SHI 11.9.22 — Be Happy You You Didn’t Buy This.

SHI 11.2.22 — May You Live In Interesting Times (Part 6)

November 2, 2022

SHI 11.16.22 – Shrinkonomics

November 16, 2022

Isn’t that pretty? That’s a photo of the Austrian Alps.

The photo, courtesy of Bloomberg, is very appropriate for two reasons. First, ski season is here! With this first major California snowfall, Mammoth opened … and the 2022 Farmers Almanac forecasts Colorado will be in a “hibernation zone” that’ll be both “glacial” and “snow-filled.” Brrrr….I’m cold just thinking about it! Let’s hit the slopes!

But, alas, once again this is an economic blog … and thus the Austrian Alps hold fascination for another reason: A couple of years ago, the country of Austria sold 100-year-duration sovereign bonds. That’s right, they are “due” in the year 2120. Try holding that baby to maturity!

“

Psssst. Anyone want a 100-year bond?”

“

Psssst. Anyone want a 100-year bond?”

Impossible. It would be hard enough to hold a 10-year Treasury to maturity … let alone a 100-year bond. Let me think … in 2120, I’ll be … hold on … carry the 1 … yep, I’ll be really, really old. Probably too old to cash in that bond. I probably couldn’t even lift it. So I’ll pass. Hey, that reminds me of a joke!

A rather old man was sitting quietly on his favorite bench, in his favorite lush and over-grown park, enjoying the sights and sounds of nature when a large frog near his feet whispered loudly, “Hey buddy! Yeah, down here! I know I look like a frog … but I’m actually a powerful genie … and if you kiss me and free me from this terrible spell cast upon me, I’ll grant you three wishes … you can have anything you’ve always wanted … wealth, power, the mansion of your dreams … anything! Whadda ya say?” The man looked at the frog, thought for a few moments, and then reached down, picked up the frog, and put it into his coat pocket. The frog loudly exclaimed, “Hey! You’re supposed to kiss me … and then you get your 3 wishes!” To which the old man replied, “No thanks. At my age, I’d rather have a talking frog.” 🙂

