SHI 5.24.23 – We Need AI Right Now

SHI 5.17.23 — Elon For Prez!

May 17, 2023

SHI 5.31.23 — Yardsticks and Labor Hoarders

May 31, 2023

We do. Because natural intelligence appears in short supply. It seems to have left the building. Like Elvis.

Again, to be clear, this is a financial and economic blog. Here, I have no interest in discussing politics. But lets face facts: Our political leaders in Washington from both parties are looking thin on intelligence these days. In fact, one could argue, their collective puffing and posturing on the debt ceiling is downright dumb.

Our dumb leaders, again in the aggregate, are putting America’s reputation as the global economic leader at risk. Even if the US doesn’t “default” — whatever that means — the continuous threat of economic instability, missed or delayed Treasury debt payments, government shutdown, etc., will absolutely and unequivocally cost you, me and America MORE. Treasury interest rates, American home loan rates, car loans, credit cards … every day we come closer to a threatened default … all of it will tick up in cost. Probably permanently. And as we all know, a tarnished reputation is a hard thing to rebuild. And so is a credit rating.

It’s worth repeating: We are dangerously close to the tipping point where our leader’s moronic failure to just agree to make the debt ceiling “issue” into a non-issue will permanently increase America’s cost of debt.

“

A reputation 100 years in the making.”

“A reputation 100 years in the making.”

To be clear, in this financial and economic blog, I’ve commented numerous times in the past that America’s debt has grown dangerously large. My opinion. Philosophically, I agree that we must get a better handle on debt and spending management. Philosophically speaking. But not now. Not today. And definitely not by holding a ‘financial gun’ to America’s head, threatening to pull the trigger, potentially destroying a 100-year reputation as the global voice of financial reason and sanity, if the other side doesn’t agree to some spending compromise now. That’s downright dumb.

So I say bring on the machines with artificial intelligence. Then we’d have some intelligence in the room. I’m confident they would make the right decision, the smart decision. The machines would move the debt ceiling issue aside … and begin to concentrate on the real issues and negotiations while, at the same time, ensuring that America preserves America’s sterling credit rating and reputation.

Our elected leaders are duty-bound to all Americans to prevent this stupid, self-inflicted, and yet easily avoidable economic wound. Their continued failure to grasp this simple principal suggests they are collectively insipid and unpatriotic.

Welcome to this week’s Steak House Index update.

If you are new to my blog, or you need a refresher on the SHI10, or its objective and methodology, I suggest you open and read the original BLOG: https://www.steakhouseindex.com/move-over-big-mac-index-here-comes-the-steak-house-index/

Why You Should Care: The US economy and US dollar are the bedrock of the world’s economy.

But is the US economy expanding or contracting?

Expanding. Even as the FED rapidly raises rates! At the end of Q4, 2022, in ‘current-dollar’ terms, US annual economic output rose to an annualized rate of $26.14 trillion. During 2022, America’s current-dollar GDP increased at an annualized rate exceeding 9%. No wonder the FED is so concerned, right? The world’s annual GDP rose to over $100 trillion during 2022. America’s GDP remains around 25% of all global GDP. Collectively, the US, the euro zone, and China still generate about 70% of the global economic output. These are the 3 big, global players.

The objective of this blog is singular.

It attempts to predict the direction of our GDP ahead of official economic releases. Historically, ‘personal consumption expenditures,’ or PCE, has been the largest component of US GDP growth — typically about 2/3 of all GDP growth. In fact, the majority of all GDP increases (or declines) usually results from (increases or decreases in) consumer spending. Consumer spending is clearly a critical financial metric. In all likelihood, the most important financial metric. The Steak House Index focuses right here … on the “consumer spending” metric. I intend the SHI10 is to be predictive, anticipating where the economy is going – not where it’s been.

Taking action: Keep up with this weekly BLOG update. Not only will we cover the SHI and SHI10, but we’ll explore “fun” items of economic importance. Hopefully you find the discussion fun, too.

If the SHI10 index moves appreciably -– either showing massive improvement or significant declines –- indicating growing economic strength or a potential recession, we’ll discuss possible actions at that time.

