SHI 8.21.19 — Irrational Anxiety?

SHI 8.14.19 – What? Me Worry?

August 14, 2019

SHI 8.28.19 – It Depends on How You Look at It

August 28, 2019

“Years ago, Alan Greenspan coined the phrase ‘irrational exuberance.’ Ruchir Sharma has now added ‘irrational anxiety’ to our economic lexicon.”

Ruchir Sharma is the ‘Chief Global Strategist’ and head of the Emerging Markets Equity team at Morgan Stanley. A few days ago, Mr. Sharma published a great OP-ED in the NY Times titled, “Our Irrational Exuberance about ‘Slow’ Growth.” It’s worth a read. Here’s the link (right click, and ‘open link in another tab’):

https://www.nytimes.com/2019/08/17/opinion/sunday/global-recession.html

The bottom line: I think Ruchir has been reading my blogs. In fact, his article seems to highlight the exact same things I’ve said for the past year or two:

Since the financial crisis of 2008, the world economy has been struggling against four headwinds: deglobalization of trade, depopulation as labor forces shrink, declining productivity and a debt burden as high now as it was right before the crisis.

- Ruchir Sharma

Spot on! High five! 🙂

Of course, I’m kidding. Mr. Sharma’s thoughts are his own … just as mine are mine … and I’m pleased to see such an accomplished individual has views so similar to my own.

So what does this have to do with GDP growth and negative interest rates? Read on, my friends, read on.

Welcome to this week’s Steak House Index update.

If you are new to my blog, or you need a refresher on the SHI10, or its objective and methodology, I suggest you open and read the original BLOG: https://www.steakhouseindex.com/move-over-big-mac-index-here-comes-the-steak-house-index/

Why You Should Care: The US economy and US dollar are the bedrock of the world’s economy. This has been the case for decades … and will be true for years to come.

But is the US economy expanding or contracting?

According to the IMF (the ‘International Monetary Fund’), the world’s annual GDP is about $84 trillion today. US ‘current dollar’ GDP now exceeds $21.3 trillion. In Q2 of 2019, nominal GDP grew by 4.6%. The US still produces about 25% of global GDP. Other than China — in a distant ‘second place’ at around $13 trillion — the GDP of no other country is close. The GDP output of the 28 countries of the European Union collectively approximates US GDP. So, together, the U.S., the EU and China generate about 70% of the global economic output. This is worth watching carefully, right?

The objective of the SHI10 and this blog is simple: To predict US GDP movement ahead of official economic releases — an important objective since BEA (the ‘Bureau of Economic Analysis’) gross domestic product data is outdated the day it’s released. Historically, ‘personal consumption expenditures,’ or PCE, has been the largest component of US GDP growth — typically about 2/3 of all GDP growth. In fact, the majority of all GDP increases (or declines) usually results from (increases or decreases in) consumer spending. Consumer spending is clearly a critical financial metric. In all likelihood, the most important financial metric. The Steak House Index focuses right here … on the “consumer spending” metric. I intend the SHI10 is to be predictive, anticipating where the economy is going – not where it’s been.

Taking action: Keep up with this weekly BLOG update. Not only will we cover the SHI and SHI10, but we’ll explore related items of economic importance.

If the SHI10 index moves appreciably -– either showing massive improvement or significant declines –- indicating growing economic strength or a potential recession, we’ll discuss possible actions at that time.

The BLOG:

I always enjoy the Hollywood movie claim: “Based on a True Story.” Well here’s a yarn also based on a true story.

A good friend of yours, spending the afternoon in your backyard, lazing the day away with an afternoon swim, and a barbecue, happens to mention, “Hey, you know, I’m a few dollars short this month. I was wondering if you can lend me $1,000? You know I’m good for it, right? I’m thinking I’ll pay you back in 30 years. But no interest. In fact, I was thinking that in 30 years, I’ll pay you back $965. Can you help me out?”

Knowing a great deal when you see one, you jump on this opportunity. Faster than you can say ‘kinck-nacks and paddy-wacks’ you set down the B-B-Q tools, whip out your check book, and write your friend a check for $1,000. Knowing full well your money is now completely safe for the next 30 years. Tonight, you will sleep well.

OK….what do you think? True story or Hollywood fiction? Before you answer, here’s the true story, from today’s Wall Street Journal:

“Germany sold 30-year debt at a negative yield for the first time, as investors desperate for safe assets bet that further falls in yields will boost the value of the bonds in the future. Investors buying debt at a negative yield get back less than they paid if they hold on until maturity. In Wednesday’s sale, Germany borrowed €824 million ($914 million) through bonds that pay no interest. The bonds were sold slightly above face value, so when they mature in 2050, Germany will pay back €795 million.“

So, summarizing:

- Issuing bonds, Germany just borrowed about $900 million.