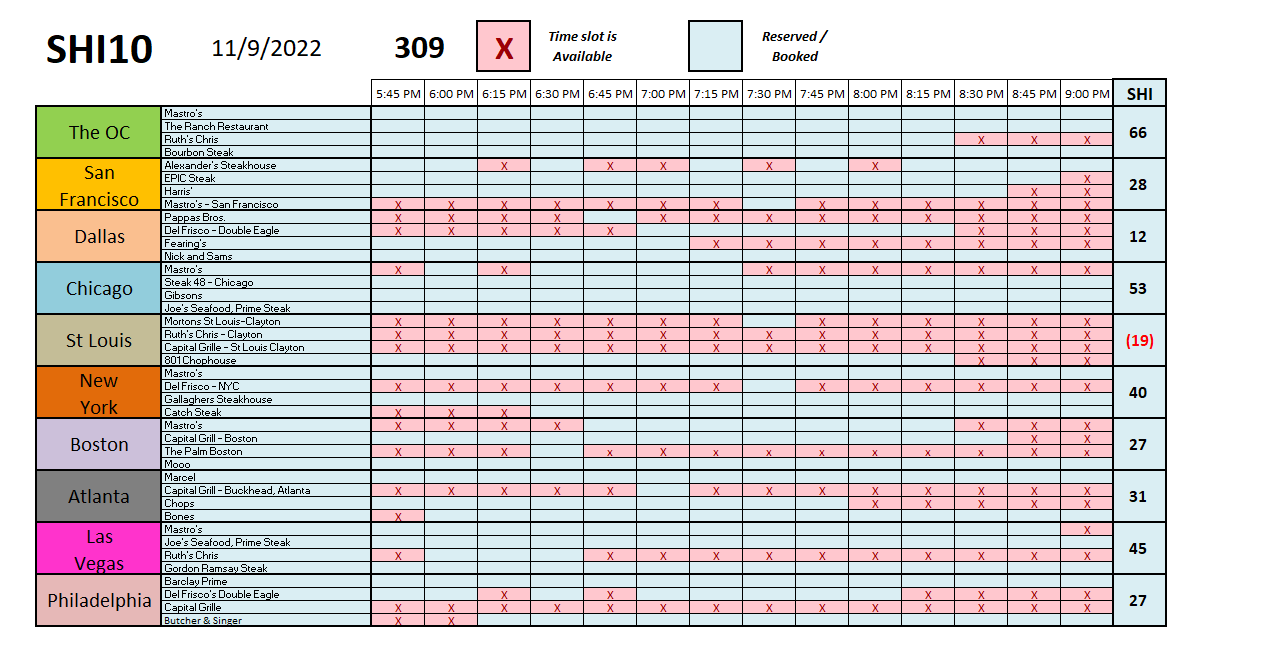

Welcome to this week’s Steak House Index update.

If you are new to my blog, or you need a refresher on the SHI10, or its objective and methodology, I suggest you open and read the original BLOG: https://www.steakhouseindex.com/move-over-big-mac-index-here-comes-the-steak-house-index/

Why You Should Care: The US economy and US dollar are the bedrock of the world’s economy.

But is the US economy expanding or contracting?

Expanding. At the end of Q3, 2022, in ‘current-dollar’ terms, US annual economic output rose to $25.66 trillion. So far this year, America’s current-dollar GDP has increased at an annualized rate exceeding 7.1%. The world’s annual GDP rose to about $95 trillion at the end of 2021. America’s GDP remains around 25% of all global GDP. Collectively, the US, the euro zone, and China still generate about 70% of the global economic output. These are the 3 big, global players.

The objective of this blog is singular.

It attempts to predict the direction of our GDP ahead of official economic releases. Historically, ‘personal consumption expenditures,’ or PCE, has been the largest component of US GDP growth — typically about 2/3 of all GDP growth. In fact, the majority of all GDP increases (or declines) usually results from (increases or decreases in) consumer spending. Consumer spending is clearly a critical financial metric. In all likelihood, the most important financial metric. The Steak House Index focuses right here … on the “consumer spending” metric. I intend the SHI10 is to be predictive, anticipating where the economy is going – not where it’s been.

Taking action: Keep up with this weekly BLOG update. Not only will we cover the SHI and SHI10, but we’ll explore “fun” items of economic importance. Hopefully you find the discussion fun, too.

If the SHI10 index moves appreciably -– either showing massive improvement or significant declines –- indicating growing economic strength or a potential recession, we’ll discuss possible actions at that time.

The Blog:

Once again, I digress. I apologize. But, hey, who doesn’t love frogs?

Back to Austria. For the second time in recent memory, Austria sold “Century Bonds” — sovereign bonds with a 100-year maturity — in June of 2020. While the bond issue was only 2 billion euro, they were significantly oversubscribed. Austria received orders for about 16 billion euro! Which might cause you to think the yield must have been fantastic, right? After all, investors would be tying up their hard-earned cash for 100 years. I imagine the yield must have been eye-popping! And it was !!!

Eye-poppingly bad, I mean. The investors who bought that 100-year beauty lent their hard-earned cash to Austria for 100 years at the paltry interest rate of 0.88%. Per year. That’s right. Less than even one percent. Now that interest rates have skyrocketed at the hands of the FED and other central banks, are you curious what that $2 billion euro bond is worth today? In other words, suppose the investor(s) wanted to sell that bond today, in the open market. What would they realize from the sale? Well, that $2 billion euro Austrian sovereign bond, today, is worth only $900 million euro today. That’s right, the value of that bond is down 55% from its sale price only about 2 years ago. I’m sure those other folks — the 14 billion euro “oversubscribers” — are happy they didn’t buy that!

I’ve written extensively on this issue over the years. You may remember this blog post (right click, open in a new tab.)

https://steakhouseindex.com/shi-3-3-21-staying-positive-in-a-negative-world/

At the time, you may recall, 0.88% was quite a princely sum when compared to the negative yields on many sovereign bonds. Discussing cash you might have in your bank account in Europe, quoting myself from that blog:

” … not only does the bank pay you NO interest, but you cannot deposit your money with the bank without cost. The bank charges you 3/4 of a percent to simply deposit your money into the bank! By comparison, your mattress is looking pretty good!

