SHI 7.24.19 – Facebook and the 5 Billion

SHI 7.10.19 – Superforecasting and Inflection Points

July 10, 2019

SHI 7.31.19 — The Last Mile

July 31, 2019

“Facebook has privacy issues? Whoa! I’m shocked!”

Not really. I’m not shocked.

The 5 billion is this case is not the number of Facebook’s monthly users. Monthly users of at least 1 or more Facebook ‘app’ total 2.5 billion today. That figure, too, is staggering. No, the $5 billion is a fine Facebook will pay to the FTC to settle ‘data-privacy practices’ issues. 2 bucks per user. Not bad! 🙂

Per the Wall Street Journal:

“The $5 billion penalty against Facebook is the largest ever imposed on any company for violating consumers’ privacy and almost 20 times greater than the largest privacy or data security penalty ever imposed worldwide,” the Federal Trade Commission said in a news release. “It is one of the largest penalties ever assessed by the U.S. government for any violation.”

Ouch. And, no, I’m not shocked. Nor am I a monthly Facebook user. In fact, I’ve never been a Facebook user. Because from day-one, I was concerned about data privacy. The thought of voluntarily “posting” very personal and private information into a public forum, for all to see, struck me as mentally unbalanced. Why would anyone do that, I thought? Yet 2.5 billion people disagreed with me and signed up. Me? I felt the whole concept was a bit Orwellian. Big Brother, in this case, isn’t the government. Big Brother is a harmless corporation. How could this possibly go wrong? 🙂

Years ago, I predicted using Facebook would end badly for individual Facebook users. To me, this was an easy prediction. On the other hand, predicting when the next US recession will begin is a bit more complex. Whether one uses steakhouse reservations, or the concept of Ray Dalio’s ‘Paradigm Shifts‘, predicting the start of the next recession is tricky.

Welcome to this week’s Steak House Index update.

If you are new to my blog, or you need a refresher on the SHI10, or its objective and methodology, I suggest you open and read the original BLOG: https://www.steakhouseindex.com/move-over-big-mac-index-here-comes-the-steak-house-index/

Why You Should Care: The US economy and US dollar are the bedrock of the world’s economy. This has been the case for decades … and will be true for years to come.

But is the US economy expanding or contracting?

According to the IMF (the ‘International Monetary Fund’), the world’s annual GDP is about $80 trillion today. US ‘current dollar’ GDP now exceeds $21 trillion. In Q1 of 2019, nominal GDP grew by 3.8%…following a 4.1% increase in Q4, 2018. We remain about 25% of global GDP. Other than China — a distant second at around $12 trillion — the GDP of no other country is close. We can’t forget about the EU — collectively their GDP almost equals the U.S. So, together, the U.S., the EU and China generate about 2/3 of the globe’s economic output. Worth watching, right?

The objective of the SHI10 and this blog is simple: To predict US GDP movement ahead of official economic releases — an important objective since BEA (the ‘Bureau of Economic Analysis’) gross domestic product data is outdated the day it’s released. Historically, ‘personal consumption expenditures,’ or PCE, has been the largest component of US GDP growth — typically about 2/3 of all GDP growth. In fact, the majority of all GDP increases (or declines) usually results from (increases or decreases in) consumer spending. Consumer spending is clearly a critical financial metric. In all likelihood, the most important financial metric. The Steak House Index focuses right here … on the “consumer spending” metric. I intend the SHI10 is to be predictive, anticipating where the economy is going – not where it’s been.

Taking action: Keep up with this weekly BLOG update. Not only will we cover the SHI and SHI10, but we’ll explore related items of economic importance.

If the SHI10 index moves appreciably -– either showing massive improvement or significant declines –- indicating growing economic strength or a potential recession, we’ll discuss possible actions at that time.

The BLOG:

Like Warren Buffet, Ray Dalio is one of the most successful investors of all times. And while I may not be listening to the 2.5 billion Facebook users, I do listen to both of those guys. To me, their opinions matter.

So I read a Dalio post, called ‘Paradigm Shifts‘, very carefully. It’s a worthwhile piece, and I’ve included a link to the article below. It is a very long piece, chock full of interesting data, and I suggest you read it. Toward the end, he forecasts the ‘coming paradigm shift’:

“I think that it is highly likely that sometime in the next few years, 1) central banks will run out of stimulant to boost the markets and the economy when the economy is weak, and 2) there will be an enormous amount of debt and non-debt liabilities (e.g., pension and healthcare) that will increasingly be coming due and won’t be able to be funded with assets.

Said differently, I think that the paradigm that we are in will most likely end when a) real interest rate returns are pushed so low that investors holding the debt won’t want to hold it and will start to move to something they think is better and b) simultaneously, the large need for money to fund liabilities will contribute to the “big squeeze.” At that point, there won’t be enough money to meet the needs for it, so there will have to be some combination of large deficits that are monetized, currency depreciations, and large tax increases, and these circumstances will likely increase the conflicts between the capitalist haves and the socialist have-nots. Most likely, during this time, holders of debt will receive very low or negative nominal and real returns in currencies that are weakening, which will de facto be a wealth tax.

