SHI 7.3.19 – A Celebration is in Order

SHI 6.26.19 – A Sea of Red

June 26, 2019

SHI 7.10.19 – Superforecasting and Inflection Points

July 10, 2019

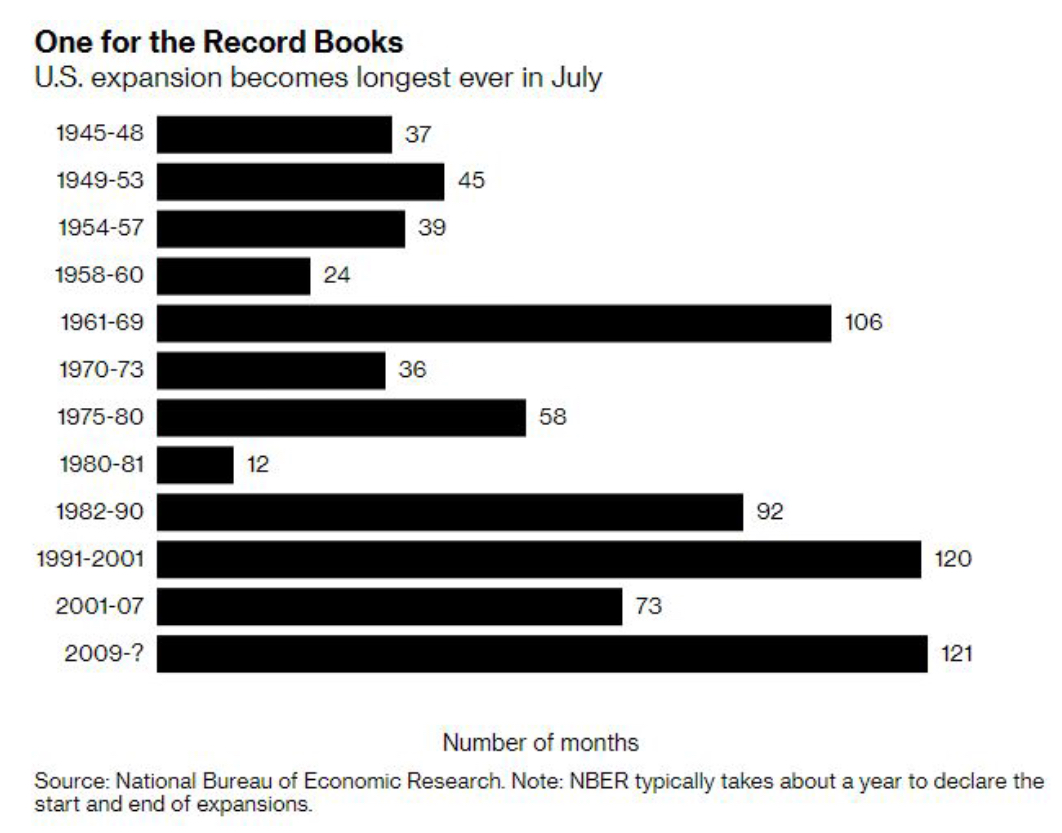

“As long-time readers of my blog know, our economic expansion is now the longest on record.”

Break out the champagne! This month, our US economic expansion celebrates its 10th birthday. Business cycles have been measured by the ‘National Bureau of Economic Research’ (NBER) since 1854. On July 1, our current cycle became the longest ever. So this July 4th we have many things to celebrate!

And, as my long-time readers also know, we also have plenty to worry about.

- How “old” will our expansion become before its nemesis — CONTRACTION — arrives here in the US?

- What forces, within the US and globally, should we now watch with concern?

- And, finally, what the heck is “the GFC?”

For these answers and more … read on!

Welcome to this week’s Steak House Index update.

