SHI 6.26.19 – A Sea of Red

SHI 6.19.19 – The Fed Holds Pat

June 19, 2019

SHI 7.3.19 – A Celebration is in Order

July 3, 2019

“Red dominates the SHI10 this week. Your concern about our economy should be elevated.”

The SHI, at its essence, is designed to be an economic barometer. Using the level of consumer spending at expensive steakhouses as our metric, the SHI should give us a window into the consumer’s mind, evidenced by their willingness to spend exorbitant amounts for a slab of beef. What are well-heeled consumers thinking? Is their spending frothy? Or is it leaner than a rare, 8-ounce filet Mignon with a bright red center? Unfortunately, more the latter than the former. Once again, reservation activity is sparse … suggesting overall consumer demand continue to wane. Meaningfully. And disconcertingly.

Welcome to this week’s Steak House Index update.

If you are new to my blog, or you need a refresher on the SHI10, or its objective and methodology, I suggest you open and read the original BLOG: https://www.steakhouseindex.com/move-over-big-mac-index-here-comes-the-steak-house-index/

Why You Should Care: The US economy and US dollar are the bedrock of the world’s economy. This has been the case for decades … and will be true for years to come.

But is the US economy expanding or contracting?

According to the IMF (the ‘International Monetary Fund’), the world’s annual GDP is about $80 trillion today. US ‘current dollar’ GDP now exceeds $21 trillion. In Q1 of 2019, nominal GDP grew by 3.8%…following a 4.1% increase in Q4, 2018. We remain about 25% of global GDP. Other than China — a distant second at around $12 trillion — the GDP of no other country is close. We can’t forget about the EU — collectively their GDP almost equals the U.S. So, together, the U.S., the EU and China generate about 2/3 of the globe’s economic output. Worth watching, right?

The objective of the SHI10 and this blog is simple: To predict US GDP movement ahead of official economic releases — an important objective since BEA (the ‘Bureau of Economic Analysis’) gross domestic product data is outdated the day it’s released. Historically, ‘personal consumption expenditures,’ or PCE, has been the largest component of US GDP growth — typically about 2/3 of all GDP growth. In fact, the majority of all GDP increases (or declines) usually results from (increases or decreases in) consumer spending. Consumer spending is clearly a critical financial metric. In all likelihood, the most important financial metric. The Steak House Index focuses right here … on the “consumer spending” metric. I intend the SHI10 is to be predictive, anticipating where the economy is going – not where it’s been.

Taking action: Keep up with this weekly BLOG update. Not only will we cover the SHI and SHI10, but we’ll explore related items of economic importance.

If the SHI10 index moves appreciably -– either showing massive improvement or significant declines –- indicating growing economic strength or a potential recession, we’ll discuss possible actions at that time.

The BLOG:

Sometimes we want to see red. My wife LOVES rare steaks. If she doesn’t see a lot of red, she’s not happy. Me, I’m more of a ‘medium-rare’ kind of guy … so I’m OK with a little less red. But I better see a bottle of red wine on the table! The more red the better!