Ouch. That doesn’t sound good. He continues:

That will happen at the same time that there will be greater internal conflicts (mostly between socialists and capitalists) about how to divide the pie and greater external conflicts (mostly between countries about how to divide both the global economic pie and global influence). In such a world, storing one’s money in cash and bonds will no longer be safe.

Bonds are a claim on money and governments are likely to continue printing money to pay their debts with devalued money. That’s the easiest and least controversial way to reduce the debt burdens and without raising taxes. My guess is that bonds will provide bad real and nominal returns for those who hold them, but not lead to significant price declines and higher interest rates because I think that it is most likely that central banks will buy more of them to hold interest rates down and keep prices up. In other words, I suspect that the new paradigm will be characterized by large debt monetizations that will be most similar to those that occurred in the 1940s war years.”

He finishes with this comment:

“Most people now believe the best “risky investments” will continue to be equity and equity-like investments, such as leveraged private equity, leveraged real estate, and venture capital, and this is especially true when central banks are reflating. As a result, the world is leveraged long, holding assets that have low real and nominal expected returns that are also providing historically low returns relative to cash returns (because of the enormous amount of money that has been pumped into the hands of investors by central banks and because of other economic forces that are making companies flush with cash).

I think these are unlikely to be good real returning investments and that those that will most likely do best will be those that do well when the value of money is being depreciated and domestic and international conflicts are significant, such as gold. For this reason, I believe that it would be both risk-reducing and return-enhancing to consider adding gold to one’s portfolio.“

Interesting. Gold. There you have it. And here’s Dalio’s post:

https://www.linkedin.com/pulse/paradigm-shifts-ray-dalio/

Dalio makes the case that ‘reflation‘ differs from ‘inflation.’

Imagine a basketball that, for some reason, lost half it’s air. Adding the missing air back into the ball would be reflating the ball. Pumping it up, so to speak. In this sense, Dalio seems to be suggesting reflation is an intermediate step in the middle of the inflation – deflation paradigm. Between inflation and deflation.

I’m not sure I’d characterize the series of central bank ‘quantitative easing’ actions over the past 10 years the same way. I believe the QE by central banks across the globe did their job: Quantitative easing did two things: First, it removed assets from the global financial system. Second, it injected cash into the system.

QE removed assets from the system when the central bank purchased sovereign debt (and other assorted high quality assets) and held them on their balance sheets. About $15 or $18 trillion worth. This amount represents about 25% of all such available assets. A staggering sum by any account.

By reducing the quantity of assets available for purchase, they prevented asset values from falling further, effectively ‘pumping air’ (in the form of cash), into the system. Globally coordinated central bank action prevented global deflation, added tens of trillions of dollars (and yen, yuan, pounds, euro, francs, etc.) into the global financial system, drove global interest rates to zero and negative, and increased asset values.

But make no mistake: Deficits — here and abroad — are being monetized right now. And have been for decades. Said another way, many developed economies around the world are spending more money than they bring in from taxes and other revenue. Germany is one of the few developed nations running a budget surplus today. Most developed nations run a budget deficit. This year, the US is expected to run about a $1 trillion deficit. Here’s a comment on France in an IMF report released earlier today:

“The fiscal deficit declined to 2.5 percent of GDP at end-2018, while public debt continued to remain elevated, at around 98 percent of GDP.”

France has an annual GDP of about $2.6 trillion.

If Dalio is right, at some time in the future, further and continued deficit monetization will cause inflation rates to skyrocket globally. In this scenario gold will produce exceptionally good returns. Is he right? Here’s the answer you always love to hear from me: Maybe. 🙂

Others have different ideas on the topic of deficit spending. One that I personally find quite entertaining is ‘Modern Monetary Theory’, also known as MMT. MMT suggests that if your currency is the world’s ‘reserve’ currency — as the US dollar is today — deficits don’t matter! No matter how large they are! Print as much of the stuff as you’d like, and spend away, because you can always print more dollars! Since the US dollar is the world’s reserve currency, every other country will always take it off our hands!

I’m not a big fan of MMT. Frankly, I’m frightened that intelligent people even consider this to be a viable theory. Here’s a good Bloomberg article if you want to read up on MMT:

https://www.bloomberg.com/news/features/2019-03-21/modern-monetary-theory-beginner-s-guide

But I do have theories of my own! In the near future, I’ll post a blog entitled “Staying Positive in a Negative World.” Be sure to check it out.

