SHI 8.14.19 – What? Me Worry?

SHI 8.6.19 — Staying Positive in a Negative World

August 7, 2019

SHI 8.21.19 — Irrational Anxiety?

August 21, 2019

“Recession fears are growing. You worried yet?”

With a tip of my hat to MAD Magazine, which recently closed after publishing for 67 years, I ask if you’ve joined the worriers? You have good cause to worry. And you have plenty of company. Today, many investors are right there with you … shoulder to shoulder. Ostensibly worried about a recession, the stock market tanked again today. Why? Let’s see if your fears are justified.

Welcome to this week’s Steak House Index update.

If you are new to my blog, or you need a refresher on the SHI10, or its objective and methodology, I suggest you open and read the original BLOG: https://www.steakhouseindex.com/move-over-big-mac-index-here-comes-the-steak-house-index/

Why You Should Care: The US economy and US dollar are the bedrock of the world’s economy. This has been the case for decades … and will be true for years to come.

But is the US economy expanding or contracting?

According to the IMF (the ‘International Monetary Fund’), the world’s annual GDP is about $84 trillion today. US ‘current dollar’ GDP now exceeds $21.3 trillion. In Q2 of 2019, nominal GDP grew by 4.6%. The US still produces about 25% of global GDP. Other than China — in a distant ‘second place’ at around $13 trillion — the GDP of no other country is close. The GDP output of the 28 countries of the European Union collectively approximates US GDP. So, together, the U.S., the EU and China generate about 70% of the global economic output. This is worth watching carefully, right?

The objective of the SHI10 and this blog is simple: To predict US GDP movement ahead of official economic releases — an important objective since BEA (the ‘Bureau of Economic Analysis’) gross domestic product data is outdated the day it’s released. Historically, ‘personal consumption expenditures,’ or PCE, has been the largest component of US GDP growth — typically about 2/3 of all GDP growth. In fact, the majority of all GDP increases (or declines) usually results from (increases or decreases in) consumer spending. Consumer spending is clearly a critical financial metric. In all likelihood, the most important financial metric. The Steak House Index focuses right here … on the “consumer spending” metric. I intend the SHI10 is to be predictive, anticipating where the economy is going – not where it’s been.

Taking action: Keep up with this weekly BLOG update. Not only will we cover the SHI and SHI10, but we’ll explore related items of economic importance.

If the SHI10 index moves appreciably -– either showing massive improvement or significant declines –- indicating growing economic strength or a potential recession, we’ll discuss possible actions at that time.

The BLOG:

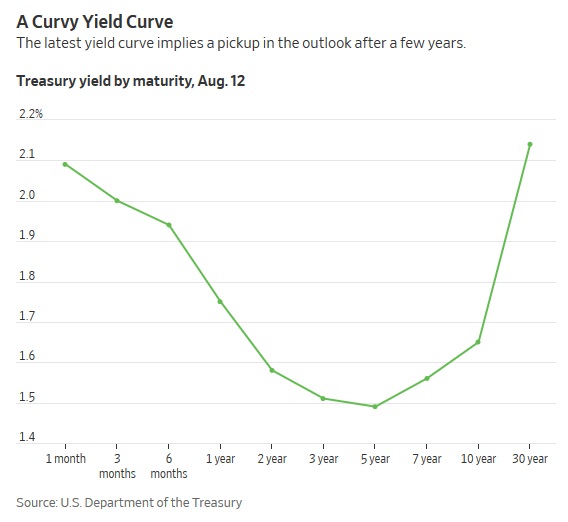

The yield curve is inverted again. Kinda. Well, it’s more of a giant “U” than inverted:

My thanks to the Wall Street Journal for the nice graphic.

There is no doubt: Shorter maturities are a lot higher in yield than longer maturities. Bond investors are telling us they feel confident that within 3 or 5 years, short-term rates will be a lot lower. Which is why they are willing to ‘lock up’ their money for 3-, 5-, or even 10-years at these historically very low interest rates. Low short-term rates suggest several things: (1) the FED will have lowered the funds rate, possibly down to near-zero once again, and (2) demand for short-term loans will be low, from both consumers (credit cards) and business, suggesting the US would be in recession. This is what bond traders are predicting.

