SHI 6.12.19 – Where Did Inflation Go?

SHI 6.5.19 – Battle Rope Exercises

June 5, 2019

SHI 6.19.19 – The Fed Holds Pat

June 19, 2019“Like Elvis, inflation has left the building.”

After rising from the dead like Lazarus at the beginning of 2019, inflation is once again heading toward zero. From November of 2018 thru January of 2019, the month-over-month change in the CPI was zero. By March of ’19, the CPI had lifted to .4% — annualized almost 5%. But since that high-water mark, the CPI has slid back toward zero. In May, the reading was a paltry 0.1%. As “Mr. Wonderful” from Shark Tank is known to say, “You’re dead to me!”

Where’d inflation go? Will it come back? Are the rumors of its demise greatly exaggerated?

Welcome to this week’s Steak House Index update.

If you are new to my blog, or you need a refresher on the SHI10, or its objective and methodology, I suggest you open and read the original BLOG: https://www.steakhouseindex.com/move-over-big-mac-index-here-comes-the-steak-house-index/

Why You Should Care: The US economy and US dollar are the bedrock of the world’s economy. This has been the case for decades … and will be true for years to come.

But is the US economy expanding or contracting?

According to the IMF (the ‘International Monetary Fund’), the world’s annual GDP is about $80 trillion today. US ‘current dollar’ GDP now exceeds $21 trillion. In Q1 of 2019, nominal GDP grew by 3.8%…following a 4.1% increase in Q4, 2018. We remain about 25% of global GDP. Other than China — a distant second at around $12 trillion — the GDP of no other country is close. We can’t forget about the EU — collectively their GDP almost equals the U.S. So, together, the U.S., the EU and China generate about 2/3 of the globe’s economic output. Worth watching, right?

The objective of the SHI10 and this blog is simple: To predict US GDP movement ahead of official economic releases — an important objective since BEA (the ‘Bureau of Economic Analysis’) gross domestic product data is outdated the day it’s released. Historically, ‘personal consumption expenditures,’ or PCE, has been the largest component of US GDP growth — typically about 2/3 of all GDP growth. In fact, the majority of all GDP increases (or declines) usually results from (increases or decreases in) consumer spending. Consumer spending is clearly a critical financial metric. In all likelihood, the most important financial metric. The Steak House Index focuses right here … on the “consumer spending” metric. I intend the SHI10 is to be predictive, anticipating where the economy is going – not where it’s been.

Taking action: Keep up with this weekly BLOG update. Not only will we cover the SHI and SHI10, but we’ll explore related items of economic importance.

If the SHI10 index moves appreciably -– either showing massive improvement or significant declines –- indicating growing economic strength or a potential recession, we’ll discuss possible actions at that time.

The BLOG:

Inflation appears to be DOA. Sure, the FED claims this condition is “transitory,” but I’m not so sure. By any of the numerous metrics we employ to track this cagey beast, with the passing of each month inflation seems to sink lower and lower, full-employment and FED efforts notwithstanding. Consider this:

- From the BLS today on the CPI: “The Consumer Price Index for All Urban Consumers (CPI-U) increased 0.1% in May on a seasonally adjusted basis after rising 0.3% in April, the U.S. Bureau of Labor Statistics reported today. Over the last 12 months, the all items index increased 1.8 percent before seasonal adjustment.”

- From the BEA on 5/31 on “Personal Income and Outlays”: While the PCE increased slightly in April, the ‘percentage change from month one year ago’ — the annual PCE rate — is running at 1.5%.

