SHI 5.29.19 A Tale of Two Viewpoints

SHI 5.22.19 – Trade, Tariffs and Inflation

May 22, 2019

SHI 6.5.19 – Battle Rope Exercises

June 5, 2019

“It was the best of times; it was the worst of times ….”

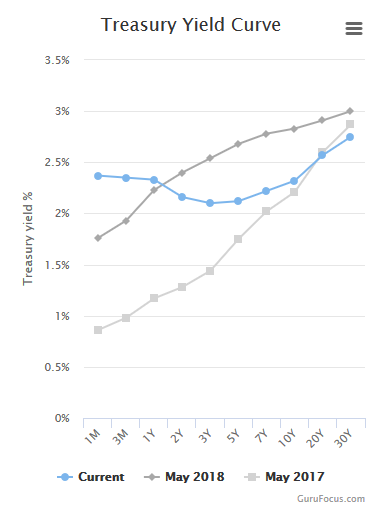

This quote, from the opening paragraph of Dicken’s novel, A Tale of Two Cities, seems exceptionally apropos today, when we consider the diametrically opposed viewpoints on the future of the US economy, viewed thru the eyes of the consumer vs. the beliefs of bond traders. According to the most recent ‘surveys of consumers’ conducted by the University of Michigan, “The Index of Consumer Sentiment surged in early May to its highest level in 15 years.” By this measure, the consumer is feeling good! Bond traders, on the other hand, are not. Here is an image of today’s yield curve, compared to May of ’18 and May of ’17, courtesy of gurufocus.com:

The BLUE line is the current yield curve. Notice the deep inversion? Well, our yield curve inversion is becoming more pronounced with each passing day. In fact, as I write this blog, the US 10-year Treasury yield has fallen to 2.22%. Bond traders, in the aggregate, clearly believe:

- We are heading toward a recession; and,

- The FED will need to lower the FED funds rate in the near future.

Who’s right? The carefree, happy consumer who is, again in the aggregate, feeling good? Or the bond traders who are not?

Welcome to this week’s Steak House Index update.

If you are new to my blog, or you need a refresher on the SHI10, or its objective and methodology, I suggest you open and read the original BLOG: https://www.steakhouseindex.com/move-over-big-mac-index-here-comes-the-steak-house-index/

Why You Should Care: The US economy and US dollar are the bedrock of the world’s economy. This has been the case for decades … and will be true for years to come.

But is the US economy expanding or contracting?

According to the IMF (the ‘International Monetary Fund’), the world’s annual GDP is about $80 trillion today. US ‘current dollar’ GDP now exceeds $21 trillion. In Q1 of 2019, nominal GDP grew by 3.8%…following a 4.1% increase in Q4, 2018. We remain about 25% of global GDP. Other than China — a distant second at around $12 trillion — the GDP of no other country is close. We can’t forget about the EU — collectively their GDP almost equals the U.S. So, together, the U.S., the EU and China generate about 2/3 of the globe’s economic output. Worth watching, right?

The objective of the SHI10 and this blog is simple: To predict US GDP movement ahead of official economic releases — an important objective since BEA (the ‘Bureau of Economic Analysis’) gross domestic product data is outdated the day it’s released. Historically, ‘personal consumption expenditures,’ or PCE, has been the largest component of US GDP growth — typically about 2/3 of all GDP growth. In fact, the majority of all GDP increases (or declines) usually results from (increases or decreases in) consumer spending. Consumer spending is clearly a critical financial metric. In all likelihood, the most important financial metric. The Steak House Index focuses right here … on the “consumer spending” metric. I intend the SHI10 is to be predictive, anticipating where the economy is going – not where it’s been.

Taking action: Keep up with this weekly BLOG update. Not only will we cover the SHI and SHI10, but we’ll explore related items of economic importance.

If the SHI10 index moves appreciably -– either showing massive improvement or significant declines –- indicating growing economic strength or a potential recession, we’ll discuss possible actions at that time.

The BLOG:

“Who’s right?” is the question. Who knows is the answer. Yeah, I know what you’re thinking, “Terry! You’re supposed to know these things and TELL US what’s gonna happen !!!!” Right. Got it.

OK, here’s the good news: I will tell you what’s gonna happen. However, unfortunately, I can’t tell you when.

WHAT: Bond traders are usually right about these things. Consumer belief and behavior tends to be the final confirmation that we’re heading toward a recession. With their fingers firmly on the economic pulse, as a group bond traders closely monitor corporate earnings, debt issuance, debt ratings, default levels, etc., because they bet their own money, every day, in search of yield while, at the same time, preventing loss. The yield curve, a reflection of global bond trader collective mentality, is telling us a recession is coming. And the curve is suggesting the recession’s start is likely hastened by the imbroglio between China and the US.

