SHI 10.4.23 – Higher for Longer?

SHI 9.27.23 – WOOF

September 28, 2023

SHI 10.11.23 – M2, Monetarists and MMT

October 12, 2023

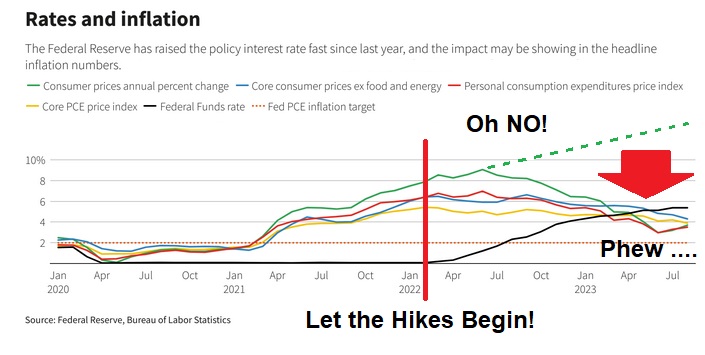

The FED began raising short-term interest rates in March of 2022. The Consumer Price Index (CPI) was clearly following the “Oh NO!” path … something had to be done!

18 months have passed since that time. Has the FEDs harsh financial medicine cured the problem? Is their work over? Is inflation crushed — permanently? Or was it transitory all along?

“

The FED crushes inflation!“

“The FED crushes inflation!“

We don’t hear the FED mention the word ‘transitory’ these days. No, these days, the FED and most economists attribute inflation’s drop to the FED rate hikes. But did FED rate hikes do the job? Or was the high inflation rate actually transitory … just a longer ‘transition’ than originally expected?

When the CPI first moved high above the FEDs long-term 2% inflation target rate, many experts – and the FED too – opined that the rising CPI rate was ‘transitory.’ Within a few months, at the “Oh NO!” point on the graph above, as the inflation rate continued to rise, the word ‘transitory’ became the billy club the media, economic experts, and many politicians used to pummel the FED for their apparent ineptitude. The FED soon caved, and the rate-hike cycle began – the fastest and largest hike cycle since the early 1980s.

Now, 18 months later, the US economy appears to have moved from the “Oh NO!” phase into the “Phew…” phase. So it’s time to ask the real question: Did the FEDs rate hikes crush inflation …. or <gasp!> would it have come down without the aggressive FEDs rate hikes?

