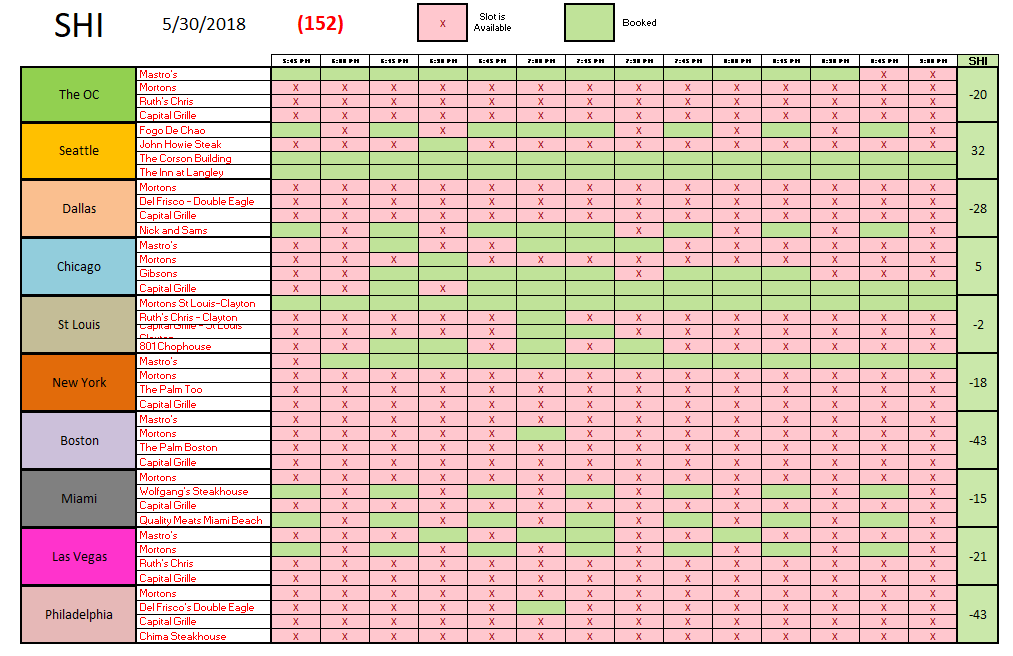

SHI 5.30.18 The Italian Stallion

SHI 5.23.18 Those Cracks I Mentioned?

May 23, 2018

SHI 6.6.18 Here We Grow Again

June 6, 2018

Where is ‘Rocky Balboa’ when you need him?

Italy has been in the news of late. We all love “Rocky” movies, pizza, and pasta, so I’m sure you find it disturbing to see Italy so maligned by the financial press. I sure do.

But beyond feeling bad, like me, you may be a bit worried about ‘contagion.’ Meaning that problems within Italy slosh over into the EU, impacting the ECB, the euro itself, and ultimately the global economy. Imagine falling dominos. “Hey, Rocky, what’s wrong with Italy?”

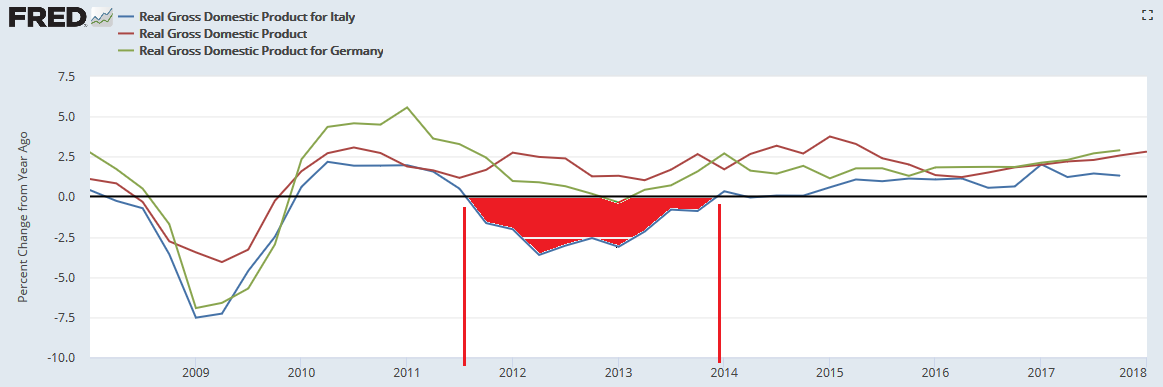

- While the economies of most other EU countries were growing and expanding, another recession pummeled Italy from the middle of 2011 thru the end of 2013. Almost 2 1/2 years.