WHEN: Probably sooner than I thought a few months ago. Why? The traders/yield curve is right: This “trade thing” is really screwing up our economy. The biggest causality is confidence. Not consumer confidence, mind you. That’s at a 15 year high. No, the trade war is messing with the heads of business leaders and CEOs across the globe. Today, they are far less confident about the future. They are worried about supply chains, tariffs, input costs, and a whole host of other new concerns, all of which add up to significant uncertainty about the future. And when business leaders and CEOs are uncertain, they pull back. They reduce investment in plant/equipment. They spend less money. They become more cautious.

All of which, unfortunately, tend to lead to a recession. Diminishing business leader and CEO confidence is the message the bond market is telegraphing. If this condition continues for the next few months … or longer … our current business expansion is doomed. Of course, not before it becomes the longest expansion in US history. The past record — held by March, 1991 thru March, 2001 — will be tied next month. In June. According to the National Bureau of Economic Research (NBER), the current expansion began in June of 2009. It’s been a bumpy ride, but the expansion continues. It’s ‘taken a lickin’, and it keeps on tickin.’ (OK, who among you doesn’t know this slogan? Look it up.) In June it will tie the record. In July, it will break it.

If you ask consumers, like the University of Michigan did, they are clearly saying party on! “We’re feeling good!” they’re saying. But the bond traders, and the financial markets in general, aren’t as giddy. They are worried. And I wish I could say it’s only the US financial markets that are worried. But, unfortunately, it’s pretty much all of them, across the globe. Here are a handful of negative yielding 10-year sovereign bonds:

- 10-year German Bund: Negative <0.18>%

- 10-year BOJ (Japan): Negative <0.09>%

- 10-year Swiss yield: Negative <0.46>%

But here’s some good news for you, if you’re looking for a positive yield: Go buy the generic 10-year Italian bond! You can get 2.64% today! At least, you can get it until Italy decides not to pay it. With a 10.7% current unemployment rate and a barely-positive GDP growth rate, Italy is in poor shape. Seriously: Don’t buy Italian bonds. Bad idea.

