SHI 11/8/17: Why Columbus Really Left Spain

SHI 11/1/17: Below the Radar

November 1, 2017SHI 11/15/17: Steaks on Plastic

November 15, 2017

It turns out, he was looking for lower interest rates across the sea.

OK, you’re right. I made that up. 🙂

But in a brand-new blog post by Paul Schmelzing, entitled “Global real interest rates since 1311,” we discover some fascinating facts. Including the fact that ‘real’ global interest rates peaked in the mid-1400s at almost 25%! Right around the time Columbus left Spain! Time to go!!!

Correlated? Yes! But we all know Chris didn’t leave Spain for that reason. Or did he? 🙂

Where did Paul find his data? What can he tell us about inflation for the past 700 years? And, more importantly, what does this data tell us about the future for interest rates? Let’s take a look.

Welcome to this week’s Steak House Index update.

If you are new to my blog, or you need a refresher on the SHI, or its objective and methodology, I suggest you open and read the original BLOG: https://www.steakhouseindex.com/move-over-big-mac-index-here-comes-the-steak-house-index/

Why You Should Care: The US economy and US dollar are the bedrock of the world’s economy. This has been the case for decades … and will continue to be true for years to come.

Is the US economy expanding or contracting?

According to the IMF, the world’s annual GDP is almost $80 trillion today.

At last count, US ‘current dollar’ GDP is almost $19.5 trillion — about 25% of the global total. Other than China — a distant second at around $11 trillion — no other country is close.

The objective of the SHI is simple: To help us predict US GDP movement ahead of official economic releases — important since BEA data is outdated the day they release it.

‘Personal consumption expenditures,’ or PCE, is the single largest component of US GDP — is typically about 2/3 of the total. In fact, the majority of all US GDP increases (or declines) usually result from (increases or decreases in) consumer spending. Thus, this is clearly an important metric to track. The Steak House Index focuses right here … on the “consumer spending” metric.

I intend the SHI is to be predictive, anticipating where the economy is going – not where it’s been. Thereby giving us the ability to take action early.

Taking action: Keep up with this weekly BLOG update. Not only will we cover the SHI, but we’ll explore related items of economic importance.

If the SHI index moves appreciably -– either showing massive improvement or significant declines –- indicating growing economic strength or a potential recession, we’ll discuss possible actions at that time.

The BLOG:

In his blog, Paul commented on his historic interest rate data sources, “We trace the use of the dominant risk-free asset over time, starting with sovereign rates in the Italian city states in the 14th and 15th centuries, later switching to long-term rates in Spain, followed by the Province of Holland, since 1703 the UK, subsequently Germany, and finally the US.”

Notice the phrase “risk-free” above? It’s a meaningful term. Debt offered by issuers where repayment is extremely likely — such as the United States Treasury debt — is considered “risk-free” today. The US Congress first authorized the issuance of government securities on August 4, 1790. So, clearly, we have no US interest rate data before that time. Thus, for data before the 1800s, Paul looked to European country debt; and, before that, to the “city-states” of Italy. (A fascinating history it itself…google it!)

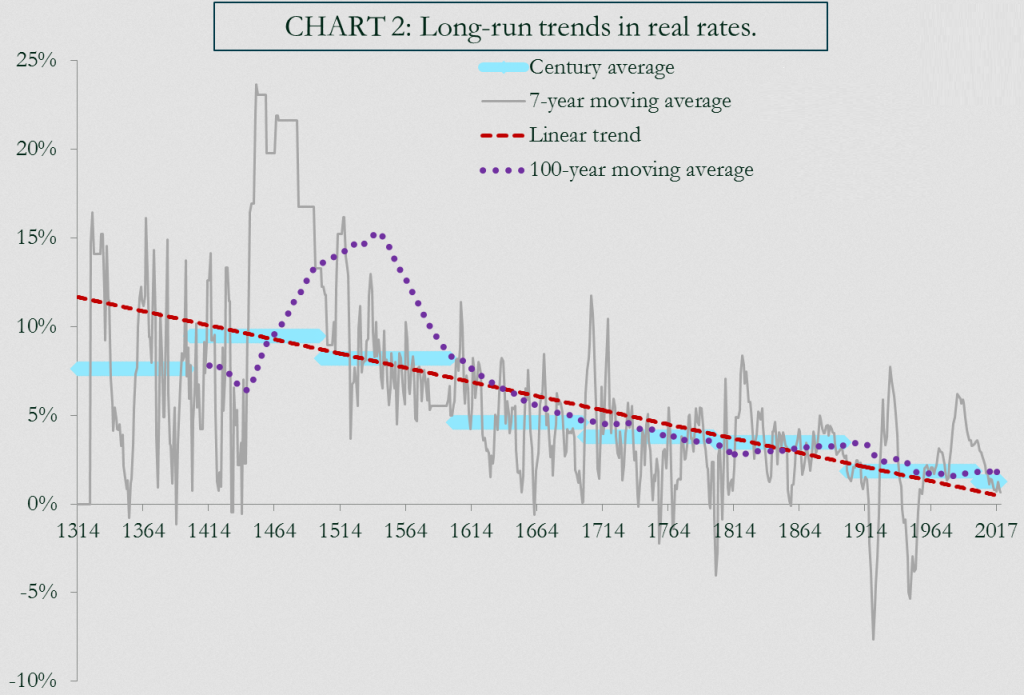

And then built the graph above, commenting the “700-year average <interest rate is> 4.78%.” Remember, this is the ‘real’ rate — the ‘nominal’ rate would be higher by the rate of inflation.