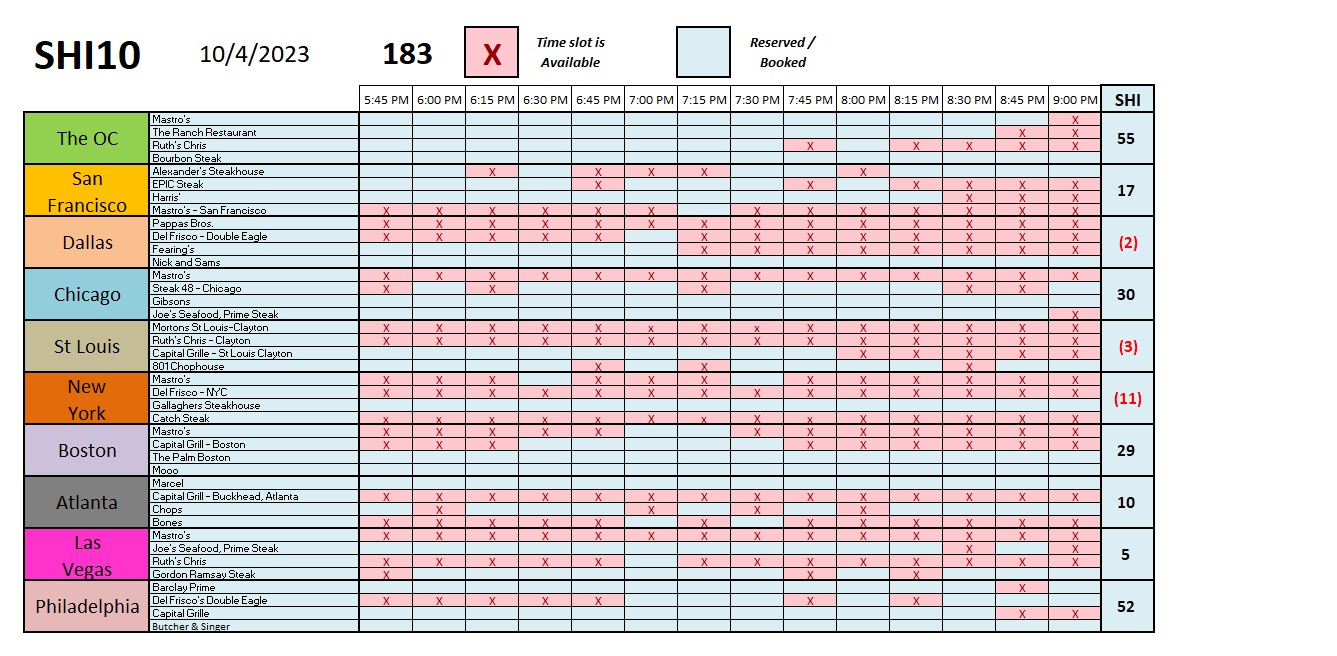

Welcome to this week’s Steak House Index update.

If you are new to my blog, or you need a refresher on the SHI10, or its objective and methodology, I suggest you open and read the original BLOG: https://www.steakhouseindex.com/move-over-big-mac-index-here-comes-the-steak-house-index/

Why You Should Care: The US economy and US dollar are the bedrock of the world’s economy.

But is the US economy expanding or contracting?

Expanding … FED rate increases notwithstanding! At the end of Q2, 2023, in ‘current-dollar‘ terms, US annual economic output rose to an annualized rate of $26.84 trillion. After enduring the fastest FED rate hike in over 40 years, America’s current-dollar GDP still increased at an annualized rate of 4.7% during the second quarter of 2023. Even the ‘real’ GDP growth rate was strong … clocking in at the annual rate of 2.4% during Q2. No wonder the FED is concerned.

The world’s annual GDP first grew to over $100 trillion in 2022. According to the IMF, in June of this year, current-dollar global GDP eclipsed $105 trillion! IMF forecasts call for global GDP to reach almost $135 trillion by 2028 — an increase of more than 28% in just 5 years.

America’s GDP remains around 25% of all global GDP. Collectively, the US, the European Common Market, and China generate about 70% of the global economic output. These are the 3 big, global players. They bear close scrutiny.

The objective of this blog is singular.

It attempts to predict the direction of our GDP ahead of official economic releases. Historically, ‘personal consumption expenditures,’ or PCE, has been the largest component of US GDP growth — typically about 2/3 of all GDP growth. In fact, the majority of all GDP increases (or declines) usually results from (increases or decreases in) consumer spending. Consumer spending is clearly a critical financial metric. In all likelihood, the most important financial metric. The Steak House Index focuses right here … on the “consumer spending” metric. I intend the SHI10 is to be predictive, anticipating where the economy is going – not where it’s been.

Taking action: Keep up with this weekly BLOG update. Not only will we cover the SHI and SHI10, but we’ll explore “fun” items of economic importance. Hopefully you find the discussion fun, too.

If the SHI10 index moves appreciably -– either showing massive improvement or significant declines –- indicating growing economic strength or a potential recession, we’ll discuss possible actions at that time.

The Blog:

Economic expansions don’t die a natural death. “I like to say they get murdered,” quipped ex-FED Chair Ben Bernanke.

And their murderer is often the FED. In the past 18 months, the FED has done all they can to murder the current economic expansion; of course, all the interest rate hikes ostensibly targeted the inflation rate, not the expansion. No, if the expansion does die, its death will be collateral damage in the FEDs war on inflation. At least that’s the ‘official line.’

Historically speaking, killing the expansion and increasing unemployment have always been required to reduce the inflation rate. As you know, it is precisely those two conditions — a robust economy and full employment — that typically triggers the need a FED rate increase cycle.

And yet, here we are, 18-months after the FED kicked off their interest rate hikes and something odd and unexpected has happened: Not only is the expansion alive and kicking, but the unemployment rate remains near 50-year lows AND the inflation rate continues to decline. One year ago, most economic experts told us this outcome was impossible.

