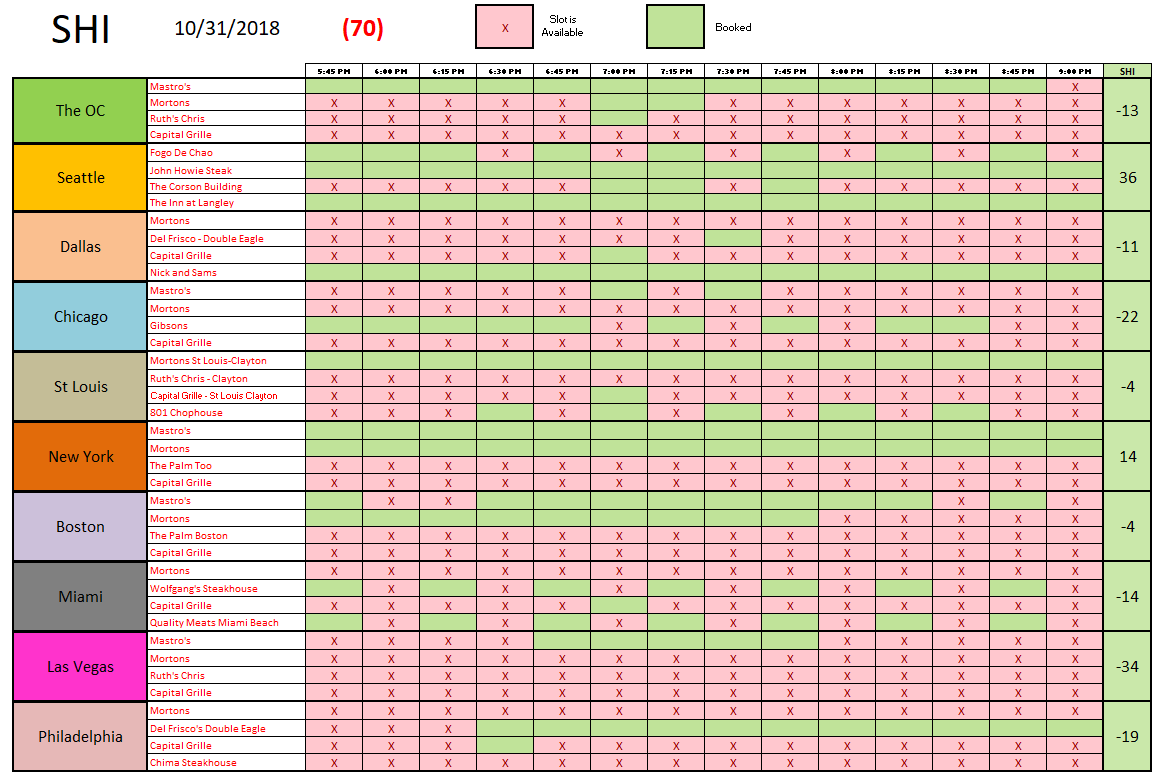

SHI 10.31.18 So Good its SPOOKY!

SHI 10.24.18 Give and Take

October 24, 2018

SHI 11.07.18 Good News? Bad News?

November 7, 2018

“Here’s a Halloween tale that will send shivers down your spine … Q3 GDP grew by a blistering annual rate of 4.9%, following on Q2 which grew at 7.6%.”

Spooky, right? Wait, are we talking about China? Where GDP growth rates are typically north of 7%? Nope. This is happening right here in the good ‘ol US of A. Granted, I’m talking about the nominal rate of increase. But get this: Adding the nominal growth in Q2 and Q3, the US gross domestic product increased by $618 billion. So good, it’s downright scary.

Welcome to this week’s Steak House Index update.

If you are new to my blog, or you need a refresher on the SHI10, or its objective and methodology, I suggest you open and read the original BLOG: https://www.steakhouseindex.com/move-over-big-mac-index-here-comes-the-steak-house-index/

Why You Should Care: The US economy and US dollar are the bedrock of the world’s economy. This has been the case for decades … and will continue to be true for years to come.

Is the US economy expanding or contracting?

According to the IMF (the ‘International Monetary Fund’), the world’s annual GDP is about $80 trillion today. US ‘current dollar’ GDP now exceeds $20.66 trillion. In Q3 of 2018, nominal GDP grew by 4.9%. We remain about 25% of global GDP. Other than China — a distant second at around $11 trillion — the GDP of no other country is close.

The objective of the SHI10 and this blog is simple: To predict US GDP movement ahead of official economic releases — an important objective since BEA (the ‘Bureau of Economic Analysis’) gross domestic product data is outdated the day it’s released. Historically, ‘personal consumption expenditures,’ or PCE, has been the largest component of US GDP growth — typically about 2/3 of all GDP growth. In fact, the majority of all GDP increases (or declines) usually results from (increases or decreases in) consumer spending. Consumer spending is clearly a critical financial metric. In all likelihood, the most important financial metric. The Steak House Index focuses right here … on the “consumer spending” metric. I intend the SHI10 is to be predictive, anticipating where the economy is going – not where it’s been.

Taking action: Keep up with this weekly BLOG update. Not only will we cover the SHI and SHI10, but we’ll explore related items of economic importance.

If the SHI10 index moves appreciably -– either showing massive improvement or significant declines –- indicating growing economic strength or a potential recession, we’ll discuss possible actions at that time.

The BLOG:

As indicted above, GDP growth here in the US is robust.

