SHI 12.14.22 — The Law of Large Numbers

SHI 12.7.22 – The Most Boring Book Ever Written

December 7, 2022

SHI 12.28.22 — The Year That Was and Wasn’t

December 28, 2022

We’ve all seen the 2022 headlines:

<:> Forbes, June 13: “2 out of 3 Americans are Spending their Savings”

<:> Business Insider, Oct 4: “Americans are Running Out of Cash”

<:> Bloomberg, Nov 10: “What Happens When Americans’ Cash Runs Out”

And then there’s this one, from CNBC on November 15th:

“Household debt soars at fastest pace in 15 years as credit card use surges, Fed report says.”

The collective media is singing from the same hymnal; the message is clear: (a) the consumer is running out of money and savings, and (b) credit cards are once again in widespread use, both of which suggest that (c) if our American ‘consumer-based economy’ is the “GDP Titanic”, and a “no-cash, no credit” consumer is the proverbial iceberg, we’d better hunker down … because we’re heading right toward it. A 2023 ‘slow down’ imminent, these articles suggest, and American GDP is gonna sink like a stone? A recession, they assure us, is foretold by our collective dwindling cash reserves.

Are they right? Have Americans now spent their massive pandemic cash-hoard … and then some … and now find themselves forced to resort to credit card spending? Right before Christmas !?!?

“

Follow the money.”

“

Follow the money.”

‘Follow the money,‘ we were told with conviction in the 1976 film All the President’s Men. And that’s precisely what we’re going to do — follow the money. Large amounts of money. In fact, today we’re going to follow all of the money held by Americans as of December 9th. Because in the aggregate, these are very large numbers, and as the ‘Law of Large Numbers‘ tells us, within those numbers we will find essential truths.

And the truth, it turns out, is far different than the media’s message. The large numbers, which we will source from the FED, convincingly show that American households remain flush with cash. I believe the facts will shock you — they certainly shocked me.

Welcome to this week’s Steak House Index update.

If you are new to my blog, or you need a refresher on the SHI10, or its objective and methodology, I suggest you open and read the original BLOG: https://www.steakhouseindex.com/move-over-big-mac-index-here-comes-the-steak-house-index/

Why You Should Care: The US economy and US dollar are the bedrock of the world’s economy.

But is the US economy expanding or contracting?

Expanding. At the end of Q3, 2022, in ‘current-dollar’ terms, US annual economic output rose to $25.66 trillion. So far this year, America’s current-dollar GDP has increased at an annualized rate exceeding 7.1%. The world’s annual GDP rose to about $95 trillion at the end of 2021. America’s GDP remains around 25% of all global GDP. Collectively, the US, the euro zone, and China still generate about 70% of the global economic output. These are the 3 big, global players.

The objective of this blog is singular.

It attempts to predict the direction of our GDP ahead of official economic releases. Historically, ‘personal consumption expenditures,’ or PCE, has been the largest component of US GDP growth — typically about 2/3 of all GDP growth. In fact, the majority of all GDP increases (or declines) usually results from (increases or decreases in) consumer spending. Consumer spending is clearly a critical financial metric. In all likelihood, the most important financial metric. The Steak House Index focuses right here … on the “consumer spending” metric. I intend the SHI10 is to be predictive, anticipating where the economy is going – not where it’s been.

Taking action: Keep up with this weekly BLOG update. Not only will we cover the SHI and SHI10, but we’ll explore “fun” items of economic importance. Hopefully you find the discussion fun, too.

If the SHI10 index moves appreciably -– either showing massive improvement or significant declines –- indicating growing economic strength or a potential recession, we’ll discuss possible actions at that time.

The Blog:

The Law of Large Numbers tells us:

“As the “sample size” grows, so does the likelihood of accuracy.”

Here in America, we can’t get a larger sample size than everyone, together, in one number. In other words, if we asked every single American to share their household’s ‘balance sheet’ in a consistent format, and then added up all the the individual household numbers to create at a single balance sheet for all American households, we would have the largest number possible. But, unfortunately, such an effort is near impossible. Unless you are the Federal Reserve.