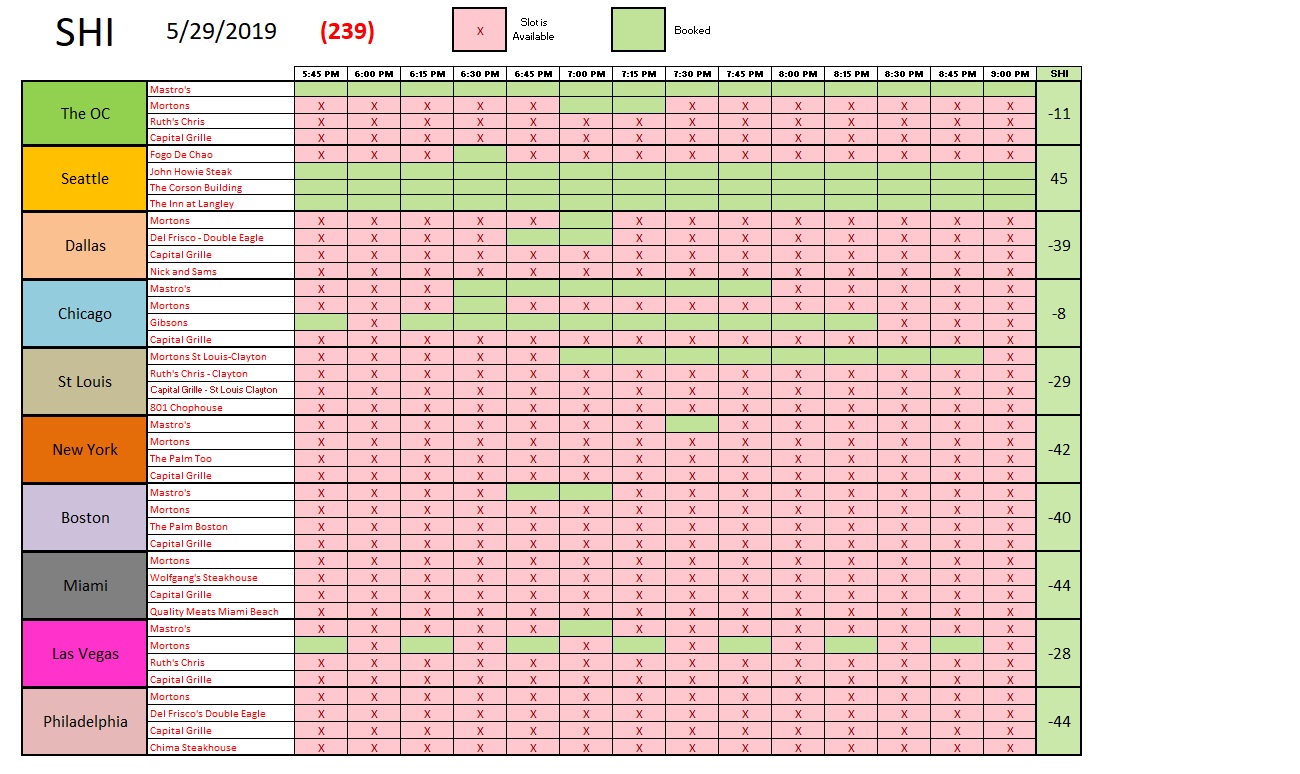

A much better idea is to head to your local, expensive, opulent steakhouse and enjoy a grilled T-Bone and a bottle of 2005 Chateau Petrus. Let’s see if you can get a reservation:

It looks like you can. In fact, from the sea of green below, you pretty much have your pick of time slots in any of the 40 restaurants in 10 cities in the SHI10:

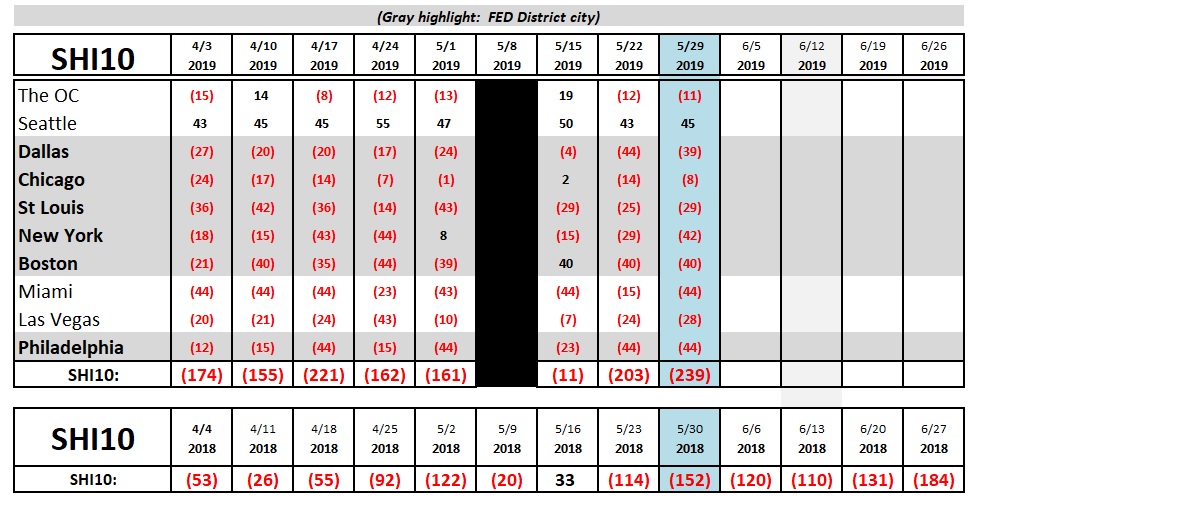

In Philly and Miami, your party of 4 can dine at any steakhouse, in any time slot you wish. And in every other city, with the exceptions of Seattle and the OC, every steakhouse has plenty of openings. But while a negative 239 is a lackluster SHI10 reading, it’s not out of line for this same time one year ago. Here is the larger trend report:

It is interesting that the SHI10 does not align with the overall consumer confidence reading from the UofM. Perhaps the explanation is we are seeing a bifurcation within the consumer ranks: Perhaps we have a ‘general’ confidence reading from the UofM; and, from our more affluent, more business-centric expensive steak-eaters, a reflection of a less robust confidence level.

The SHI10 reflects weak reservation demand, but not to a worrisome level.

Oh … Are you curious about this week’s photo image? That’s a recent picture of Mr. Everest. Pricey steakhouses may not be crowded this Saturday, but Everest is. From what I’ve read, during “good weather” periods, the wait line to summit the peak can add more than 1.5 hours to the climb. Ouch. I’d rather be at Ruths Chris enjoying a beautifully grilled fillet.

– Terry Liebman