SHI 7.31.19 — The Last Mile

SHI 7.24.19 – Facebook and the 5 Billion

July 24, 2019

SHI 8.6.19 — Staying Positive in a Negative World

August 7, 2019

“The ‘advance estimate of 2nd quarter 2019 GDP was 2.1%. This number was surprisingly good.”

I was not shocked by Facebook’s violation of customer privacy. I am mildly surprised by the first Q2, 2019 GDP growth reading. Pleasantly surprised, but surprised nonetheless. Once again, ‘current dollar GDP’ growth was strong — 4.6%, or $239.1 billion — for the quarter. US nominal GDP is now up to $21.34 trillion annually. Fabulous.

Personal Consumption Expenditures, or PCE, picked up a bit of steam … rising 2.4% (YOY) during the quarter, following an exceptionally weak 1.1% (annualized) increase in Q1. Looking a bit deeper, I find it fascinating to compare the behavior of ‘durable goods’ (stuff that lasts more than 1 year) and ‘non-durable goods.’ The price-index for durable goods has fallen in 15 of the last 16 quarters. That is de facto deflation, folks. At least where washing machines, furniture, tools and computers are concerned.

Right here — focusing directly on this concern — is where we start today’s blog. Read on, my friends. Read on.

Welcome to this week’s Steak House Index update.

If you are new to my blog, or you need a refresher on the SHI10, or its objective and methodology, I suggest you open and read the original BLOG: https://www.steakhouseindex.com/move-over-big-mac-index-here-comes-the-steak-house-index/

Why You Should Care: The US economy and US dollar are the bedrock of the world’s economy. This has been the case for decades … and will be true for years to come.

But is the US economy expanding or contracting?

According to the IMF (the ‘International Monetary Fund’), the world’s annual GDP is about $84 trillion today. US ‘current dollar’ GDP now exceeds $21.3 trillion. In Q2 of 2019, nominal GDP grew by 4.6%. The US still produces about 25% of global GDP. Other than China — in a distant ‘second place’ at around $13 trillion — the GDP of no other country is close. The GDP output of the 28 countries of the European Union collectively approximates US GDP. So, together, the U.S., the EU and China generate about 70% of the global economic output. This is worth watching carefully, right?

The objective of the SHI10 and this blog is simple: To predict US GDP movement ahead of official economic releases — an important objective since BEA (the ‘Bureau of Economic Analysis’) gross domestic product data is outdated the day it’s released. Historically, ‘personal consumption expenditures,’ or PCE, has been the largest component of US GDP growth — typically about 2/3 of all GDP growth. In fact, the majority of all GDP increases (or declines) usually results from (increases or decreases in) consumer spending. Consumer spending is clearly a critical financial metric. In all likelihood, the most important financial metric. The Steak House Index focuses right here … on the “consumer spending” metric. I intend the SHI10 is to be predictive, anticipating where the economy is going – not where it’s been.

Taking action: Keep up with this weekly BLOG update. Not only will we cover the SHI and SHI10, but we’ll explore related items of economic importance.

If the SHI10 index moves appreciably -– either showing massive improvement or significant declines –- indicating growing economic strength or a potential recession, we’ll discuss possible actions at that time.

The BLOG:

Even as global supply-chains fall victim to the latest tariff threats, trade disruption, and political vitriol, the battle for the fastest consumer product delivery platform rages on.

In April, Amazon announced it intends to spend $800 million to upgrade is supply-chain, beginning this July, to bring its “free” current 2-day delivery down to just 1-day. Not to be beat, Alibaba — China’s answer to Amazon — is spending even more. Cainiao – Alibaba’s logistics platform – is investing 100 billion yuan ($14.5 billion) for upgrades it believes will guarantee next-day delivery in China and 3-day delivery worldwide.

