SHI 12.2.2020: Accelerating Trends Speed Up

SHI 11.25.2020: Gobble!

November 25, 2020

SHI 12.9.2020: The Bahamas go Digital

December 9, 2020

One of my all-time favorite Churchill quotes comes from his now famous 1942 WW2 speech after England had won an important battle, and he tells the nation, “Now this is not the end. It is not even the beginning of the end. But it is, perhaps the end of the beginning.” Fabulous. He had such a great way with words.

The world has been at war with a particularly difficult foe: COVID-19. Paraphrasing Mr. Churchill, with the vaccines soon in hand, I suggest that while we may not be at the end, we are, perhaps, at the beginning of the end of this war.

2021 will begin soon. We are all optimistic is will be far different than 2020. I believe it will. In fact, I believe 2021 will kick off “The Roaring 20’s – Take 2!” Almost exactly 100 years ago, the world was throwing off the yoke of another global pandemic and a world war. The 1920s decade that followed, the collective desire to live in the moment, throw caution to the wind, and P-A-R-T-Y ! were obvious. I believe history will repeat in the 2020s. And I believe cultural and economic trends that were beginning to take root before the pandemic will accelerate in speed and size as the new Roaring-20s begins.

“

We are, perhaps, at the beginning

of the end of this war.“

“

We are, perhaps, at the beginning

of the end of this war.“

COVID will soon be in our rear-view mirror. Get ready for the future. It’s right around the corner.

Welcome to this week’s Steak House Index update.

If you are new to my blog, or you need a refresher on the SHI10, or its objective and methodology, I suggest you open and read the original BLOG: https://www.steakhouseindex.com/move-over-big-mac-index-here-comes-the-steak-house-index/

Why You Should Care: The US economy and US dollar are the bedrock of the world’s economy.

But is the US economy expanding or contracting?

Before COVID-19, the world’s annual GDP was collectively about $85 trillion. Then it shrank … then bounced back! We can thank global fiscal and monetary policy for the bounce. According the the Q3, 2020 ‘preliminary’ numbers, annual US GDP is back UP to about $21.1 trillion. And still, together, the U.S., the EU and China continue to generate about 70% of the global economic output.

The objective of this blog is singular.

It attempts to predict the direction of our GDP ahead of official economic releases. Historically, ‘personal consumption expenditures,’ or PCE, has been the largest component of US GDP growth — typically about 2/3 of all GDP growth. In fact, the majority of all GDP increases (or declines) usually results from (increases or decreases in) consumer spending. Consumer spending is clearly a critical financial metric. In all likelihood, the most important financial metric. The Steak House Index focuses right here … on the “consumer spending” metric. I intend the SHI10 is to be predictive, anticipating where the economy is going – not where it’s been.

Taking action: Keep up with this weekly BLOG update. Not only will we cover the SHI and SHI10, but we’ll explore related items of economic importance.

If the SHI10 index moves appreciably -– either showing massive improvement or significant declines –- indicating growing economic strength or a potential recession, we’ll discuss possible actions at that time.

The Blog:

We are now writing the final chapters on the COVID-19 pandemic. Once the first, second, third, etc., vaccines are widely distributed, memories of this crisis will recede and the world will move on. COVID will have many lasting legacies, but I think none will be more enduring than the simple acceleration of trends than began long before COVID hit our shores.

General trends like automation, artificial intelligence, the IoT, etc., will pick up pace. Economic trends will also accelerate. Today, we all stand witness to the end of the “Monetary Era” and the beginning of the “Fiscal Era.” Let me explain.

First, let me talk about something that is not ending: Globalization. COVID-19 will accelerate already evolving changes, but rest assured, globalization is here to stay. In his book Ten Lessons for a Post-Pandemic World, Fareed Zakaria comments, “Human beings don’t want to stand still. Movement has been the way of the world for tens of thousands of years.” Agreed. People, and later goods and services, have moved from place to place for centuries. I have zero expectation that globalization trends will end with COVID.

In a National Bureau of Economic Research (NBER) paper from more than 20 years ago, titled “When Did Globalization Begin?” the authors commented:

“Some world historians attach globalization ‘big bang’ significance to 1492 (Christopher Columbus stumbles on the Americas in search of spices) and 1498 (Vasco da Gama makes an end run around Africa and snatches monopoly rents away from the Arab and Venetian spice traders). Such scholars are on the side of Adam Smith who believed that these were the two most important events in recorded history.”

