SHI 6.16.21 – The Big Apple is Back!

SHI10 6.9.21 – Quite a JOLT!

June 9, 2021

SHI 6.23.21 — Tales From the Crypt-Oh!

June 23, 2021

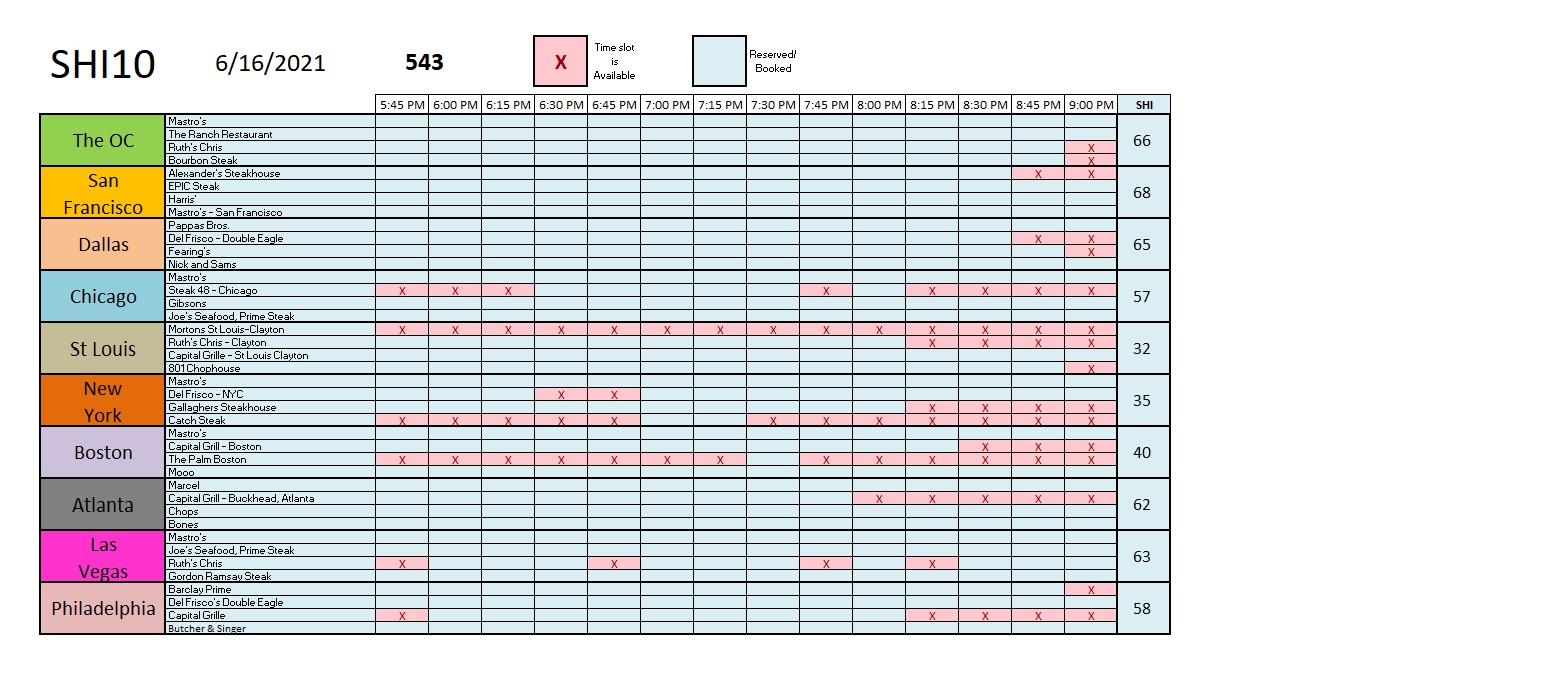

Beef prices may be up, but opulent eaters in NYC don’t seem to care. Reservation demand is strong. Check out this week’s SHI10:

For the first time since the pandemic, the SHI for New York’s expensive steak houses is out of the red. This is a first since putting the pandemic in the rear-view mirror. Mastros is fully booked for this coming Saturday … only Catch Steak has widespread availability. New York is back and pricey restaurants are booking up. Further, ‘Broadway’ has announced that beginning in September, theatres can now reopen at full capacity and dozens of Broadway shows have confirmed they will return as soon as possible.