I contend the FED rate hikes WERE necessary — but not to quelch inflation. No, the rate hikes were needed to slow a run-away economy, fueled by the massive post-Covid fiscal stimulus, and the gigantic on-shoring and infrastructure bills which are also dumping trillions of dollars into the US economy. These are the facts. Whether or not one or both were good ideas is a debate we’ll leave for the history books. And sovereign debt discussions.

Decades ago, Milton Friedman told us dumping trillions of dollars into an already-robust economy is somewhat like pouring gasoline on a bonfire. The past few years have proven him right once again. The fire rages. The FED, in this analogy, is simply trying to control the size of the fire by dumping a few buckets of water on the blaze. Have they done enough? Is the economy back “under control” and is inflation tamed?

When talking inflation, the FED prefers to focus on “personal consumption expenditures” and a price index based on those expenditures, called the PCE price index. Personal consumption expenditures are, like the name implies, just that: Stuff consumers buy. About 70% of all American economic activity is consumer consumption.

Like the consumer price index, or CPI, the PCE index is presented two ways: unaltered and as a “core” index. More on the topic from the Bureau of Economic Analysis … what is the PCE index?:

“A measure of the prices that people living in the United States, or those buying on their behalf, pay for goods and services. The PCE price index is known for capturing inflation (or deflation) across a wide range of consumer expenses and reflecting changes in consumer behavior.”

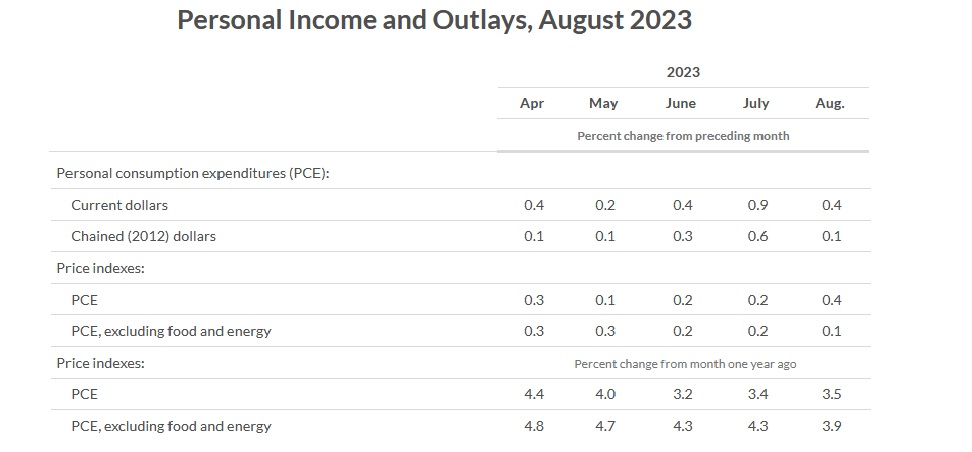

Yes, this sounds a lot like the CPI. And it is. However, it uses different component weights than the CPI. Moving on, the most recent PCE and PCE index readings were released by the BEA at the end of September. Here’s a chart with information from the first page of the economic report:

First, note the most recent reading is from August … and the report reflects the results from 6 consecutive months. Then, look at the ‘core’ PCE readings line called the “PCE, excluding food and energy” — clearly that is a downward trendline. In August of last year, the monthly core PCE peaked at 0.6% … and repeated that high in January, but fell to 0.3% in February and March, followed by the 6-months of reading above. By this metric, therefore, the trendline is clearly moving in the direction the FED wants. As we see above, the most recent core PCE reading was only 0.1%.