If you are new to my blog, or you need a refresher on the SHI10, or its objective and methodology, I suggest you open and read the original BLOG: https://www.steakhouseindex.com/move-over-big-mac-index-here-comes-the-steak-house-index/

Why You Should Care: The US economy and US dollar are the bedrock of the world’s economy. This has been the case for decades … and will be true for years to come.

But is the US economy expanding or contracting?

According to the IMF (the ‘International Monetary Fund’), the world’s annual GDP is about $80 trillion today. US ‘current dollar’ GDP now exceeds $21 trillion. In Q1 of 2019, nominal GDP grew by 3.8%…following a 4.1% increase in Q4, 2018. We remain about 25% of global GDP. Other than China — a distant second at around $12 trillion — the GDP of no other country is close. We can’t forget about the EU — collectively their GDP almost equals the U.S. So, together, the U.S., the EU and China generate about 2/3 of the globe’s economic output. Worth watching, right?

The objective of the SHI10 and this blog is simple: To predict US GDP movement ahead of official economic releases — an important objective since BEA (the ‘Bureau of Economic Analysis’) gross domestic product data is outdated the day it’s released. Historically, ‘personal consumption expenditures,’ or PCE, has been the largest component of US GDP growth — typically about 2/3 of all GDP growth. In fact, the majority of all GDP increases (or declines) usually results from (increases or decreases in) consumer spending. Consumer spending is clearly a critical financial metric. In all likelihood, the most important financial metric. The Steak House Index focuses right here … on the “consumer spending” metric. I intend the SHI10 is to be predictive, anticipating where the economy is going – not where it’s been.

Taking action: Keep up with this weekly BLOG update. Not only will we cover the SHI and SHI10, but we’ll explore related items of economic importance.

If the SHI10 index moves appreciably -– either showing massive improvement or significant declines –- indicating growing economic strength or a potential recession, we’ll discuss possible actions at that time.

The BLOG:

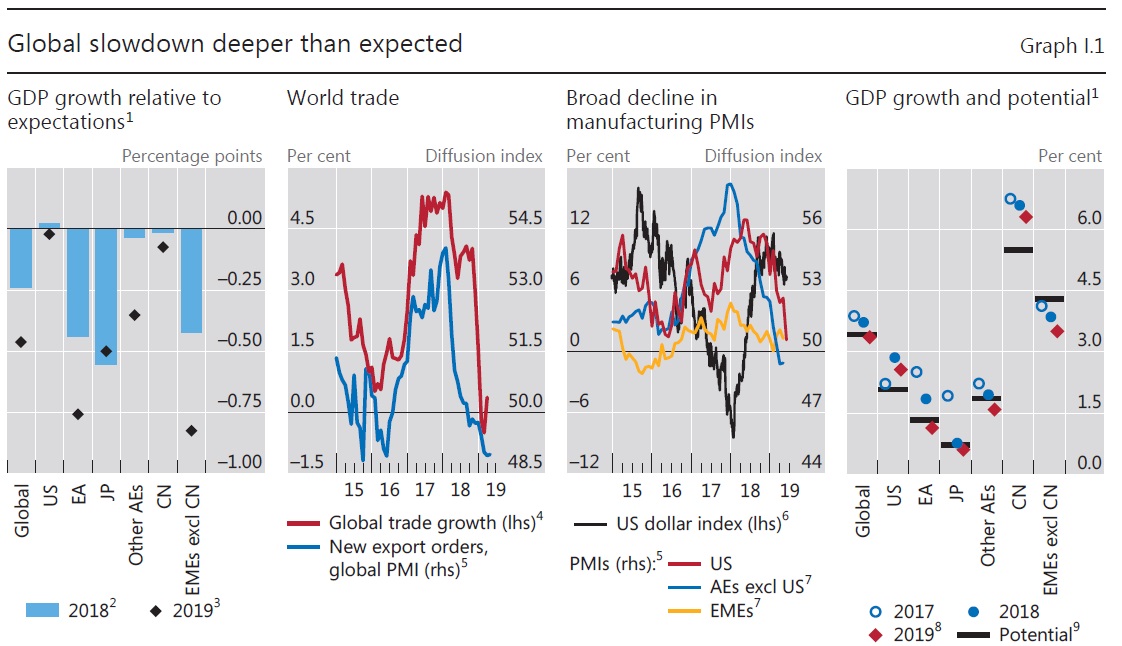

“Over the last 12 months, the global economy slowed down.”

