SHI 10.27.21 – Common Prosperity Crushes the Ant

SHI 10.20.21 – Let the Good Times Roll!

October 20, 2021

SHI 11.3.21 – “The Tales of my Demise …

November 3, 2021

For about 40 years, China promoted old-fashioned, capitalist-style economic growth to lift their masses out of poverty. It worked very, very well.

“

Common prosperity. China’s new goal.“

“Common prosperity. China’s new goal.“

No longer. China and President Xi have a new goal: “Common prosperity.” That slogan is popping up everywhere both inside and outside of China, in public speeches, state-controlled media and schools, and even from slapped-down business tycoons like Jack Ma, who has now “agreed” to permit his “Ant Group Co,” a company valued at more than $300 billion earlier this year, to become a “financial holding company overseen by China’s central bank.” Ant owns Alipay which has more than one billion users in China. Alipay is reported to have handled over $17 trillion of digital payments in the year ending June of 2020. Further, in the year prior, Alipay made short-term loans to 500 million people. With Ma at the helm, Ant realized staggering success. No longer. ‘Common Prosperity’ has crushed the Ant.

Ant publicly commented, “We will put our growth proactively within the national strategic context and will strive to create societal value.” Regulators have demanded Ant and Alipay remove “unfair competition in its payment business,” and “break” the information monopoly of the company’s vast consumer database, permitting unfettered access by Chinese regulators. Ouch.

It no longer pays to get rich in China.

Welcome to this week’s Steak House Index update.

If you are new to my blog, or you need a refresher on the SHI10, or its objective and methodology, I suggest you open and read the original BLOG: https://www.steakhouseindex.com/move-over-big-mac-index-here-comes-the-steak-house-index/

Why You Should Care: The US economy and US dollar are the bedrock of the world’s economy.

But is the US economy expanding or contracting?

The short answer? Expanding. By a staggering measure. In fact, during Q1 and Q2, annualized 2021 ‘real’ growth averaged about 6.4%. In nominal terms, our US economy averaged almost 12% growth — adding $1.245 trillion of economic activity during the first half of the year. The world’s annual GDP is expect to end 2021 near about $93 trillion. Annualized, America’s GDP settling in at almost $23 trillion by mid-year — still around 25% of all global GDP. Collectively, the US, the euro zone, and China still generate about 70% of the global economic output. These are your big players.

The objective of this blog is singular.

It attempts to predict the direction of our GDP ahead of official economic releases. Historically, ‘personal consumption expenditures,’ or PCE, has been the largest component of US GDP growth — typically about 2/3 of all GDP growth. In fact, the majority of all GDP increases (or declines) usually results from (increases or decreases in) consumer spending. Consumer spending is clearly a critical financial metric. In all likelihood, the most important financial metric. The Steak House Index focuses right here … on the “consumer spending” metric. I intend the SHI10 is to be predictive, anticipating where the economy is going – not where it’s been.

Taking action: Keep up with this weekly BLOG update. Not only will we cover the SHI and SHI10, but we’ll explore “fun” items of economic importance. Hopefully you find the discussion fun, too.

If the SHI10 index moves appreciably -– either showing massive improvement or significant declines –- indicating growing economic strength or a potential recession, we’ll discuss possible actions at that time.

The Blog:

OK, that’s a bit of hyperbole. It still pays to get rich in China. But you’d better do it very quietly, without the regulators noticing. Because if they do, you may not be rich much longer. But, selfishly and cynically, we don’t care much about that, right? No one these days, politician or citizen, in China or America, is shedding a tear for billionaires. That’s clear in both countries. But regardless of your personal view about China’s invigorated efforts around common prosperity, or America’s newly invigorated focus on taxing billionaires, my concern is more focused on the US and global economic impact of these changes. For today, we will focus on China.

