SHI 2.21.18 Buy a House

SHI 2.14.18 Happy Valentines Day

February 15, 2018

SHI 2.28.18: Fears and Beliefs

February 28, 2018

“With an estimated value of $200 trillion, across the globe, homes are collectively worth about 3X as much as all publicly traded stocks.”

This per the Economist magazine. And they have a great interactive graphic you can play with. Check it out: https://www.economist.com/blogs/graphicdetail/2018/02/daily-chart-5 (you may have to ‘copy’ and then paste this link into your browser … for some reason I can’t get the URL to remain a URL.)

When is the best time to buy a house?

- The best time to buy a house was before.

- The second best time is today.

- The third? Tomorrow.

My advice: Go by a house. Don’t wait.

Welcome to this week’s Steak House Index update.

If you are new to my blog, or you need a refresher on the SHI10, or its objective and methodology, I suggest you open and read the original BLOG: https://www.steakhouseindex.com/move-over-big-mac-index-here-comes-the-steak-house-index/

Why You Should Care: The US economy and US dollar are the bedrock of the world’s economy. This has been the case for decades … and will continue to be true for years to come.

Is the US economy expanding or contracting?

According to the IMF (the ‘International Monetary Fund’), the world’s annual GDP is almost $80 trillion today.

During the calendar year 2017, US nominal GDP increased by $833 billion … by an amount approximately equal to the market capitalization of Apple. At the end of 2017, US ‘current dollar’ GDP was about $19.749 trillion — about 25% of the global total. Other than China — a distant second at around $11 trillion — no other country is close.

The objective of the SHI10 and this blog is simple: To predict US GDP movement ahead of official economic releases — an important objective since BEA (the ‘Bureau of Economic Analysis’) gross domestic product data is outdated the day it’s released.

Historically, ‘personal consumption expenditures,’ or PCE, has been the largest component of US GDP growth — typically about 2/3 of the total. In fact, the majority of all US GDP increases (or declines) usually result from (increases or decreases in) consumer spending. This is clearly an important metric. The Steak House Index focuses right here … on the “consumer spending” metric.

I intend the SHI10 is to be predictive, anticipating where the economy is going – not where it’s been. Thereby giving us the ability to take action early.

Taking action: Keep up with this weekly BLOG update. Not only will we cover the SHI, but we’ll explore related items of economic importance.

If the SHI index moves appreciably -– either showing massive improvement or significant declines –- indicating growing economic strength or a potential recession, we’ll discuss possible actions at that time.

The BLOG:

I’m not just talking about here in the US, either. Globally, in all ‘developed economies,’ home prices are on a tear. So much, in fact, that that same Economist blog claims,

“…house prices appear to be on an unsustainable path in Australia, Canada and New Zealand. Ten years ago they reached similarly dizzying heights against rents and incomes in Spain, Ireland and some American cities, only to endure a brutal collapse….”