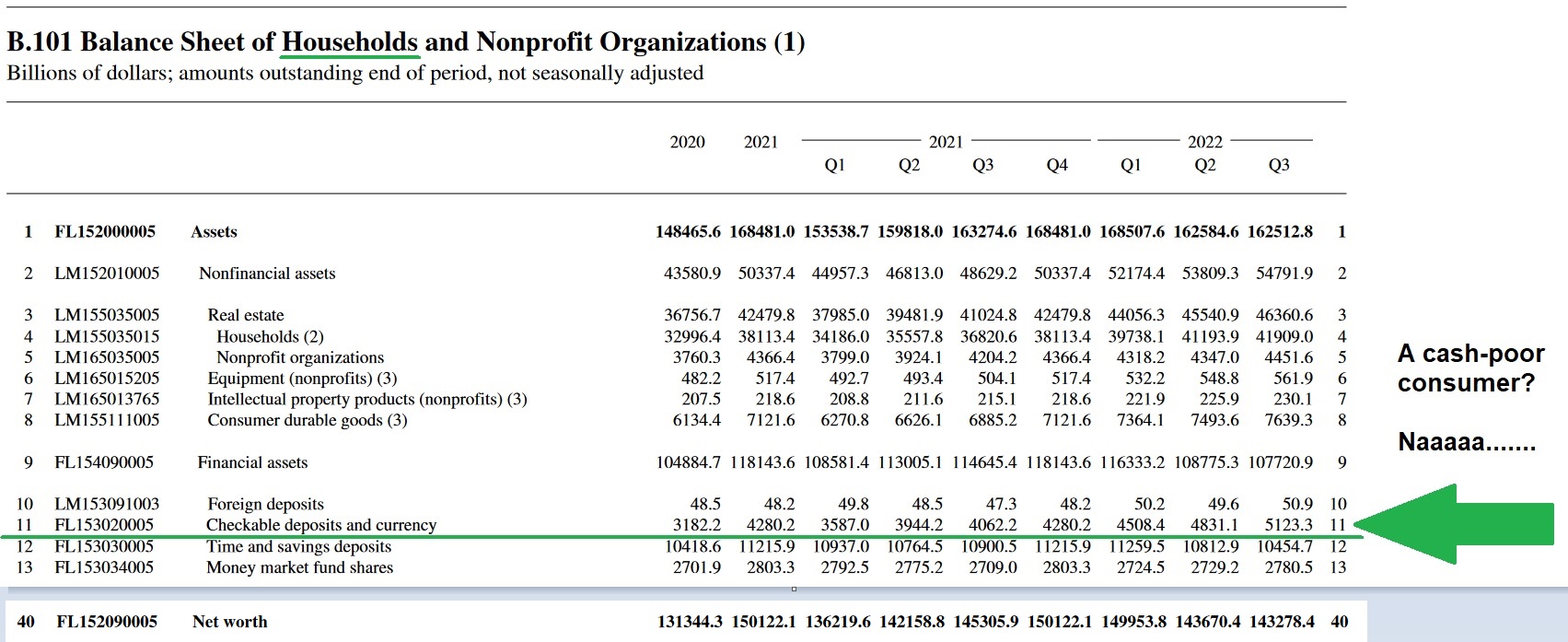

Because that’s precisely what the FED does for you and me, once a quarter, in their “Z.1 Financial Accounts of the United States” report. Considering we have over 150 million ‘households’ here in America, it’s a staggering undertaking. So when I opened the newly-minted report, about one week ago, I was shocked when I saw this:

It turns out that at the end of Q3, 2022, Americans — collectively — were absolutely flush with cash. Cash balances in ‘Checkable deposits and currency’ totaled $5.123 trillion. Compare that figure to the end-of-year in 2020, an impressive, but much smaller, $3.182 trillion. In fact, right now Americans have almost $2 trillion more than at the end of 2020!

