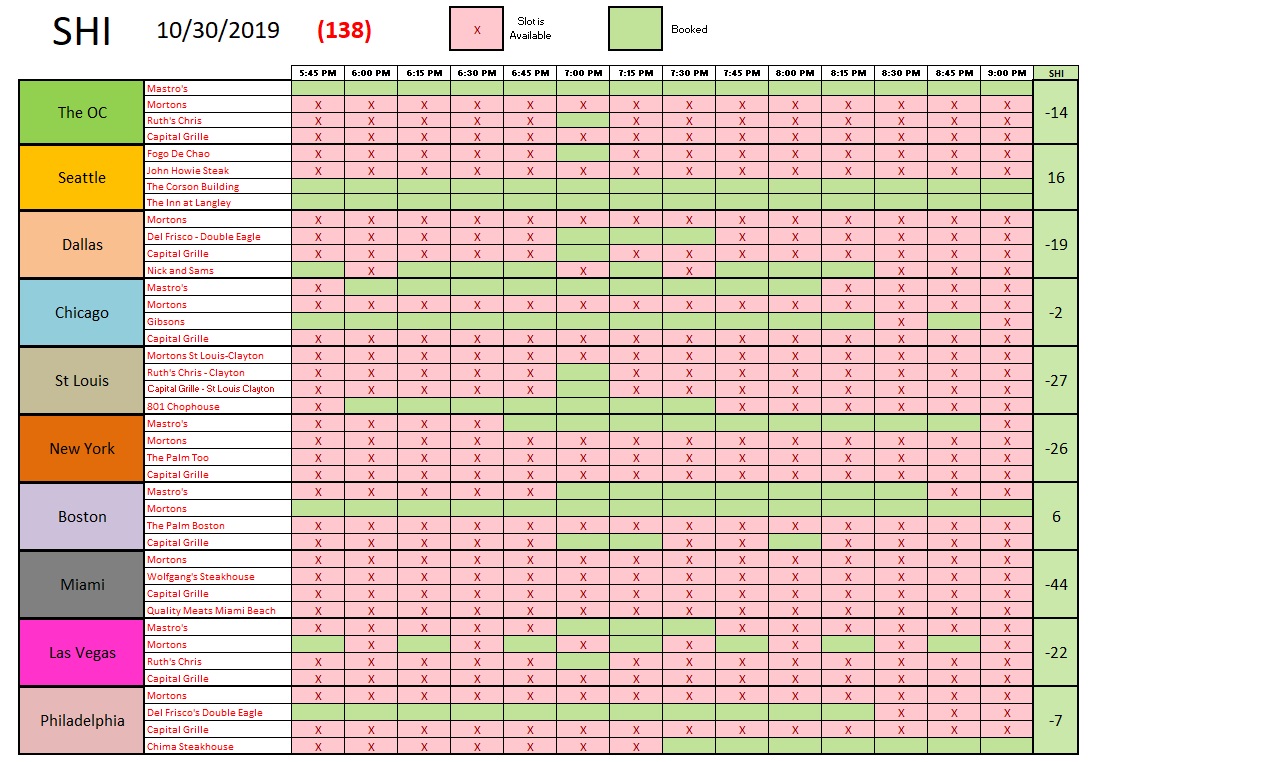

SHI 10.30.19 – Today is GDP Day!

SHI 10.23.19 – Watching A Rare Grilling

October 23, 2019

SHI 11.6.19 – Sputtering Along on 5-Cylinders

November 6, 2019

“The ‘advance reading’ for 2019 Q3 GDP was released at 5:30 am (CA) today.”

Did you watch? I did! Riveting TV, to be sure! Even if you missed its debut, I’m sure you’re curious about the number.

But before we get to that, I’m bet you are also wondering about the most-recent NY Fed and Atlanta FED forecasts, right?

- Atlanta FED ‘GDPNow’ forecast from Monday, October 28: 1.7%

- NY FED ‘Nowcast’ from October 25th: 1.91%

Interesting. You may recall the ‘final’ second quarter GDP reading was 2.0% … quite a bit lower than the blistering growth rate of 3.1% in Q1. Clearly, the FEDs believe Q3 will be lower still. Were they right? Were they close? Read on, my friends, read on.

Welcome to this week’s Steak House Index update.

If you are new to my blog, or you need a refresher on the SHI10, or its objective and methodology, I suggest you open and read the original BLOG: https://www.steakhouseindex.com/move-over-big-mac-index-here-comes-the-steak-house-index/

Why You Should Care: The US economy and US dollar are the bedrock of the world’s economy. This has been the case for decades … and will be true for years to come.