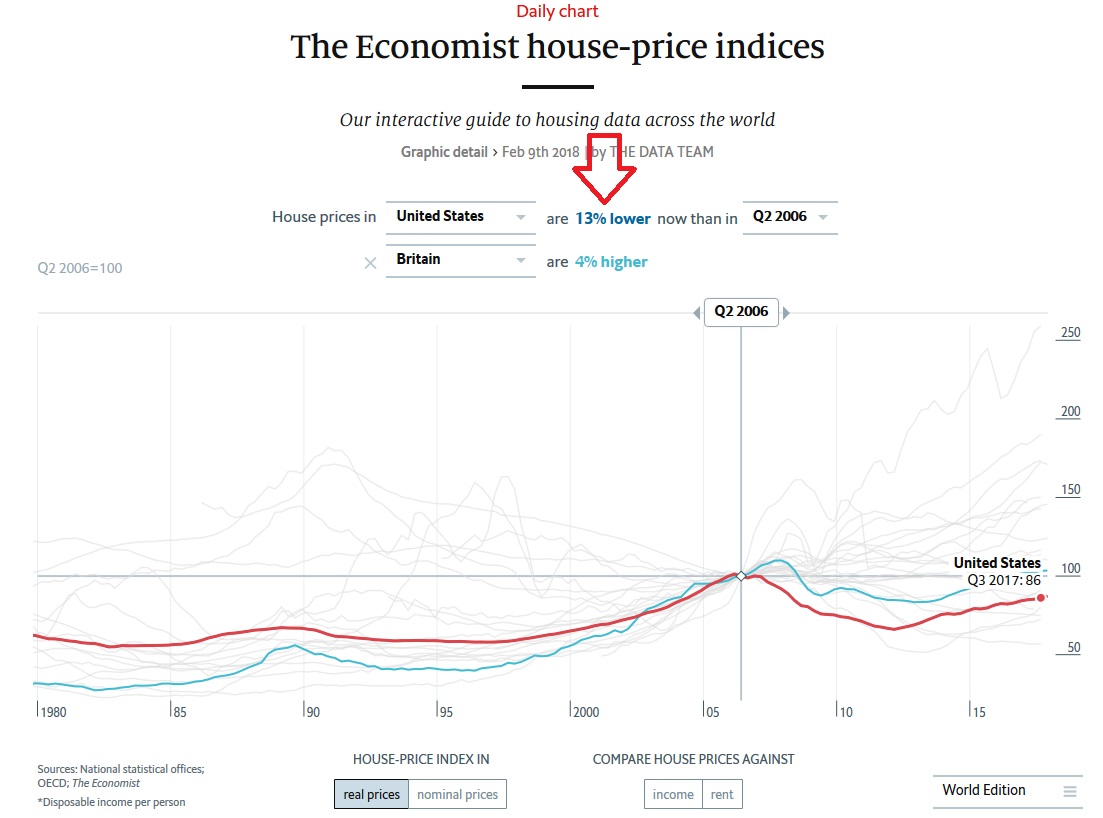

US home prices, at least in “real prices” (remember, “real” means adjusted for inflation), have yet to recover from their prior peak in Q2, 2006. In fact, as you can see below, they remain about 13% or 14% lower than peak values:

Of course, this chart uses national data, sourced from the Organization of Economic Co-operation and Development (OECD). Values in many geographic areas — especially here on the west coast — are much higher than their prior peak. But home values in many other areas have not yet recovered.

So, should you buy a house? And if yes, where?

Yes. Buy a house. I like to buy local. And I prefer to live in my house.

But if one wants an investment property, an argument can easily be made one should first identify areas where home values remain depressed and then, within this sub-set, pick one where (1) you feel the area will see economic and population growth over the next 10 or more years, and (2) where you can effectively manage income property. It’s a bit dated, but perhaps this URL may help you get started: http://www.lao.ca.gov/reports/2015/finance/housing-costs/housing-costs.aspx

Why buy a house? Here are a few reasons.

- The US housing market is very different than in Australia, Canada or New Zealand. I agree with the Economist: Their home prices are so excessively inflated, so absurdly high, one can only surmise when they will crash and prices plummet back to earth. It may take years, but I believe it will happen.

- As I said above, in many cities around the US, local housing values remains below prior peaks. Values will rise over time … as long as the area continues to expand demographically and economically.

- The US has a housing shortage. And it’s getting worse.

Yep, we need more houses. But they probably won’t be built. The reasons have more to do with regulation, building standards, land use restrictions, and fees. The problem is really not economic.

At least not in the traditional sense. Think about the problem this way: Suppose you wanted to build a typical, traditional house. You prepare your plans and submit them to the local building authority. Only to hear, “Sorry, your application to build a home is denied.” Why you ask? What did I do wrong? “Well,” the representative replies, “all new homes in our city must be built with gold bricks. Concrete is not permitted.”

Absurd, right? But as absurd as this metaphor is, it’s not that far off. Building standards here in California have added thousands of dollars to new home construction. Google “what’s the cost” of California Title 24 and you’ll get sense of what I’m talking about. Throw in land use restrictions, minimum square footage requirements, local fees, impact fees, school fees, etc., etc., etc., and you have a very expensive marketplace in which to build a new home. Gold bricks might be cheaper.

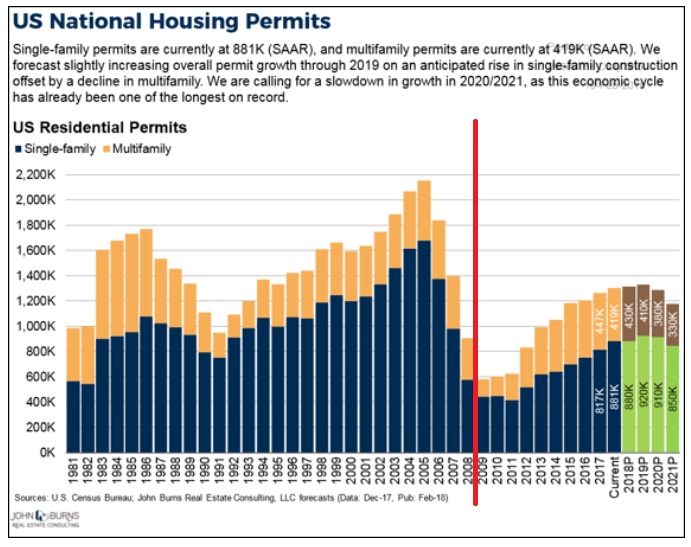

I’m not suggesting the regulations and/or fees are a bad idea or unnecessary. I’m only suggesting we shouldn’t be surprised by the outcome. And the outcome is fewer single family homes are being built due to exceedingly high construction costs. Here’s a great chart courtesy of John Burns Real Estate Consulting:

Note the blue bar represents single-family residences and the beige bar, apartment or multi-family (5+ units.) It’s interesting to see that new home construction peaked in 2005. Just about a year before home values peaked.

