SHI 12.1.21 – Money Talks

SHI 11.24.21 – It Takes A Lot of Power …

November 24, 2021

SHI 12.8.21 – People Wanted, Apply Within

December 8, 2021

“Talk is cheap … ”

Or, at least, it used to be. No longer. “Talk,” or more accurately, the current trend on college campuses to prevent free speech, is costing some universities millions in donations. According to the Wall Street Journal, some college alumni are withholding cash donations because of a “declining tolerance toward competing viewpoints.” Fascinating.

“

Is Free Speech still Free?“

“Is Free Speech still Free?“

It appears the answer is no. Free speech is neither free, nor is it free. I’m not stuttering, being difficult or redundant: Per the WSJ, free speech on many college campuses is an endangered species. A survey that covered more than 37,000 students at 159 different colleges found that 80% “self-censor” at least some of the time, carefully calibrating their comments depending on who is listening. Consider this quote from the article:

“The poll found that 66% of students said it is acceptable to shout down a speaker to prevent him or her from speaking on campus and 23% say it is acceptable to use violence to stop a campus speech.”

Wow. As a big supporter of vigorous intellectual debate, I am shocked. I fail to understand why debate is a bad thing. And these attitudes are not free for another reason: Apparently, colleges and universities raised nearly $50 billion last year from outside sources. More than $11 billion came from alumni. And donations make up nearly 19% of the budget spent on students at private, four-year colleges. Denying free speech may get expensive, as alumni choose to deny donations. It is not free.

Welcome to this week’s Steak House Index update.

If you are new to my blog, or you need a refresher on the SHI10, or its objective and methodology, I suggest you open and read the original BLOG: https://www.steakhouseindex.com/move-over-big-mac-index-here-comes-the-steak-house-index/

Why You Should Care: The US economy and US dollar are the bedrock of the world’s economy.

But is the US economy expanding or contracting?

Expanding. Significantly. In fact, in the 6 months of Q2 and Q3, growth nominal terms exceed $1.1 trillion of economic activity. The world’s annual GDP is expect to end 2021 near about $93 trillion. Annualized, America’s GDP settling in at $23.17 trillion — still around 25% of all global GDP. Collectively, the US, the euro zone, and China still generate about 70% of the global economic output. These are your big players.

The objective of this blog is singular.

It attempts to predict the direction of our GDP ahead of official economic releases. Historically, ‘personal consumption expenditures,’ or PCE, has been the largest component of US GDP growth — typically about 2/3 of all GDP growth. In fact, the majority of all GDP increases (or declines) usually results from (increases or decreases in) consumer spending. Consumer spending is clearly a critical financial metric. In all likelihood, the most important financial metric. The Steak House Index focuses right here … on the “consumer spending” metric. I intend the SHI10 is to be predictive, anticipating where the economy is going – not where it’s been.

Taking action: Keep up with this weekly BLOG update. Not only will we cover the SHI and SHI10, but we’ll explore “fun” items of economic importance. Hopefully you find the discussion fun, too.

If the SHI10 index moves appreciably -– either showing massive improvement or significant declines –- indicating growing economic strength or a potential recession, we’ll discuss possible actions at that time.

The Blog:

Talk is no longer cheap nor free. If it ever was. Except here. My blog is free. You may not wish to read it, after my comments above, but it’s still free. 🙂

The spoken word has always had immense power. Whether on college campuses, at the FED, of from the mouths of politicians, the spoken word is very powerful. Thru an economic lens, this concept is clearly demonstrated thru financial market distress caused by the latest Covid “variant of concern,” appropriately called OMICRON. OOOOOOooooo! Even the name sounds ominous! And the same is true with Chairman Powell’s suggestion that the FED may “speed up the taper.” Both moved financial markets this week.