“

NYC is opening up!“

“NYC is opening up!“

New York City. Broadway shows. The Rockettes 2021 Chrismas Special. Sky-high Pastrami on rye. It’s all back. And so are the other nine (9) SHI cities on the chart above. In fact, only St Louis has a high-dollar steakhouse that is fully available for this coming Saturday. Across the US, in ten cities with four (4) restaurants each, only 1 expensive steakhouse out of 40 offers reservations at every time slot. Restaurant reservations at pricey eateries, like used cars, are in high demand!

Welcome to this week’s Steak House Index update.

If you are new to my blog, or you need a refresher on the SHI10, or its objective and methodology, I suggest you open and read the original BLOG: https://www.steakhouseindex.com/move-over-big-mac-index-here-comes-the-steak-house-index/

Why You Should Care: The US economy and US dollar are the bedrock of the world’s economy.

But is the US economy expanding or contracting?

The short answer? Expanding. A lot. Forever more, COVID-19 will be mentioned concurrently with any discussion about 2020 GDP. Collectively, the world’s annual GDP was about $85 trillion by the end of 2020. But I am confident all 2021 GDP discussions will start with a nod to the blowout 1st quarter GDP growth number, because our ‘current dollar’ GDP grew at the annual rate of 10.7%! Annualized, America’s GDP blew past $22 trillion during the quarter, settling in at $22.0489 trillion. The US, the euro zone, and China continue to generate about 70% of the global economic output.

The objective of this blog is singular.

It attempts to predict the direction of our GDP ahead of official economic releases. Historically, ‘personal consumption expenditures,’ or PCE, has been the largest component of US GDP growth — typically about 2/3 of all GDP growth. In fact, the majority of all GDP increases (or declines) usually results from (increases or decreases in) consumer spending. Consumer spending is clearly a critical financial metric. In all likelihood, the most important financial metric. The Steak House Index focuses right here … on the “consumer spending” metric. I intend the SHI10 is to be predictive, anticipating where the economy is going – not where it’s been.

Taking action: Keep up with this weekly BLOG update. Not only will we cover the SHI and SHI10, but we’ll explore related items of economic importance.

If the SHI10 index moves appreciably -– either showing massive improvement or significant declines –- indicating growing economic strength or a potential recession, we’ll discuss possible actions at that time.

The Blog:

As I write this blog, I’m watching the Jerome Powell press conference on CNBC. The FED just released their post-meeting statement. In response, all equity markets immediately tanked, the 10-year Treasury spiked by more than 10 basis points, and gold prices fell. All of which I find quite surprising, in that the FED statement said:

“Amid this progress and strong policy support, indicators of economic activity and employment have strengthened.”

Which makes the macro-market sell-off all that much more surprising. Especially, since for the first time since I’ve been tracking FED commentary and forecasts, the FEDs “Summary of Economic Projections” (which accompanied the FED statement) is now projecting a 7.00% ‘real’ increase in the GDP in 2021!

That is amazing. Recall that our ‘current dollar’ GDP exceeds $22 trillion. Assuming a 3% inflation for this year, that means US GDP could grow by over $2.2 trillion this year. That is a staggering increase. The US hasn’t seen growth like this for more that 2 or 3 decades. And the FED forecasts a 3.3% growth rate the following year in 2022 … which could add about another trillion dollars to the annual US economy. These are huge numbers … numbers I frankly never thought we’d see again in this country.

And yet the markets were selling off … ostensibly demonstrating their unhappiness. Odd. Massive growth … a burgeoning economy … but stocks are lower.

Why? I suspect this “inflation thing” has people flummoxed and confused. Which makes sense given the ubiquitous news stream around things like used car sales, lumber, and home prices. Supplies are crimped for various reasons, and demand is soaring. Causing prices to surge … and inserting the “inflation thing” into everyone’s psyche. But, again, the FEDs message today was clear:

“Inflation has risen, largely reflecting transitory factors.”

