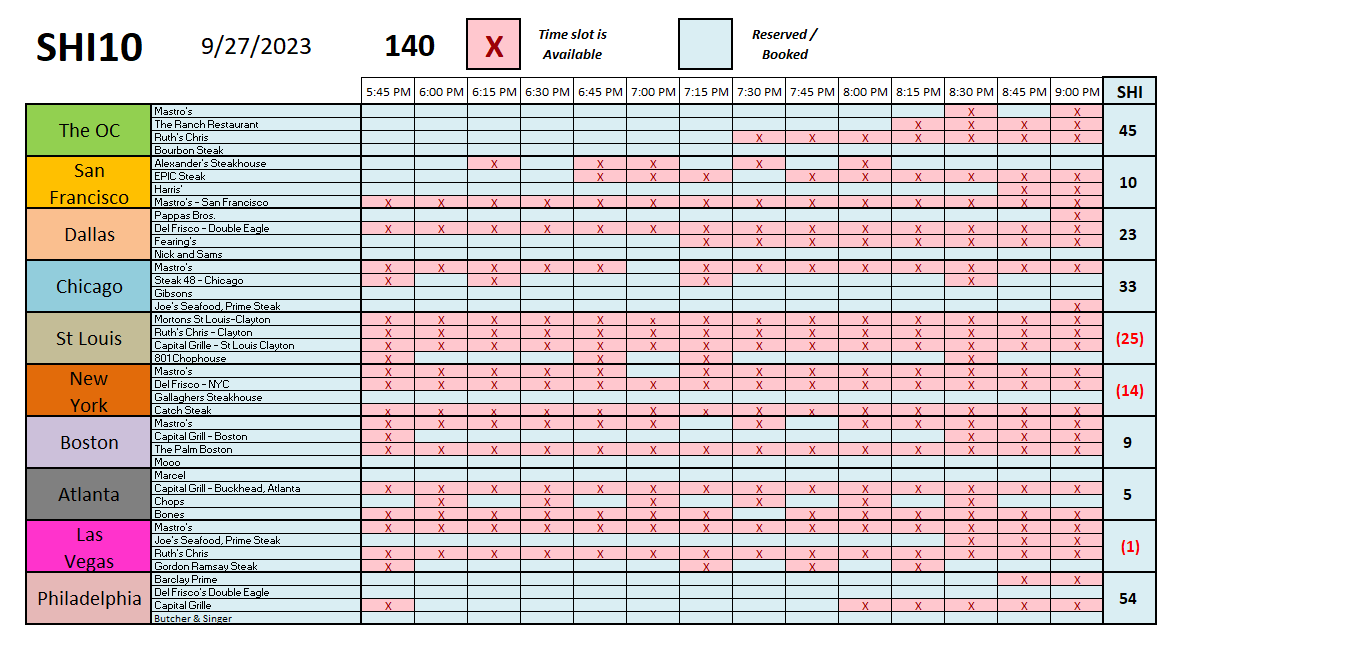

SHI 9.27.23 – WOOF

SHI 9.13.23 — Charge It!

September 13, 2023

SHI 10.4.23 – Higher for Longer?

October 5, 2023

I shop at Petco.

But you knew this already. You remember my amazement a few weeks back over the price of cat food? Yes, that was at Petco.

Two years ago, Petco — a publicly traded company under the symbol ‘WOOF‘ — borrowed $1.7 billion in the public capital markets. This fact, alone, is not overly interesting. Most public companies have issued “corporate debt” and many investors own the “corporate bonds” issued by large, publicly-traded companies.

“

Woof? Nope. Ouch.“

“Woof? Nope. Ouch.“

Ouch? Yes, ouch. Here’s why: The $1.7 billion I mentioned above had an interest rate of 3.5% when the loan was first made 2 years ago. Today, due to the variable interest rate feature in the note, that interest rate is now almost 9%.