- The term of the bond is 30 years. They will be repaid in 2050.

- The bond is a zero coupon bond. Meaning is has no interest rate.

- The bonds sold for more than the face value of the bond.

- When a $1,000 bond is repaid, Germany will pay the bondholder about $965.

No this is not a Hollywood fantasy. This is a true story.

Truth is definitely stranger than fiction. Because in 30 years, not only will this investor receive less than their original investment back … but if inflation is above zero, their inflation-adjusted return is much, much worse. For example, if annual inflation is only 1.0% for this 30 year period — only half of what the ECB is working hard to achieve — then after adjustment for inflation, $1 lent to Germany today will be worth 74 cents in 30 years. And this is at an annual inflation rate of only 1.00%. Are you wondering what would happen at a 2% inflation rate? That same $1 would be worth 55 cents in 2050. Ouch. That really hurts. The only logical conclusion: These investors must be expecting zero inflation over the next 30 years — or even worse, deflation in Germany.

Joachim Fels works at PIMCO. And he also writes a blog. Back in 2015, he wrote one called, “No End to the Savings Glut.” And earlier this month, followed it up with a blog entitled, “Interest Rates: Naturally Negative?”

Google him and the blogs, if you’re interested. Good reads.

Anyway, here’s the bottom line. There’s a lot of money sloshing around out there. Ben Bernanke commented on this issue more than a decade ago … and more capital has accumulated since then. Add to this mix the aging population and longer life expectancy, and the fact that older folks tend to be savers as opposed to investors or spenders, and you have a lot of people with a lot of money looking for very safe places to keep their capital for the long term.

In the history of mankind, this phenomenon has never occurred before. This is new.

Now, add to this incendiary mix the fact that populations and labor forces in most developed countries are actually shrinking — again, something that has never happened before — and we have a really perplexing problem: GDP will have trouble growing in shrinking countries. In fact, if not for new technologies and robots, GDPs in shrinking countries might even shrink.

So in this new age, we must view each country’s potential long-term GDP growth as some function of its population growth rate. If population and labor force is shrinking (think Japan), then that country’s GDP is likely to shrink, too. If both are somewhat static, or growing slowly, then perhaps that country can eek out 1.5 – 2.0% annual GDP growth. Maybe. And if population is growing meaningfully, under the right conditions annual GDP growth could potentially be 4% plus.

Which brings me to a fascinating variable impacting population growth: Immigration. Consider this: Capable and industrious folks from other nations want to immigrate to the US. Even today. Which is why I find current US “legal” immigration policy so vexing. After all, if capable, educated, hard-working folks wish to legally immigrate to the US, and the US GDP growth rate would be enhanced by there presence here, shouldn’t we welcome them with open arms? The US remains a highly desirable destination for educated, legal immigrants. Should we take ’em in? High-quality legal immigrants sure help solve the US labor-force growth challenge, right?

Or is my idea dumb? Just one more to stack on the “irrational” pile with exuberance and anxiety? My 2 cents. OK…let’s head to the steakhouses and see if Mastros is serving a ‘Beyond Beef’ Filet.