Walmart, too, is in the game. “A competitor who will remain nameless…is forcing all of us to think differently, and we should,” commented a Walmart exec. Nameless? I think I can guess who he’s talking about. Using robotics, digitization, automated ‘storage and retrieval’ systems, and a new system of ‘continuous replenishment’, they too plan to increase speed-to-customer. Walmart plans to ‘crowdsource’ the last-mile of order delivery. And on June 7th, Walmart unveiled a new service that allows customers who order groceries online to have them delivered directly into their fridge. Cool! Order beer on-line, and it shows in in the ‘fridge! This might be time to sell your stock in 7-Eleven.

Clearly, we live in a very different world than just a decade ago. But if you’re not yet convinced, consider this headline from the Independent, a UK newspaper:

“Chinese police to use facial recognition technology to send jaywalkers instant fines by text”

Yep. In Shenzhen, China, a jaywalker’s face — and name — instantly appears on a giant screen, for all to see, intending to shame the scoff-law. And then BONG! A fine quickly appears by text on their cell phone. Ouch. From that same article: “Shenzhen began using AI-enabled cameras in April last year and had within 10 months had displayed the 13,939 jaywalking offenders in one LED scree at a busy junction in Futian district, according to police.” Imagine the benefit of importing this technology to Chicago. In less than a year, I surmise, the jaywalking fines alone could balance Chicago’s annual budget! 🙂

“This Time is Different” is the title of a phenomenal book written by Carmen Reinhard and Kenneth Rogoff. Frankly, it has nothing to do with supply chains. The book is a deep and comprehensive look at 8 astonishing centuries of government defaults, banking panics, and inflationary spikes, including the “Great Recession of 2008.” Only the book’s title is a joke – poking fun at those who believe we’ve learned lessons from the past. The conclusion of the book, frankly, is that the 2008 financial crisis was no different than those that preceded it. Poor, even stupid, choices have triggered every financial crisis in history. Rogoff and Reinhard assure us this has not changed. Financial markets remain the same. Nothing, really, is different.

But Amazon, Alibaba, and Walmart want us to know this time is different for the consumer. It’s a new world. And the changes are showing up in various economic and financial metrics. Just like consumer marketplaces, age-old economic theories, too, have been disrupted in the past decade. For example, the Philips Curve is on life support. According to FED Chairman Powell, when questioned in recent congressional testimony a few weeks ago, there is at most “a faint heartbeat” of inflationary pressure from tight labor markets.

Inflation forecasting has been disrupted. Triggering, or curtailing, inflation use to be relatively easy. Not today. In Japan, the EU and here in the US, increasing the inflation rate has proven elusive.

Please note I’m making a distinction here between inflation and hyper-inflation. Triggering hyperinflation is still a no-brainer. Venezuela did it. So did Zimbabwe. It’s really pretty easy to do. But lifting the inflation rate from, say, zero to the FEDs target of 2% is clearly much more difficult. Even worse, it may no longer be possible.

Inflation has never been homogeneous, in spite of how it’s reported as a single number — a ‘CPI‘ or ‘PCE.’ In fact, it can be parsed into a number of integral parts, and viewed thru very different lenses. Two NBER economists, James Stock and Mark Watson, just released a paper on this topic, entitled “Slack and Cyclically Sensitive Inflation” further demonstrating precisely this fact. In the paper’s summary, they comment:

“We investigate the flattening Phillips relation by making two departures from standard specifications. We study the components of inflation instead of the standard aggregates. We find that some inflation components have strong and stable correlations with the cyclical component of real activity; these components tend to be relatively well-measured and domestically determined. Other components, typically prices that are poorly measured or internationally determined, have weak and/or unstable correlations with cyclical activity.”

Above, they use the words ‘strong’ and ‘weak’ to describe the correlation different products have to the economy’s expansion or contraction. When the GDP is growing, and folks have more money in their bank accounts and pockets, a strong correlation suggests prices — in other words, inflation — should increase. But many of the components did not. Some prices rose slightly, dipped slightly or stayed the same. This outcome was unexpected.