And a few paragraphs later, the authors debunk Adam Smith’s theory, suggesting “there is no evidence supporting this view.” Perhaps. But regardless of whether these events triggered globalization, or were mere milestones along the way, globalization has been with us for eons.

This fact will not change due to COVID. No, in fact the world is growing more homogeneous.

More than a century ago, the highly regarded British historian, Lord Bryce suggested that “the exploration of this earth is now all but finished” and that “mankind is fast becoming one people.” One people? Nope, not a chance. Events of the 20th century proved that was not the case. His observation may have been somewhat accurate, but likely at least a century too early: I would argue the human inter-connectivity Bryce observed at the turn of the 19th century accelerated as the adoption of the internet accelerated. In our post-COVID world, this trend will simply speed up.

No. People will continue to move about. And countless billions of them will continue to adopt new and developing technologies. But expanding technology requires infrastructure, infrastructure requires capital, and that’s where we return to the accelerating trend in modern economics gripping the globe. We are living history right now, folks, witnessing a changing of the palace guard. Central banks are losing their position of hegemony to the rising power of the state. Governments around the globe are awakening to the fact that monetary policy – meaning asserting economic control using the primary tool of interest rates – is no longer the economic answer for most developed economies. Monetary policy will now take a back seat to reinvigorated fiscal policy.

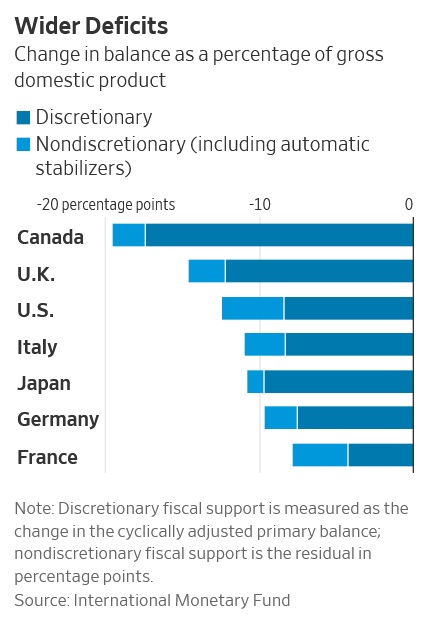

In 2020, the US ran a deficit of over $3 trillion. We might do that again in 2021. Not to be outdone, according to a recent article in the Wall Street Journal, Canada’s deficit is “growing at the fastest rate among developed nations as it seeks to prop up its economy during the COVID-19 pandemic.” That’s quite the prize. And, of course, the article states the obligatory platitude, “some economists warn the heavy spending could lead to a financial crisis.” Right. Got it.

In 2020, the US ran a deficit of over $3 trillion. We might do that again in 2021. Not to be outdone, according to a recent article in the Wall Street Journal, Canada’s deficit is “growing at the fastest rate among developed nations as it seeks to prop up its economy during the COVID-19 pandemic.” That’s quite the prize. And, of course, the article states the obligatory platitude, “some economists warn the heavy spending could lead to a financial crisis.” Right. Got it.

International Monetary Fund estimates suggest that Canadian government debt will surge to roughly 115% of GDP this year – up from just 89% last year – a fact that likely led to a recent credit-downgrade for the country. Fitch Ratings dropped Canada’s rating from AAA to AA+ in June, citing a skepticism about the ability of Canada’s political leaders to stabilize debt growth after the pandemic passes.

But Canada is not alone: The IMF now estimates global government stimulus of close to $12 trillion in response to COVID-inspired economic disruptions. The debt-to-GDP ratio in the U.S. is forecast to reach 131% by the end of 2021; 108% in the U.K.; and 73% in Germany.

And the expansion of fiscal policy and stimulus has just begun! We’re in the early innings of the ball game here, folks. Might the US experience the same credit downgrade as Canada?

Back in July, Fitch Ratings “affirmed” the AAA rating of US debt, stating, “The U.S. sovereign rating is supported by structural strengths that include the size of the economy, high per capita income and a dynamic business environment. The U.S. benefits from issuing the U.S. dollar, the world’s preeminent reserve currency, and from the associated extraordinary financing flexibility, which has been highlighted once again by developments since March 2020. Fitch considers U.S. debt tolerance to be higher than that of other ‘AAA’ sovereigns.”