Here at the Steak House Index I work hard to separate rhetoric from fact. For example, did you know the original cost of the Big Mac was $0.45 back in 1967? Fact. Today, it sells for $3.99 here in America — a cost increase of 8.87X in the past 54 years. Which, as it turns out, is rather benign when compared to the 1967 – 2021 increase in the cost of a new home. Back in 1967, the “average price of a new home” was $14,250 … this year that cost is $408,800 — that a 28.7X increase. Sure, unlike the Big Mac, a new home today is significantly different that one from over 50 years ago. Only the Big Mac remains unchanged! This aside, had the Big Mac increased by that same factor, today it would cost almost $13.

Inflation is a funny thing. It may be that we “feel” food price inflation more than home value inflation because we deal with it multiple times each day or week. Home price inflation is something we personally confront once every 5 or 10 years. Other components, like ‘rent’ or used cars, we have to deal with more often, and so price changes here are more challenging. But food inflation is in our face every day.

And don’t get me started on the price of college tuition. OK, since you brought it up: In 1967, when a Big Mac was only 45 cents, annual college tuition at a 4-year collage averaged about $640. Today, at private colleges, that number is $37,650 — a 58.5X increase. Unlike the Big Mac, the college experience was quite different back in 1967. On campuses across America, protesters armed with free speech argued against the war in Viet Nam and many other social issues. Much like today, in fact, but without the cancel culture. 🙂