The Blog:

All right, I’ve put away the soap box. 🙂

Interestingly enough, concurrent with all the dummies and drama in Washington, across America the economy is looking pretty good thru a few different lenses. Lense #1:

PRODUCER PRICES ARE PLUMMETING

Yes, yes, the PPI is not the CPI. True. However, if the costs of making stuff is falling, then it stands to reason that the cost of the stuff made will eventually fall too.

![]()

Powell was tarred-and-feathered for his use of the word ‘transitory’ when discussing consumer inflation. But the graph above sure looks transitory to me. Powell may have been wrong about the duration of transitory — as the ‘mountain’ above does cover two calendar years — but it certainly looks transitory nonetheless.

The PPI is plummeting. Peaking at a 16.3% annualized rate of increase in April of 2022, food costs rose by only 2.5% in April of 2023. And that same month, the ‘total’ PPI rate of increase was only 2.3% — very, very close to the FEDs long-run goal of 2%.

Speaking of inflation, a retired FED luminary, Ben Bernanke and friends, just yesterday posted a quick 50-page read on that topic. Here’s a link if you’re feeling frisky and want to take a deep dive (right click, open in a new link):

https://www.brookings.edu/wp-content/uploads/2023/04/Bernanke-Blanchard-conference-draft_5.23.23.pdf

If that’s too big a hill to climb, here’s the question and answer, in summary format:

WHAT CAUSED THE HIGHEST INFLATION RATE SINCE THE 1980s?

They hope to settle the debate once and for all. Was it pandemic-caused supply shocks as some economists believe? Or was excessive fiscal stimulus to blame? The short answer: Both. According to Ben and friends it was a one-two punch.

Supply shocks were quick and widespread after the world shut down in early 2020. Shortages and disruptions, Ben argues, explain why inflation shot up in 2021. But as the supply chains healed, our economy subsequently overheated due to massive fiscal stimulus and exceptionally low interest rates, which kept the inflation rate high.

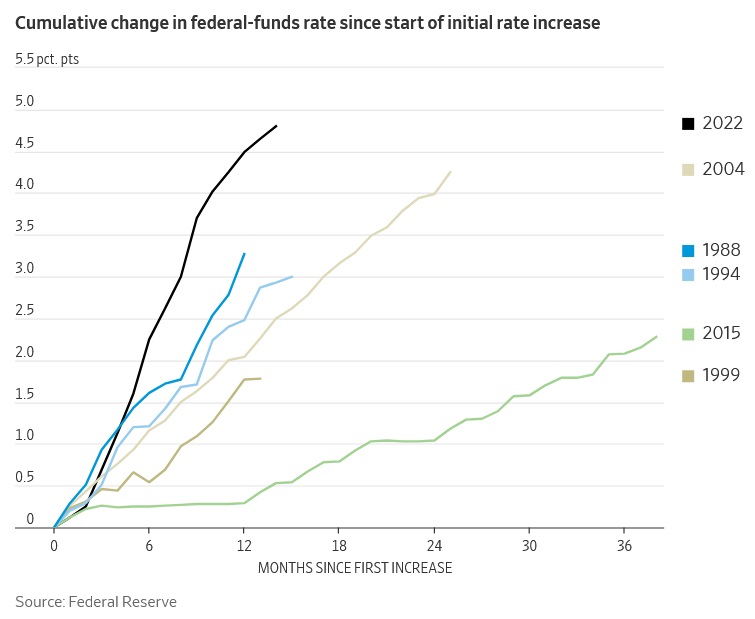

Well, interest rates are no longer exceptionally low. In fact, as I’ve said a number of times in past blogs, the FED has now raised interest rates higher and faster than at any time since 1980.

