SHI 5.23.18 Those Cracks I Mentioned?

SHI 5.16.18 Buying Steaks and Other Stuff

May 16, 2018

SHI 5.30.18 The Italian Stallion

May 30, 2018

The cracks are small, but they are forming.

I hate being ‘Debbie Downer’ from Saturday Night Live, but sometimes that’s my job as an economic blogger. Sorry.

The US economy looks pretty rosy right now. Q2 2018 GDP growth is likely to set a new high-water mark, propelled by a number of tailwinds such as the tax cuts, repatriation, and increases in US government spending. But, sorry, I think that’s where the party ends.

I put much of the blame on the FED. Sure, they had to tighten conditions eventually. I think we all understand that. But for almost 6 years– from 2010 to the end of 2015 — consumers and businesses enjoyed low — or no — interest cost. And decisions made during this “free money” are now coming home to roost. A lot of new debt was accumulated … and that debt is hard to carry when rates rise. Right or wrong, that’s the reality.

The FED began lifting rates on December 16, 2015. Since that time:

- The FED has raised the FED funds rate six (6) times by .25% each time … for a total rate increases of 1.50%.

- Buoyant from near-zero interest rates and the budding recovery, from about 2010 thru today, consumers took on more debt — especially auto and student loans — at an increasing rate.

- Add larger debt loads to the increased debt cost and, “Houston, we have a problem”: The 90+ day delinquency rates in credit card and auto debt is accelerating, also at an increasing rate.

Ironically, only housing debt — the culprit of The Great Recession — has shrunk during this period. Exuberant debt expansion always helps an economy expand … but when the party is over, the hangover is soon to follow.

The bottom line: Consumers are finding their heavier debt loads harder to manage. And they are falling behind. Over time, increased corporate debt cost will have similar effects on business debt. The cracks may be small, but they are appearing.

Welcome to this week’s Steak House Index update.

If you are new to my blog, or you need a refresher on the SHI10, or its objective and methodology, I suggest you open and read the original BLOG: https://www.steakhouseindex.com/move-over-big-mac-index-here-comes-the-steak-house-index/

Why You Should Care: The US economy and US dollar are the bedrock of the world’s economy. This has been the case for decades … and will continue to be true for years to come.

Is the US economy expanding or contracting?

According to the IMF (the ‘International Monetary Fund’), the world’s annual GDP is almost $80 trillion today. US ‘current dollar’ GDP almost reached $20 trillion during Q1, 2018. We remain about 25% of global GDP. Other than China — a distant second at around $11 trillion — the GDP of no other country is close.

The objective of the SHI10 and this blog is simple: To predict US GDP movement ahead of official economic releases — an important objective since BEA (the ‘Bureau of Economic Analysis’) gross domestic product data is outdated the day it’s released.

Historically, ‘personal consumption expenditures,’ or PCE, has been the largest component of US GDP growth — typically about 2/3 of all GDP growth. In fact, the majority of all GDP increases (or declines) usually results from (increases or decreases in) consumer spending. Consumer spending is clearly a critical financial metric. In all likelihood, the most important financial metric.

The Steak House Index focuses right here … on the “consumer spending” metric. I intend the SHI10 is to be predictive, anticipating where the economy is going – not where it’s been.

Taking action: Keep up with this weekly BLOG update. Not only will we cover the SHI and SHI10, but we’ll explore related items of economic importance.

If the SHI10 index moves appreciably -– either showing massive improvement or significant declines –- indicating growing economic strength or a potential recession, we’ll discuss possible actions at that time.

The BLOG:

If you enjoy meandering through a well-designed garden of economic delights, I recommend a trip to Yardeni Research. http://www.yardeni.com/

