-house-index/

Why You Should Care: The US economy and US dollar are the bedrock of the world’s economy.

But is the US economy expanding or contracting?

Expanding. At the end of Q3, 2022, in ‘current-dollar’ terms, US annual economic output rose to $25.66 trillion. So far this year, America’s current-dollar GDP has increased at an annualized rate exceeding 7.1%. The world’s annual GDP rose to about $95 trillion at the end of 2021. America’s GDP remains around 25% of all global GDP. Collectively, the US, the euro zone, and China still generate about 70% of the global economic output. These are the 3 big, global players.

The objective of this blog is singular.

It attempts to predict the direction of our GDP ahead of official economic releases. Historically, ‘personal consumption expenditures,’ or PCE, has been the largest component of US GDP growth — typically about 2/3 of all GDP growth. In fact, the majority of all GDP increases (or declines) usually results from (increases or decreases in) consumer spending. Consumer spending is clearly a critical financial metric. In all likelihood, the most important financial metric. The Steak House Index focuses right here … on the “consumer spending” metric. I intend the SHI10 is to be predictive, anticipating where the economy is going – not where it’s been.

Taking action: Keep up with this weekly BLOG update. Not only will we cover the SHI and SHI10, but we’ll explore “fun” items of economic importance. Hopefully you find the discussion fun, too.

If the SHI10 index moves appreciably -– either showing massive improvement or significant declines –- indicating growing economic strength or a potential recession, we’ll discuss possible actions at that time.

The Blog:

Are you familiar with John Cochrane? He is an accomplished macroeconomist and publishes his own blog titled “The Grumpy Economist.” Funny. I mean, how can he — exclusively — claim that title? Aren’t all economists grumpy? 🙂

Well, maybe not me. But, alternatively, I’m not classically trained.

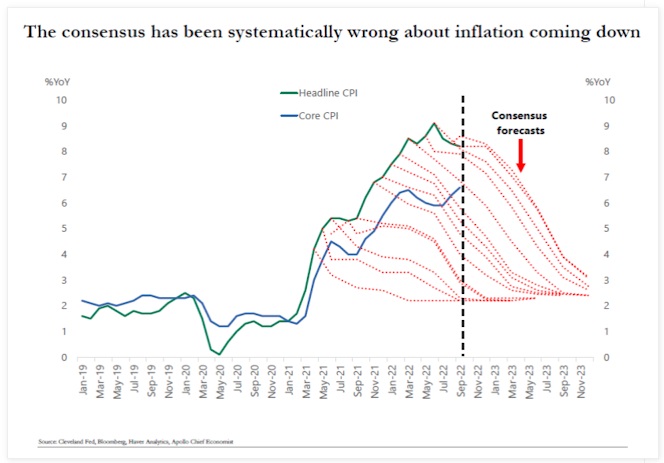

Anyway, in his blog, John shared this chart:

This is an impressive demonstration of the statistical theory of “reversion to the mean” — and it shows just how wrong “the consensus” has been for well over a year on this topic. The consensus is simply an aggregate of experts and their forecasts. Why have they been so wrong?

Well, the answer depends on who you ask … especially today, as the November mid-term elections loom large. Both political parties are quick to blame the other for the current bout of inflation. Their opinions are clear. So as I often do, I will share recent comments from The Economist magazine, a typically somewhat centrist financial publication. Before I do, I ask that you please remember mine is an economic blog and not a political commentary … so here goes:

“In July economists with the Federal Reserve estimated that fiscal policy had added about 2.5 percentage points to America’s annual inflation rate. In other words, nearly half of America’s “extra” inflation, relative to its pre-pandemic norm, is attributable to the government’s profligacy.”

The Economist article is not complimentary of either Biden or Trump … and suggests the $3 trillion in economic stimulus during Covid from the Trump administration, when combined with the March 2021 ‘American Rescue Plan’ with $1.9 trillion of stimulus from the Biden administration, are responsible for much of the inflationary spurt we’re now experiencing.