And in fact, the FED now forecasts “PCE Inflation” growth in 2021 of 3.4%. This is up one full percentage point from the prior FED meeting 6 weeks ago. But as the DJIA and S&P500 were down today, inflation clearly remains a concern. Suggesting gold prices should rise in response. Nope. Gold prices were down today too. Odd.

How can I explain these odd and contradictory behaviors? Simple: Once again, Coronavirus is the culprit. These are unprecedented times. Without a road map, we find ourselves without easy signals to follow. The fear that the FED could be wrong, and inflation is not transitory, seems to rule to day. But here’s a though? Could they be right? 🙂

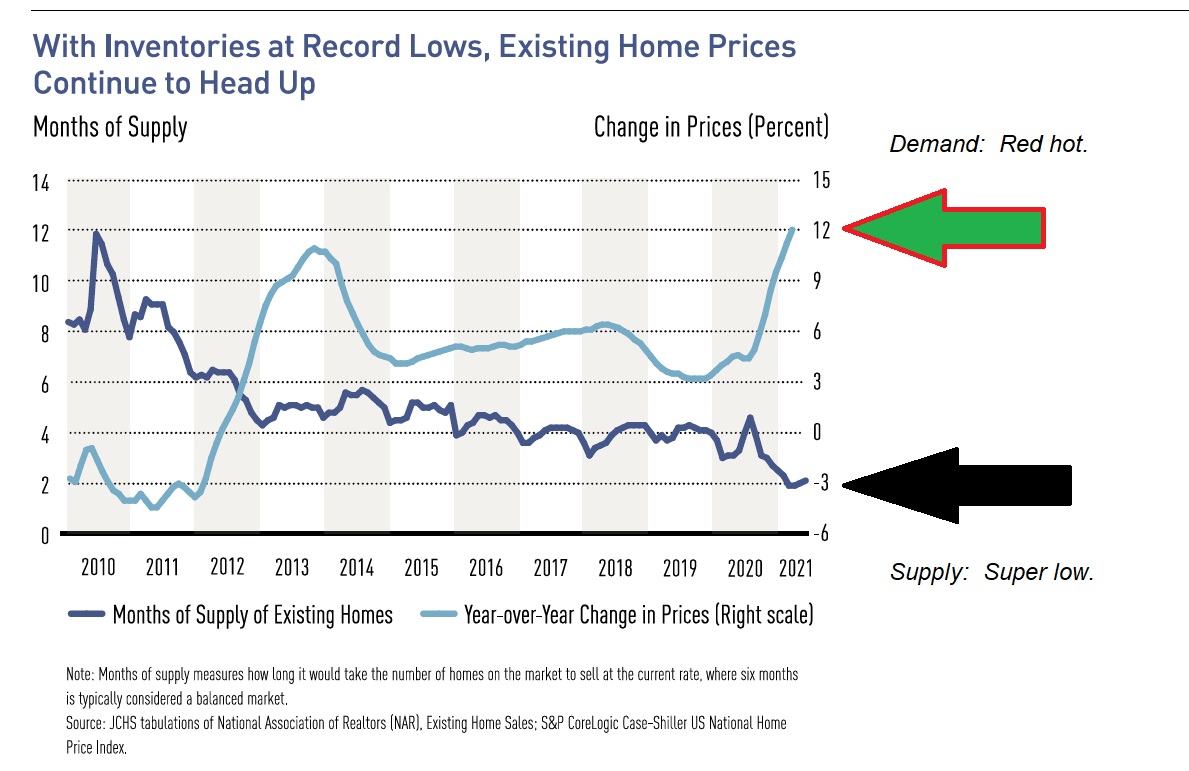

Oh, I mentioned housing above. permit me one more quick comment on housing and home values before we return to the steak houses. Once again, supply and demand are driving the markets. Take a look at this graphic, courtesy of Harvard University’s “State of the Nation’s Housing 2021” report:

Is this inflation? No, not by the traditional definition … but I would put this into the category of asset inflation. And unlike lumber and car prices, this problem lacks a potential fix. At least a fast one. No, this problem is likely to be with us for many more years. Why? New home development (supply) simply cannot keep up with demand. The Harvard report places the “supply” blame primarily on “restrictive land use regulations” across the country:

“Restrictive land use regulations are among the most significant barriers to housing production … In addition, some land use and zoning practices, as well as other local and state requirements, restrict the amount of land available for development … Many communities also require multiple approvals for residential developments ….”