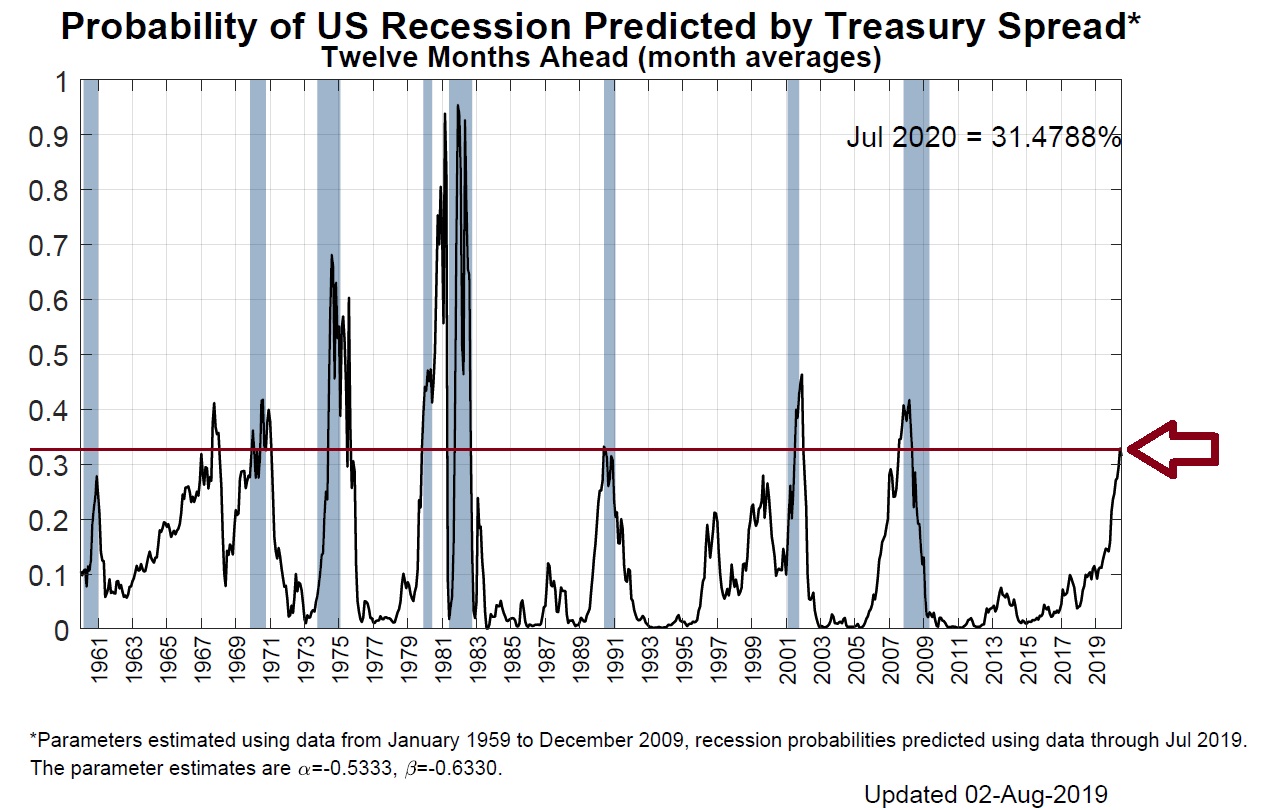

The NY FED produces a lot of research on the topic of “predicting recessions.” Here’s a good link to some of their research, if you want to take a look: https://www.newyorkfed.org/search?text=recession+probability+indicator&application=ny_pub&sources=ny_pub If not, take a look at this. Here’s one of their charts — right on point:

I’ve added the red line and the arrow. So, the NY FED, too, is a bit more worried about a recession than they were at the beginning of 2019. Back then, they felt about a 10% chance of recession was in the cards. Today, that number is closer to 33%.

When did this indicator hit — or exceed — 33% in the past? Follow the red line: In every instance where the indicated value exceeded 33%, going back to 1970, the the US was either in, or shortly thereafter in, a recession. It’s worth noting there was one ‘false positive’ back in 1967. So, the question remains:

Should you be worried a recession is around the corner? In a word: Yes. Caution is warranted. But ‘when‘ remains the better question. And, remember, this is not a simple, binary issue. Meaning that a slowing economy doesn’t necessarily suggest our economic expansion is at an end. It may simply be signaling slower growth ahead … but not a contraction.

