SHI 11.10.21 – Have You Heard About Inflation?

SHI 11.3.21 – “The Tales of my Demise …

November 3, 2021

SHI 11.14.21 – Looking at the Numbers

November 17, 2021

Of course you have. Everyone has. Because talking about inflation is today’s favorite economic activity.

After attempting to stoke inflation every year since The Great Recession of 2008, the US has finally done it. For more than a decade, the official US inflation rate was far below the 2% target. Until now. Now, for the first time in many years, the official inflation rate is significantly above the FEDs target. Oops. So, many investors and economists are now asking:

“

Is it Transitory or Not?“

“Is it Transitory or Not?“

Great question. Here’s my answer: It all depends on your definition of the word ‘transitory.’

Welcome to this week’s Steak House Index update.

If you are new to my blog, or you need a refresher on the SHI10, or its objective and methodology, I suggest you open and read the original BLOG: https://www.steakhouseindex.com/move-over-big-mac-index-here-comes-the-steak-house-index/

Why You Should Care: The US economy and US dollar are the bedrock of the world’s economy.

But is the US economy expanding or contracting?

Expanding. Significantly. In fact, in the 6 months of Q2 and Q3, growth nominal terms exceed $1.1 trillion of economic activity. The world’s annual GDP is expect to end 2021 near about $93 trillion. Annualized, America’s GDP settling in at $23.17 trillion — still around 25% of all global GDP. Collectively, the US, the euro zone, and China still generate about 70% of the global economic output. These are your big players.

The objective of this blog is singular.

It attempts to predict the direction of our GDP ahead of official economic releases. Historically, ‘personal consumption expenditures,’ or PCE, has been the largest component of US GDP growth — typically about 2/3 of all GDP growth. In fact, the majority of all GDP increases (or declines) usually results from (increases or decreases in) consumer spending. Consumer spending is clearly a critical financial metric. In all likelihood, the most important financial metric. The Steak House Index focuses right here … on the “consumer spending” metric. I intend the SHI10 is to be predictive, anticipating where the economy is going – not where it’s been.

Taking action: Keep up with this weekly BLOG update. Not only will we cover the SHI and SHI10, but we’ll explore “fun” items of economic importance. Hopefully you find the discussion fun, too.

If the SHI10 index moves appreciably -– either showing massive improvement or significant declines –- indicating growing economic strength or a potential recession, we’ll discuss possible actions at that time.

The Blog:

Everyone is talking about inflation. Well, maybe not everyone. I suspect football fans are talking about football. But here at the Steak House Index, we don’t talk football. We talk about finance and economics. And if you talk finance or economics, you’re talking about inflation.

The almost-20 year chart to the right says it all: “Talk” is way up. The year-over-year change in mentions of the word “inflation” is quite substantial. This chart measures the YOY change in mentions during S&P 500 earnings calls.

How often has the word ‘inflation’ been uttered in the media during the past 6 months? The number must be tens of millions. The media can’t get enough of the word … or the topic … often suggesting that inflation today is reminiscent of the surge America experienced in the 1970’s, that today’s inflation “problem” may usher in the same economic malaise, called “stagflation”, that wrapped around our economy, like a wet blanket, about 50 years ago.

The financial media’s appetite for inflation talk appears insatiable. Today’s CNBC headline:

Inflation Rises at FASTEST PACE in 30 years!

30 years?!? That certainly gets your attention, right?

With all the dialog in the media, and S&P500 earnings calls, you probably would not be surprised to learn that “inflation” is one of the top 100 searched words on Google. After all, if all the “pros” are talking about it, people must be worried and must be researching the topic, right?

Well, no, it turns out that while the general public is worried about inflation, they are not researching the word on Google. According to Infidigit, an SEO services company, the top 2021 Google search — both here in the US and globally — is youtube.