The size and speed of the rate increases are almost unprecedented. I’ve argued repeatedly this has been too much … too fast. And I think we all now know the FEDs rate choices contributed to the bank failures we recently experienced. Sure there were other contributing factors, but the catalyst came from the FED. Sorry … I almost pulled out that soap box again! 🙂

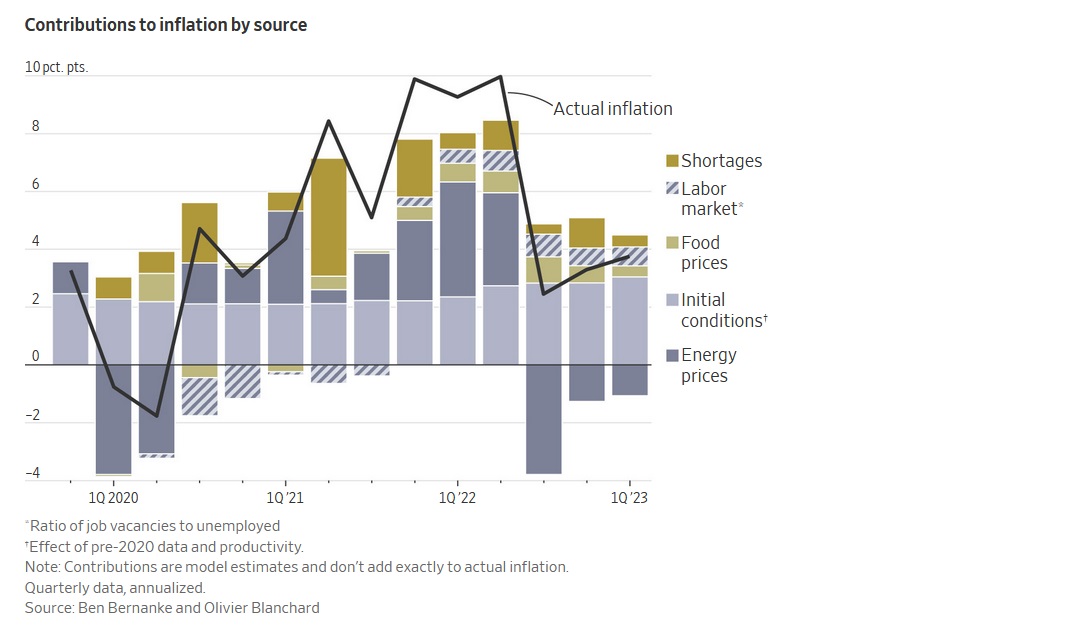

Let’s get back to Bernanke’s paper. Here’s an interesting graph, one that separates the individual inflation components, each calendar quarter, making it easier to understand the contributing source:

Notice how similar it looks — in shape only — to the PPI graph at the beginning of the blog? Yes, very similar.

Bernanke and friends conclude we probably need a weaker labor market to push inflation back down to the FEDs long-term 2% goal. They believe that either the unemployment rate needs to rise to about 4.3%, putting another 1.5 million hard-working American’s out of work, or the underlying demand for labor as evidenced in the JOLT report must ease, without a simultaneous increase in unemployment. Or some combination of both.