Imagine a homeowner with a $1.7 billion home mortgage? Impossible? How about Elon Musk? I think he might owe more. 🙂

At a 3.5% rate, Elon’s payment on his $1.7 billion is manageable at only $4,958,333 per month. Of course, that’s ‘interest only.’ There is no principal repayment included in that figure. Elon could handle that monthly payment, right?

But at 9%, that monthly payment rises to $12,750,000 per month. This is precisely what has happened to Petco. The FED rate-hike cycle has essentially increased the monthly interest expense on their senior debt from under $5 million to almost $13 million. We don’t need to look much further to see the staggeringly deleterious results of the higher rates. Of course, this is only one story of millions across the US and the globe.

There is no happy ‘woof’ here. No. Only an ouch. And the story gets worse from here.

Welcome to this week’s Steak House Index update.

If you are new to my blog, or you need a refresher on the SHI10, or its objective and methodology, I suggest you open and read the original BLOG: https://www.steakhouseindex.com/move-over-big-mac-index-here-comes-the-steak-house-index/

Why You Should Care: The US economy and US dollar are the bedrock of the world’s economy.

But is the US economy expanding or contracting?

Expanding … FED rate increases notwithstanding! At the end of Q2, 2023, in ‘current-dollar‘ terms, US annual economic output rose to an annualized rate of $26.84 trillion. After enduring the fastest FED rate hike in over 40 years, America’s current-dollar GDP still increased at an annualized rate of 4.7% during the second quarter of 2023. Even the ‘real’ GDP growth rate was strong … clocking in at the annual rate of 2.4% during Q2. No wonder the FED is concerned.

The world’s annual GDP first grew to over $100 trillion in 2022. According to the IMF, in June of this year, current-dollar global GDP eclipsed $105 trillion! IMF forecasts call for global GDP to reach almost $135 trillion by 2028 — an increase of more than 28% in just 5 years.

America’s GDP remains around 25% of all global GDP. Collectively, the US, the European Common Market, and China generate about 70% of the global economic output. These are the 3 big, global players. They bear close scrutiny.

The objective of this blog is singular.

It attempts to predict the direction of our GDP ahead of official economic releases. Historically, ‘personal consumption expenditures,’ or PCE, has been the largest component of US GDP growth — typically about 2/3 of all GDP growth. In fact, the majority of all GDP increases (or declines) usually results from (increases or decreases in) consumer spending. Consumer spending is clearly a critical financial metric. In all likelihood, the most important financial metric. The Steak House Index focuses right here … on the “consumer spending” metric. I intend the SHI10 is to be predictive, anticipating where the economy is going – not where it’s been.

Taking action: Keep up with this weekly BLOG update. Not only will we cover the SHI and SHI10, but we’ll explore “fun” items of economic importance. Hopefully you find the discussion fun, too.

If the SHI10 index moves appreciably -– either showing massive improvement or significant declines –- indicating growing economic strength or a potential recession, we’ll discuss possible actions at that time.

The Blog:

The price of WOOF stock is down more than 58% this year. As interest rates went up, the Petco stock price went down. A lot.

Today, the ‘market capitalization’ of Petco is about $1.17 billion. Yes, the total value of all the publicly traded stock is significantly less than the amount they owe on their long-term debt reflected on their July 29, 2023 balance sheet. More than $400 million less, to be more precise.

Back in February, when the stock traded north of $12 per share, the company’s market cap was more than $3.6 billion. Trading today at $3.80 per share, the market cap is less than the long-term debt owed.

Under the ‘traditional’ definition of insolvency, Petco is solvent. They can pay their debts. From that same balance sheet mentioned above, they had over $1 billion in ‘current assets’ on the books. And their total assets of over $6.6 billion exceeds their total liabilities of $4.2 billion.

But stock market investors, apparently, aren’t buying the “everything’s fine” story. They are worried. Today, the value the company, as measured by the value of all it’s common stock in the aggregate, is far less than the $2.4 billion “shareholder equity” on the July balance sheet. In fact, today’s market cap is less than 1/2 that amount.