So the answer appears to be no. For now. And unlike Canada – or any other country for that matter – the US dollar remains the worlds reserve currency. In fact, the prominence of the US dollar cannot be overstated. Consider this fact:

The US dollar is the underlying currency

in almost 90% of all global currency transactions.

So, against this backdrop, we will watch an accelerating trend away from the Central banks to a globally-coordinated government fiscal expansion. Like it or not, in the coming years, we will see a lot more money “sloshing around the globe,” to borrow a phrase from Ben Bernanke.

(Do you remember the now-famous 2005 speech? Here’s a link: https://www.federalreserve.gov/boarddocs/speeches/2005/200503102/ )

I can make one assertion without equivocation: Sea levels are rising. No, not the ones with water in them. I make no “climate change” comment, but I am stating an economic fact: The ocean of debt and equity capital has been rising for years. Bernanke observed this fact 15 years ago. The trend accelerated in 2020 and it will pick up pace from here. For both governments and households, in the aggregate, debt and equity levels have never been higher.

Household debt levels have never been higher. At the prior peak — the 3rd quarter of 2008 — the levels ‘housing debt’ and ‘non-housing debt‘ were both lower. You may recall that at the time many economists felt household over-leverage was the cause or, or at the minimum a significant contributor to, the Great Recession. Assuming this is true, you have to wonder if these new record levels of both housing debt and consumer debt will trigger another financial crisis? Or is this time different for some reason?

Household debt levels have never been higher. At the prior peak — the 3rd quarter of 2008 — the levels ‘housing debt’ and ‘non-housing debt‘ were both lower. You may recall that at the time many economists felt household over-leverage was the cause or, or at the minimum a significant contributor to, the Great Recession. Assuming this is true, you have to wonder if these new record levels of both housing debt and consumer debt will trigger another financial crisis? Or is this time different for some reason?

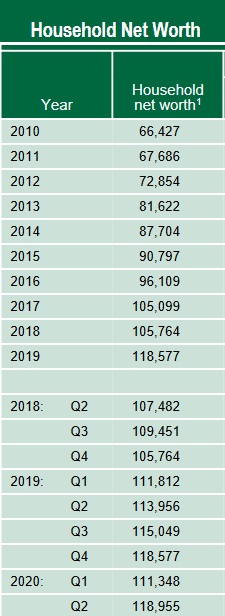

This time is different. This time, household net worth has also reached a new high point. To the right is a chart I clipped from the most recent FEDs “Z.1 Financial Accounts of the United States” report. The report I’m referencing was published on 9/21 so expect an update toward the end of December.

The “household net worth” in this case is essentially the sum of all the individual net worths’ of all Americans. Remember: Your net worth is the amount left after subtracting your total liabilities from your total assets. As of the end of 2019 (the full ‘balance sheet’ is compiled only annually), Americans had about $127.2 trillion in assets, $15.5 trillion in liabilities, and a net worth of $111.8 trillion. Two calendar quarters later, that figure was up to almost $119 trillion. That increase included:

- > $5.7 trillion increase in the value of ‘corporate equities’

- > $0.5 trillion increase in the value of real estate.

During Q3, both corporate equity values and home prices increased significantly. Said another way, in the past few months, the value of the stock markets increased significantly. Thus, I’m expecting significant improvement in the combined balance sheet of all Americans in the next Z.1 report.

But for now, let’s consider the data in the Q2 report. You, me … everyone combined, make up this particular balance sheet. In the aggregate, the balance sheet looks pretty healthy: Our debts total only about 12% of our total assets. Not bad. But at the same time, American households have never before carried this level of debt.

According to the just published update from the Federal Reserve Bank of NY and their Center for Microeconomic Data, “total household debt increased by $87 billion in the third quarter of 2020 and now stand at $14.35 trillion. Balances are now $1.68 trillion higher, in nominal terms, than the 2008Q3 peak of $12.68 trillion and 28.7% above the 2013Q2 trough.”

Further quoting the report, “Delinquency rates have dropped markedly in the second and third quarters,” partially reflecting loan forbearance from both the CARES Act and voluntarily offered by lenders. In fact, as of September 30th only 3.4% of the outstanding debt was in some stage of delinquency.