But wait. While this may be the average, a deeper dive shows the long-run trend is quite different. In fact, a regression of the 7-year average shows real rates have declined 1.6 basis points — or .016% — per year for centuries:

In his blog, Paul warns that conditions can change quickly. He suggests rates often spike rapidly after an extended low rate cycle. It’s worth noting…and worth watching for. But in my opinion — and he disagrees — this outcome is unlikely in today’s world. More fascinating, I believe, are his findings about the 700-year average of inflation and deflation:

“The 700-year average annual inflation stands at 1.09%. The 200-year average, since 1817, stands at 1.55%, with a further pickup in the 1900s. Three observations stand out:

- First, the past 60 years has been the most inflationary in our whole sample period.

- Second, current inflation rates of slightly below 2% remain fully in-line with modern times.

- Third, never before has a longer period without deflation existed than the ongoing 70-year spell since World War Two.”

Which makes one wonder: Is the FEDs goal of 2% inflation realistic? Can 2% inflation be achieved over the long-run?

The graph below, courtesy of a recent article in The Economist entitled “Gone Missing,” sums up the current global rate/inflation condition quite nicely. The small blue bar shows the “target” inflation rate in each country; the orange ‘dot,’ the current ‘core’ PCE rate in each. Countries with the highest core inflation rate top the chart, the lowest are at the bottom. What does this tell us?

Simply this: At a time when almost every developed nation is experiencing economic expansion, core inflation remains quite muted. And, in fact, current inflation rates are well aligned with the 200-year average observed by Paul Schmelzing.

Against this backdrop, can the FED and their brethren in other central banks push the core inflation rate up to 2%? An excellent question, no? Because the inflation rate always impacts interest rates. For example, back around the time Mr. Columbus decided to cruise to the New World, inflation was in the low-teens. In the middle of the 15th century, the inflation rate approached 13%, according to Paul Schmelzing. (The US has seen higher inflation rates for brief periods: In both 1880 and 1918, the inflation rate was about 20%. Ouch. It was the persistence of inflation that pushed then-FED Chair Volcker to dramatically increase FED interest rates in 1979.)

Possibly more important than the actual rate of inflation at a given moment in time may be general inflation expectations. Expectations drive behavior; many economists believe inflation expectations are an excellent forward-indicator for future inflation. And what are today’s inflation expectations? According to the Cleveland FED, and the St. Louis FEDs economic model, FRED, the 10-year future inflation rate expectations are low by historic standards. Here are the latest comments from both:

Latest Inflation Expectations Model Release (October 13, 2017)

“The Federal Reserve Bank of Cleveland reports that its latest estimate of 10-year expected inflation is 1.89 percent. In other words, the public currently expects the inflation rate to be less than 2 percent on average over the next decade.”

10-year Breakeven Inflation Rate

“As of 11/6/17, the 10-year breakeven inflation rate is 1.86%. The breakeven inflation rate represents a measure of expected inflation derived from 10-Year Treasury Constant Maturity Securities and 10-Year Treasury Inflation-Indexed Constant Maturity Securities. The latest value implies what market participants expect inflation to be in the next 10 years, on average.”

The clear conclusion: Inflation expectations, for the next 10-years, are well anchored. Suggesting that the actual inflation rate is likely to remain near its current level, thereby further adding further support for low long-term interest rates for the foreseeable future.

Let’s turn our attention to the SHI. And see if we can dine at Mastros Ocean Club this Saturday with our 3 best friends.

Well, on the ‘good news’ side of the ledger, yes we can! But, unfortunately, we can’t get a reservation until 9:45pm — which is 10:45 in ‘pre-DST’ time — and I’ll be fast asleep! The SHI is a bit stronger this week, only 9 points off this same week last year:

Once again, Mortons and The Capital Grill are completely available. But Ruths’ Chris does have three (3) completely booked time slots. You may recall from last year, seasonality should start to impact reservation levels. In 2016, the SHI peaked at 57 on December 21st. I’ll be curious to see if we see a similar trend this year. Here is our longer term trend analysis:

Summing up, from an economic perspective we find ourselves in a somewhat unique place today.

Our current economic expansion continues, unabated … albeit at a historically slow pace. All developed nations, too, are enjoying an expansionary economy.

Corporate earnings are strong, US corporate tax cuts are on the horizon, and while the FED is very likely (actually, I would predict 100% likely) to raise the funds rate in December, in general, economic conditions remain accomodative.

The unemployment rate is extremely low, by historic standards, and yet inflation — and inflation expectations — remain well grounded. Below the FED target rate.

Against this backdrop, one might expect to see a more rapid expansion of US GDP. Yet while equipment capital investment has grown meaningfully in the past two calendar quarters consumer spending has not, according to the most recent report from the BEA. As I’ve discussed in previous blog posts, I believe the US has a structural GDP growth rate ceiling imposed by the growth rates of the civilian labor force (CLF) and productivity. And while productivity has shown recent signs of improving, the civilian labor force has not — in fact, the CLF shrunk by 765,000 folks between September and October. Hmmm….

Last quarter’s GDP growth rate of 3% per annum was excellent. But I don’t think it will be repeated this quarter. The SHI, of course, at present agrees. The SHI is suggesting a growth rate nearer to 2%. We’ll continue to watch and see how conditions develop this quarter.

But for now, everything economic is looking quite rosy!

- Terry Liebman