But as the Steak House Index is not a Petco blog … you may be wondering what this deep dive into a can of cat food has to do with economics? Here we go ….

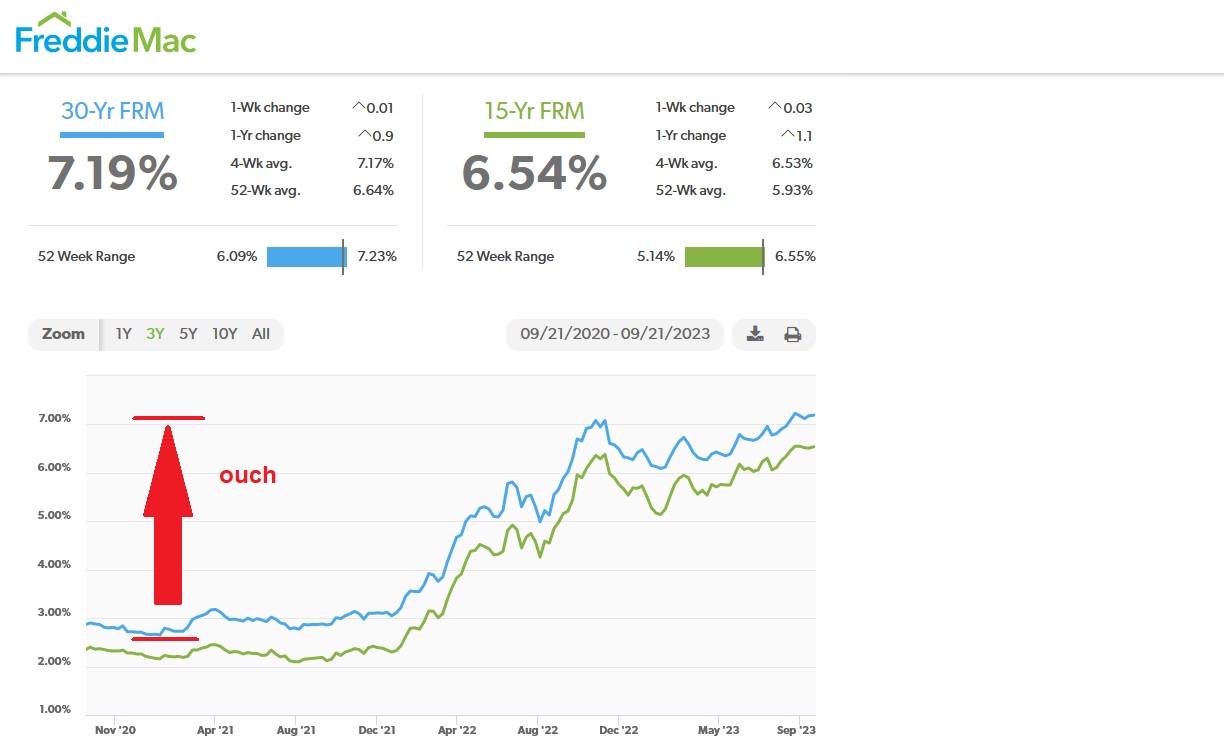

Interest rates are way up from 2 years ago. If you’ve borrowed money lately you have personally experienced this reality. As of 9/21/23, the “US weekly average” (conforming) home-loan interest rate, according to Freddie Mac, was up to 7.19%. Here’s a 3-year rate chart:

And housing debt rates are cheap compared to today’s corporate debt rates. Of course, these rates are all over the map since some companies — take Microsoft for example — have triple-A ratings from the big credit rating agencies Fitch, Moody’s and S&P. But companies like Petco are not AAA rated. In June of 2022, S&P upgraded Petco’s senior, secured corporate debt one level up to a ‘B+’. However, this level is still one below ‘investment grade’ — in other words, Petco’s senior debt is still considered “highly speculative” by the S&P rating agency. In simple jargon, their debt is known as “junk.” Of course, senior corporate debt issued by Microsoft is considered “Prime” … you know, much like the best beef grilled up in our expensive eateries? Yep, prime. It doesn’t get any better than Prime.