But is the US economy expanding or contracting?

According to the IMF (the ‘International Monetary Fund’), the world’s annual GDP is about $85 trillion today. According to the most recent estimate, US ‘current dollar’ GDP now exceeds $21.53 trillion. In Q3 of 2019, nominal GDP grew by 3.5%, following a 4.7% annualized growth rate in Q2. The US still produces about 25% of global GDP. Other than China — in a distant ‘second place’ at around $13 trillion — the GDP of no other country is close. The GDP output of the 28 countries of the European Union collectively approximates US GDP. So, together, the U.S., the EU and China generate about 70% of the global economic output.

The objective of this blog is singular.

It attempts to predict the direction of our GDP ahead of official economic releases.

Historically, ‘personal consumption expenditures,’ or PCE, has been the largest component of US GDP growth — typically about 2/3 of all GDP growth. In fact, the majority of all GDP increases (or declines) usually results from (increases or decreases in) consumer spending. Consumer spending is clearly a critical financial metric. In all likelihood, the most important financial metric. The Steak House Index focuses right here … on the “consumer spending” metric. I intend the SHI10 is to be predictive, anticipating where the economy is going – not where it’s been.

Taking action: Keep up with this weekly BLOG update. Not only will we cover the SHI and SHI10, but we’ll explore related items of economic importance.

If the SHI10 index moves appreciably -– either showing massive improvement or significant declines –- indicating growing economic strength or a potential recession, we’ll discuss possible actions at that time.

The BLOG:

About a year ago, the Wall Street Journal surveyed 48 economists, asking if they believed the US was in a “trade war.” Exactly half — 24 of the respondents — said no. But in their latest survey, conducted in early August of this year, 87% of the respondents said yep, the US is now in a trade war. This is a shocking outcome, in light of the fact that it’s hard to get economists to agree on something as simple as which wine they prefer to pair with their T-Bone at Mastros, let alone something more complex like the general state of the economy.

And they appear to be correct, if we look at today’s data:

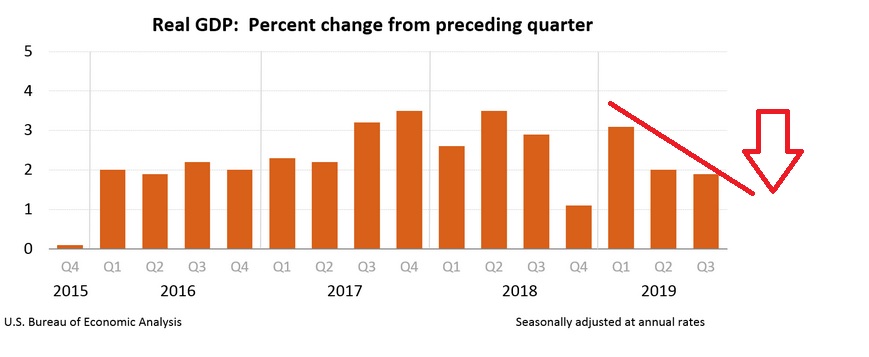

Look at the chart. US GDP growth is clearly decelerating. After tipping the scales at a robust 3.1% annual rate in Q1, Q2 and Q3 are telling a very different story. You’ll recall the Q2 GDP growth rate was 2.0%. Today’s ‘advance’ estimate of the Q3 growth rate is slightly lower — at the annualized rate of 1.9%. The facts seem incontrovertible: The trade war appears to have taken about 1% off our annual GDP growth rate. Looking at the graph, one has to wonder if the trend will continue. Will GDP growth continue to decline? Are we heading to that “bad place” where our economy begins to contract? That place known as a recession?

Let’s take a closer look at the GDP components from today’s release.

Once again, we see the ‘consumer consumption’ component of GDP is driving the growth. Repeating the same pattern we saw in Q2, in this quarter the growth in consumer consumption exceeded total GDP growth for the quarter. This may sound odd, but remember that any of the 4 primary GDP components can either add to growth or reduce growth. And, in fact, that’s what we see this quarter. Consumer consumption added 1.93% to the GDP figure … while both ‘investment’ and ‘exports’ reduced the GDP growth rate by (-.27%) and (-.08%), respectively. Government expenditures/consumption contributed a positive .35% to growth.