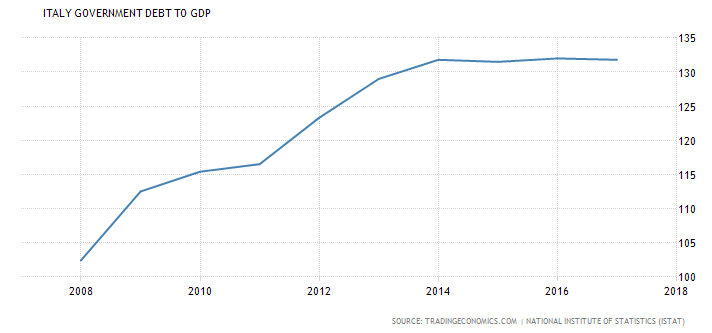

- Italy now has a “debt to GDP” ratio of almost 132% — they owe over $2.3 trillion. That’s a lot of debt for a country with about a $1.85 trillion annual GDP. On the other hand, until this week, their short-term interest rates were negative. Nice!

- Membership in the euro constrains the maximum annual Italian budget deficit. The result: The same “austerity” and ill will many Greeks felt.

- Geography has forced Italy to take the brunt of the migrant issues confronting Europe as a whole.

As a result, many Italian folks are irritated. Perhaps rightfully so. Recent Italian elections have brought people to power who are proposing some disturbing ideas … such as leaving the euro and mini-BOTS. What? Mini-BOTS? What the heck is a mini-BOT? Here’s a hint: You won’t find a mini-BOT in the picture above. This will help: (remember: ‘right click’ and select ‘open link in new tab’.)

The bottom line: This too shall pass. Not quickly or easily, particularly for the Italians …. But Italy will remain in the euro and I don’t envision an meaningful impact on the US economy.

Welcome to this week’s Steak House Index update.

If you are new to my blog, or you need a refresher on the SHI10, or its objective and methodology, I suggest you open and read the original BLOG: https://www.steakhouseindex.com/move-over-big-mac-index-here-comes-the-steak-house-index/

Why You Should Care: The US economy and US dollar are the bedrock of the world’s economy. This has been the case for decades … and will continue to be true for years to come.

Is the US economy expanding or contracting?

According to the IMF (the ‘International Monetary Fund’), the world’s annual GDP is almost $80 trillion today. US ‘current dollar’ GDP almost reached $20 trillion during Q1, 2018. We remain about 25% of global GDP. Other than China — a distant second at around $11 trillion — the GDP of no other country is close.

The objective of the SHI10 and this blog is simple: To predict US GDP movement ahead of official economic releases — an important objective since BEA (the ‘Bureau of Economic Analysis’) gross domestic product data is outdated the day it’s released.

Historically, ‘personal consumption expenditures,’ or PCE, has been the largest component of US GDP growth — typically about 2/3 of all GDP growth. In fact, the majority of all GDP increases (or declines) usually results from (increases or decreases in) consumer spending. Consumer spending is clearly a critical financial metric. In all likelihood, the most important financial metric.

The Steak House Index focuses right here … on the “consumer spending” metric. I intend the SHI10 is to be predictive, anticipating where the economy is going – not where it’s been.

Taking action: Keep up with this weekly BLOG update. Not only will we cover the SHI and SHI10, but we’ll explore related items of economic importance.

If the SHI10 index moves appreciably -– either showing massive improvement or significant declines –- indicating growing economic strength or a potential recession, we’ll discuss possible actions at that time.

The BLOG:

Don’t worry about Italy — at least no more than about the US. Things will work out fine. Probably.

While the US and Germany (and most of northern Europe) were recovering, Italy “double-dipped” back into a recession:

As their real GDP shrunk, and deficit spending increased, the country ‘debt-to-GDP’ ratio really spiked:

And since the ECB member countries have de-facto deficit spending ceilings, some brilliant Italian politicians proposed the idea of the mini-BOT.