This is a real problem. Unfortunately, our political leaders have formulated no public policy to resolve it. And, thus, Harvard’s conclusion is:

“Given the extremely limited supply of homes for sale across the country, prices will likely continue to rise for the foreseeable future even if interest rates tick up and more sellers put their homes on the market.”

There you have it. If we can’t believe the folks at Harvard, who can we believe? (You’ll recall that FED chairman Powell went to Princeton … perhaps that’s why people don’t believe him on the “inflation thing?”) 🙂

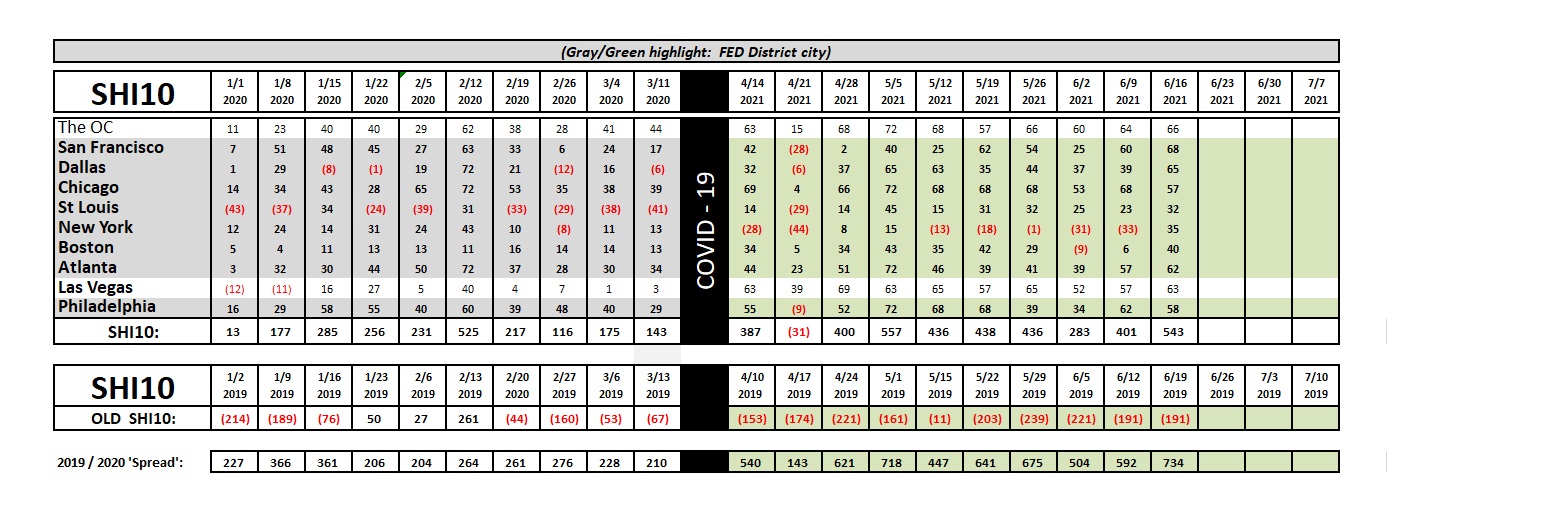

Moving from the ‘people houses’ to the steak houses, here’s the longer-term trend report:

A ‘spread’ of 734 is the biggest we’ve ever seen.

Steakhouses are booked. People are spending tons of money. The FED is now forecasting full-year GDP growth of 7.00% in 2021. Yes, costs and prices are up … but this trend is likely to continue in many segments of our economy for quite some time. If you were waiting for a strong economy to invest or expand your business, I suggest you wait no longer. My opinion only, but the time is now.

<|> Terry Liebman