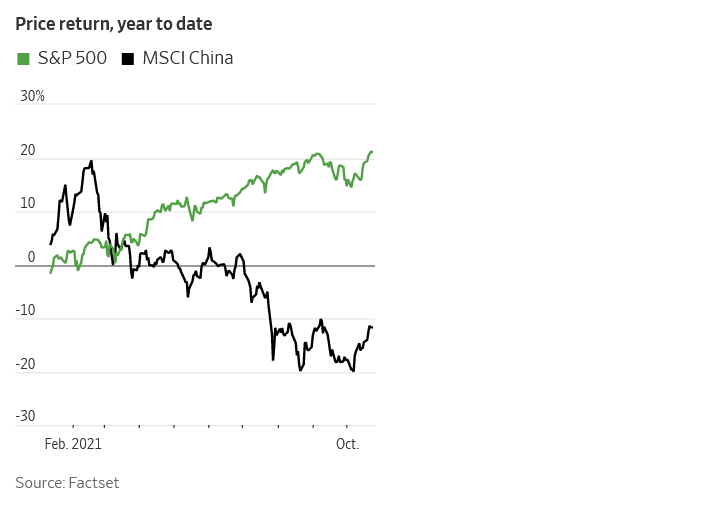

About a year ago, Jack Ma publicly criticized China’s financial system. One year later, the company he founded, Alibaba, is worth about $344 billion less. Many other public Chinese companies have felt the same pain: Softbank, Tencent, and others have also lost value between $40 billion and $100 billion each. Evergrande has lost even more value. The aggregate effect on the Chinese stock market is rather chilling, especially when compared to the S&P 500 during the same time-frame. Common prosperity may be good for the masses … but their stock market doesn’t see it that way:

So I ask: Is this the best way for the leaders in China to create common prosperity? Can common prosperity improve by destroying corporate capital and ruining shareholders? The approach seems ill-conceived to me.