The market reactions notwithstanding, I think this is all just noise. I don’t believe Italy or the EU will permit the issuance of mini-BOTs, nor is the threat to exit the euro a legitimate threat. The obstacles are too great…the binds too strong.

Speaking of noise (see that segue? Impressive, right?), how are our loud and boisterous steakhouses doing this week? Let’s take a look:

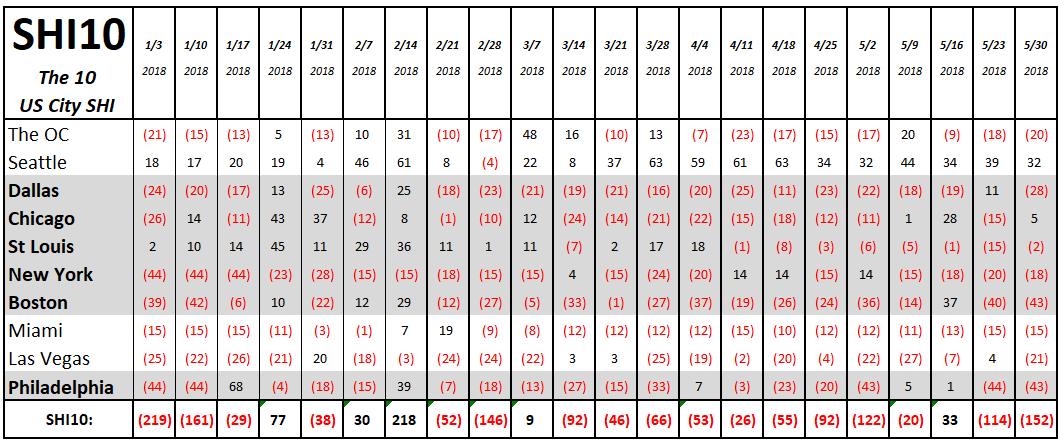

Hmmm….not to well, it turns out. It has been months since the SHI10 reading has been this weak. Most of our SHI markets are consistent with last week…with the exceptions of Dallas and Las Vegas. All in all, reservations at our 40 steakhouses this Saturday are very plentiful. Interesting. Here is this week’s data:

It’s worth noting that earlier today, the FED released their latest ‘Beige Book‘ which comments on “Current Economic Conditions” across the 12 Federal Reserve Districts. Hot off the press, the FED commented:

Overall Economic Activity

- Economic activity expanded moderately in late April and early May. The Dallas District was an exception, where overall economic activity sped up to a solid pace.

- Manufacturing shifted into higher gear with more than half of the Districts reporting a pickup in industrial activity and a third of the Districts classifying activity as “strong.”

- By contrast, consumer spending was soft. Non-auto retail sales growth moderated somewhat and auto sales were flat.

- In banking, demand for loans ticked higher. Delinquency rates were mostly stable at low levels.

- Homebuilding and home sales increased modestly.

Employment and Wages

- Employment rose at a modest to moderate rate across most Districts. Again, the Dallas District was the exception, where solid and widespread employment growth was reported.

- Labor market conditions remained tight across the country, and contacts continued to report difficulty filling positions across skill levels.

- Shortages of qualified workers were reported in various specialized trades and occupations, including truck drivers, sales personnel, carpenters, electricians, painters, and information technology professionals.

- Many firms responded to talent shortages by increasing wages as well as the generosity of their compensation packages.

- In the aggregate, however, wage increases remained modest in most Districts. Contacts in some Districts expected similar employment and wage gains in the coming months.

Prices

- Prices rose moderately in most Districts, while the remainder reported slight or modest increases.

- There were several reports of rising materials costs, notably for steel, aluminum, oil, oil derivatives, lumber, and cement.

- Some Districts noted that their retail contacts were more able to pass along price increases to their customers than in the recent past.

It’s interesting to look at the Dallas SHI number in light of the FEDs comments above. While “consumer spending was soft,” the Dallas District seems to be hotter than the grill at Ruth’s Chris. Hmmm….

‘Nuff said.

- Terry Liebman