How is that possible you ask? That question I cannot answer. I was quite surprised by this data … in fact, I was so surprised, I sent an email to the FED asking for their data source. I was surprised once again when they replied to me via email … sharing both the source and methodology of their calculations. I’m sure the Board of Governors of the Federal Reserve really don’t think much about me, my blog, or my opinion, but as near as I can tell, their data and conclusions appear accurate. 🙂

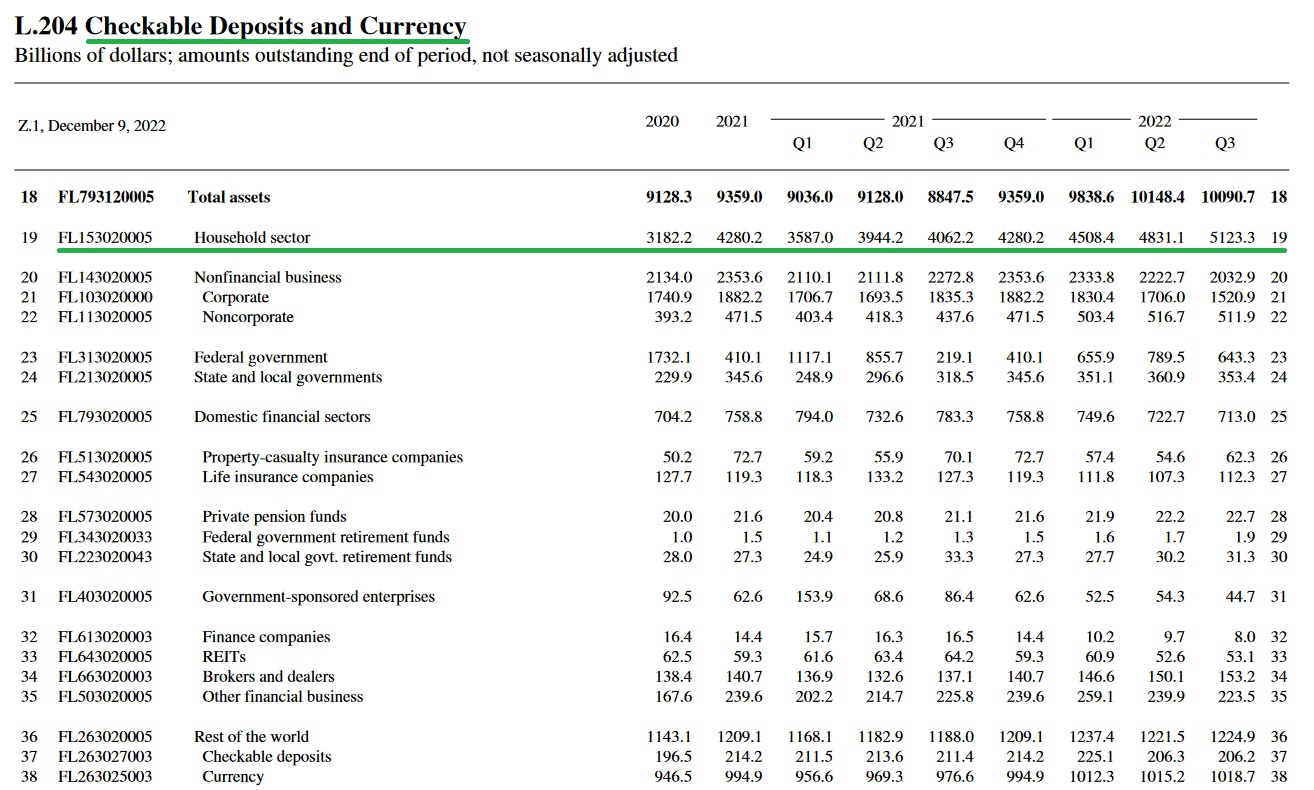

American households are flush with cash … as this additional Z.1 chart shows in more detail:

I included other ‘lines’ showing cash and deposits … for the sole purpose of showing how unique the increase in ‘household sector’ deposits truly is. No other ‘line item’ saw the same almost 60% increase during the same period. The growth in household cash is both exceptional and impressive.