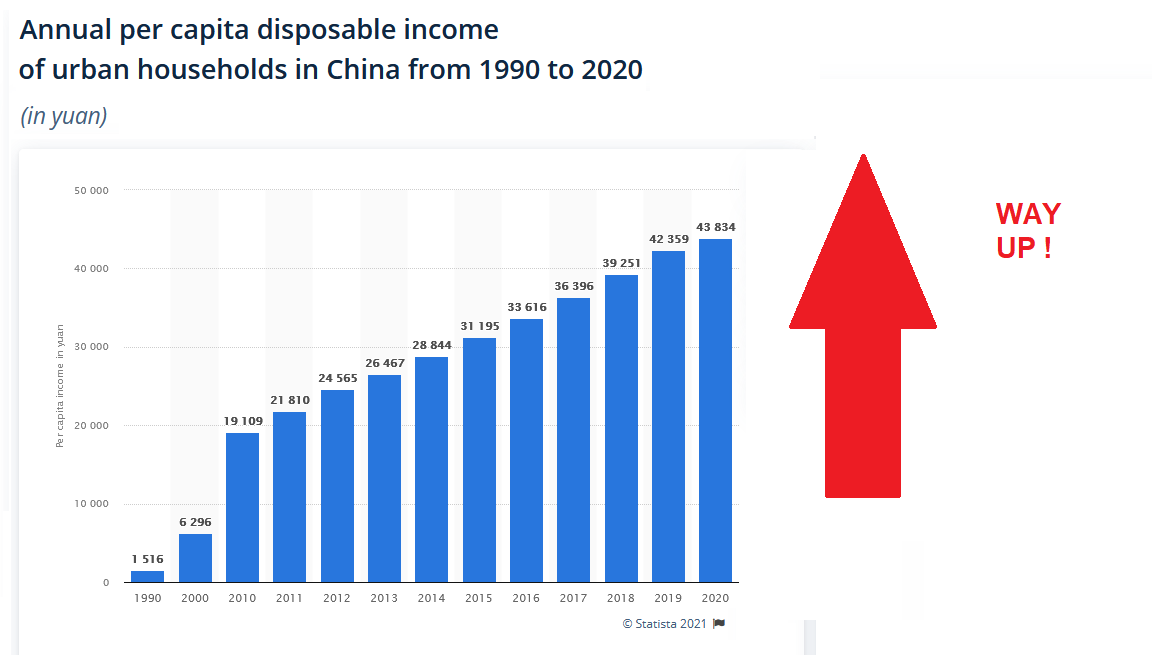

Of course, thru the lens of Communism, we all understand President Xi’s objections to corporate greed and run-away housing speculation. Clearly, the enrichment of a few, potentially at the expense of the many, within a quasi-communist financial system, doesn’t ring true to the masses. Understood. But for many decades, China’s far-more capitalist than communist system has ushered in massive increases in the average Chinese household’s income:

I don’t know about you, but I consider an increase from 1,516 yuan per annum to 43,834 yuan/year, in a 30 year period, to be rather miraculous. To me, this outcome has been a staggering success for the average Chinese household.

Which is why I find it rather surprising that all of a sudden, in 2021, Chinese leadership feels rampant income growth is a bad thing for China and her people.

It turns out they do not. Recently, leadership scaled back the rhetoric. On October 15th, China released a more in-depth transcript of President Xi’s earlier remarks on common prosperity. The community party paper, “Seeking Truth,” the rhetoric is softened a bit, reassuring global investors and Chinese entrepreneurs earlier spooked by the novel approach and language, targeting a “rational adjustment” of excessive Chinese incomes.

“If the system is stable, the country is stable, and if the system is strong, the country is strong. The world today is undergoing major changes unseen in a century, and the Chinese nation is forging ahead on its journey to achieve a great rejuvenation. The people’s congress system is a fundamental political system that supports competition in comprehensive national strength and wins strategic initiative. We must unswervingly persist, advance with the times and improve, and strengthen and improve the work of the people’s congress in the new era. In accordance with General Secretary Xi Jinping’s important instructions, we must fully implement the Constitution and safeguard its authority and dignity; accelerate the improvement of the socialist legal system with Chinese characteristics; make good use of the supervision rights granted by the constitution to the people’s congress; give full play to the role of the people’s congress; strengthen the self-construction of the people’s congress; Strengthen the party’s overall leadership over the work of the people’s congress.”

The bottom line: The word “people” is used quite often. The new message appears to be that the policy pendulum will move more toward economic equality: higher taxes and more pressure to donate for high-income individuals, higher spending on social programs, and tougher anti-monopoly enforcement.

Hmmm …. sounds an awful lot like the agenda of the US Senate of late, doesn’t it?

Sorry, sorry, I know: I’m supposed to stay away from politics here. My mistake. Only economics. 🙂

Why is this issue critically important to us?

China has the largest population, and is the second largest economy, on the planet. In fact, according to the Economist magazine’s Big Mac Index, in June of this year the Chinese yuan was 38.8% undervalued against the US dollar. A Big Mac costs 38.8% less in China … so if we adjust for “purchasing-power parity,” called PPP in economic theory, China’s GDP is actually larger than ours by a significant margin. Perhaps not when measured in dollars, but when measured by purchasing power within China, their effective GDP exceeds that of the United States.

https://www.economist.com/big-mac-index

Thus, like the US, China is a big fish, economically speaking. If their top leadership is making sweeping changes that have the potential to crush their economy, we should be concerned. And we need to understand what impact China’s new policies could have on the global economy, inasmuch as economic globalization and supply chain inter-connectivity are realities of today’s marketplace. Remember, the vast majority of US imports, and by extension US consumer spending, originate in Chinese manufacturing facilities.

And there are corollary, tangentially related issues to consider as well. For example, suppose China falls into an economic funk due to these changes … and their people threaten to revolt. What’s the best way to quell a revolt within your borders? How about a war? If the Chinese economy weakens … and unrest spikes … why not attack Taiwan? That will certainly change focus. Impossible you say? Could never happen? Sure it could. In fact the exact same thing happened back in 2014 … except the “attacker” was Russia and the “attackee” was the Ukraine, ultimately resulting in the annexation of the Crimean Peninsula by Russia. Sure, there are a number of essential differences … but the concept and reasons are striking similar. In fact, the official name for Taiwan today is “the Republic of China,” and for years, China has sought to reunite the two countries. Perhaps the time has come?