The FED Bank of San Francisco (FRBSF) agrees, having published numerous papers on the same topic. FRBSF suggests there are ‘cyclical’ inflation factors – those that behave as we would expect during robust economic conditions – and others that appear to be ‘acyclical,’ behaving in a non-inflationary manner, or even deflationary, at a time when economic theory suggests their prices should be rising significantly. A recent article in the Wall Street Journal summarized current FRBSF findings: “The cyclically sensitive components of core inflation, which excludes food and energy, have accelerated to 2.33% in the 12 months through May from 0.41% in mid-2010, according to the San Francisco Fed, just as falling unemployment would predict. But that has been offset by falling inflation in acyclical categories—such as health care, financial services and most goods—which has slowed to 1.04% from 2.26% in the same period.”

In fact, according to the FRBSF, 58% of the FEDs favorite inflation gauge, the ‘personal consumption expenditure’ index, or PCE index, fall into the acyclical group. Let me repeat that: 58% of the PCE index components are behaving acyclically. It appears this time is different: global trade, robotics, and disruptive technologies are keeping a lid on inflation – even driving down prices.

Kristen Forbes, an economist working with the Bank for International Settlements, known as the BIS, recently published a paper entitled, “Has globalization changed the inflation process?” Ms. Forbes’ conclusion:

“The relationship central to most inflation models, between slack and inflation, seems to have weakened. Do we need a new framework? This paper uses three very different approaches – principal components, a Phillips curve model, and trend-cycle decomposition – to show that inflation models should more explicitly and comprehensively control for changes in the global economy and allow for key parameters to adjust over time. Global factors, such as global commodity prices, global slack, exchange rates, and producer price competition can all significantly affect inflation, even after controlling for the standard domestic variables. The role of these global factors has changed over the last decade, especially the relationship between global slack, commodity prices, and producer price dispersion with CPI inflation and the cyclical component of inflation. The role of different global and domestic factors varies across countries, but as the world has become more integrated through trade and supply chains, global factors should no longer play an ancillary role in models of inflation dynamics.”

Notice she used the word ‘ancillary?’ Another word for ancillary is subordinate. Ms. Forbes feels trade and supply chains are no longer subordinate to the other inflationary forces. It’s time, she clearly believes, for them to step out of the shadows and take a prominent role in inflation forecasting.

So, if this time is different, what does this mean to us … and the FED? Even as the US economy continues to grow in this longest-ever expansion, the FED is worried about the trajectory of the recovery vis-à-vis the global trade dispute and supply-chain disruptions. But they should be even more worried about what those supply chains have done to inflation.

David Dollar with the Brookings Institution, uses a different word: Transformation. He believes the landscape has been transformed. His comment:

“Walk into a Toyota dealership in New York or Munich, and you might think you are looking at cars made in Japan. You would be mistaken. In fact, the 15,000 components that make up a modern car are often produced by different firms in different locations. There are three main hubs for auto production—North America, Europe, and east Asia. Research and development and design mostly take place in Germany, Japan, and the United States, with China starting to play a significant role as well, given the 5 million STEM (science, technology, engineering, and mathematics) graduates it trains each year. Each of these hubs combines production in high-wage economies with parts and components from lower-wage, emerging market economies. Parts and components crisscross multiple borders during the production process.

From smartphones and autos to TVs and computers, more than two-thirds of international trade now takes place within such global value chains. That’s up from 60 percent in 2001. The rise of value chains has reshaped the world economy, fueling dramatic advances in living standards in emerging-market economies like China and Vietnam, where labor costs are relatively low, while widening income inequality in advanced economies, including the United States. Yet decades-old methods of gathering trade data, developed in the pre-value-chain world, fail to reflect this transformation, giving rise to a skewed picture of the movement of goods and services around the world. The result: acrimonious debates over job losses blamed on trade are rooted in inadequate data, amplifying misguided calls for protectionism.”

His article is worth a quick read. Check it out: https://www.imf.org/external/pubs/ft/fandd/2019/06/global-value-chains-transforming-manufacturing-dollar.htm?utm_medium=email&utm_source=govdelivery

After several years of hand-wringing, the FED has finally admitted the relationship between full employment and wages — described by the Phillips Curve — no longer seems to work. That relationship, too, appears weakly correlated at best. And now it appears other components are not behaving as they have in past decades. The economic forecasting tools of the past seem less effective today. Why?