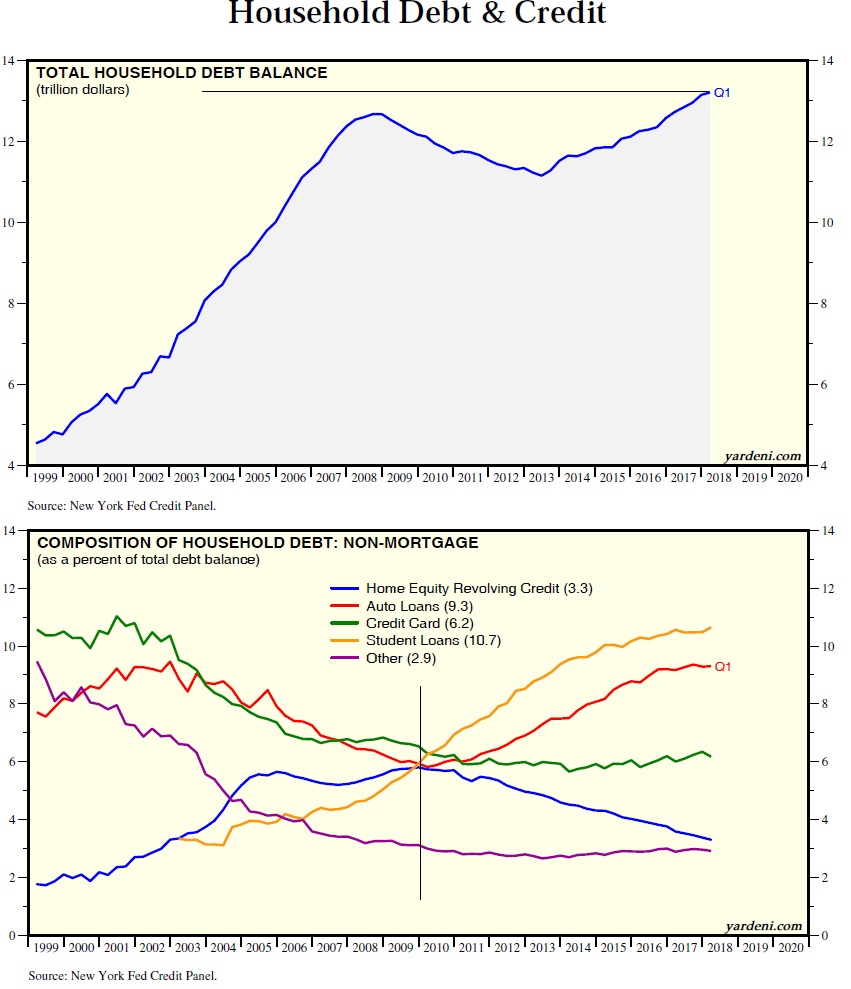

Dr. Ed Yardeni and his staff cull thru reams and reams of economic, stock market, financial market, and demographic data and then distill it down into (relatively) easy to understand charts and graphs. For example, take a look at the two (2) charts below:

In the top chart, you can see households owe more today than they did in 2008 — in fact, household debt now exceeds $13 1/2 trillion. It’s worth noting the cost of that debt is lower, due to lower interest rates from 2008 thru 2015. Even though total debt has grown.

In the lower chart, we see auto loans really took off in 2010. Auto and student loan debt have grown the most since 2010. Outstanding credit card debt has actually shrunk.

It’s also important to note that while $13.5 trillion is a pile of debt, US households today have a net worth of almost $100 trillion. Here’s a great chart courtesy of the FED and their Z.1 report:

An aggregate net worth of $100 million doesn’t mean everyone is doing just fine, however.