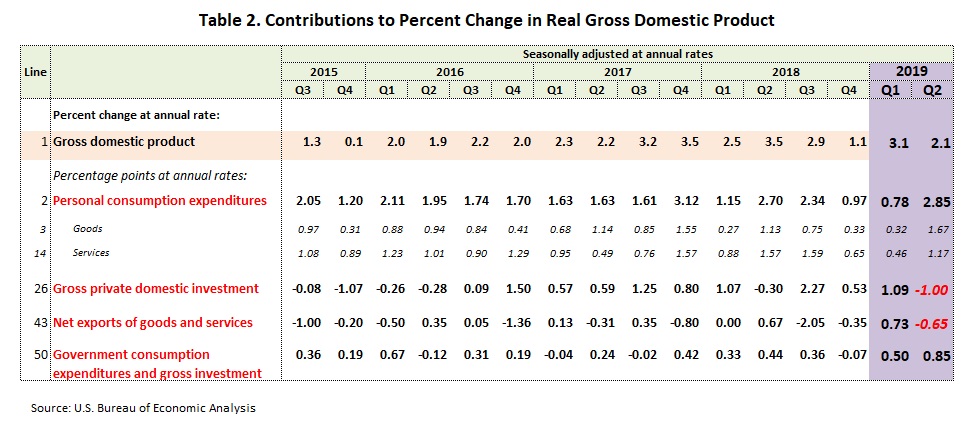

Interestingly enough, while investors seem quite worried about an imminent recession, the consumer does not. They’re spending money like drunken sailors. And it’s a good thing they are: Without the consumer “lighting cigars on fire with $100 bills”, spending money like crazy, the Q2, 2019 GDP growth number would have been quite a bit lower than the reported 2.1%.

Let me explain. Take a look at this chart I’ve compiled from GDP data provided by the US Bureau of Economic Analysis:

Remember, GDP growth comes from the four (4) distinct channels highlighted in red above. Two of those 4 channels were negative last quarter. Uh oh. And consumer consumption — known as the ‘Personal consumption expenditures — equaled 135% of the quarter’s GDP figure, not it’s typical 70%. In fact, if it wasn’t for excessive consumer spending, GDP would have been close to flat in the second quarter.

GDP components ‘investment’ and ‘trade’ are problematic. Lower investment reflects business leader’s fear of an unpredictable future. And, well, we all know what’s happening with trade.

