SHI 6.6.18 Here We Grow Again

SHI 5.30.18 The Italian Stallion

May 30, 2018

SHI 06.13.18 The Real GDP

June 13, 2018

America’s population gains 1 person every 13 seconds.

That’s interesting, right? Every 13 seconds? OK … wait for it … wait for it … POOF! Another person is here!

As you can see above, US population growth is a combination of births, deaths, and net immigration. And to the right, we see the world population. Note that the US is the 3rd most populous country in the world. China and India are clearly MUCH larger, however, and combined they exceed 2.6 billion people. More than 1/3 of the globes’ total population.

Also note US population number showing in that box is slightly different than the number at the red arrow. And, frankly, the population numbers shown for both China and India are a bit lower than other sources may indicate. Precise numbers aside, it appears both US and world population are growing. Why is population growth important in an economic blog?

- Economic systems require a combination of growing population and increasing productivity to maintain economic health.

- Headwind: The US ‘fertility rate’ has once again slipped lower.

- Headwind: In the 9 years since the end of the “Great Recession,” US labor productivity growth has been stunted, averaging only about 1% per year.

Friday, we saw the release of the most recent ‘Employment Situation Summary.‘ The headline unemployment rate fell to 3.8%. Employment increased by 223,000. The number of “unemployed” people is down to about 6 million. These are very good, very positive numbers.

The bottom line: Our economy is on solid footing. The ‘participation rate’ is concerning…but not surprising given the aging of America. And for the first time in history, the number of “open jobs” exceeds the number of ‘unemployed’ Americans. Is inflation about to rise again? A great question. Read on.

Welcome to this week’s Steak House Index update.

If you are new to my blog, or you need a refresher on the SHI10, or its objective and methodology, I suggest you open and read the original BLOG: https://www.steakhouseindex.com/move-over-big-mac-index-here-comes-the-steak-house-index/

Why You Should Care: The US economy and US dollar are the bedrock of the world’s economy. This has been the case for decades … and will continue to be true for years to come.

Is the US economy expanding or contracting?

According to the IMF (the ‘International Monetary Fund’), the world’s annual GDP is almost $80 trillion today. US ‘current dollar’ GDP almost reached $20 trillion during Q1, 2018. We remain about 25% of global GDP. Other than China — a distant second at around $11 trillion — the GDP of no other country is close.

The objective of the SHI10 and this blog is simple: To predict US GDP movement ahead of official economic releases — an important objective since BEA (the ‘Bureau of Economic Analysis’) gross domestic product data is outdated the day it’s released.

Historically, ‘personal consumption expenditures,’ or PCE, has been the largest component of US GDP growth — typically about 2/3 of all GDP growth. In fact, the majority of all GDP increases (or declines) usually results from (increases or decreases in) consumer spending. Consumer spending is clearly a critical financial metric. In all likelihood, the most important financial metric.

The Steak House Index focuses right here … on the “consumer spending” metric. I intend the SHI10 is to be predictive, anticipating where the economy is going – not where it’s been.

Taking action: Keep up with this weekly BLOG update. Not only will we cover the SHI and SHI10, but we’ll explore related items of economic importance.

If the SHI10 index moves appreciably -– either showing massive improvement or significant declines –- indicating growing economic strength or a potential recession, we’ll discuss possible actions at that time.

The BLOG:

Is inflation about to rear its ugly head once again? The answer is obvious: Maybe. 🙂

Sorry. I couldn’t resist. Everyone knows economists cannot answer questions with certainty! But with my investor hat on, I will answer the question with a timid ‘no.’

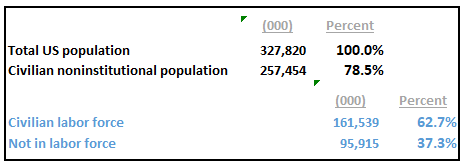

155.5 million folks are employed in the US. Just about 1/2 of our total population. Here are some other high-level stats you may find interesting:

And we have almost 96 million people who could, in theory, hold a job, but are not interested in doing so. At this time. These are people “not in the labor force.”