Q2, 2023 GDP GROWTH IS TRACKING AT 2.9%

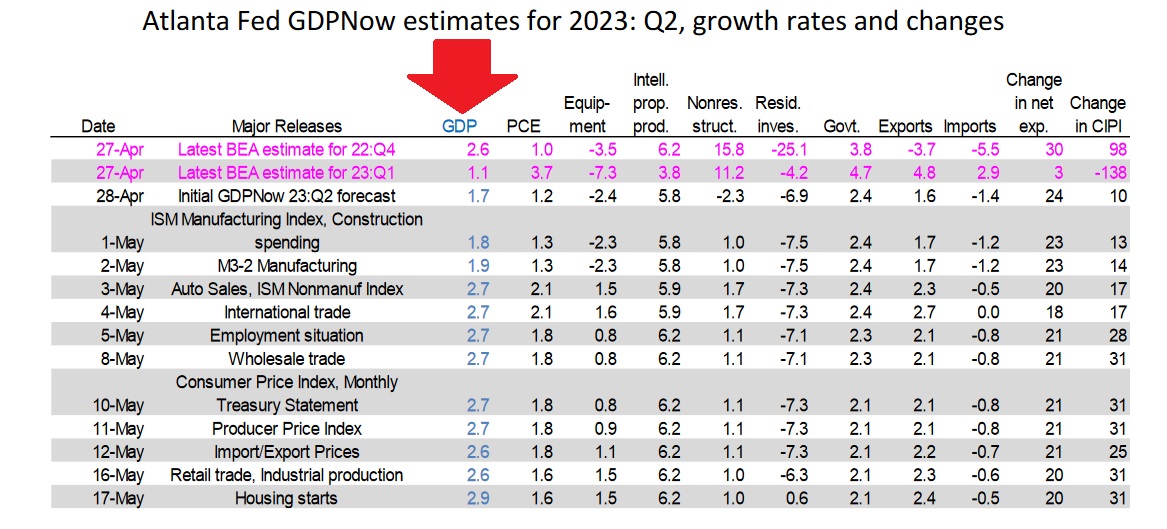

Finally, we have the latest report from the Atlanta FED which publishes their GDP Now analysis every few days. Their latest forecast puts our real Q2 GDP growth rate at 2.9%. Wow. If they’re right — and they almost never are — that suggests our nominal GDP growth rate is still over 6%! That, folks is a hot US economy. They may not be right, but they are often directionally close.

It’s interesting — well, at least to me — to watch the Atlanta FEDs analysis and progression as new economic data comes in and modifies their analysis. Here’s a chart … focus on the ‘GDP‘ column …

It looks like robust auto sales and the ISM kicked up the GDP forecast on May 2nd … and housing starts added more fuel to the fire on May 17th. I’ll repeat: The Atlanta FED forecast is rarely accurate. But it is indicative. FED rate increases have clearly taken the froth off the top — and many interest rate sensitive sectors of the US economy are feeling the pain — but the bigger picture still looks fairly robust.