So says the Bank for International Settlements, known worldwide as the BIS, on page 1 of their 2019 annual report. The graphic below, appearing on page 3 of the report, sums it up, both with the heading and the images:

“Global slowdown deeper than expected.” Ouch. Now look at the ‘World trade’ image. In light of the continuing trade war, the steepness of the decline comes as no surprise. The first image reflects the impact of the slowdown on various economies. Clearly, the US is holding up quite well … when compared to our peers around the globe. Interesting.

The BIS describes itself this way:

“Established in 1930, the BIS is owned by 60 central banks, representing countries from around the world that together account for about 95% of world GDP. Its head office is in Basel, Switzerland and it has two representative offices: in Hong Kong SAR and in Mexico City.”

Yes, the BIS is the central bank for central banks. Collectively, the countries represented at the BIS garner 95% of all global earnings. It’s interesting to note that even here, income inequality is a fact. The BIS is owned by 60 countries … that’s 60 out of a total number across the globe of about 195 or 196, depending on who you ask. So the BIS is owned by the central banks of 30% of all countries … and that 30% earns 95% of global income. Fascinating. Who are the BIS members?

https://www.bis.org/about/member_cb.htm

Just days ago, the BIS published their annual report. Trust me: If you are a self-admitted economic wonk, you will want to read this report. It, too, is fascinating. Here’s a link (remember, right click … and select ‘open in another window.’)

https://www.bis.org/publ/arpdf/ar2019e.htm

Here you will learn what ‘GFC‘ means: On page ‘ix’ of the report, you will see this comment:

“Another factor, at work in some of the large economies at the heart of the Great Financial Crisis (GFC), was the financial cycle upswings, most notably in the United States.”

The financial collapse of 2008 now has an official name: The GFC. The Great Financial Crisis. Toss this acronym around at parties … you’ll immediately become the most popular person in the room. Trust me. 🙂

Maybe not. Regardless, I suspect decades from now, this is the name by which it will be known. And, according to the BIS report, it may have ushered in a new era in the business cycles. Per the report:

“Less appreciated is the fact that ever since inflation has been low and stable,

starting some three decades ago, the nature of business fluctuations has changed.

Until then, it was sharply rising inflation, and the subsequent monetary policy

tightening, that ushered in downturns. Since then, financial expansions and

contractions have played a more prominent role.”

Interesting. Since the FED was first formed back in 1913, they have struggled to contain the cycles of rising and falling inflation within the US financial system. This is one of their primary mandates. And we all know the FEDs current inflation target is 2% per year. But the BIS report suggests inflation in the US and across the globe continues to be muted by:

- Globalization

- Technology

- Demographics

Sound familiar? I’ve been touting these inflation-constraining factors for years. I completely agree. Longer term, the BIS believes four “longer-term forces” (including chronic, cyclically low inflation) are at work … possibly adversely impacting global economic growth:

- Muted inflation. The bottom line: the relationship between labor cost and prices has weakened. The three factors above have reduced — not eliminated, mind you, but reduced — the relationship between pricing power and labor input costs. As a result, inflation from traditional sources has been and will likely continue to be, muted.

- Financial markets. The report suggests we now live in a “financially highly integrated world.” Got it. So, we must now pay much greater attention to “financial markets, credit developments and real estate prices.” Interesting, right?

- Productivity growth. Per the report, the lack of productivity growth is a serious constraint, holding back potential economic growth. Agreed.