Credit agency ratings matter. They directly impact the interest rate an entity must pay to borrow money. It doesn’t matter if the rating we’re talking about is a personal FICO score, a corporate bond rating, or a sovereign debt rating. The edict — whatever it is — from Fitch, Moody’s and S&P will always determine the interest rate an entity can borrow at.

Which is why is pains me deeply — and should pain you too — that America’s credit rating is no longer AAA. No, sorry folks, but Microsoft has a higher credit rating than Uncle Sam. And so does Canada … home of the Looney. (That’s the $1 coin issued in Canada.)

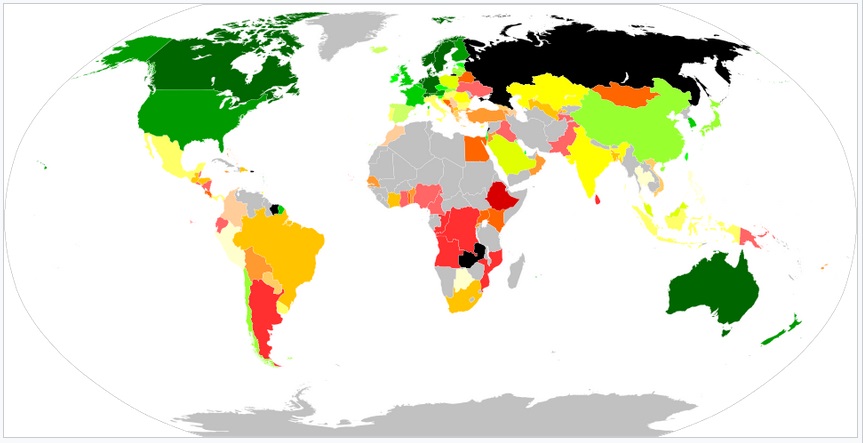

In fact, according to S&P, there are 11 countries around the globe with the AAA credit rating. The debt issued by these 11 sovereign entities is considered ‘Prime’ by S&P. The United States is one notch lower. Same on the Fitch rating scale. Only Moody’s still has the US rated as Prime. Who are the 11? Here’s the list, courtesy of Wikipedia:

Yes, that’s us at the bottom. With our ‘AA+’ rating. According to S&P and Fitch, America is no longer Prime. We are only ‘high grade.’ At best, we are ‘Choice’ beef … and even worse, the US is now on ‘negative’ credit watch!

What does that mean? It means some of the credit agencies are considering lowering our credit rating again! America, with it’s greatest economy in the world, is on negative credit watch. Ouch.

And why, you ask, is the US credit rating on negative watch? We all see it every day: The dysfunction in Washington DC. Our massive and ever-growing public debt, the result of America’s annual budget deficit. Whether you are a devout Republican, Democrat or “other” party believer, this is an America issue … and an American problem.

And once again, the issue is exacerbated yet again by America’s latest ‘fiscal cliff’ — the failure of Congress and the Senate to pass the 12 ‘spending’ bills before the end of the current fiscal year — which occurs 2 days from now. On October 1, 2023, America’s new fiscal year begins. If this issue is not resolved on or before Sunday, in theory “America shuts down.”

And this is the problem. The credit agencies are fed up with America’s dysfunction. And, over time, that ire reflects itself as a lower bond rating. I mean, one notch lower than our current S&P AA+ rating places us at the same credit rating as Abu Dhabi! Really?

A lower credit rating almost always translates to a higher borrowing cost. If you own US Treasuries, this fact may make you gleeful. But if you are an American citizen, you should be upset. Over the long haul, a lower credit rating will cost each of us an awful lot more interest. ‘Billions and Billions,’ as Carl Sagan was known to say.

Do we have easy solutions to solve the US debt issues? Certainly not. This is a great and complex nation, with a long history, plenty of disagreements, and many divergent interests. But in the final analysis, we must. In the immortal words of Benjamin Franklin:

“We must, indeed, all hang together or, most assuredly, we shall all hang separately.”