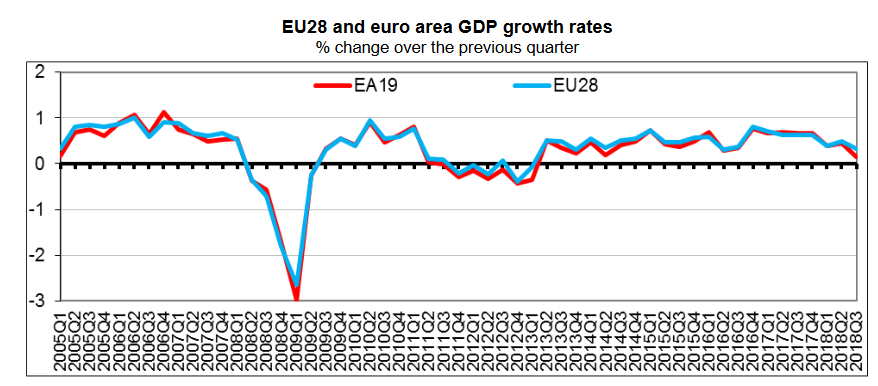

But the EU is lagging. Their GDP rose by only 0.3% in the “EU28” during the 3rd quarter. Notice how the right edge of the graph below is looking a bit like wilted asparagus from The Capital Grille:

In the opposite corner, we have Friday’s GDP figures. Hotter than Ruths’ Chris grill, our Q3 GDP growth figures remained quite impressive. It’s pretty clear that our US economy is firing on all cylinders.

But again, let me remind you that this blog is called “The Steak House Index” for a reason. It is designed to help our readers forecast future US economic performance. Not discuss what has already happened. The SHI is intended to be a predictive gauge the future performance of the US economy. Because economic slowdowns can only be identified about 6-months AFTER they begin. By the time we learn GDP has shrunk for 2 consecutive quarters, we have little opportunity to adjust our decisions – business or personal – to deal with the change. But if the SHI can help us predict when a slow-down or recession will occur, we can make better choices ahead of the curve, so to speak.

You will recall that about 70% of the US GDP results from ‘consumer spending.’ Which means, far and away, ‘Personal Consumption Expenditures’ (also known as ‘consumer spending’) is the single most important economic indicator – one that bears close scrutiny if you’re trying to gauge how the economy is doing – now and in the near future. In the macro, collectively, our behaviors are rational. Meaning, when faced with danger, we pull back. When faced with ‘financial’ danger, we do the same: we adapt our behavior to the conditions in which we find ourselves. If we – or our business (for those of you on a company ‘expense account’) – are feeling financially stressed, it’s unlikely we will take a party of 4 people to an expensive steak house for dinner on a Saturday night. Conversely, if we’re feeling flush, sure, we’ll go to Ruth’s Chris Steak House on Saturday night and shell-out $300 or $400 for dinner. Thus, the SHI postulates the availability of — or lack of availability of — reservation ‘slots’ at our pricey steakhouses is statistically meaningful.

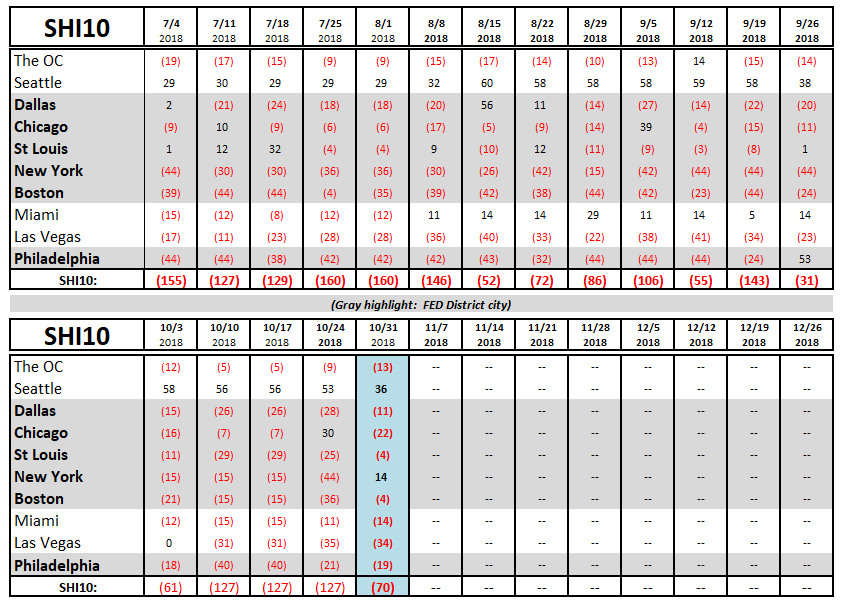

So let’s see what the steak houses are telling us today:

Steakhouse reservations are in demand! This week, we see SHI improvement in most of the SHI10 markets. Reservations in Chicago seem to have ‘reverted to the norm,’ trending negative once again. And Miami slipped a bit. I think they prefer salads in Miami. Even NYC jumped into the black this week. Steak and potatoes for everyone!

Here is the week’s SHI chart:

For now, the SHI10 is predicting steady as she goes. Here in the US.

But I’m a bit worried about Europe. Their economy is about the same size as ours (collectively) and they are slowing. China may be doing the same. Remember, the US is not an island. Well, maybe we are, if you consider North America to be an island. A very large island.

But here’s my point: Our economy is HOT right now. But I remain concerned a year or two out.

For now, enjoy your steaks!

- Terry Liebman