These are the kinds of things, on a short list of things, that keep me up at night. My wife tells me I shouldn’t worry so much … but I do. Perhaps an argument to worry less might be the evidence I shared on Russia above? After all, they attacked and annexed another country without so much as a blip on the global economy, right? Right … but the difference is that the GDP of Russia is only about $1.4 trillion — in fact, their GDP is less than half of California’s. Sorry, Russia, I hate to offend, but in the scheme of global economics, Russia, you really don’t matter. You do in the oil markets, but not global economics. Sorry. Another significant difference: The US did not join the fight. Russia was able to annex Crimea without much resistance. But would the US stand by, and do nothing, if China invaded Taiwan? Would the rest of the world? Hard to say, right? After all, Taiwan is a US ally, an important trading partner, and it is considered a geographically important nation by the US military.

For the moment, I’m not overly concerned about either an economic collapse in, a housing collapse in, or a military attack from, China. For now. I believe the central committee has the proverbial Chinese tiger by the tail, and so far they seem to be holding on. Thus, at the present time, my sleep is uninterrupted. For now. 🙂

Hungry? Let’s head to the steakhouses. And this week, let’s begin with the trend report:

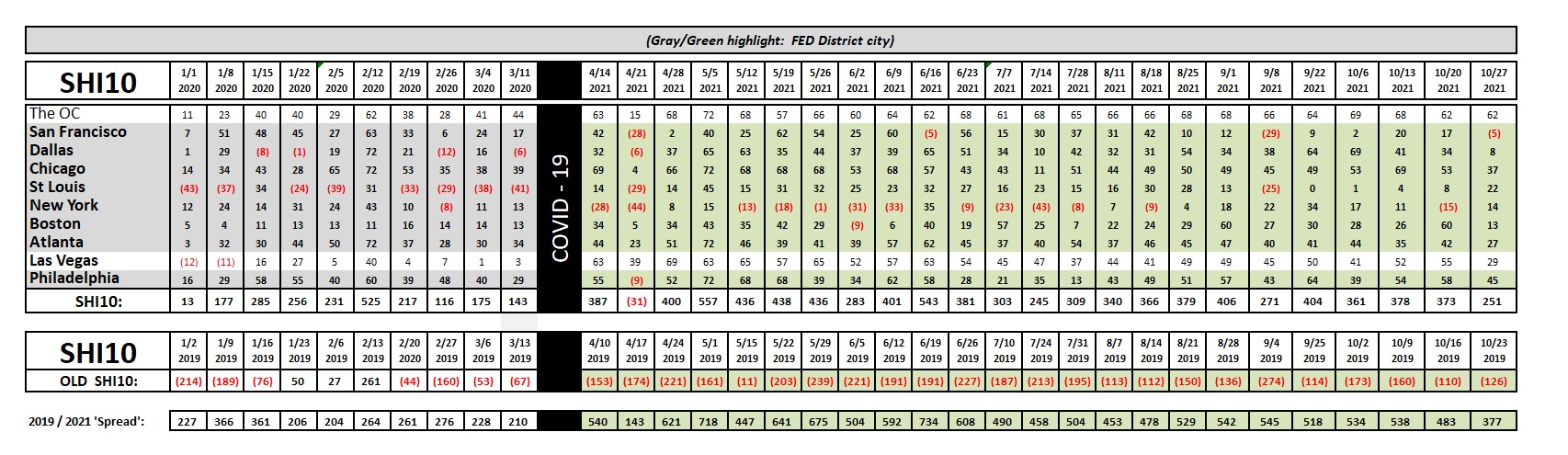

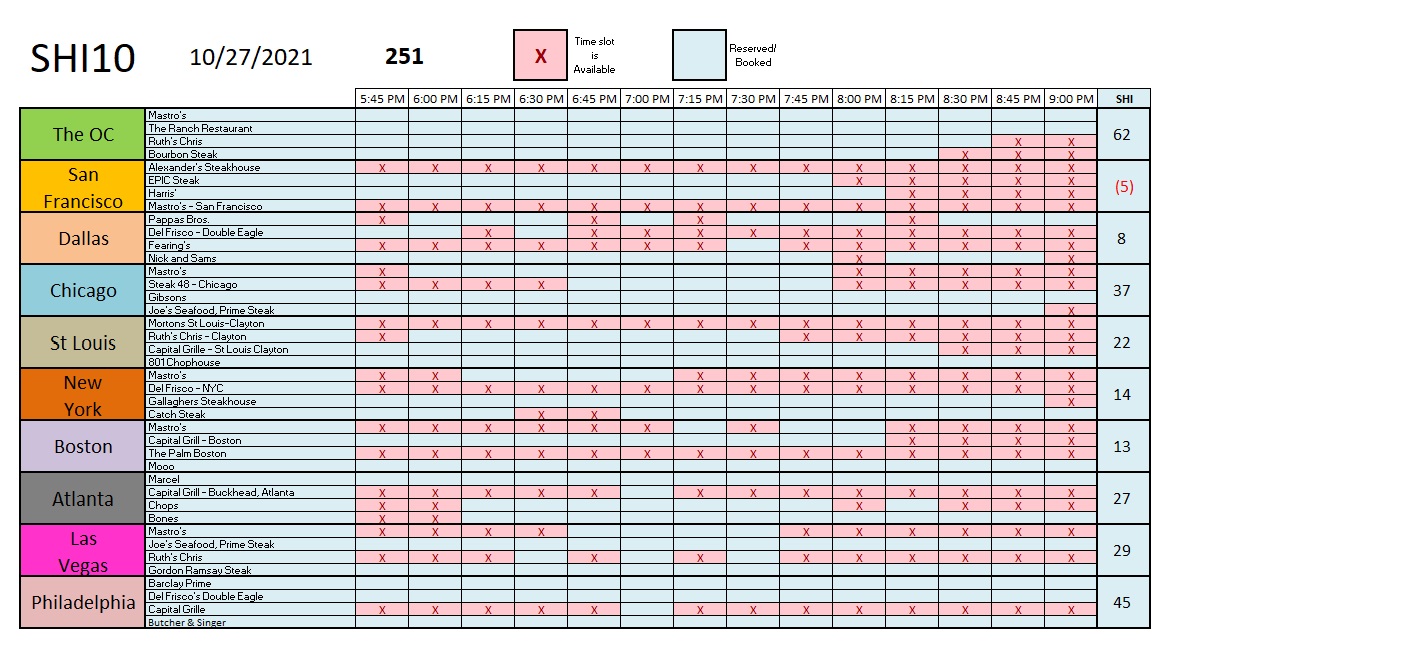

With an SHI10 reading of 251, today’s reading is softer than I would have expected. Then I realized the following day is Halloween … and many folks may have given up a fancy, expensive, Saturday-night steak dinner in exchange for a fun-filled Halloween party! Maybe. Regardless, after trending in the “mid-300s” for several weeks, today’s reading is definitely soft. Other than here in the OC and back east in Philly, most of our SHI cities saw a sizable reduction in Saturday reservation demand this week. Only NYC saw a significant increase in reservation demand. Here’s the city chart:

Reservation demand in San Francisco remains surprisingly weak. Even Las Vegas has quite a few open tables this Saturday. We’ll have to wait and see if this is an aberration or a trend.

The good news, economically speaking, is that consumer spending and consumer confidence are both trending up as of late. In fact, consumer confidence numbers are up globally. (https://www.conference-board.org/data/consumerconfidence.cfm) Thus, while the SHI may be indicating some demand softness, it is not yet concerning. For now, by my read, the US expansion continues unabated.

I can look forward to a good night’s sleep. For now. 🙂

<:> Terry Liebman