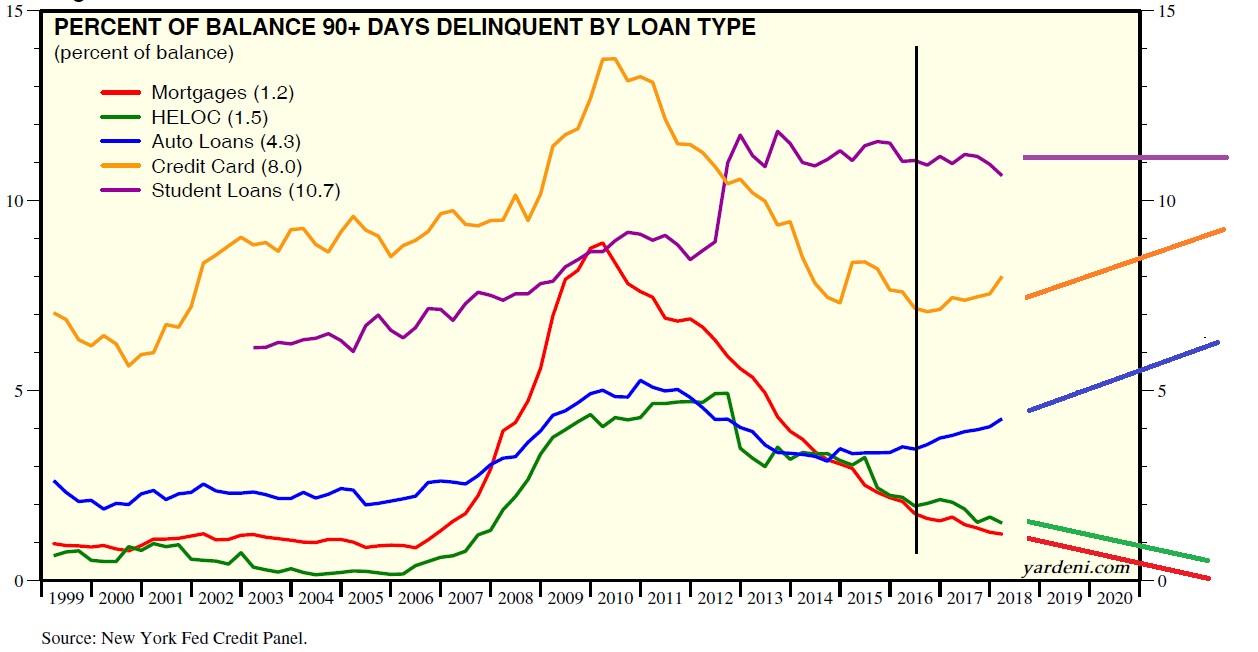

In the Yardeni chart below, we see a rising delinquency rate in credit cards and auto loans. Note this is the 90+ day delinquency rate. Falling behind 30 days is quite common; but, when a loan is 90+ days delinquent, it is considered “serious”:

All interest rates are sensitive to FED rate increases. But variable rate loans – such as credit cards – are the most impacted when the FED has raises the FED funds rate. Which has happened six (6) times by .25% each, for a total rate increases of 1.50%, in the past 2 or so year.

It’s obvious consumers have increased their debt burden in recent years. And it’s obvious from the above chart, many are now struggling.

This point made even more abundantly clear in the FEDs recent report entitled, “Report on the Economic Well-Being of U.S. Households in 2017,” published just days before.

Here are some highlights:

- When asked about their finances, 74% of adults said they were either “doing okay” or living comfortably in 2017—over 10% more than in the first survey in 2013.

- For many, stability of income is valued highly. Three-fifths of workers would prefer a hypothetical job with stable pay over one with varying but somewhat higher pay.

- Four in 10 adults, if faced with an unexpected expense of $400, would either not be able to cover it or would cover it by selling something or borrowing money.

- Less than two-fifths of non-retired adults think that their retirement savings are on track, and one fourth have no retirement savings or pension whatsoever.

Finally, over 20% of adults are not able to pay all of their current month’s bills in full. Remember: more than 10% of those surveyed felt better now than in 2013.

The bottom line: Cracks are appearing. The robust economy and a 3.9% unemployment rate notwithstanding, clearly the FED rate increases have taken their toll on consumers. And will continue to take their toll as time progresses.