In 1935, John Maynard Keynes completed his opus, “The General Theory of Employment, Interest and Money.” Since that time, almost 85 years ago, most economists and central bankers have used the foundational principals of ‘Keynesian Economics’ to guide theory and decisions. And for decades Keynesian principles helped guide us. But do they still today? Do Keynesian principles still accurately predict market response to changes in economic conditions?

No, I don’t believe they do. At least not to the extent they once did. I think the wisdom of Dr. Keynes, too, has been disrupted. Remember: In 1935, the English Pound was the worlds reserve currency, the ‘gold standard’ was the backbone of currency value, and the economy of each country was very independent of others. Sure, some international trade existed, but compared to today’s system, international trade in the 1930 was infinitesimal by comparison to today. Nor did many international supply-chains exist. Goods were typically created in one country and then exported to another. Products like tea. And tobacco.

Back then, inflation behaved much like Keynes described it in his “Quantity Theory of Money:”

“It follows that an increase in the quantity of money will have no effect whatever on prices, so long as there is any unemployment, and that employment will increase in exact proportion to any increase in effective demand brought about by the increase in the quantity of money; whilst as soon as full employment is reached, it will thenceforward be the wage-unit and prices which will increase in exact proportion to the increase in effective demand. Thus if there is perfectly elastic supply so long as there is unemployment, and perfectly inelastic supply so soon as full employment is reached, and if effective demand changes in the same proportion as the quantity of money, the Quantity Theory of Money can be enunciated as follows: “So long as there is unemployment, employment will change in the same proportion as the quantity of money; and when there is full employment, prices will change in the same proportion as the quantity of money”.

For decades this principle seemed sound. And accurate. And it worked as a forecasting tool. Inflation was highly correlated with employment and money supply. Year after year. But these correlations began to break down in the past decade or two, as economies, supply-chains and manufacturing went global. Clearly, conditions today are vastly different than they were during Keynes’ time. The disruption is global.

It’s also worth reviewing Keynes’ comments on interest rates from almost 85 years ago:

“There is evidence that for a period of almost one hundred and fifty years the long-run typical rate of interest in the leading financial centres was about 5 per cent, and the gilt-edged rate (about) 3 per cent; and that these rates of interest were modest enough to encourage a rate of investment consistent with an average of employment which was not intolerably low.”

‘Gilt-edged’ is a term to describe the high-quality securities issued by the UK. So, per Keynes, the sovereign rate in the UK, from around 1785 to 1935 was about 3 or 3 and a half percent. And while this rate is higher than levels today, it is significantly lower than levels of the past 3 decades. I find it interesting that while discussing levels of interest rates, Keynes talks about the theories of Silvio Gesell, a ‘socalist,’ anarchist, and theoretical economist, who wanted to “free the economy” from rent and interest payment. Gesell believed interest is paid to those with capital just as rent is paid to those with land. So, essentially, interest is simply another form of rent. And, by extension, Gesell believed that the growth of capital is severely restricted by the interest rate that capital demands. Gesell suggested that a zero-interest rate in the “modern world” would change the paradigm:

“(Gesell) argues that the growth of real capital is held back by the money-rate of interest, and that if this brake were removed the growth of real capital would be, in the modern world, so rapid that a zero money-rate of interest would probably be justified, not indeed forthwith, but within a comparatively short period of time. Thus the prime necessity is to reduce the money-rate of interest, and this, he pointed out, can be effected by causing money to incur carrying-costs just like other stocks of barren goods.”

Said another way, if all people could borrow money without the obligation to pay an interest charge, Gesell believes that “real capital growth” would grow rapidly. Interestingly enough, in some ways, that’s precisely what happened in the past decade. Not because Gesell and his socialist brethren were able to throw off the yoke of capitalism and declare interest rates to be zero. No, because the capitalists did if for them.