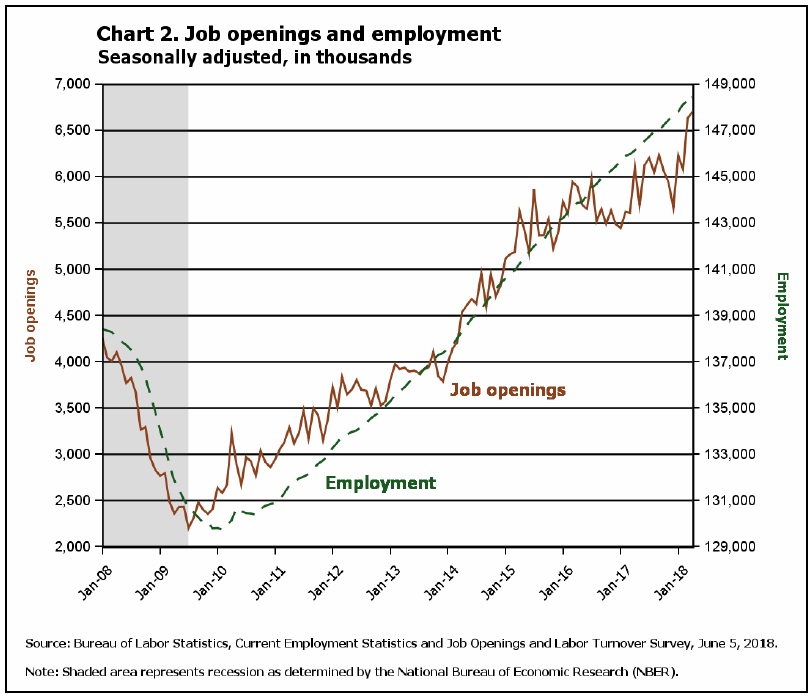

The number of “job openings” bottomed in July of 2009. The number of people employed bottomed in February of 2010. Since that time, both openings and the number of people employed have grown significantly. And today, the number of jobs seeking a qualified employee has reached an all time high: The US has about 6.7 million open jobs seeking a qualified worker:

And we have about 6 million Americans still defined as “unemployed.” With 6.7 million job openings and only 6 million available workers, the numbers suggest American employers have a problem. And the numbers further suggest wage inflation may soon become a reality.

Perhaps.

But if we once again look at Japan as a leading indicator for the US, an ultra-low unemployment rate does not necessarily mean inflation is close behind. Japan’s unemployment rate has been below 3.8% since 2014. Today, it rests near 2.5%. During that same time-period, the inflation rate in Japan has fallen from a 2014 high of about 3.8% to a reading of 0.6% today. In fact, during much of 2015 and 2016, Japan’s inflation rate was slightly above, or slightly below, zero.

How do economists explain near-zero inflation with a 2.5% unemployment rate? Why doesn’t the “Phillips Curve” work in Japan? There is no consensus explanation.

I think the explanation goes back to demographics. Japan’s labor force participation rate is 61.7%…suggesting they have over 40 million folks “not in the labor force.” The US has almost 96 million people in the same category. I believe this group keeps wage increases in check, acting as both a buffer against temporary job needs and a defacto lid on wage increases.

There is no doubt the US is experiencing moderate increases in prices in the “service” side of our economy, housing, and fuel. But wage inflation has been muted so far … and I think it will remain subdued. I will keep a close eye on this one.