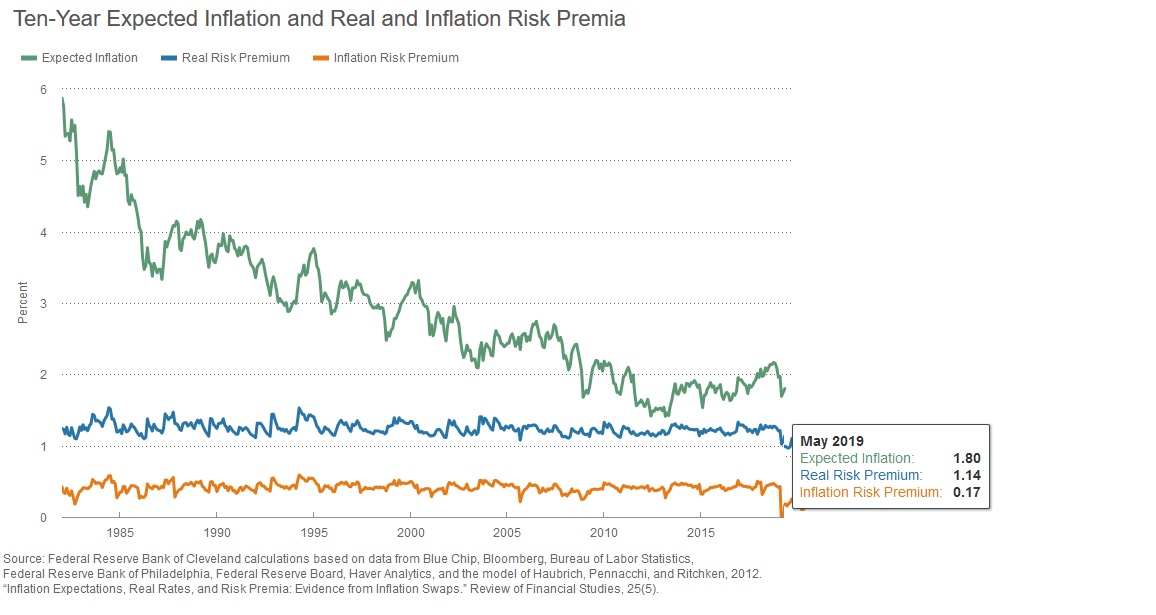

- Finally, from the Federal Reserve Bank of Cleveland on May 10th, inflation expectations are near an all time low. Take a look at the graphic below:

Expected inflation is now down to 1.8%.

Do you notice the phrase ‘Inflation Risk Premium’ in the graphic? Think of this number as the additional ROI an investor needs to compensate them for inflation risk. 0.17%. A pittance.

These are low, low numbers. Whether viewed thru the lens shown above — from about 1980 — or over the longer term — say the past 200 years — these are low, low numbers.

Martin Feldstein, a brilliant Harvard economist, just passed away. He will be missed. He was a luminary, considered by many to be one of the greatest economic minds ever. One of his most revered quotes was:

“Inflation is always and everywhere a monetary phenomenon.”

Perhaps. But what causes inflation? And conversely, what causes deflation?

Back in 1984, Frederic Mishkin wrote a paper for the NBER entitled “The Causes of Inflation.”

Here is the abstract, or summary, from the NBER site:

- This paper attempts to provide a perspective on the causes of inflation by exploring why sustained inflations occur and the role of monetary policy in the inflation process. The conclusion reached in this paper is that in the last ten years there has been a convergence of views in the economics profession on the causes of inflation. As long as inflation is appropriately defined to be a sustained inflation, macro-economic analysis, whether of the monetarist or Keynesian persuasion, leads to agreement with Milton Friedman’s famous dictum, “Inflation is always and everywhere a monetary phenomenon.”

- However, the conclusion that inflation is a monetary phenomenon does not settle the issue of what causes inflation because we also need to understand why inflationary monetary policy occurs. This paper also examines this issue and it finds that the underlying cause of inflation in the United States has been accommodating monetary policy geared to achieving a high employment target. The role of expectations has been important in the inflationary process so that to prevent the resurgence of inflation at a minimum cost in terms of unemployment and output loss, monetary policy must be both non-accommodating and credible.

Remember: This article was written in 1984. At a time when the battle to tame inflation was raging. Back then, inflation was too high and out of control. And, truly, monetary policy was a culprit behind the huge spike. But that was then ….