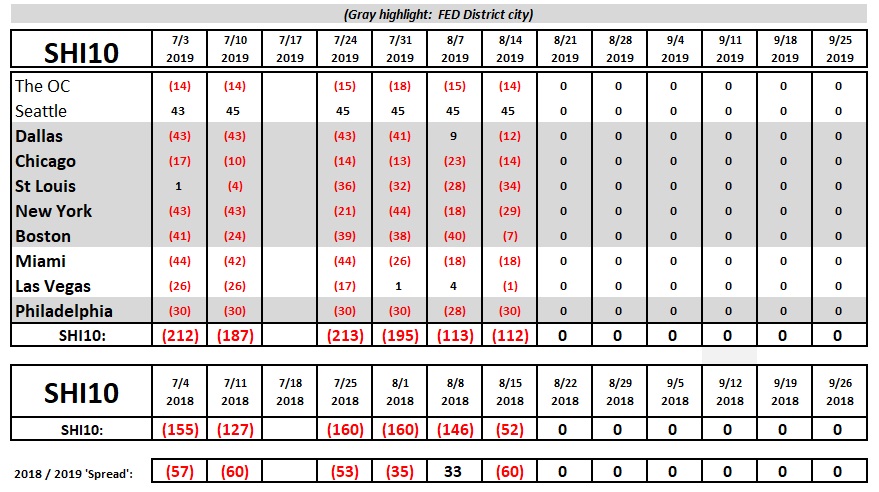

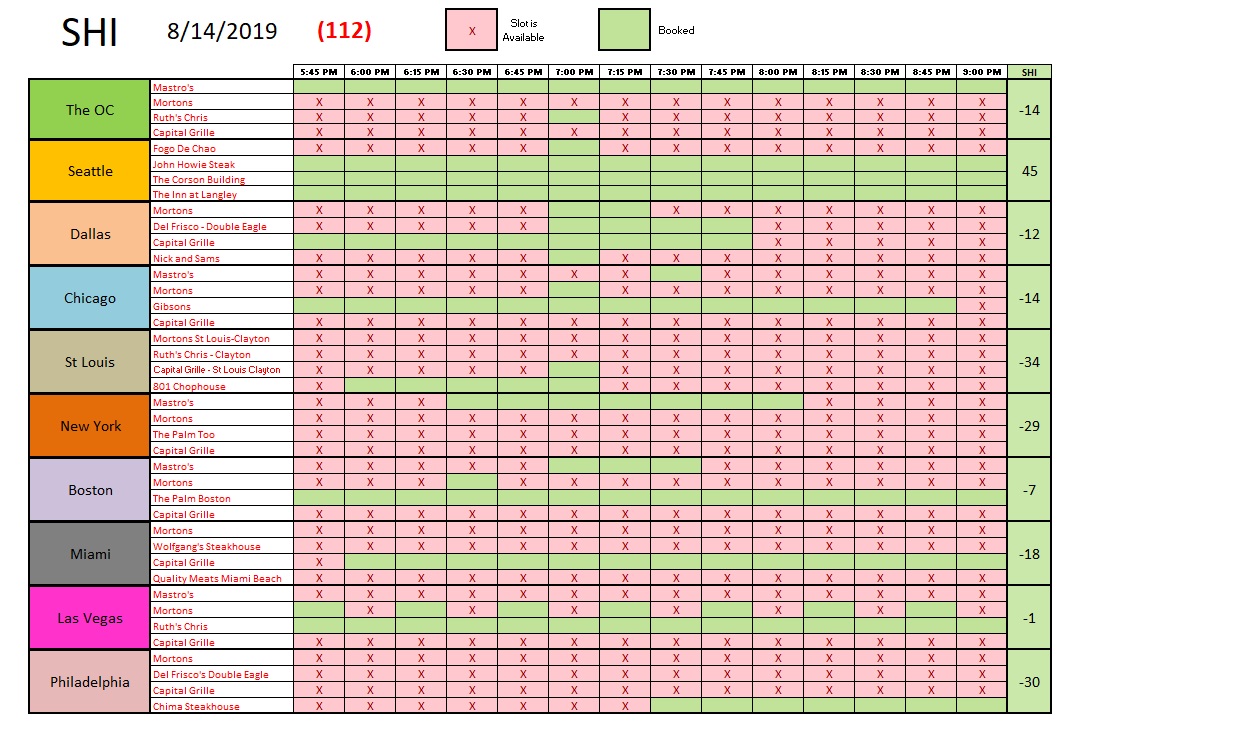

Enough said. Let’s grab a steak. Here is the trend report for today:

It looks like last week may have been an aberration. This week’s SHI10 reading is more consistent with prior weeks — and the 2018/2019 spread, too, is consistent with prior weeks. It’s worth noting that while the consumer may be lighting $100 bills on fire elsewhere, few seem to be doing that at our pricey steakhouses. Once again, with the exception of the Seattle market, you can find an open table this Saturday at almost every expensive eatery we track. Take a look:

Summarizing, consumer demand for reservations at the most expensive of restaurants continues, but not at levels I’d associate with strong economic growth. At best, recent SHI trends suggest lukewarm GDP growth in the future.

I’ll finish today’s blog with this comment: Recessions tend to ruin the incumbent president’s chances of re-election. Consider these historical facts, courtesy of the Washington Post:

- Since the Civil War, only one president has won reelection with a recession occurring in the final two calendar years of his first term: William McKinley in 1900.

- Since then, all four presidents running for reelection who had such a recession lost: William Taft, Herbert Hoover, Jimmy Carter and George H.W. Bush.

- Over the same span, all 10 who have sought reelection without such a recession have won: Woodrow Wilson, Franklin D. Roosevelt (3x), Dwight D. Eisenhower, Richard M. Nixon, Ronald Reagan, Bill Clinton, George W. Bush and Barack Obama.

- When you include all presidential elections (and not just presidents seeking reelection), the party in power has lost 13 of the last 19 races in which there was such a recession.

- Of the last 21 races without such a recession, the president’s party has won 16 of them.

I’m sure these facts are not lost on President Trump. So … ask yourself this question: With only about 15 months before the 2020 elections, will the president “stay the course” with China, potentially tilting the US into a recession, knowing this may end of his re-election chance? Or will he shortly change course, announce a “win” in the trade negotiations, and jump-start the economy once again? Or, might he be too late? Is the die already cast?

Hmmm……….

– Terry Liebman