Globally, thru September 2, 2021, the phrase “youtube” was searched 1,361,079,416 times. Yes, that’s billion with a “b.” Amazing. By that date, in addition to youtube only a few words/phrases exceeded 500 million Google searches: Facebook, google, gmail, and ‘whatsapp web.’ It’s easy to see what’s important to the general public. And it is clearly not economics or inflation. 🙂

Are you curious about the “top 100 search” list? Take a look … I found it rather interesting:

https://www.infidigit.com/blog/top-google-searches/

But the consumer, when asked if they are worried about inflation, generally does answer “yes.” Consider this press release from the US Conference Board on the topic of “consumer confidence:”

“Consumer confidence improved in October, reversing a three-month downward trend as concerns about the spread of the Delta variant eased,” said Lynn Franco, Senior Director of Economic Indicators at The Conference Board. “While short-term inflation concerns rose to a 13-year high, the impact on confidence was muted. The proportion of consumers planning to purchase homes, automobiles, and major appliances all increased in October—a sign that consumer spending will continue to support economic growth through the final months of 2021. Likewise, nearly half of respondents said they intend to take a vacation within the next six months—the highest level since February 2020, a reflection of the ongoing resurgence in consumers’ willingness to travel and spend on in-person services.”

Why isn’t the consumer more worried about inflation? I discussed my answer in my last blog: The American public is flush with savings, has historically low credit card balances, and very cheap mortgages. Sure, many products and services are more expensive today. Supply shortages have made many either less or completely unavailable, which, in turn, pushes up prices.

For the first time in decades, many large US corporations have “pricing power.” Which simply means they are now able to pass thru operating expense increases to the consumer. Why now? Again, the consumer is flush. So there’s are renewed willingness to pay up for that “pre-owned” car, a hotel room, or a can of cat food. This is new. For more than a decade, companies have found the consumer to be resistant to price increase. Not any more. Today, the consumer is demonstrating a willingness to pay more. How much more? Time will tell. But for the moment, price does not seem to be an object. Perhaps like inflation itself, corporate pricing power, too, is transitory? 🙂

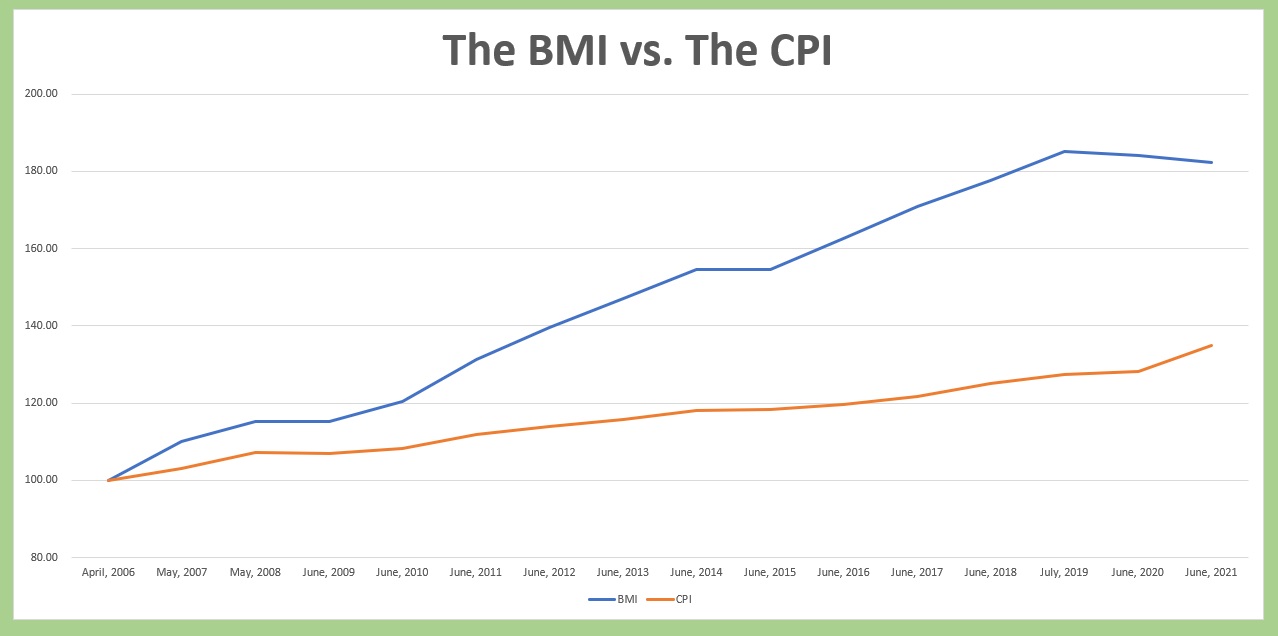

Ironically, McDonald’s appears to have had pricing power for years. It turns out that the Big Mac Index (BMI), which was originally designed to track international currency relationships, is a great historical repository for Big Mac prices! Who knew!