Globally, interest rates have slid to historic lows, closely resembling Gesell’s “vision” of zero rates. And, indeed, capital formation has followed at a blitzkrieg rate:

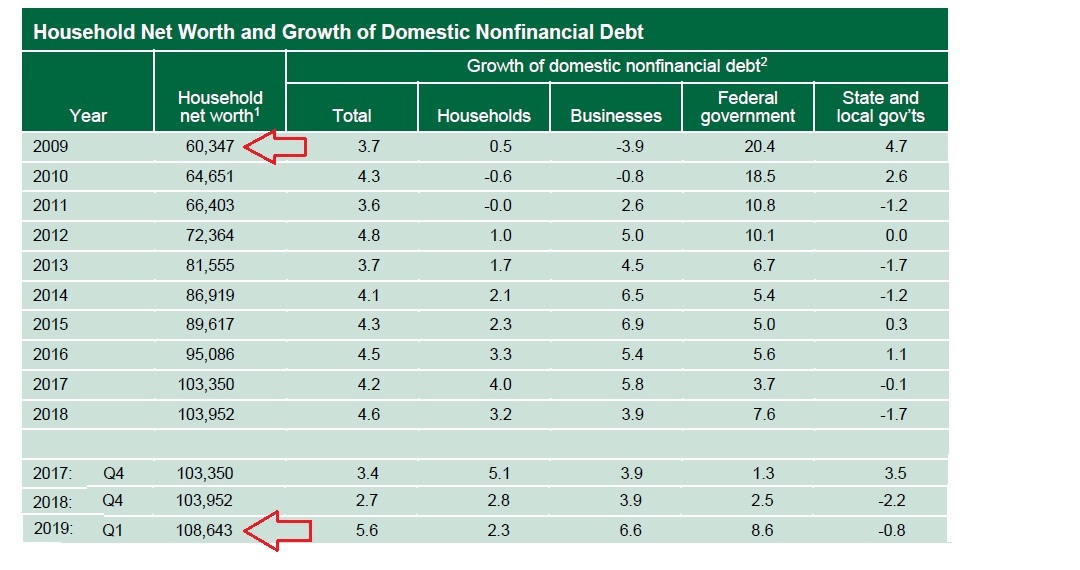

The ‘net worth’ (capital) of US households has never been higher.

Here’s a chart from the most recent FED Z.1 “Financial Accounts of the United States” report:

Note the two red arrows I’ve added. In 2009, as the Great Recession ended, US household net worth was about $60 trillion. At the beginning of 2019 — almost 10 years later — household net had almost doubled. This change is not confined to the US. In the 28 countries of the European Union, in the 4 years prior to Q4, 2018, household net worth increased by 22.6%, according to Eurostat.

Are the capital increases the result of the almost zero interest rates around the globe? Clearly, we see the correlation. But do we have causation? This question, I’m afraid, will take longer to answer. But there are things we know — with certainty — today:

-

The inflation rate in all developed nations is stubbornly low. And efforts to change this fact have proven unsuccessful to date.

-

Global wealth, or capital, has increased at a staggering rate. According to the 2018 ‘Global Wealth Report’ by Credit Suisse, global wealth has reached $317 trillion.

From the Credit Suisse report:

The ninth edition of the Global Wealth Report published by the Credit Suisse Research Institute provides the most comprehensive and up-to-date source of information available on global household wealth. During the twelve months to mid-2018, aggregate global wealth rose by $14.0 trillion (4.6%) to a combined total of $317 trillion, outpacing population growth. Wealth per adult grew by 3.2%, raising global mean wealth to a record high of $63,100 per adult. The US contributed most to global wealth adding $6.3 trillion and taking its total to $98 trillion. This continues its unbroken run of growth in both total wealth and wealth per adult every year since 2008. Unsurprisingly, China is now clearly established in second place of the world wealth hierarchy. The country overtook Japan with respect to the number of ultra-high net worth (UHNW) individuals in 2009, total wealth in 2011 and the number of millionaires in 2014.

Interested in reading more: https://www.credit-suisse.com/about-us/en/reports-research/global-wealth-report.html

Regardless of the accuracy of this number, the size of today’s number is much larger than about a decade ago: Credit Suisse reported the number was $200 trillion back in 2010.