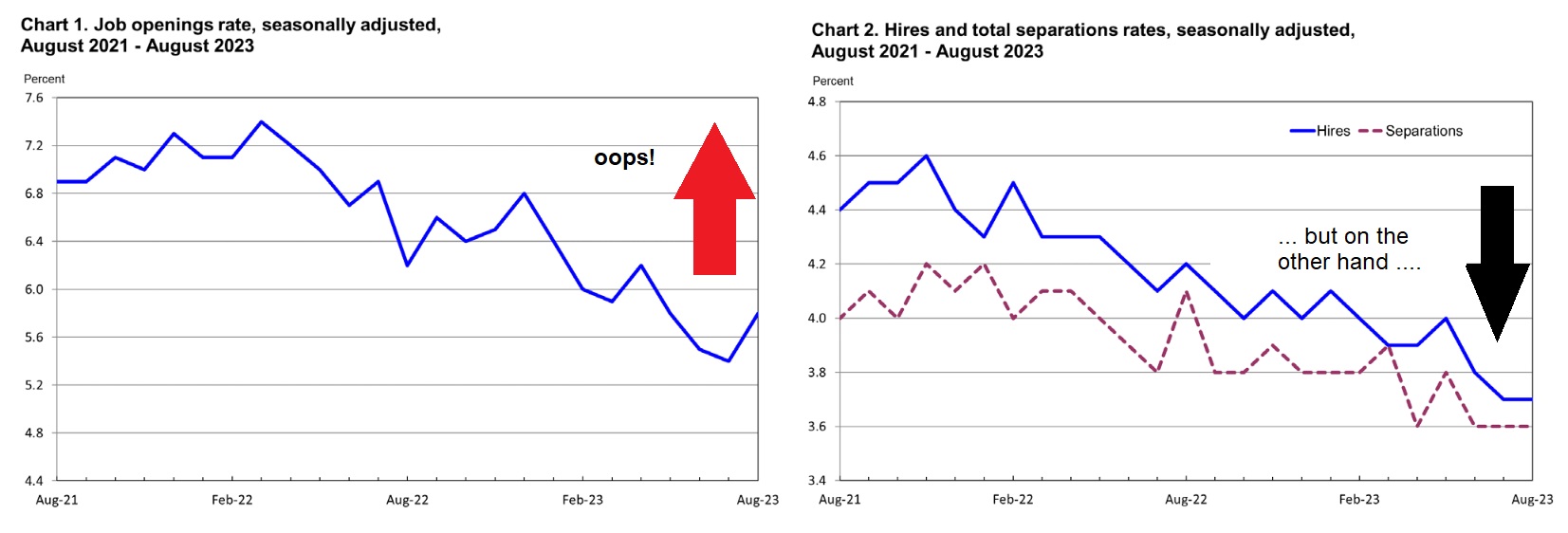

But wait! Tuesday morning the latest JOLTS report was released by the labor department. Job openings were up – a lot! In July, job openings clocked in at 8.92 million … and in August, JOLTS were jolted up to 9.610 million – an increase of 690 thousand, or 7.7%.

At least “hires” and “separations” are both much softer. Both are at levels far more reminiscent of those pre-pandemic.

Regardless, this JOLTS figure will not make Federal Reserve Chairman Jerome Powell very happy. Back on March 8, 2023, Powell testified in front of Congress and was pleased to report that the JOLTS report for January showed a decline in job openings from 11.23 million to 10.8 million. This fact, he commented, was consistent with the Fed’s view that the labor market was “improving gradually.” By that comment, Powell really meant the labor market was softening – fewer job openings translates to lower demand for labor.

Presumably if asked – and I suspect he will be asked – this latest JOLTs report is not welcome news.