Look, no one knows the future of America’s economy or GDP. But “reading the tea leaves” so to speak — as we attempt to do here at the SHI — gives us an opportunity to measure probabilities … to gain a bit more insight into possible futures. I only wish the media worked harder to use “factual tea leaves”. So often, it appears to me their objective is more to shock than to accurately report factual data.

So, are American’s running out of money? Nope. Not yet. They are still sitting on a pile of cash — an even larger pile than before! And since American ‘consumer spending’ is the foundation of American GDP growth, from this indicator alone, I feel both our economy and the steak houses are well insulated from a ‘cash-shortage’ triggered slowdown or recession.

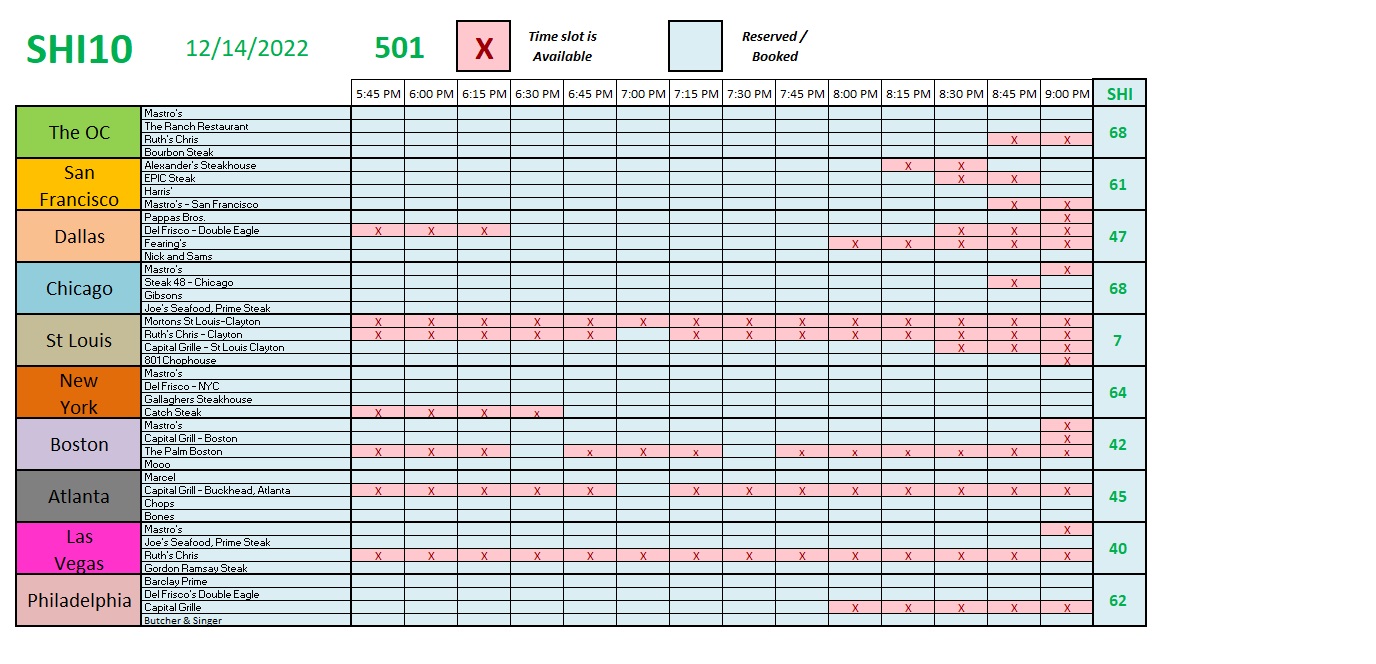

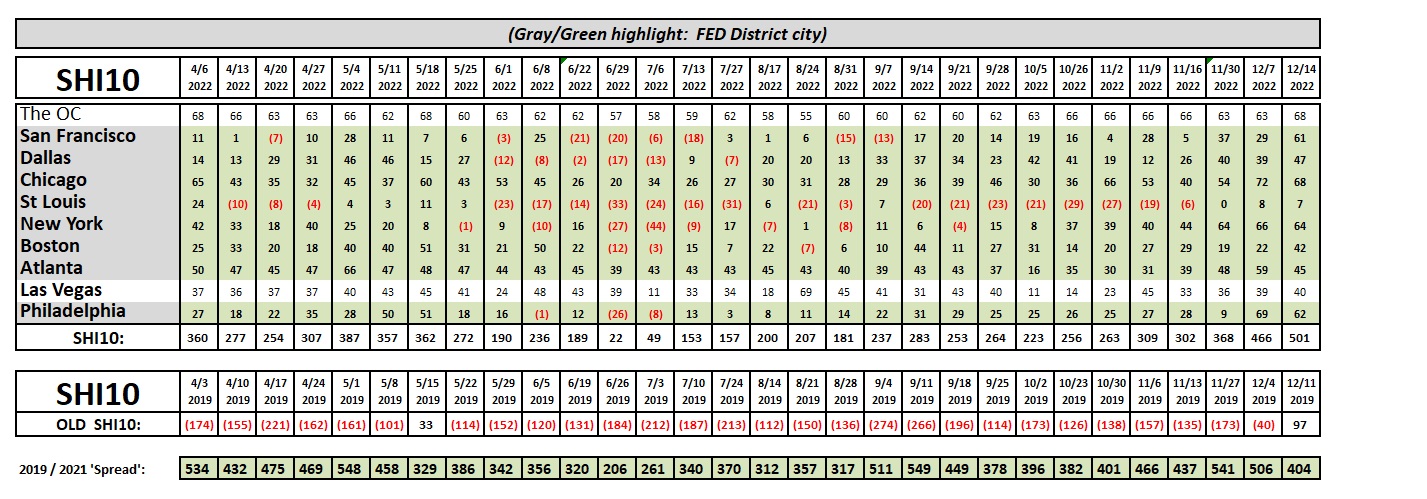

To the steakhouses! Are they flush with diners … enjoying a little holiday spurt in reservations?

It appears they are! For the second week running, every SHI city is in the green. Reservations for this Saturday are hard to find in the OC, San Fran, Chicago, and NYC, and there is only slightly more availability in Philly, ‘Vegas, Atlanta and Boston. St Louis, once again, remains weak. Here’s the longer term trend:

Measured by ‘consumer cash’ and available expensive eatery reservations, the economy continues to look robust. Which probably explains today’s “action” over at the FED.

They raised interest rates again today. Up 1/2% … to a high-water mark of 4.5% — the highest FED funds rate in more than 15 years. So notwithstanding my “cash comments” above, the FED is doing all they can to prove my optimism inaccurate. No, I was expecting a 50 basis point ‘hike’ today — but today they signaled they expect rates to “stay higher for longer” than before. In fact, in the FEDs ‘Economic Projections‘ released today with their FOMC statement, they tell us their ‘median‘ expectation is for a 5.1% Federal Funds rate at the end of 2023. Ouch. That’s harsh. I find that really hard to believe.

I don’t see it … but, hey, I don’t have 400 Economic PhDs working for me. Sure, the job market remains tight, but if inflation tapers, that’s not a bad thing. It’s a good thing to have more people employed. And inflation is tapering … slowly but surely.

So we will see how it all plays out next year. But for now, the consumer has plenty of cash to spend … and I suspect they will. It’s going to be a Green Christmas!

Expect no blog post next week. My final 2022 post will take place on the 28th. Happy Holidays!

<:-:> Terry Liebman