Essentially, this is what the credit agency firms are telling our politicians: Figure it out. Solve the problems. Together, we must find sustainable solutions.

Let’s see how the Prime beef is grilling up over at the steakhouses.

Not bad … this week’s SHI10 is looking strong. It’s interesting to note reservation demand at our expensive Orange County steak houses continues to slip a bit. Does this mean the ‘well heeled’ folks in the most expensive housing market in the United States are feeling a bit peaked? Reservation demand remains quite strong, of course, but we are definitely seeing signs of weakness in demand.

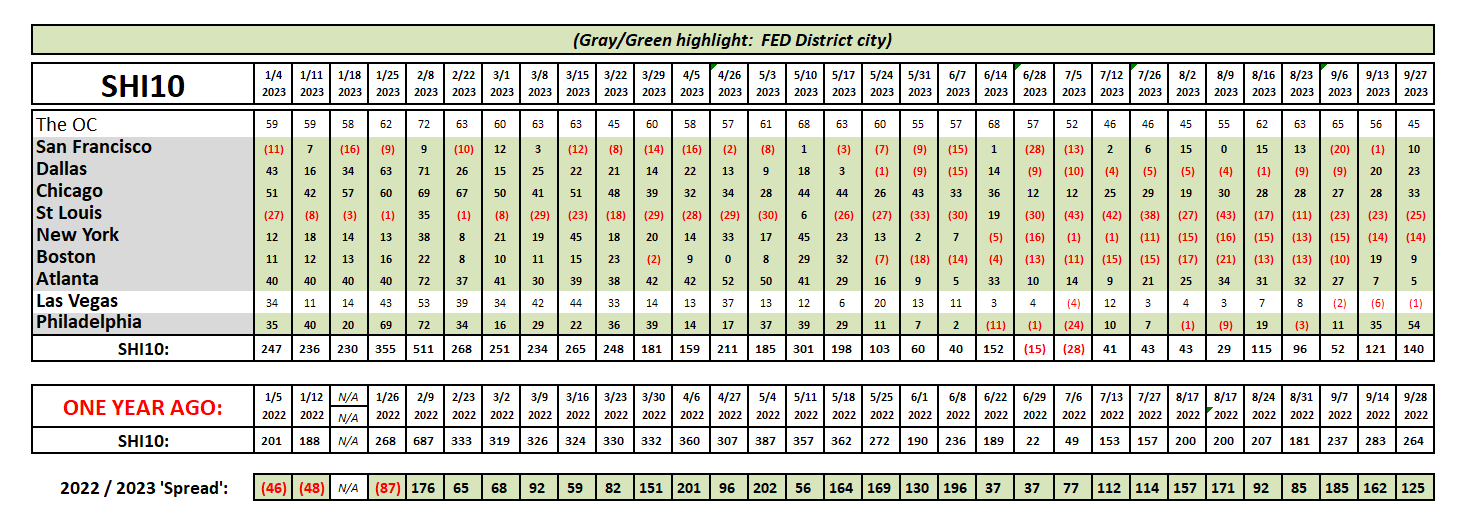

Here’s the long term chart:

Most SHI markets were very stable this week. Nothing exciting here, folks.

Earlier this morning, the Bureau of Economic Analysis released their final Q2, 2023, GDP report. In the second quarter, GDP grew at the annual rate of 2.1%. Nice. In current-dollar terms, the increase was 3.8%. Corporate profits saw an upward revision of $17.5 billion from the prior estimate.

My longer term concern about DC dysfunction and debt issues aside, the US economy is chugging along right now. Of course, there are plenty of things to worry about. No shortage. But for now, keep doing what you’re doing. It should work. 🙂

And write or call your Congressman. Let’s keep America running beyond Sunday and deny S&P any more fodder for their potential credit downgrades. We all deserve better.

<>-:-<> Terry Liebman