Clearly, the FED should be concerned. Whether ‘disruption’ or ‘transformation,’ today’s global economy is very different. So if inflation is no longer 100% correlated with a country’s money supply and employment levels, what’s a central bank to do? Great question. Because on one hand, the US economy is chugging along nicely, people have jobs, and expensive sizzling steaks are selling pretty well. On the other hand, inflation seems stuck in the mud. And worse, our trading partners around the world seem worse off, or already immersed in a deflationary cycle (Japan.)

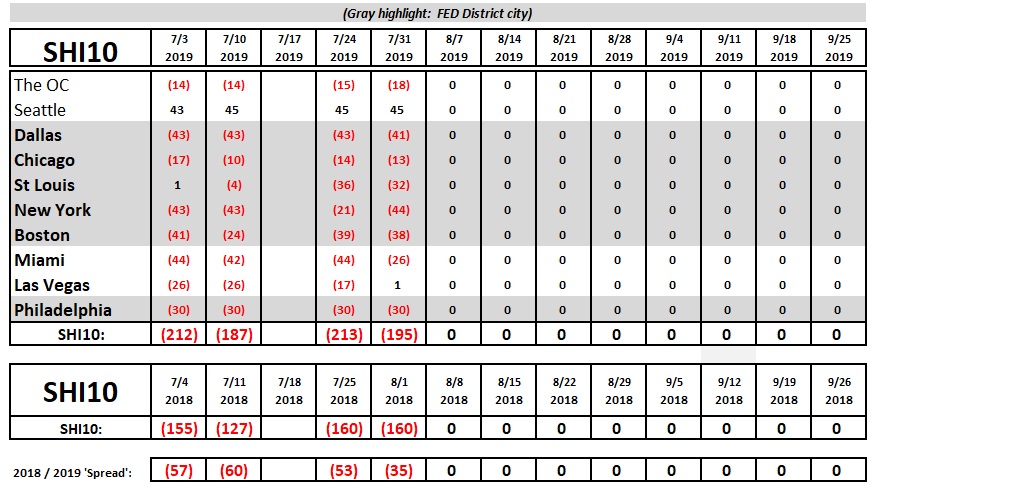

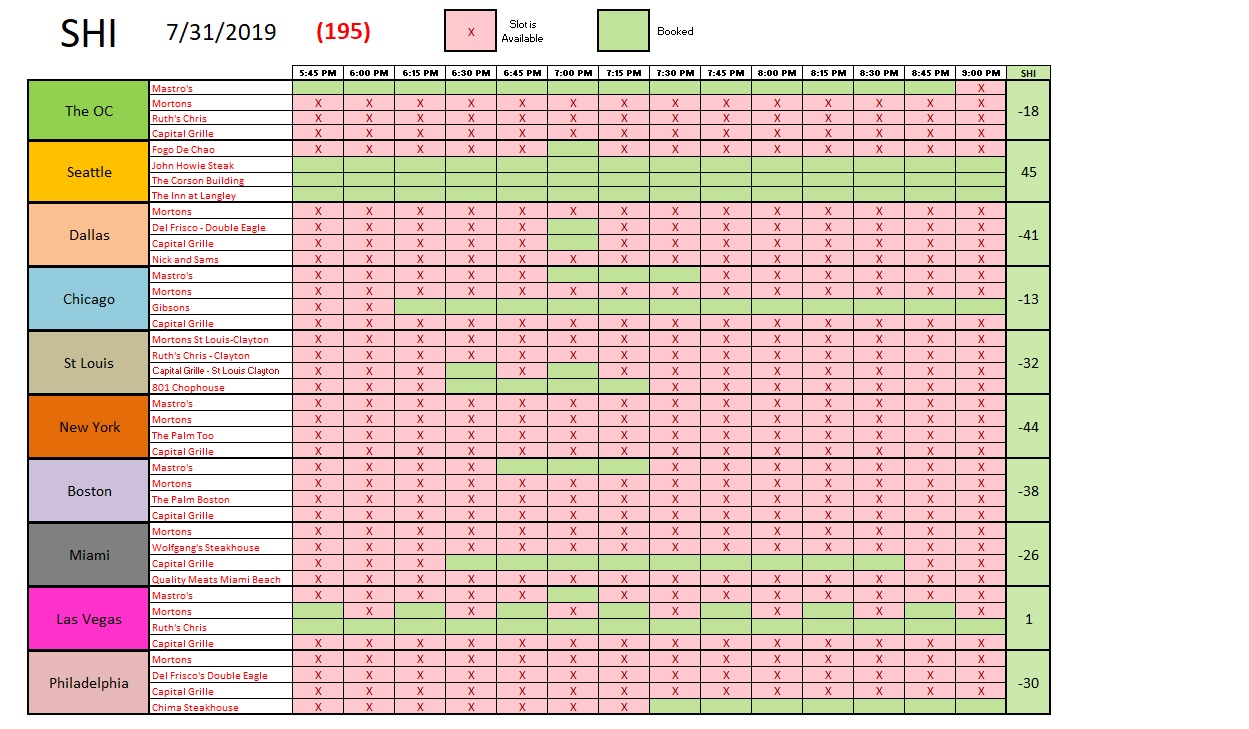

Speaking of sizzling steaks, let’s check in with OpenTable and see how hot pricey steakhouse reservations are this weekend across the US.

Not bad. This week the ‘spread’ between 2018 and 2019 has thinned. The SHI10 reading itself is more lukewarm than hot. Las Vegas made it into the ‘black’ this week:

In general, most restaurants had similar table availability as last week. In fact, not much has changed for our expensive eateries for the past several weeks. Reservation demand has been fairly consistent, remaining on the weaker side of the ledger. Here are this weeks results:

OK…let’s get back to current events. The FED has spoken: They cut rates by 0.25%. For the first time since the ‘Great Recession,’ the FED has reduced the funds rate.

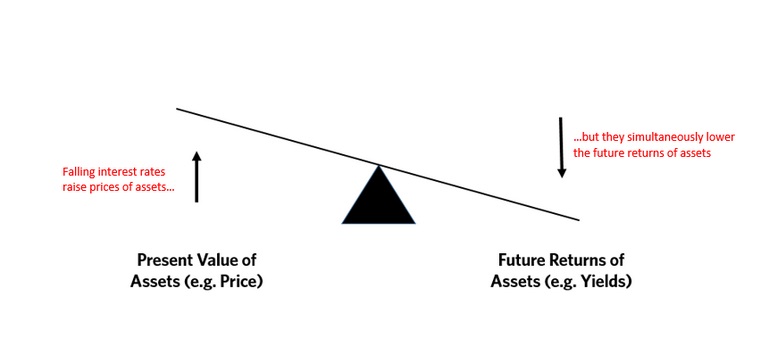