Sink your teeth into this chart, showing the historic relationship between Big Mac prices over the past 15-years and the Consumer Price Index over the same period :

I’ve converted both price histories into a “index” with April, 2006 pegged at “100.” Since 2006, the price you would have paid for a Big Mac here in the US has increased from an index reading of 100 up to an index of 182 — a more than 80% increase. Back in April of 2006, you could buy a Big Mac for $3.10. In July of 2021, you would pay $5.65 for the same delectable sandwich. During the identical time period, the CPI increased only 35%. McDonald’s has been success in raising the price of the Big Mac at more than double the rate of inflation. Is this the result of McDonald’s pricing power, or the unique allure of the Big Mac? The economic principal of substitution states:

The principle of substitution states that the upper limit of value tends to be set by the cost of acquiring an equally desirable substitute, assuming no untimely delays.

Apparently, there is no substitute for the Big Mac. When you gotta have one, you gotta have one! 🙂

Time for a trip to the steakhouses?

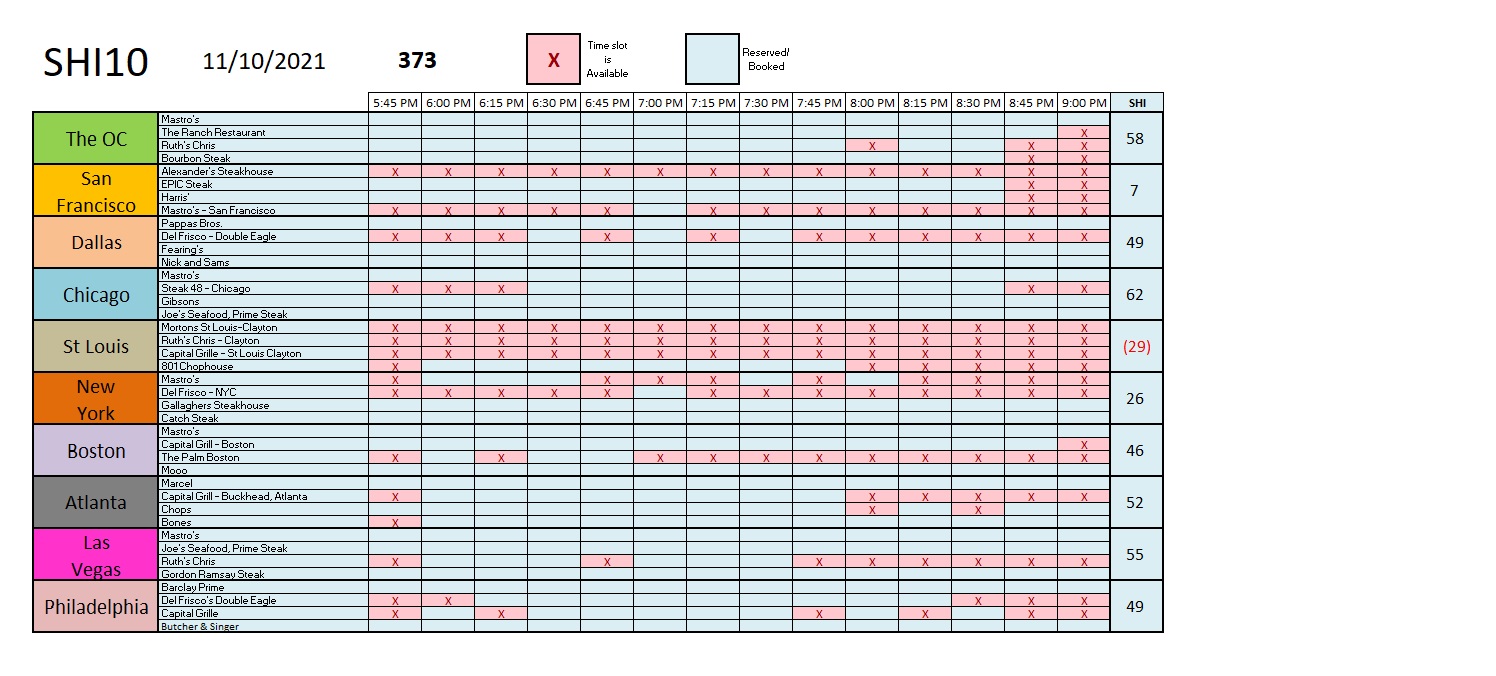

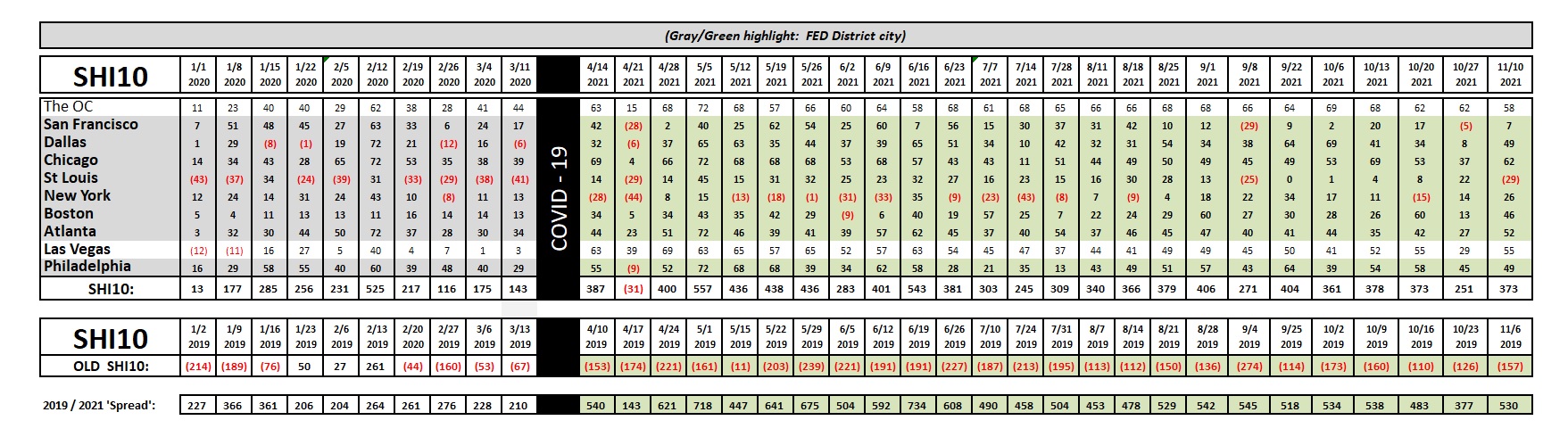

This week, the SHI10 reflects generally strong reservation demand for Saturday evening at our opulent eateries. For some odd reason, demand is quite weak in St Louis on Saturday night. When I post the trend chart below, you’ll notice St Louis fell off a similar demand cliff about 6 weeks ago. Weather? Football game? I have no idea. But it is for this reason that the longer-term trend chart is more indicative. Expensive steak house demand remains weak in San Francisco. Here’s the trend chart:

The “2019/2021 Spread” suggests that the SHI10 is back on its trend-line. A spread near 500 points seems to be the “norm” for today’s economy. For now. 🙂

Let’s return to my original question: Is today’s excessive inflation a transitory phenomenon … or should we expect high inflation to be with us for quite a while?