- Political and social backlash against “open international order.” If the 20 or 30 years before the GFC were the era of globalization, post-GFC appears to be the opposite. Trade conflicts, protectionism, nationalism, immigration … these factors are big news today. And they are significantly impacting post-globalization economics across the globe.

I again suggest you glance at the report. It really is fascinating … well, at least to me. But if I haven’t convinced you yet, here are the ‘Cliff’s Notes’ of the key economic takeaways from the BIS report:

-

Although global growth appears to have hit a soft patch late last year, the resilience of services and buoyant labour markets bode well for the near term.

-

Risks remain on the horizon. Trade and manufacturing may slow further, especially if trade tensions escalate. Deleveraging in some major emerging market economies, weak bank profits in advanced economies and high corporate debt may all act as a drag on growth.

-

Normalising policy against this backdrop involves potential trade-offs: what is good for today need not necessarily be good for tomorrow. More fundamentally, monetary policy cannot be the engine of growth. A greater role for fiscal, structural and prudential policy would contribute more effectively to sustainable growth.

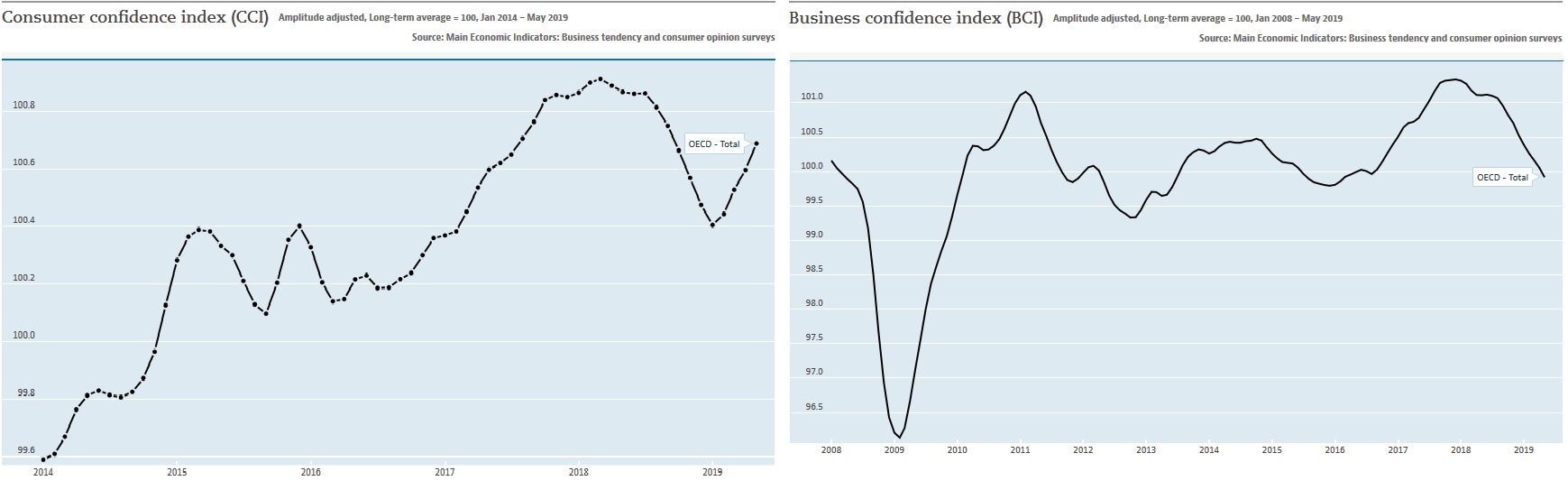

Permit me a brief tangent. The BIS report also touches on “Confidence and uncertainty.” I believe these are very important metrics. So, it’s worth noting, once again, the glaring difference between business and consumers across developed countries — specifically in their belief about the future. Take a look at the image below, courtesy of the OECD. Note the very different direction of 2019 ‘confidence’ for consumers and business:

Consumer confidence is lifting … but business confidence continues to decline. Consumers are feeling better about the future as 2019 unfolds, but business are not. Again, interesting.