Nope. No Beyond Beef entrees at Mastros just yet. 🙂

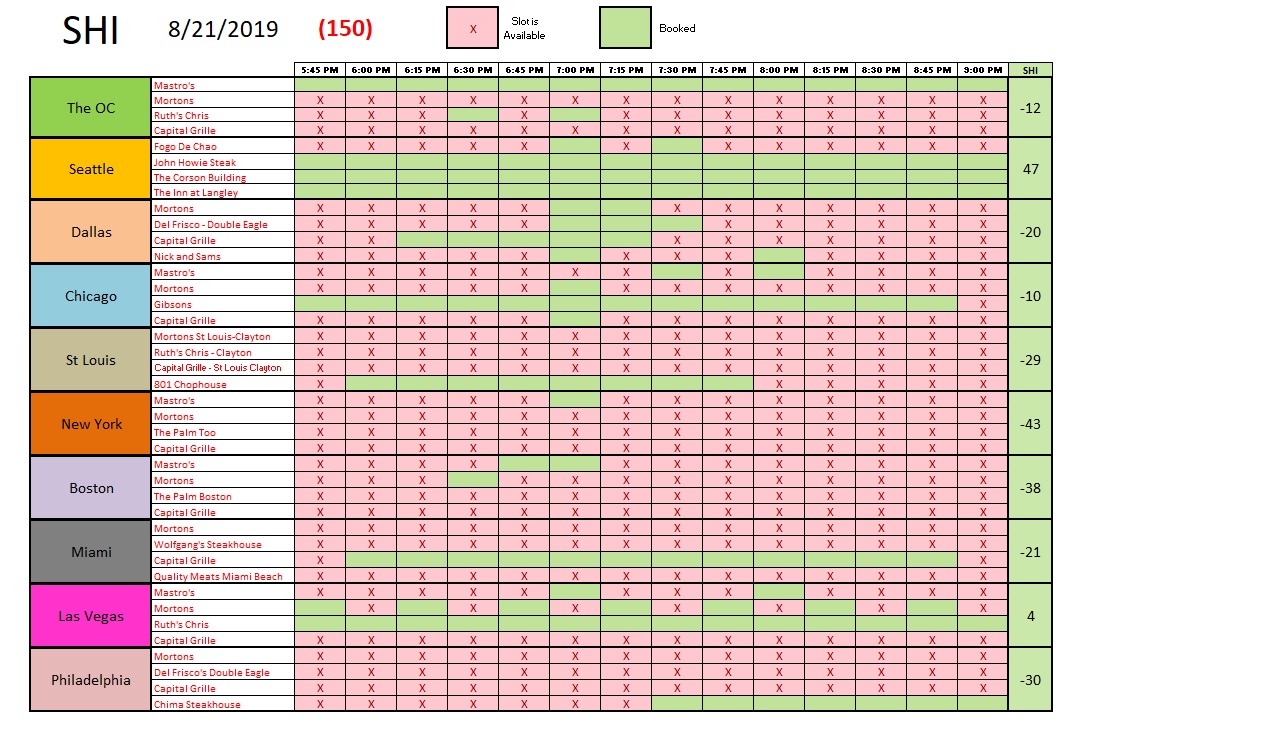

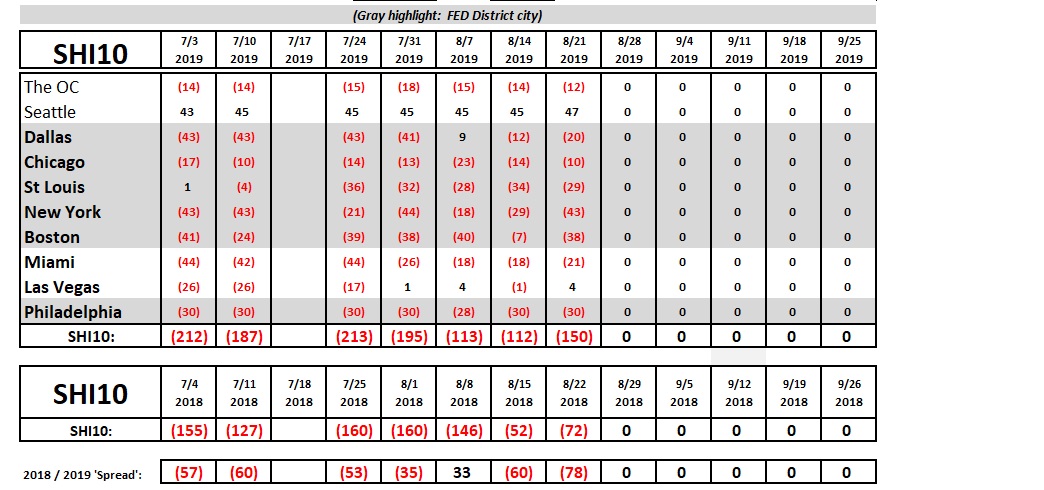

And not much new on the reservation front either. The SHI10 number is a bit worse than last week … but not appreciably. Here’s the grid:

The long-term trend, too, is quite stable.

As you can see, reservation demand — week over week — remains fairly consistent. The consumer is consuming expensive steaks with the same basic vigor as the year progresses.

By the way, switching gears back to the conversation above, were you wondering where the United States labor force growth ranks compared to our peers? Is our labor force shrinking, like Japans? Or are we growing like gangbusters?

The reality is somewhere in between. If we head over to the BLS to grab some numbers, we find that the US ‘Civilian Labor Force’ (CLF) grew from about 154.2 million folks in January of 2009 to about 163.2 million people in January of 2019 — about 10 years later. So the growth rate of our CLF is just slightly above 0.5% per year. Good news. We’re growing. Bad news. We’re growing very slowly.

Which is why the days of US GDP growth rates of 4% or more are likely a thing of the past. Any suggestion that the US can achieve or exceed this level today, assuming conditions remain the same, is pure Hollywood fiction.

– Terry Liebman