So our stalwart consumer is clearly still driving the economic bus. Consumer spending is the single bright spot in this GDP release. My long time readers know that about 70% of all long-term GDP growth is the result of consumer spending. Whether the spending is on goods or services … whether the the spending is on ‘durable’ goods or goods for immediate consumption, the consumer is the backbone of the US economy. Make no doubt, there are minor signs of fatigue in the consumer spending “picture.” More important today, fortunately, are (1) the employment picture and (2) the inflation picture. The US labor force is employed and working away. At the same time, both the levels of current inflation and consumer inflation expectations are firmly anchored at very low levels. As long as folks are employed, and inflation expectations remain firmly anchored, a little consumer fatigue is unlikely to change the picture much. But if either change meaningfully, look out. Because consumer consumption will be adversely impacted — in a big way.

I do not anticipate the inflation picture moderating any time soon. I watch this very closely … and I really don’t see any storm clouds on the horizon. The employment picture is a little more complex. On one hand, demographic changes are causing the civilian labor force (CLF) to grow much slower. So with our current robust demand for labor, pretty much anyone who wants a job (and is qualified), has one. The impacts of globalization, automation, and AI offer a bit of a counter-balance. But overall, this is a healthy market. For now. We’ll keep a close eye on it.

So, since the consumer is KING, the SHI10 is even more important than ever! 🙂

Let’s jump over to the steakhouses and see how reservation demand is holding up.

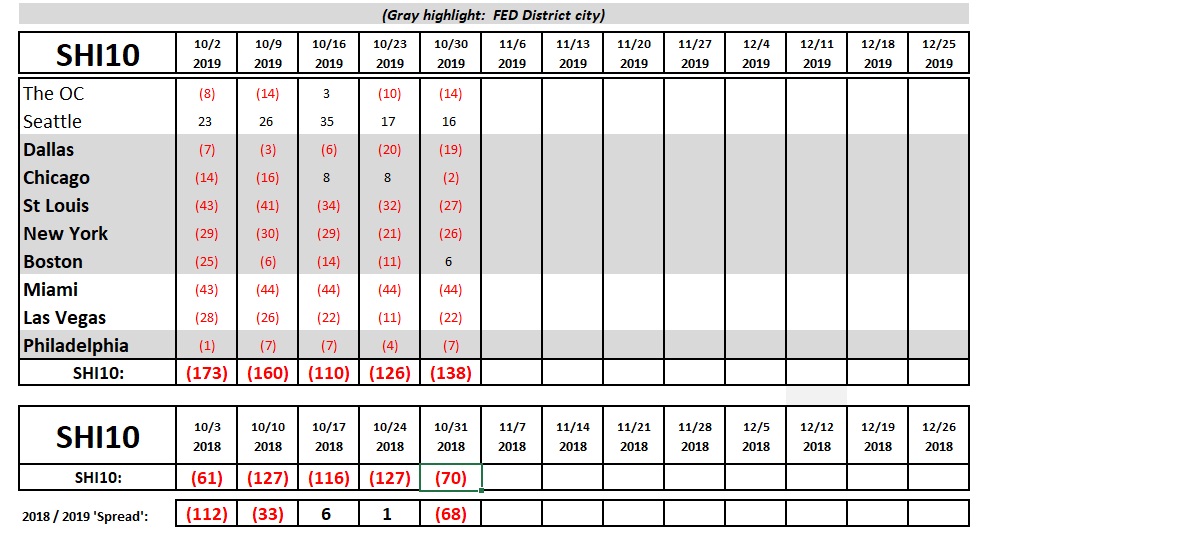

So so. Not as well as the past two weeks, but not bad. Once again, the SHI10 reflects a lower overall demand for high-priced steaks at America’s most expensive steakhouses when compared to historic metrics. Again, remember, this is not bad. But it is very much in alignment with today’s GDP number. Luke warm. Like a well-prepared ‘rare’ Filet Mignon. Here are today’s numbers:

It’s worth mentioning the FED finished their 2-day October meeting today and made the decision to cut short-term rates for the 3rd time this year, again by 1/4 of a percent. Commentary in their press release mirrors my blog comments above:

“Although household spending has been rising at a strong pace, business fixed investment and exports remain weak. On a 12-month basis, overall inflation and inflation for items other than food and energy are running below 2 percent. Market-based measures of inflation compensation remain low; survey-based measures of longer-term inflation expectations are little changed.”

This week, the FED could have written my blog. And used far less words. 🙂

Make no mistake, the FEDs move today is another indication of their level of concern about our economic expansion. 3 rate cuts means they’re concerned. They want to keep the expansion rolling along … and they’re doing all they can to ensure this happens.

– Terry Liebman