OK…after all that hard work, you deserve a steak. Let’s head to the steakhouses!

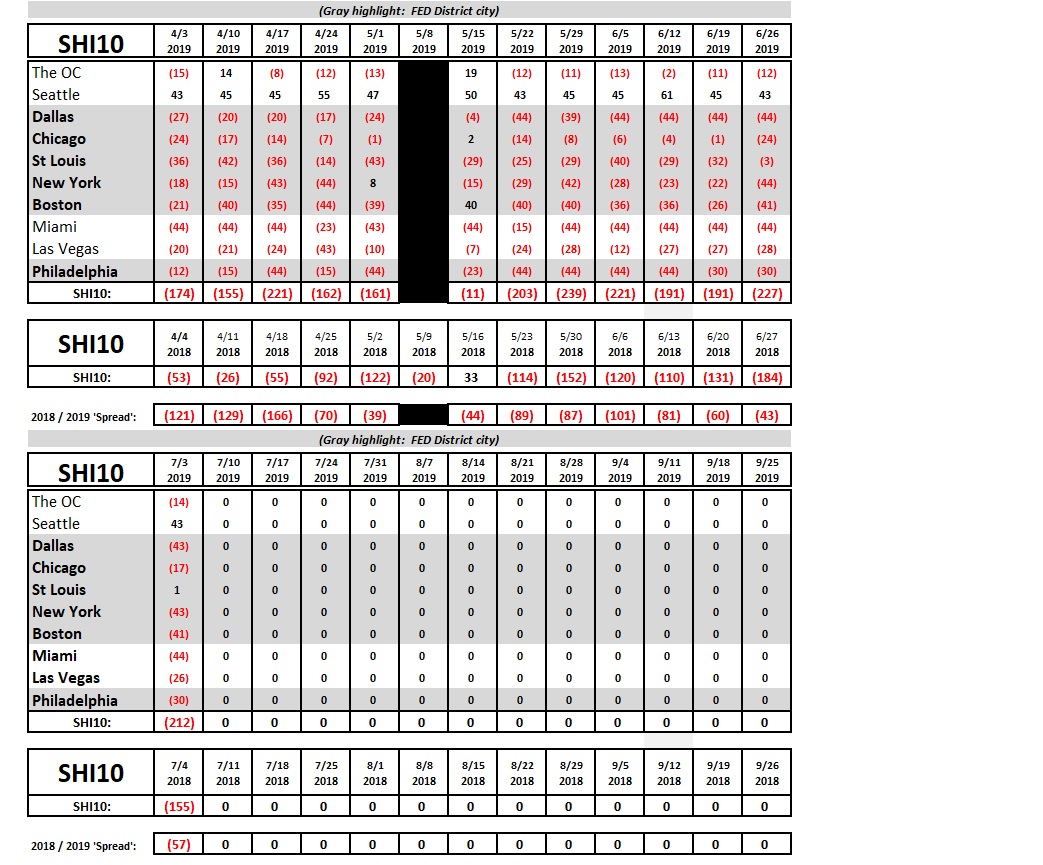

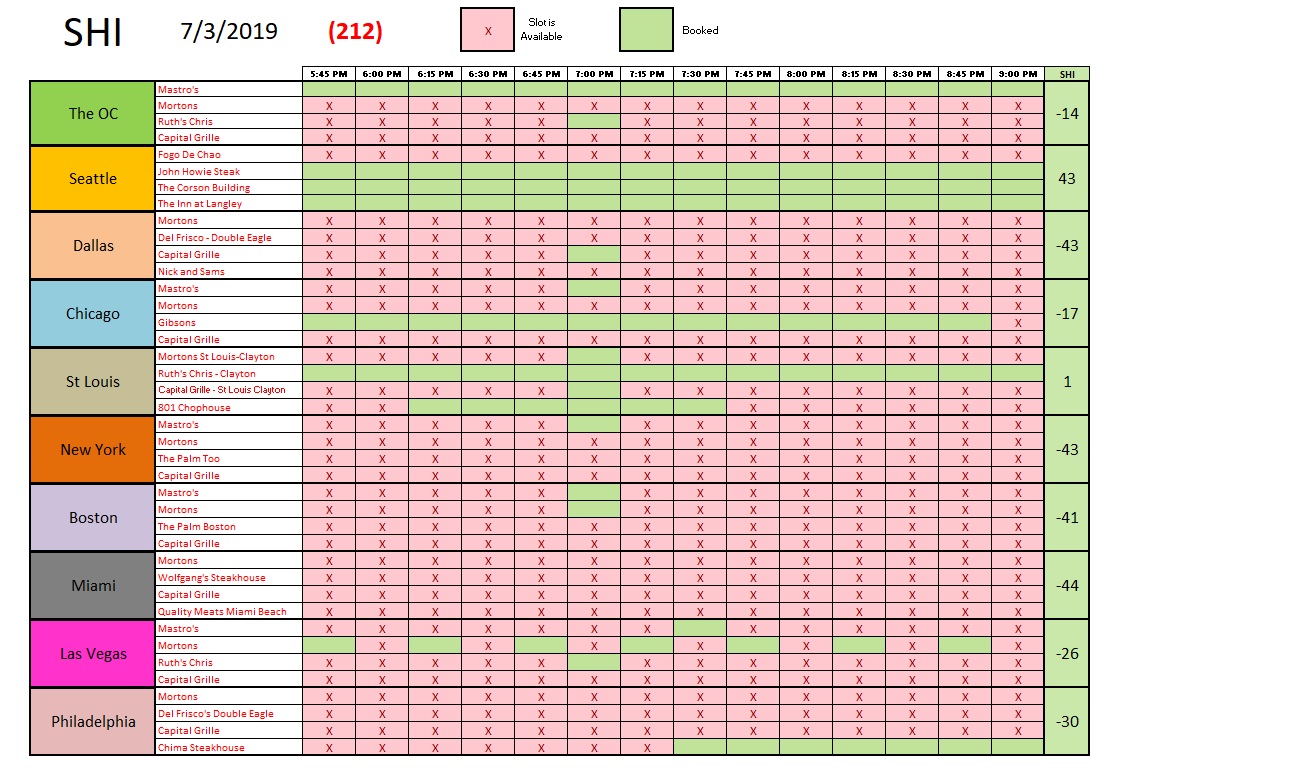

As you see below, this week looks like a repeat of the last. Not much change, frankly. There are plenty of open tables at all of our expensive eateries across the USA. The ‘spread’ between this week’s SHI10 and the reading from about a year ago is still sizable, indicating weaker steak demand this year than last:

As I’ve said before, the SHI10 is designed to be a future economic barometer. Consumers, in general, seem far more positive and optimistic than business leaders about the future. (I’m referencing the OECD chart above.) Yet, their their willingness to spend exorbitant amounts of their hard-earned cash for a slab of beef appears to be waning. Perhaps the behavior of our “well-heeled consumer” is more aligned with business than the general consumer? Clearly, our barometric reading seems to reflect the attitude of business leaders more than the ‘typical’ consumer, so this seems likely. Here are this weeks SHI numbers:

The BIS report reflects the same cautions and concerns we’ve noted. They’ve entitled the report, “NO CLEAR SKIES YET” for good reason. The BIS is concerned … and rightfully so. The US seems to be holding up better than most other areas … but even here there are no clear skies.

Hopefully you’ll have clear skies to watch the fireworks as we all celebrate the July 4th holiday. Happy birthday, America!

– Terry Liebman