Let’s start here: What is the definition of “transitory?”

Searching the web, “not permanent” was one result. Another, from the folks at the Merriam-Webster on-line dictionary, is “lasting only a short time.” Well, that doesn’t help at all, now does it? What does a “short time” mean? A minute … a week … a month … a year? Clearly this qualitative term is highly variable. Which is why it is somewhat helpful to have Chairman Powell’s comment from just last week. When asked for his definition of ‘transitory,’ here is what he said:

“Transitory is a word that people have had different understandings of. For some, it carries a sense of short-lived. And that’s – you know, there’s a real time component measured in months, let’s say. Really, for us, what transitory has meant is that if something is transitory, it will not leave behind it permanently or very persistently higher inflation.

So that’s why we took a step back from transitory. We said expected to be transitory, first of all, to show uncertainty around that. We’ve always said that, by the way, in other contexts. We just hadn’t done it in the statement, but also to acknowledge, really, that it means different things to different people.”

Right. Hmmm….once again, not overly definitive.

But I think our take-away is this: Powell and the FED continues to believe that the inflation rate will not remain persistently high. We have a historical example of persistently high inflation: Inflation was persistently high in the late ’60s, the entire decade of the 1970s, and into the 1980s, at which time the FED raised interest rates into the mid-teens. Thus, I believe ‘persistently high’ would be defined as more than one year — perhaps even 18 months. If we’re still experiencing CPI and PCE inflation above 5% a year from now, then it might be time to worry. For now, I continue to believe today’s rather high inflation rates are transitory.

<:> Terry Liebman