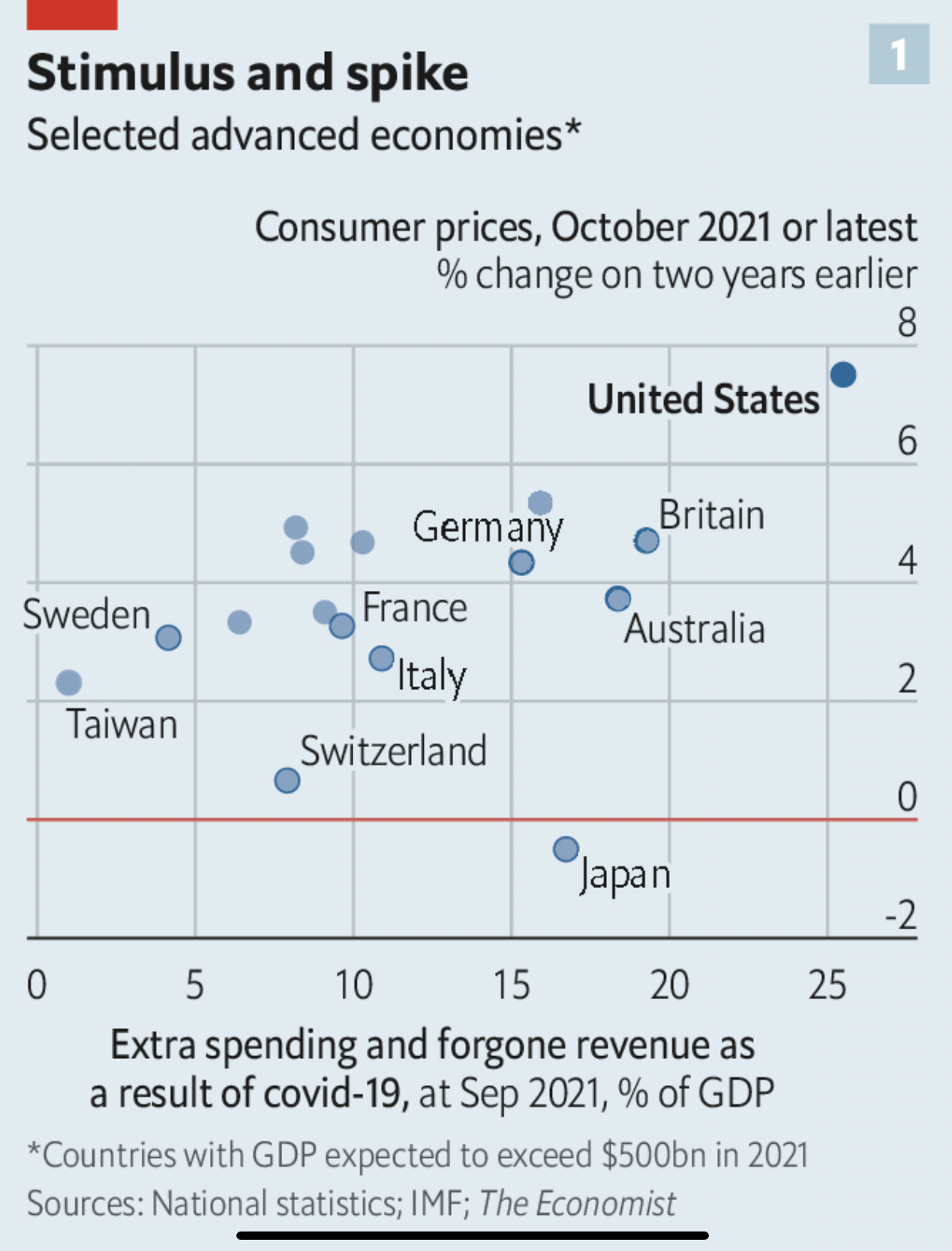

I digress. Back to inflation. I found the graphic below in a recent Economist magazine article. Take a look:

On the chart above, the vertical axis reflects a 2-year change in consumer prices. The horizontal axis measures ‘extra spending’ and ‘forgone revenue’ resulting from Covid, as a percentage of that country’s GDP. Look at the US number: More than 25%! According to this chart, the US has thrown about 25% of it’s annual GDP — or about $6 trillion or more — at the economy because of Covid. Britain, Australia, Japan and Germany aren’t far behind. These numbers are staggering. The amount of money added to the global economy in the past 2 years is unprecedented.

The article debates the question if America’s elevated inflation is the result of the massive fiscal and monetary stimulus here in the US. Jason Furman, a prior head of the President’s “National Economic Council” contends the answer is yes. Paul Krugman, a Nobel prize winner, believes the answer is no. Me? I find the debate itself humorous … because these luminaries, in my opinion, are debating the wrong question. The question is not “did American Covid spending trigger inflation in America.” The answer is obviously yes, to some degree, and is completely irrelevant to the bigger issue: A TON of fiscal stimulus, by almost every developed nation around the globe, will always ignite inflation. Remember, we’re not talking about a small amount of stimulus — the numbers in the chart above are HUGE. Pushing a TON of extra cash into the hands of consumer around to globe will ALWAYS trigger inflation. IT. IS. INEVITABLE. Any debate on this topic is economic nonsense.

It is not an economic debate … but a political one. If one has a political agenda — and it’s hard to find a public figure these days who does not — they better take up the debate, because my conclusion flies right in the face of the Modern Monetary Theorists. These are the folks who believe the US can print and spend endless amounts of money without any adverse consequences. Nope. No can do. If you fill the consumer’s pockets with cash, you’d better expect them to spend it.

No, the better question (yes, Bill, this is the better question) is: ” Why did the ‘extra spending’ and ‘foregone revenue’ in all the countries around the globe, in the aggregate, trigger differing amounts of inflation in America and other countries?”

Look at the image above once again. The vertical axis reflects the 2-year change in consumer prices. Prices are up quite a bit more in the US than in England, Australia and Germany. Then we have Japan. Even after stimulus give-aways totaling more than 16% of GDP, consumer prices declined. Huh? How is that possible?

It turns out that much — if not most — of Japan’s stimulus payments to consumers ended up in bank accounts. Savings swelled, much like they did here, but unlike here in the US, much of that government largess remains in Japanese bank accounts even today. It turns out that no matter how large a government stimulus program, if the consumer saves the money, prices remain relatively stable. Supply and demand remain in relative balance.