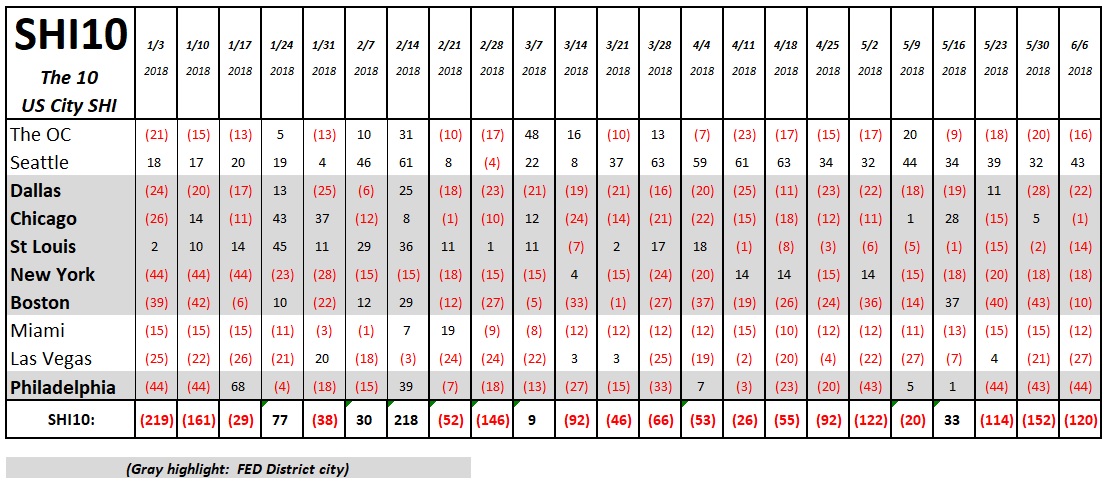

How are the steakhouses doing this week? Let’s take a peek:

The answer: A sliver better than last week. Clearly, folks in Philadelphia don’t like costly cuts of beef. Or, if they do, they certainly don’t make steakhouse reservations several days ahead of time. Maybe Philly is overrun by vegetarians?

At the other end of the SHI spectrum, it’s pretty clear folks in Seattle either (1) LOVE expensive steaks, or (2) there are not enough pricey steakhouses in the city. Across the board, with the exception of Boston that saw some meaningful reservation increases, most of the other SHI10 cities showed consistent reservation demand. Here are the week’s numbers:

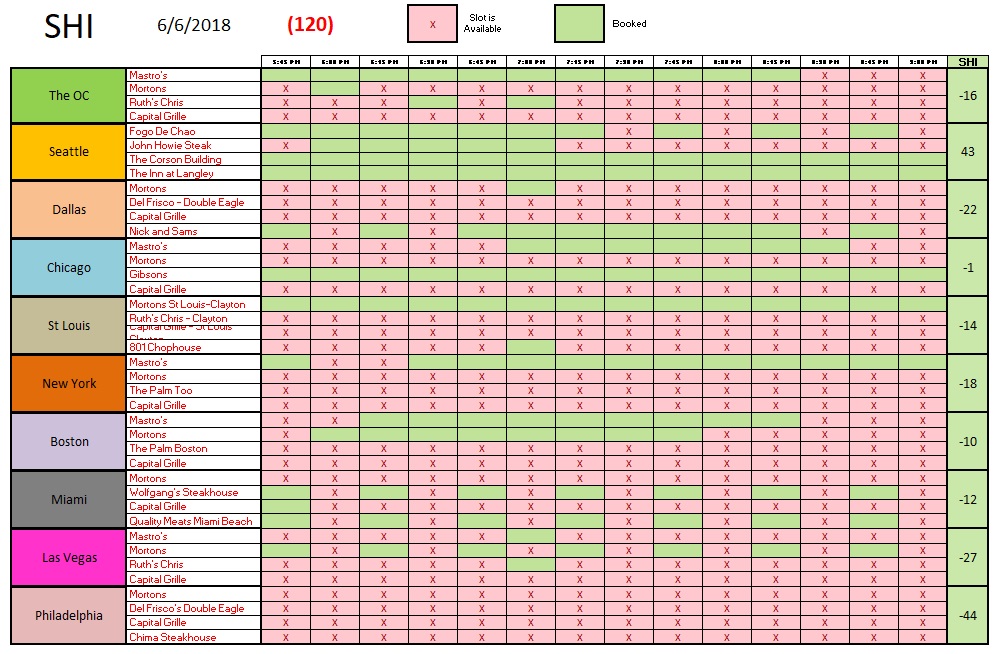

In most markets, Mortons and Mastros are quite popular. I’ll definitely have to check out ‘Gibsons‘ the next time I’m in Chicago. But I’ll make my reservation early.

In the big picture, this week is pretty much a repeat of last week. Not much new information.

Repeating what I said above, our economy is on solid footing. With 6.7 million jobs available, employment — for those who seek it — is plentiful. Of course, the 6 million unemployed folks — those who want jobs but cannot find them — probably don’t have the skills needed for the open jobs. This is a real challenge. And while I do expect the inflation rate to increase a bit more, I don’t expect run-away wage inflation.

- Terry Liebman

1 Comment

I would recommend Gibson’s several times over.