Consider this: one year later … that mythical $50K you deposited in the bank? Your account balance is now $49,625. What a great deal! Well, for the bank maybe. Not for you.

For all of human history, banks and “lenders” have been profitable charging their borrowers interest. Not today. Not in Denmark. Today, some banks pay borrowers to borrow money! And since the bank charges no interest, they must charge their depositors a “fee” for “safely storing” their cash. And that’s what’s happening in Denmark today.

And in Germany, too. Germans are prolific savers. In fact, 30% of all savings in the eurozone are from German citizens — over $3 trillion in total.

Germany’s biggest lenders, Deutsche Bank and Commerzbank, have required new customers since 2020 to pay a 0.5% annual rate to keep large sums of money with them. The banks say they can no longer absorb the negative interest rates the European Central Bank charges them. According to price-comparison portal Verivox, 237 German banks now charge “negative interest rates” to private customers, up from 57 before the pandemic hit in March of last year. Charges range between 0.4% and 0.6% for deposits beginning anywhere from €25,000 to €100,000. The charge for bank deposits is higher in Switzerland. There, you will pay the same as in Denmark: 0.75% per year.

Insanity redux. The world of finance is upside down.

The ‘official’ interest rate in Denmark is 0.05%. In Switzerland? Negative <0.75%>. Denmark and Switzerland have lived with negative interest rates since January of 2015. The Swiss 10-year bond currently yields a negative <.269%>. Denmark’s is a negative <.17%>. And, at least for now, these ultra-low and negative rates are here to stay.”

Insanity indeed. And yet trillions of dollars were “invested” into negative yielding securities.

No longer.

For now, and perhaps for many years to come, interest rates around the world are very much positive. But this is brand new — post-FED rate increases.

Why did seemingly intelligent people buy negative yielding bonds and exceptionally long-duration bonds with paltry, diminutive positive yields? Probably because they were advised to do so. Did they get bad advice? No. The advice was neither good or bad. It was simply advice. My suspicion: Hundreds of finance “experts” around the globe advised their clients to buy those bonds for reasons that seemed to make sense at that time. At that time, according to the experts, the decision was sound. Of course, if you’ve read my blog for the past 4 or 5 years, you know that I’ve been advising quite the opposite: Run, don’t walk, as fast as you can from negative yielding bonds, I advised for years. Why? Because I believed the day or reckoning would come … the day when longer-duration bonds at very low rates would lose significant value. I was right. The “experts” were wrong.

And therein lies the point. Expert advice is neither good nor bad. It is simply the best advice a well-intentioned, competent, knowledgeable, experienced “source” has at that moment. But at the end of the day, expert advice is still just an opinion. Consider this opinion about the future, published on the first day of January, 2022, from a behemoth expert, one I follow closely and consider to be quite skilled:

About 10-months ago, as 2022 began, these experts forecasted S&P earnings growth as high as 14% this year, and a total-year return between 7 – 10%.

The year is not over yet, so their prediction could still come true. However, it’s doubtful, given current state.

When the FED rapidly changed the “rules of the game” early in the year, the investment landscape changed quickly and drastically. Very quickly, the same experts shifted their forecasts from significant real GDP growth to the opposite — a recession — possibly in early 2023. And that’s the source of the problem: Future-looking forecasts are often heavily reliant on past-data. The longer the duration of a prior trend, the more durable economic and financial forecasters believe it will be in the future. Every forecaster struggles with this.

Not only does JPM’s January 2022 forecast now look very wrong, but so do hundreds if not thousands of other expert forecasts that suggested investors buy trillions of dollars in long-dated maturity bonds at generational-low yields. Be happy you didn’t buy those bonds either.

And that brings us to the point, my friends. The point is this: Gather all the expert advice you can get. Investment or otherwise. Cast a wide net. Listen to everyone. Including me.

But when making your final decision, you should listen to only one voice: Yours. Make your own decision. Time will prove your decision right or wrong … but either way, it will be your decision, one that you made with as much excellent and expert advice you could have accumulated at the time. That’s the best advice I can give you. 🙂

To the steakhouses!