And since the Great Recession, new home construction has been far below the level of new household formation. According the the US Census Bureau, US household formation averaged 944,000 per year for the past 10 years. In six of those 10 years, new households were formed at the rate of about 1.1 million or more. Yet the number of new homes or apartments built was far below that number. And this doesn’t take into account the number of homes lost each year due to floods, fire, obsolescence, etc. We have a housing shortage. And it’s getting worse every year.

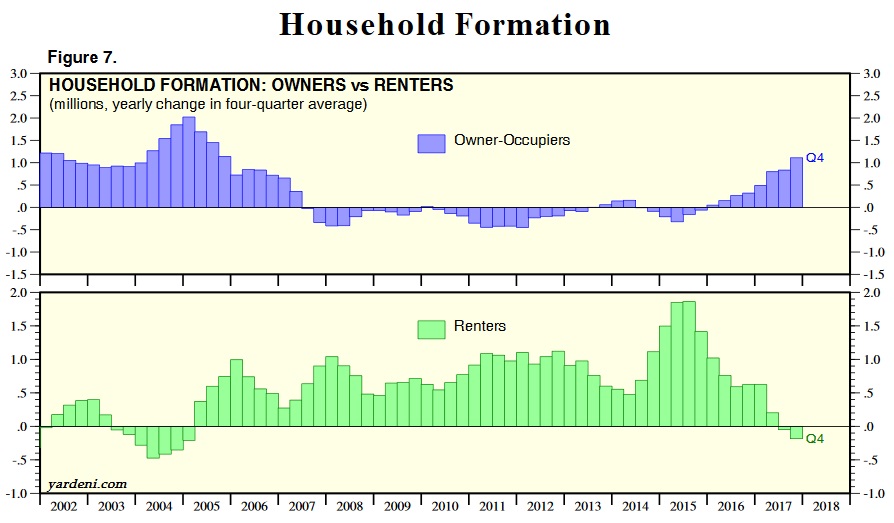

Here’s an interesting chart, courtesy of Yardeni:

It looks like home ownership is back in vogue … and renter demand may be declining. Hmmm….