Fascinating. Today, the FED picked their battle. By this move, they are saying below-trend inflation is MORE important — a more significant issue — than the significant growth in asset values/capital. Make no mistake, as interest rates fall, asset values tend to rise. In his ‘Paradigm Shift’ piece, Ray Dalio had a great graphic that summarizes this relationship:

However, this relationship probably only holds if deflation does not become entrenched. If and when deflation is believed to be entrenched and continuous, all bets are off. Asset values — across the board — will begin to lose value. Why?

The answer is simple and foundational: The value of an asset is some function of its future income stream. If the value of that income stream is falling, the value of the asset will fall.

I’ll leave this debate here for now. But here’s your take away for today:

The FED is worried about persistently low inflation. Very worried. And they should be.

Thanks for tuning in.

– Terry Liebman

2 Comments

Hi Terry,

Love the blog and insightful posts- not gonna lie, they’re quite long and I don’t understand it all.

That said, from what I can tell, it appears you’re in favor of a more nationalistic society- economically speaking, especially considering the focus on GDP, which is by definition non-globalistic. So do you think there are benefits to just some people for this model and downsides to others? Or do you think this represents an equal opportunity model based on merit and integrity alone?

Then again, am I way off here because I couldn’t understand the full blog?

Cheers and thanks for the thought-provoking post!

Best,

Scott

5 Bridington

Really interesting and educational. Thanks for continuing to put this out!