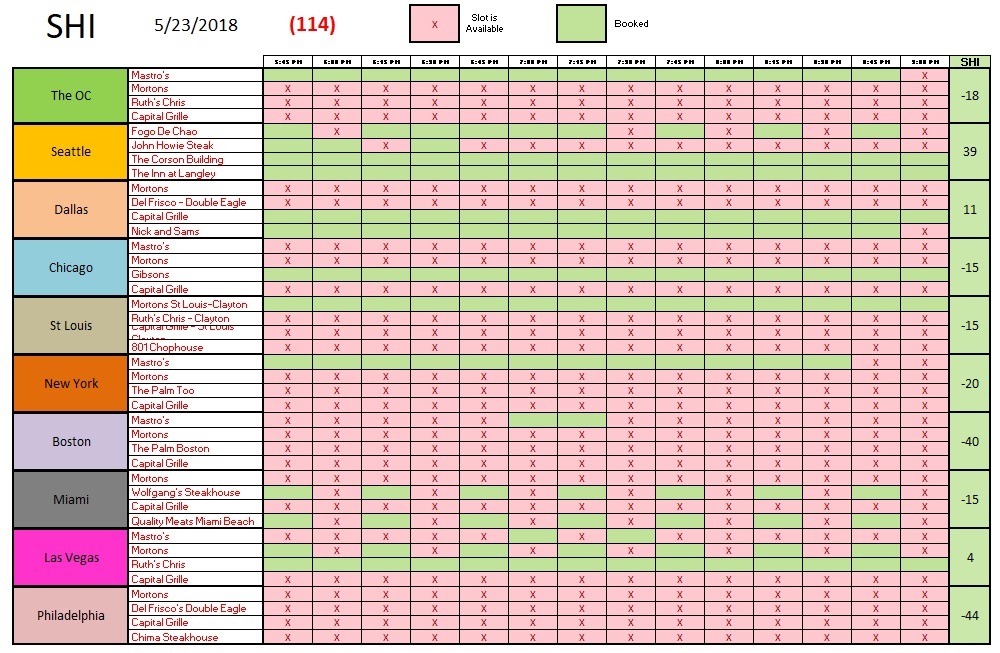

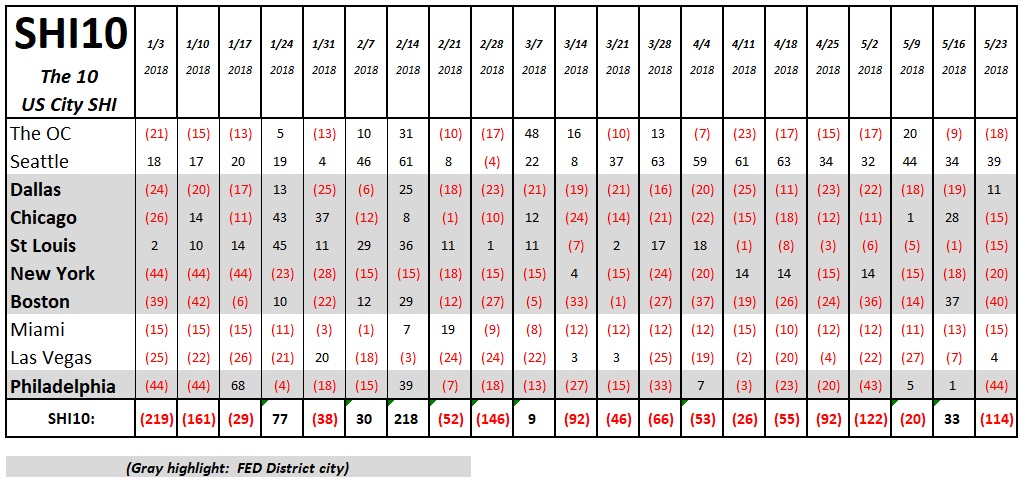

Let’s see how the steakhouses are doing this week.

Hmmm…not so good. Reservations couldn’t be weaker in Philly. And tables this Saturday are far more “available” in most markets. Take a look at our trend report:

Seattle continues to be a beacon. Dallas improved. But steak lovers in Boston and Philadelphia are clearly staying home this weekend. Odd. Well, one week does not a trend make.

It’s important to note that the developments I discussed above do not, in themselves, guarantee a near-term economic contraction. They are indicative only. But they do create headwinds that are hard to overcome. We will continue to monitor conditions as they develop.

And as I said above, GDP growth in Q2 2018 should be robust. Historically, Q2 growth is usually quite a bit stronger than Q1. Further, the economy is experiencing a nice lift from tax cuts, corporate profit repatriation, and increased government spending. I won’t be surprised with a reading north of 3%.

In the meantime, this is a good weekend to go out and enjoy that flat-iron steak at your favorite local opulent eatery! Go do your part: The US economy is depending on you! 🙂

- Terry Liebman

2 Comments

I’m not quite ready to lay blame for delinquency rate increases at the feet of the FED. Two of the three loan types experiencing significant delinquency increases (auto loans and credit cards) are, for the most part, discretionary decisions to incur debt. When times appear to be good, we forget the lessons of the past. It seems as though we, as a nation of consumers, have yet to learn how to live within our means.

Kevin, I completely agree. My point was less to lay blame and more to shine a light on the larger issue of debt growth and the possible down-steam implications on the US economy. New debt is always discretionary. Whether sovereign, corporate or consumer. A choice is made to take on more debt. Unfortunately, in all 3 cases, little attention is paid to the potential long term cost or the long term implications. Often the consumer understands these least of all. If I lay any blame in the lap of the FED, it would be to suggest they tend to pay scant attention to the plight of the typical American struggling under their self-imposed debt load when they consider only their “dual mandate” of full employment and a 2% inflation rate.

The FED lowered interest rates to near zero. Consumers responded by borrowing money. I feel the FED is a bit disingenuous in ignoring the cause/effect relationship. Just a bit. 🙂