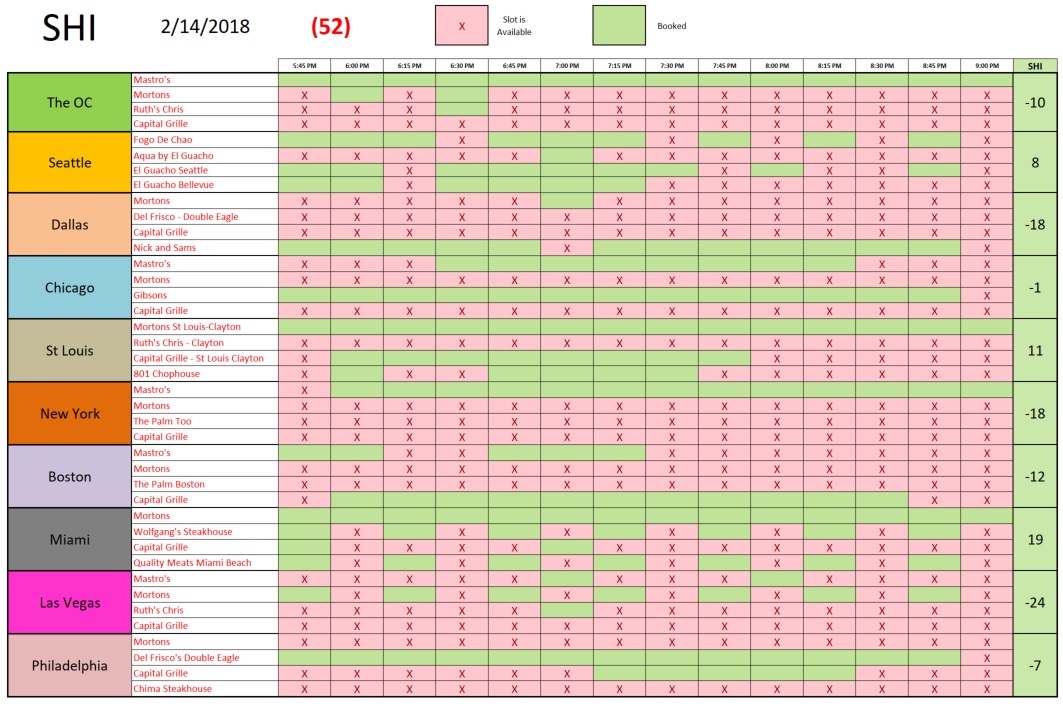

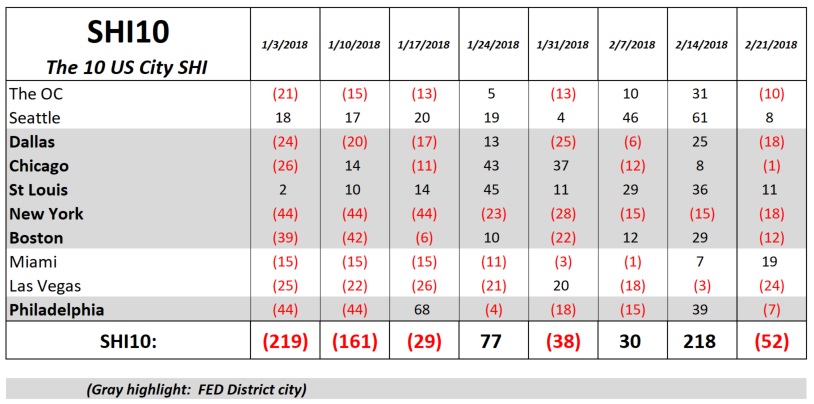

Time for a steak. The Valentine’s Day effect is definitely over. This week, the SHI10 is a negative (52). Cattle herds around the world are breathing a sigh of relief. Here’s this weeks chart:

Seattle, our long-running leader in ‘Filet’ sales slipped (presumably on butter) this week. (I couldn’t help myself; I know, a bad pun.) The “hot” market: Miami, with an SHI of positive 19. And Las Vegas, once again, had a weak SHI showing. Here’s our longer term trend:

On other economic news, the FED released their January 30th ‘minutes’ earlier today. I’ve edited their comments below, and given you a succinct version that I believe summarizes the key comments:

Inflation Analysis and Forecasting

- Almost all participants who commented agreed that a Phillips curve-type of inflation framework remained useful as one of their tools for understanding inflation dynamics.

- Participants generally agreed that inflation expectations played a fundamental role in understanding and forecasting inflation, with stable inflation expectations providing an important anchor for the rate of inflation over the longer run.

Staff Review of the Economic Situation

- GDP expanded at about a 2-1/2 percent pace in the fourth quarter of last year.

- The national unemployment rate remained at 4.1 percent.

- The ‘new orders’ indexes from national and regional manufacturing surveys point to further solid increases in factory output in the near term.

- Consumer spending — including gains in employment, real disposable personal income, and households’ net worth — continued to be supportive of further solid growth of real PCE in the near term.

- Available data for goods trade in December suggested that import growth again outpaced export growth.

- Core PCE price inflation was 1-1/2 percent over that same period.

Staff Review of the Financial Situation

- The dollar index declined nearly 4% relative to its value at the time of the December FOMC meeting.

- The Bank of Canada raised its policy rate at its January meeting, largely in response to better-than-expected economic data. The Bank of England, the Bank of Japan, and the European Central Bank (ECB) left their monetary policy stances unchanged.

- ECB president’s comments were interpreted by market participants as a signal that ECB monetary policy would become less accommodative.

- US consumer credit increased notably in November, exceeding the more moderate volume of borrowing observed earlier in the year.

Staff Economic Outlook

- The U.S. economic projection prepared by the staff for the January FOMC meeting was stronger than the staff forecast at the time of the December meeting.

- Real GDP was estimated to have risen in the fourth quarter of last year by somewhat more than the staff had previously expected, as gains in both household and business spending were larger than anticipated.

- Beyond 2017, the forecast for real GDP growth was revised up. Real GDP was projected to increase at a somewhat faster pace than potential output through 2020;

- The staff continued to assume that the recently enacted tax cuts would boost real GDP growth moderately over the medium term.

- The unemployment rate was projected to decline further over the next few years, below its longer-run natural rate.

- The staff projected that core inflation would reach 2 percent in 2019 and that total inflation would be at the Committee’s 2 percent objective in 2020.

The bottom line? Our US economy is strong, GDP is in the mid-2’s and possibly higher due to the tax cuts; inflation expectations should keep our inflation rate below 2% until 2019 or 2020. No recession in sight, folks. Deficits, yes. But no recession.

One final comment on housing. Long term, the growth in home values will continue irrespective of the general US economic cycle. Sure, one day we’ll see another recession. And home values may dip or flatten for a while. But long term, they’re heading higher. Go buy a house.

- Terry Liebman