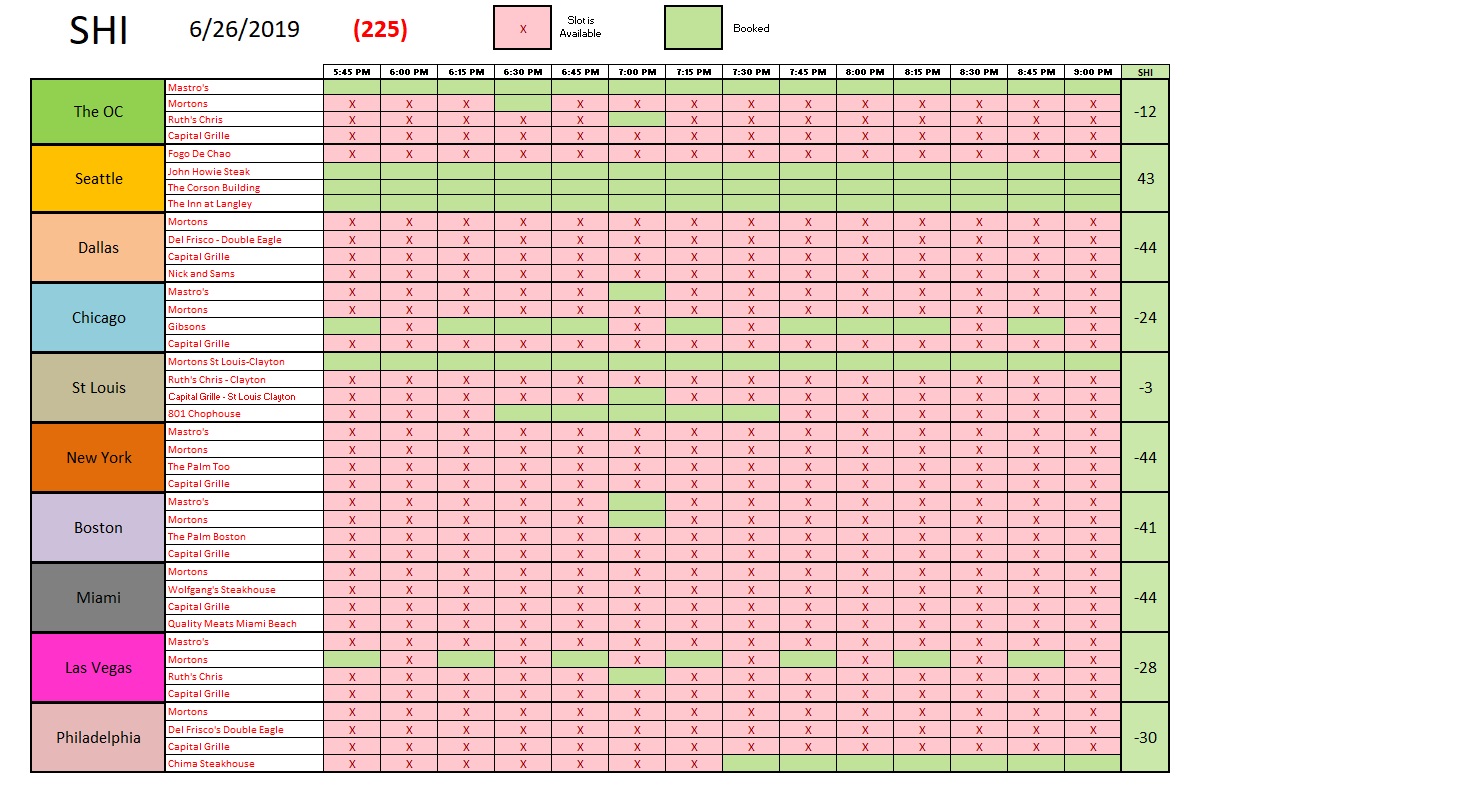

But if red is the predominant color on the weekly SHI10 report, as it is today, that’s worrisome. Because it indicates that US economic weakness is becoming more pervasive:

Other than Seattle, I see a lot of red. Not good.

Until yesterday, most indices tracking ‘Consumer Confidence’ here in the US were fairly robust. Consumers were feeling confident about the future. Seemingly until yesterday. Here are the comments from Lynn Franco, the Senior Director of Economic Indicators at the US Conference Board:

- “After two consecutive months of improvement, Consumer Confidence declined in June to its lowest level since September 2017 (Index, 120.6).”

- “The decrease in the Present Situation Index was driven by a less favorable assessment of business and labor market conditions.

- “The escalation in trade and tariff tensions earlier this month appears to have shaken consumers’ confidence.”

- “Although the Index remains at a high level, continued uncertainty could result in further volatility in the Index and, at some point, could even begin to diminish consumers’ confidence in the expansion.”

The words “shaken confidence,” and “continued uncertainty” ring true. They have been appearing on the lips of central bankers around the world, in the gut of the financial markets, and now more extensively in the SHI10. Demand for reservations at our steakhouses appears to reflect the same diminished demand, the same uncertainty.