The article is worth a read. (right click, open in new tab)

All of which brings us back full circle to my comment above that I am a big supporter of vigorous intellectual debate. I will gladly debate anyone on this topic. Even Paul Krugman. If any of you know Paul, please feel free to forward this blog post. Hmmm … perhaps Paul is one of my 6 SHI readers? Probably not. As a Nobel prize wining economics, he has better things to do with his time than read my insignificant blog. 🙂

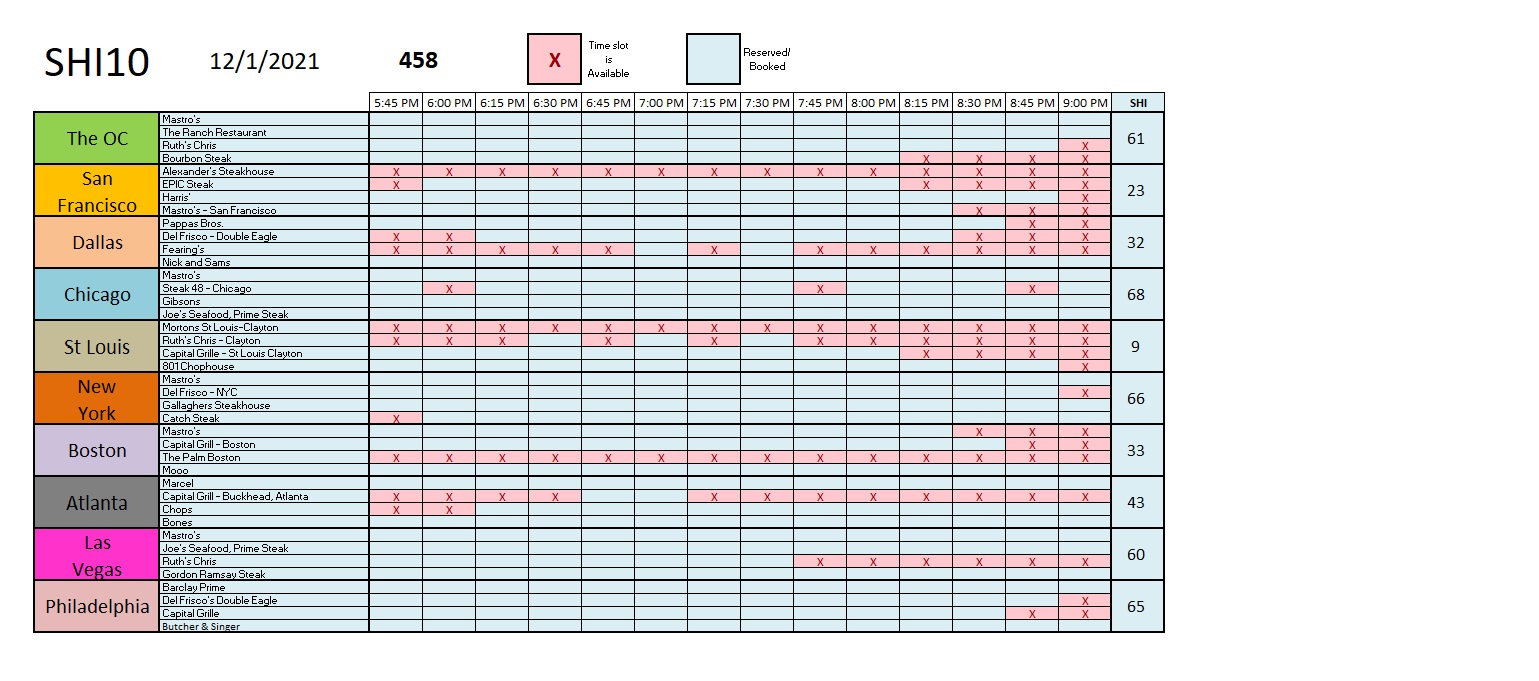

All right, let’s head to the steakhouses and see if their opinion on the economy match mine this week. Free speech may still be free in some places, but make no mistake: Steaks will cost you a pretty penny in our expensive eateries. Here this week’s SHI10:

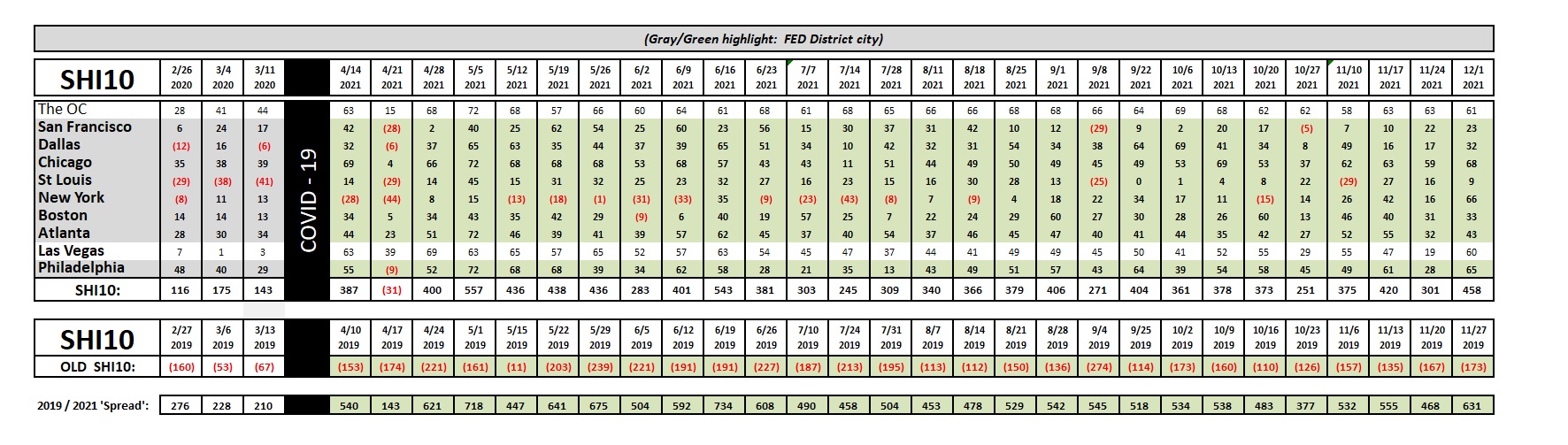

I’m guessing the Holiday spirit has infused our steakhouses because this week reservation demand is up quite a bit. Check out NYC! It will be easier to see in the longer-term trend report below, but this week NYC is hotter than a grill at Ruths’ Chris. Reservation demand remains hot in the OC, Chicago, ‘Vegas and Philly. Here the trend report:

Jumping to 458 this week from a prior reading of 301, the SHI10 reflects both strong pricey steakhouse demand and a strong US economy. The FED ‘Beige Book,’ released earlier today, reflects similar sentiment:

“Overall Economic Activity: Most Federal Reserve Districts reported that economic activity increased modestly since the previous Beige Book period. Reports on consumer spending were mixed. Some Districts noted declines in retail sales and demand for leisure and hospitality services, largely owing to the recent surge in COVID-19 cases and stricter containment measures. Most Districts reported an intensification of the ongoing shift from in-person shopping to online sales during the holiday season. Auto sales weakened somewhat since the previous report, while activity in the energy sector was said to have expanded for the first time since the onset of the pandemic. Manufacturing activity continued to recover in almost all Districts, despite increasing reports of supply chain challenges. Residential real estate activity remained strong, but accounts of weak conditions in commercial real estate markets persisted. Although the prospect of COVID-19 vaccines has bolstered business optimism for 2021 growth, this has been tempered by concern over the recent virus resurgence and the implications for near-term business conditions.”

Supply chain issues and Covid remain headwinds, but economic activity “increased modestly” regardless. Our economy remains on sound footing. Even if our universities do not. 🙂

<:> Terry Liebman