Well, this week’s SHI10 is above 300 once again! Could this mean our economy is actually expanding, at the same time it faces the interest-rate onslaught from the FED? Sure! Anything’s possible, as we saw today with the continued melt-down in the price of the FTX cryptocurrency token. Be happy you didn’t buy that one, either. 🙂

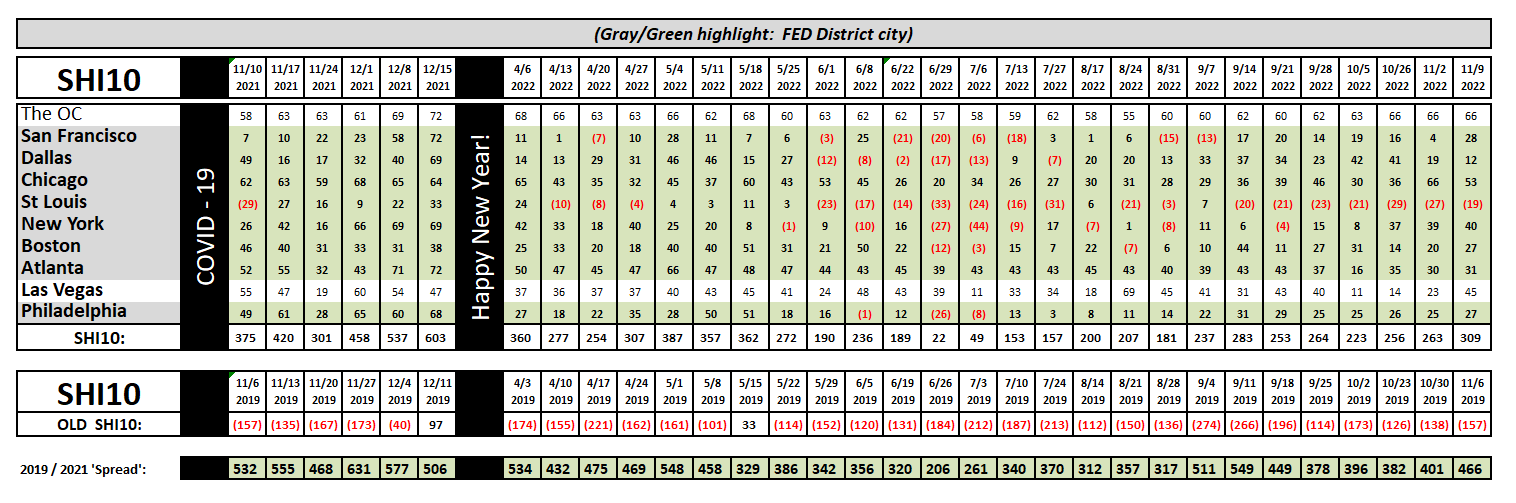

I find the resilience of the steakhouses fascinating. Here in the OC, they remain almost fully booked for Saturday. Only St Louis is showing red ink. Impressive. Here’s the longer term chart:

A very impressive SHI week indeed … especially in light of the FED headwinds. Could the economy be expanding faster than we expect? Hmmm…..

Yes it can, says the Atlanta FED! Earlier today, they released their latest reading of their GDPNow metric. From the Atlanta FED:

Latest estimate: 4.0 percent — November 9, 2022

The GDPNow model estimate for real GDP growth (seasonally adjusted annual rate) in the fourth quarter of 2022 is 4.0 percent on November 9, up from 3.6 percent on November 3. After last week’s employment situation report from the US Bureau of Labor Statistics and this morning’s wholesale trade report from the US Census Bureau, the nowcasts of fourth-quarter real personal consumption expenditures growth and fourth-quarter real gross private domestic investment growth increased from 4.0 percent and 0.7 percent, respectively, to 4.2 percent and 2.1 percent, respectively.

Wow…the Atlanta FED is now forecasting a 4% real GDP increase for Q4, 2022. Even as interest rates soar, courtesy of their brothers at the FED (well, to be more precise, the FOMC.), and the experts are forecasting a slowdown or recession?

In these crazy times …. what can you count on? What can you believe? The SHI, my friends. Believe in the SHI. 🙂

<:> Terry Liebman