Perhaps. Perhaps like the proverbial ‘pig-in-the-python’ this fiscal largess, and the resulting consumer spending spikes, simply needs to work its way thru the system. This seems to be what “the consensus” is saying in the chart above. They have simply all be wrong about how long that process will take. Because once that the majority of money is spent, if it ends there, won’t the economy re-adjust on its own, thereby reverting to the mean so to speak? If fiscal stimulus ends, doesn’t that suggest normalcy will return?

On a corollary, is this almost $5 trillion also responsible for the sizable nominal GDP increases during 2021 and 2022? After all, nominal GDP increased over $2.3 trillion during that time-frame. Probably.

Again, the answer to the “pig” question is perhaps. It’s really hard to tell, today, how much of different the post-pandemic economic world really is. Which brings us full circle back to Professor Cochrane. A little off topic, here’s a chart from his blog I found interesting:

Anyway, Professor Cochrane has written an exceptionally dense economic textbook called, “The Fiscal Theory of the Price Level.” No I don’t recommend you read it. Frankly, I probably won’t. Especially after reading this (right click, open in new page):

https://johnhcochrane.blogspot.com/2022/08/the-fiscal-theory-of-inflation.html

You get the point. 🙂

Cochran also edited a book to be published in February of 2023, entitled, “How Monetary Policy Got Behind the Curve — and How to get Back” from which excerpts are available. In that book, Cochran also emphasizes the the “initial cause of our current inflation” was a “fiscal shock” from the almost $5 trillion of treasury borrowing … and further, that while higher interest rates might “end inflation,” monetary policy alone cannot “durably lower inflation. Only a joint monetary, fiscal, and growth-oriented microeconomic reform will do so.”

OK, let me translate.

FED rate hikes, alone, cannot solve the long-term inflation issue. They can moderate the inflation rate in the short-run. But over longer periods of time, inflation rates will be more broadly impacted by the size of fiscal deficits. Per Cochrane, the larger the deficit over time, the higher the inflation rate.

Let me finish with this comment: Theories are theories until they are thoroughly tested. Neither “Modern Monetary Theory” nor Cochrane’s opposite view have been tested. You can argue fiscal and monetary policy, post-Covid, have “proven” that MMT causes inflation — which I have argued in prior posts — but neither theory has been deeply tested. My opinion, however, remains firmly in the camp that money supply growth far in excess of GDP growth, which suggests excessive levels of fiscal borrowing and deficits, does create excessive levels of inflation. Again, my opinion. 🙂

Let’s see what the steakhouses are telling us about our economy this week.

This weeks SHI10 is very consistent with prior readings. Once again, MOOO (Boston) is fully booked this Saturday next, and reservations at the steakhouses in Atlanta are much stronger this week. Reservation demand in Chicago saw a HUGE increase … I have no idea why. Dallas saw a dip. But overall, this weeks reading was, in the aggregate, unchanged week over week.

Here’s the trend report.

OK, let me move on to today’s FED decision. As you probably know, the funds rate was increased by .75%. Short term rates are now about 4%. The FEDs statement, released along with the rate increase, said “… the Committee will continue to monitor the implications of incoming information for the economic outlook. The Committee would be prepared to adjust the stance of monetary policy as appropriate if risks emerge that could impede the attainment of the Committee’s goals. The Committee’s assessments will take into account a wide range of information, including readings on public health, labor market conditions, inflation pressures and inflation expectations, and financial and international developments.”

In the press conference, Powell remains resolute and did suggest more rate increases are coming … but the statement above, at least, suggests they will be “data driven” in their decisions.

It wasn’t that long ago that Powell said something like “we’re not even thinking about thinking about raising interest rates.” Today, essentially, Powell uttered a similar thing: The FED is not even thinking about thinking about pausing interest rate hikes. It’s important to keep in mind that just as the first statement proved completely untrue, the second may also prove false as well. They may not be thinking about thinking about pausing … but perhaps developing housing data between now and December may change their mind.

Interesting times indeed.

<:> Terry Liebman