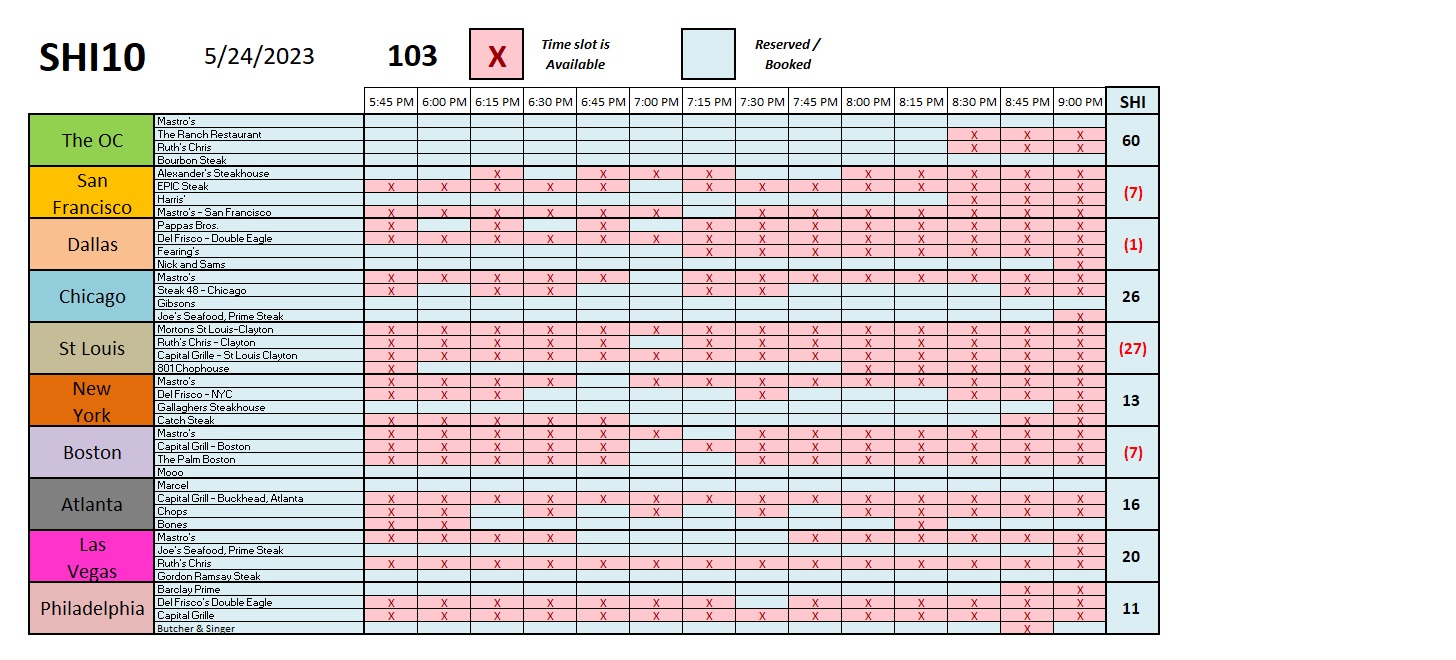

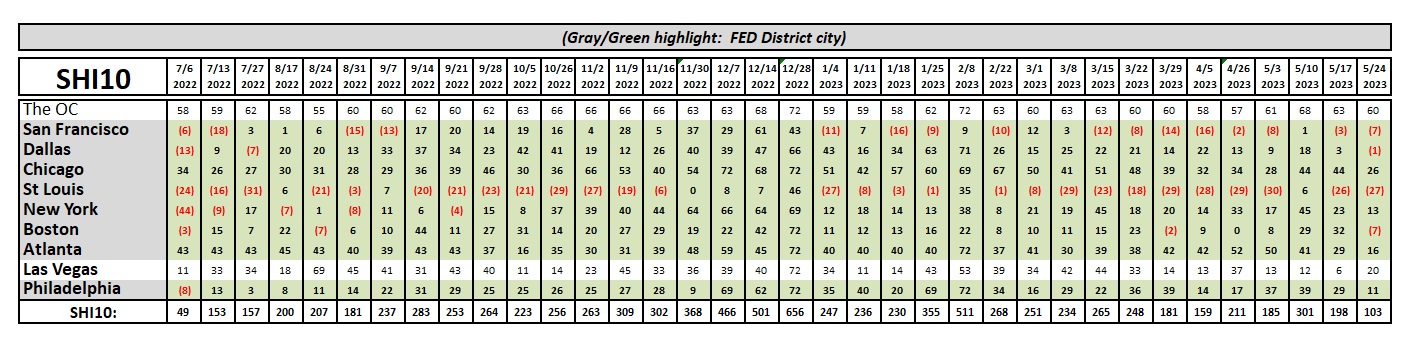

Do the steakhouses agree?

The short answer: NO, not really. Across the board, this week with few exceptions just about every one of the 40 SHI pricey steakhouses, in all ten cities across America, has more available reservation slots than in the past few weeks.

One notable exception is the OC. Demand for opulent eateries seems to be holding up fine amongst the affluent populace. And ‘Vegas saw a small bump in reservation demand this week — mostly attributable, however, to that perennial favorite, Gordon Ramsay Steak. It’s easier to see the longer term trend here:

Yes, with an SHI10 reading this week of only 103, we are dangerously close to falling into double digits. We have to go all the way back to July of 2022 to find a weaker reading. Even the ‘post-New Year’ hangover date of January 4th, 2023 had a higher SHI reading.

It’s interesting that the SHI is somewhat at odds with the Atlanta FED ‘GDP Now’ forecast. Which is right? Or, at least, ‘right-er’?

One thing that’s clear is economic uncertainty is at a near-term apex. Questions abound: Will the FED raise rates further? Will the bozos in Washington come to their senses and take America’s credit rating out of jeopardy? Will inflation continue to ease? Will Putin ramp up Russia’s war effort, and possibly consider using nuclear weapons? Will the chill between China and the US grow frostier?

There’s no shortage of worries today. Perhaps some, or all, are keeping more Americans home this weekend. However, make no mistake, there are economic storm clouds forming out there on the horizon … and we’ll keep watching.

Thanks for tuning in.

<:> Terry Liebman