I see this outcome as nothing short of extraordinary in light of the millions of job losses. Of course, things change, and as 2020 ends, many federal support programs end as well. Without an extension, delinquencies may increase.

New housing debt drove the majority of the increase. In fact, the report states that “newly originated mortgage debt increased by $1.05 trillion in 2020Q3.” This fact makes sense in light of the surge in new- and existing-home buying activity across the country.

Which beings me to today’s point:

In my opinion, government debt levels in 2020 cannot be compared to government debt in 2000. Or 1990 … or 1980. Because interest rate levels have experienced a structural shift, decade after decade, until now, where they are close to zero in every major developed nation. And here they will remain.

Don’t get me wrong: A mountain of debt can become be a problem. In some instances, it might become impossible to handle … impossible to support. But that mountain is far smaller and manageable if the average 10-year treasury rate is 0.95% … than if the average interest rate is 9.50%. And it wasn’t that long ago that the 10-year Treasury was 9.50%. I simply contend it never will be 9.50% again. In fact, I believe a negative treasury yield is more likely than a 10% treasury rate. 🙂

And what would happen if the treasury rate became negative? Remember, the 10-year ‘bund’ rate in Germany is negative. In theory, the bigger your mountain of debt, the better off you are! Germany could borrow $1 trillion today, pay zero interest to the “lender” for 10-years, and then return $950 billion and be done. Why is Germany not borrowing trillions and trillions of euros right now? Their history constrains them … but this, too, is changing. Their reluctance to offer fiscal stimulus has waned significantly.

Let me be clear: I am NOT in support of a willy-nilly, throw-caution-to-the-wind, massive debt binge across the globe. But I am suggesting that an intelligent, surgical, use of debt to create “revenue-generating” assets might be quite prudent where the long-term benefits far outweigh costs. Today, in many developed nations across the globe, this idea is increasingly being considered.

Clearly, we’re in uncharted waters here, folks. These conditions have never before appeared. In the past, mountains of debt have always proven to be a problem. Always. Across time, mountains of debt have caused countries to collapse. But in past years, that debt had a cost known as “debt service.” Payments had to be made. But this is very different today. Today, in many countries, a mountain of debt is likely to create a net benefit for the country’s treasury. If money can be borrowed at near zero or lower rates, and those funds can be invested in infrastructure or other income-producing assets, shouldn’t countries consider borrowing and investing more?

Indeed. That trend is picking up popularity and pace.

Remember, back in September the Federal Reserve assured us that short term rates will be near-zero for years. Their Federal funds rate forecast:

- > 2020: 0.1%

- > 2021: 0.1%

- > 2022: 0.1%

- > 2023: 0.1%

In other words, at the present time, the FED expects to leave rates unchanged for more than 3 years. Once again, this has never happened before. So let me repeat that: The FED expects short-term interest rates to remain near zero for more than 3 years.

By the way, the FEDs balance sheet has grown to almost $7.22 trillion as of 11/27/20. This trend is gaining speed too.

Jason Furman is a former chief economist to President Obama and currently an economics professor at Harvard. In the final analysis, I think Jason said it best:

“It’s not important how much debt you have … what’s important is the amount of debt service.”

Welcome to the new world. The debt level no longer matters … as long as you make the payments. As monetary policy hegemony takes a pause, and global fiscal stimulus and policy take the lead, ‘debt service’ becomes the metric to watch.

My Final Comments:

Earlier today, England became the first country to authorize use of the Pfizer vaccine. The end-game begins.

Brazil’s stock market, the Bovespa, is surging this year. Today, there are 3X the number of investors as there were 2 years ago. Why? Interest rates were 14% only 4 years ago. Today, due to low inflation and a central bank rate of 2% (down from 14.25% in 2016), “fixed income” returns in the country are paltry causing many Brazilians to swap out of fixed-income into stocks for the first time ever.

Here in the US, and across the globe, massive fiscal spending combined with near-zero interest rates will fuel a continued, and continuous, surge in asset values. In my opinion, this macro trend is inevitable over the next decade or more. The new-Roaring 20s will cause asset values to spike. Homes, stocks, investment real estate, art, coins, gold …. everything. There will certainly be some exceptions, but by and large, asset values will rise as long as interest rates stay low. Which I believer is very, very likely.

- Terry Liebman