The abstract uses the words ‘credible‘ and ‘expectations.’ So while an exceptionally loose monetary policy may be an inflation trigger, ultimately the people within the economy in question must be convinced that the battle to either kill inflation — the objective in the 1980s, or stoke inflation — the current FED objective, must be credible, and must be in alignment with the expectations of the citizens. And those expectations, ultimately, are formed by personal experience and perception. In the aggregate. At least here in the US.

Because as a blunt tool, used and abused for the wrong reasons, monetary policy can easily trigger boatloads of inflation. For example, Venezuela has experienced hyper-inflation in the past 3-5 years. Their money supply has grown like a garden of weeds. Out of control.

So the challenge is to control inflation, with targeted results, within an acceptable range — without permitting it to become a raging wildfire, threatening to take down the entire economy as prices rise to the heavens.

In my understanding, Feldstein’s vision of inflation was fairly simple: By increasing or decreasing money supply, above or below the nominal GDP growth rate, using this methodology as a lever, the FED can increase or decrease the level of sustained inflation.

OK, after re-reading that sentence, it seems exceptionally dense to even me. Let me simplify my own comments for a change. Here we go. 🙂

Suppose the FED wants to increase inflation. As they do right now. According Feldstein’s theory, the FED simply has to consistently increase the supply of US dollars sloshing around the economy at a rate that is slightly higher than the nominal (not adjusted for inflation) growth rate of the US GDP. What is the current nominal GDP growth rate? I mention it at the start of the blog each week — right now, about 4%. So, in theory, if the FED wants to increase inflation, they simply have to increase money supply by a rate that’s slightly higher than 4% … and VIOLA! Inflation is here again! Simple right?

Perhaps in theory. If it was that easy, Central Banks around the globe could easily hit their inflation targets. Yet Central Banks from Japan to Europe, from Australia to the US are all struggling with this problem. It has not been transitory.

The challenge, I believe, is the inherent nature of the problem in today’s world. While the underlying methodology (described above) may be well understood, applying those principals in the real world is far more difficult for these reasons:

- Nominal GDP doesn’t hold still. It fluctuates constantly … officially changing every 3 months. And the fluctuations are sizable. How the heck can the FED set a money supply growth rate target based on an underlying metric that is constantly moving and changing?

- US money supply, in and of itself, is no longer easily definable or quantifiable. You’d think it would be, right? I mean, we have to know how many dollars are out there, floating around the world, right? Consider this question: Are ‘eurodollars’ and ‘asia-dollars’ included in the formal US money supply definition? Hmmm…good luck with this one. How about currency moving in and out of foreign exchanges? How about dollar-denominated sovereign debt issued in other countries? Is this part of US money supply? Today, the USD is the backbone behind about 2/3 of all global finance. So, because the US dollar is the ‘world currency,’ movement within our money supply more closely resembles an amoeba than your bank account.

- Finally, the FED’s target is really small. Infinitesimal, really. Let me say this another way: If the FED wanted to increase inflation to 10% per annum, it would be much easier than increasing inflation to 2.0% from 1.0 or 1.5%. This is a very, very small increase, more of a course correction, really. A big change would be relatively easy to achieve. This one is not.

Think of it this way: The FED is tasked with throwing a limp thread thru the eye of a tiny needle while traveling in a car at 65 miles per hour, on a bumpy road. With the windows open. Good luck.

It’s much easier to get a reservation for a party of 4 this Saturday at our extravagant eateries. Can we get into Mastros this weekend?

We sure can. While the 2018/2019 gap for this week has narrowed a bit, there are plenty of open reservation slots around the United States for you and your guests this weekend. The world is your oyster! Here are the weekly stats:

Once again, things look bleak for pricey steakhouses in Philly, Miami, and Dallas. The cows are safe this weekend. Philly and Dallas are both FED district cities … so I’ll pay close attention to the FED comments on these two cities in their next ‘Beige Book.’

In summary, for now, as another week drops behind us, I see no reason to believe the current inflation weakness is transitory, nor do I have high expectations for Q2 GDP performance. The SHI seems to agree.

Thanks for tuning in.

– Terry Liebman