Sovereign interest rates are down here in the US and around the globe. The 10-year US Treasury recently closed below 2%. Across the pond, in the country facing Brexit and massive uncertainty, the 10-year UK bond is trading at a whopping 0.83%. By comparison to Germany, that’s a high rate. German’s 10-year ‘Bund’ is trading at a negative 0.30%. In fact, around the globe today, there are more sovereign bonds trading with negative interest rates than ever before.

These conditions are not indications of economic strength. They are indications of fear. And fear that global deflation is a reality.

Of course, none of these indicators are facts. Like the SHI, they offer us a view into a potential future. It’s entirely possible the central banks around the world will be able to pull another rabbit out of their collective hats and avoid another general slowdown. And, of course, it’s possible Powell and his friends on the FED may be able to do the same thing here in the US. The direction of the US economy is unknown. Of course.

Given the low level of inflation, it’s very possible the FED will cut short term rates at the end of July, as a precautionary measure given the flashing red lights. But it may be too little too late, since it takes a good amount of time for the economic benefits of a rate cut to make their way thru our economy. But it should be done regardless … and perhaps it will help turn those flashing red lights yellow.

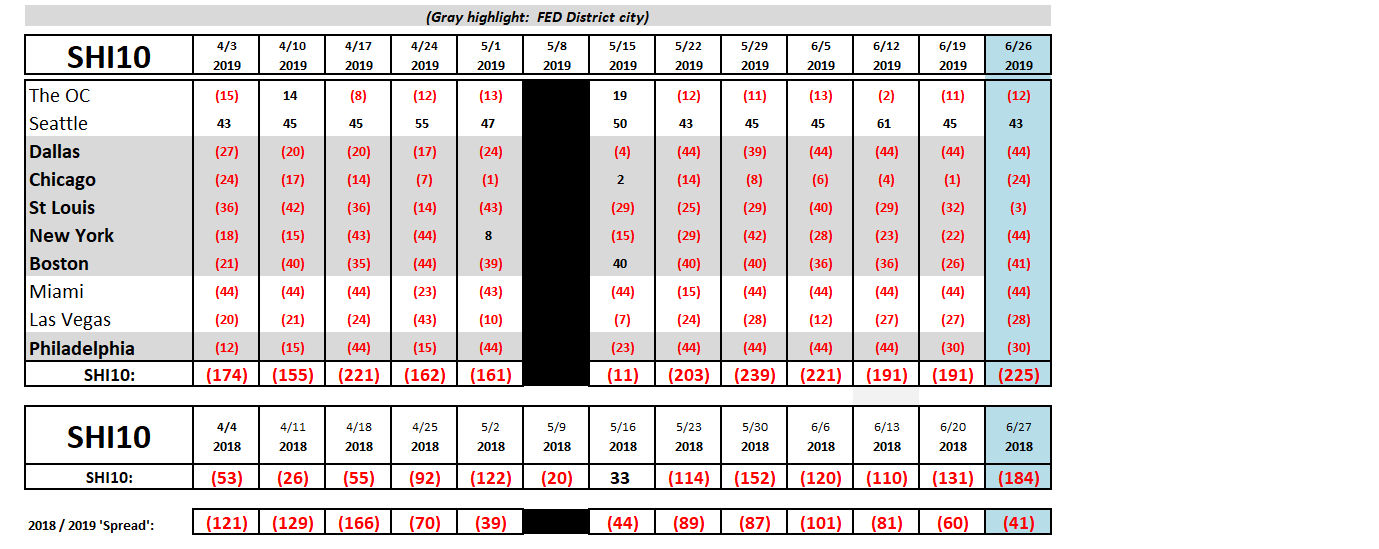

Here’s the longer term trend report:

One meaningful observation is the ‘spread’ between 2018 and 2019 is narrower this week. That’s a good sign. But this one good metric aside, I still see an awful lot of red in this chart.

My suggestion: Drink copiously. Preferably red wine. Enjoy your steak!

- Terry Liebman