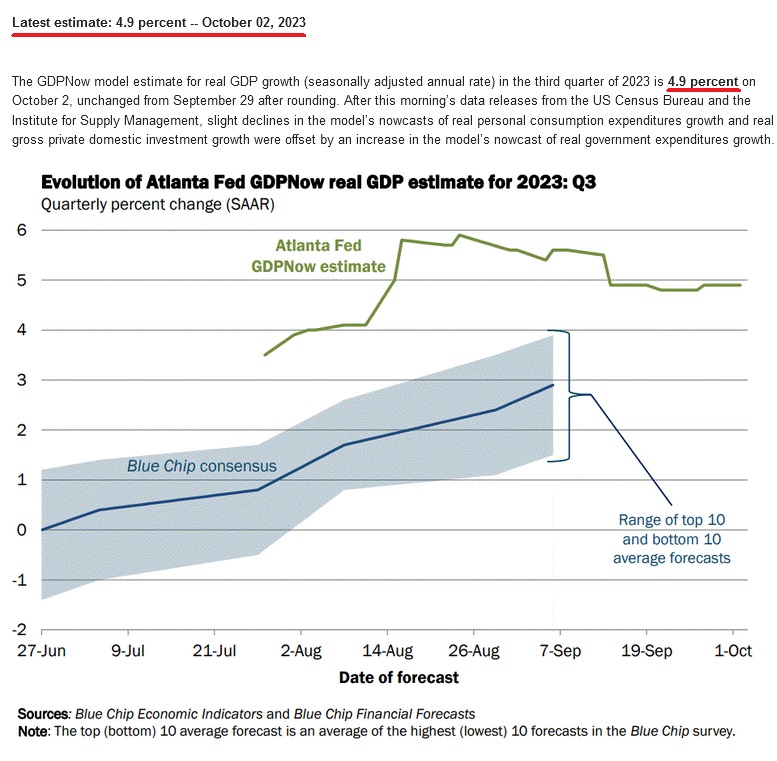

So which is it? Is price inflation falling? Or is wage inflation reigniting? Is the economy slowing right now? Or is it accelerating, as suggested by the October 2nd Atlanta FED ‘GDPNow’ forecast of 4.9% for Q3?

That’s right, I kid you not. The latest Atlanta ‘GDPNow’ forecast is a 4.9% ‘real’ growth rate in Q3. Check out this image from their site:

Last quarter, the “GDP deflator” – which is essentially the amount of nominal growth attributed to inflation, used to “deflate” the nominal growth figure to the “real” number – was fairly low at 1.7%. This number is significantly below the current CPI or PCE, but lets assume the Q3 number is the same. Using these numbers – 4.9% from the Atlanta FED and a PCE deflator of 1.7%, the forecast for Q3 nominal GDP growth is running at a 6.6% annual rate!

Talk about conflicting signals! What can possibly make sense out of this soupy hodgepodge of conflicting signals?

The steakhouses can! Let’s see if the SHI agrees that the economy is sizzling.