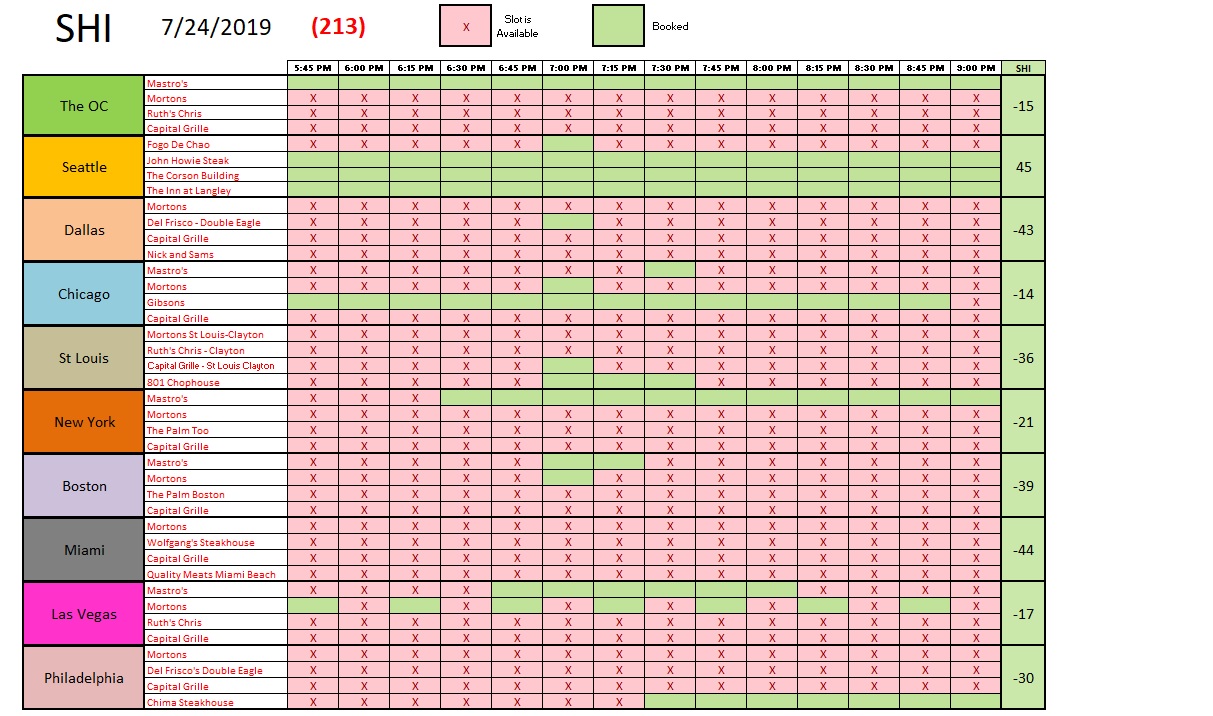

But now it’s time to head to the steakhouses. Here is this week’s chart:

Once again, demand is relatively weak for pricey steaks. Mastros continues to hold the #1 demand slot in all marketplaces, but most other expensive eateries are experiencing slow reservation demand for this coming Saturday.

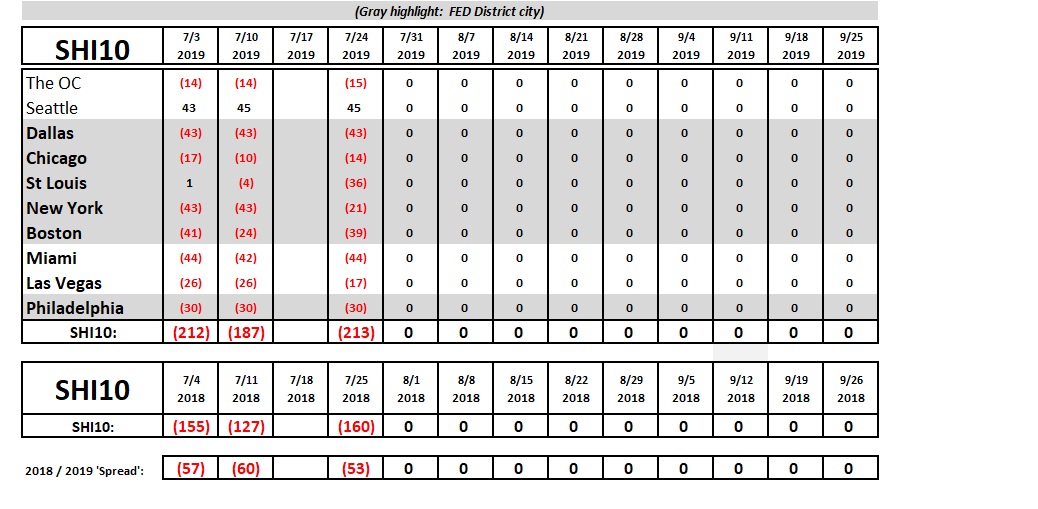

Here’s the long term trend chart. Once again, we see a high degree of consistency week over week, when compared to the results of about a year ago.

The FED meets again next week. Just about every economic forecaster is projecting a 25- or 50-basis point cut in the ‘federal funds rate.’ I think we’ll see a 25 basis point cut. Not because our economy needs a rate reduction at the moment, but because such an action is a bit preventative.

The wreaking ball currently crushing global supply chains has the FED and most other economists increasingly worried about a global recession. For good reason. Ben Franklin once said “an ounce of prevention is worth a pound of cure.” I think he really meant a pound of beef. No matter, I suspect the FED agrees with Ben right about now, and will act accordingly next week.

– Terry Liebman