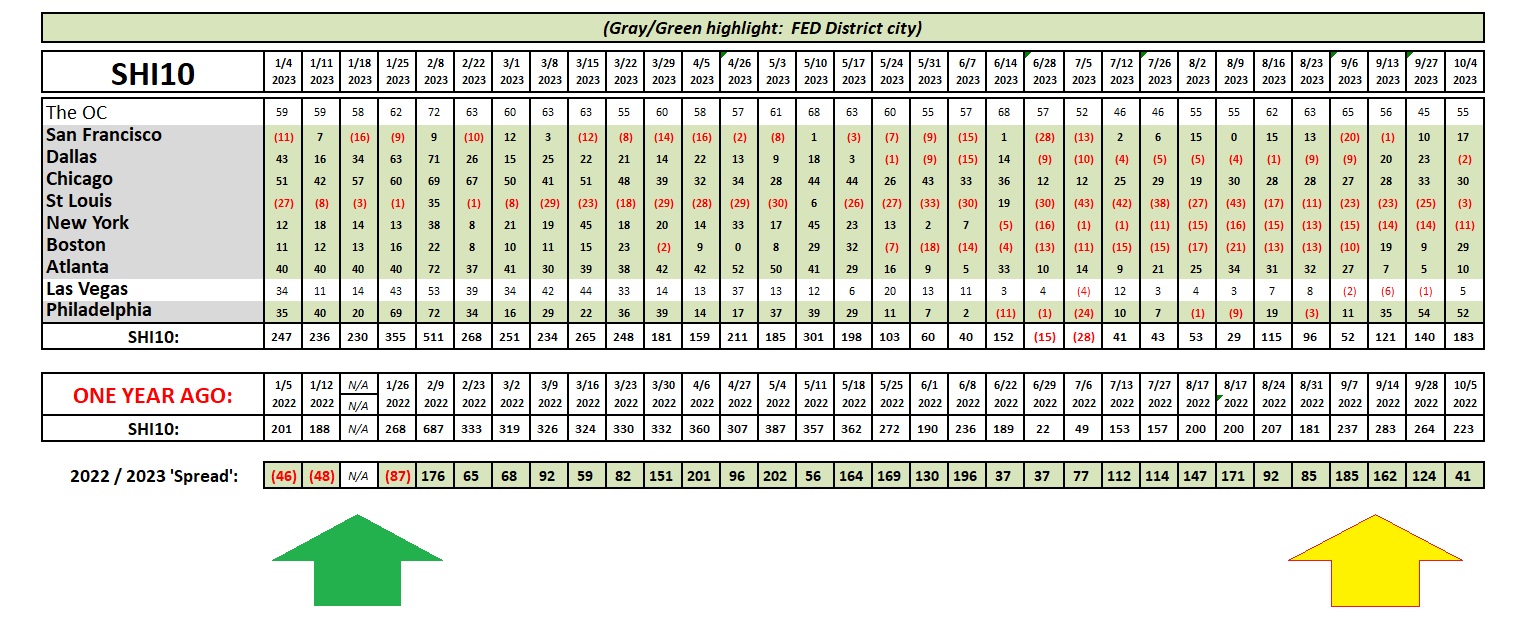

It appears the answer is yes, the grills are hot; reservation demand for this coming Saturday at our 40 expensive eateries across America is quite robust too. Like the Atlanta FED, the SHI10 suggests the American consumer is actively consuming. That’s a good thing for the economy. Steaks. Wine. And plenty of other expensive fare.

Note the green and yellow arrows above. When the year began, the 2022/2023 ‘spread’ was negative — meaning reservation demand in 2023 was hotter than in 2022. In the past six months, this has reversed. 2023 demand is smaller than last year. Pricey steakhouse demand is cooler. In theory, this suggests weaker consumer demand and a slower GDP growth rate.

The bottom line, of course, is we wait. A lot more data will become available as the month rolls on:

- <> The next non-farm payroll report is due out on Friday, October 6th.

- <> The BEA releases the first estimate of Q3 GDP on October 26th.

- <> The FED meets next on Halloween – spooky! Will they raise rates again?

Non-farm payroll numbers have been slipping of late. The ‘whisper’ forecast for Friday is around 170,000 new jobs and a 3.7% unemployment rate – both consistent with the prior month readings. I don’t expect we’ll see a jobs number this high. My guess.

I think the JOLT number reflects the choppy nature of the market. Look at the graph again: The trendline is clearly down. So I’ll dismiss this month as a choppy aberration.

The gentlemen responsible for the NY FED Q3 ‘nowcast’ are painting a quieter picture than their brothers in Atlanta. Even so, they still forecast a resounding 2.1% annual GDP growth rate. So … 4.9% from the folks in Atlanta … 2.1% from New York. Both are quite robust.

And then we have the FED. Will the FED stand pat or will they raise rates again? I think they will stand pat.

Which begs the question: Why are long term rates rising today?

It’s entirely possible the bond market has now decided, in the aggregate, that a recession is off the table. Certainly, this is the message from the NY and Atlanta FEDs. And if the FED is able to leave short-term rates “higher for longer” then it’s entirely possible that the current lift in mid- and long-term yields simply reflects a pending correction in the yield curve. The yield curve is typically not inverted. It is now.

If that now “corrects” as many experts seem to be suggesting, and the FED overnight funds rate remains in the mid-5’s, then it is not too much of a stretch to expect the 10 year Treasury rate to move even higher than that. Watching CNBC a few days ago, their ‘bond expert’ actually opined he felt there is a good chance the 10-year Treasury could reach 13% sometime in the next 7 years. Normally I don’t repeat such outlandish forecasts, but this one was more shocking than most. Is this possible? Sure. Is it likely. No. The 10-year Treasury has reached that level only 1 time before. I don’t believe the catalysts that pushed the rate to that level will ever repeat. But, regardless, a forecast of this type shows you what some experts are thinking and saying.

A few blogs ago, I raised the question … are interest rates “higher permanently?”

After the past 10 or 15 years, this seems exceptionally unlikely to me. But financial conditions and variables are changing constantly. Not only is our US economy much larger than 5 years ago, so is our national debt, and our annual deficit. How these play out in the next two or three years will likely have a big impact on the direction of rates.

For now, I expect rates to remain higher for longer. Probably a few years, anyway. And after that, I expect rates to once again test old lows. This is my believe today. But this, too, may prove as fleeting as last year’s inflation rate.

<:> Terry Liebman