SHI: Steak House Index UPDATE 9/14/16

The FED Watches Inflation like a Hawk

September 13, 2016The Rise of the Central Bank

September 18, 2016What a week in the financial markets! Are we having fun yet? ?

After months of tranquil, almost boring stability in both the stock and bond markets, domestically and around the globe, both have awakened with attitude! The VIX is thru the roof (https://terryliebman.wordpress.com/2016/09/09/the-vix-goes-crazy/), the DOW is down hundreds of points, and rates are up across the globe.

All of which begs the questions: What does this mean? Why is this happening now? And finally, what does this volatility portend for the SHI? Let’s take a look.

(If you need a refresher on the SHI, or it’s purpose and methodology, open and read the original BLOG: https://terryliebman.wordpress.com/2016/03/02/move-over-big-mac-index-here-comes-the-steak-house-index/)

Why You Should Care: The US BEA publishes the most recent GDP figures the instant they’re available. Unfortunately for us, it is a trailing index. The data is old news, a lagging indicator.

Year to date in 2016, the real US GDP is trending at only 1.0%. A lackluster reading at best. Will Q3 be better? I’d sure like to know in advance, wouldn’t you? 🙂

Personal consumption expenditures, or PCE, was the strongest component of the last GDP reading. In fact the vast majority of the latest quarter 1.2% GDP increase came from consumer spending. Clearly this is an important metric to track.

The SHI may help us do just that. I intend the SHI is to be predictive, helping us anticipate when the economy is going to move in a different direction – up or down. Giving us the ability to take action early – not when course corrections might be too late.

Taking action: Just keep up with the weekly column. If the index changes appreciably – either showing massive improvement or significant declines – indicating expanding economic strength or a potential recession, we’ll discuss possible actions at that time.

Trending is very important…and we’ll watch the trend.

THE BLOG: Clearly the halcyon days of summer are gone. In just the past few days, we’ve had FED bank presidents, industry titans, hedge funds, and an assorted group of economists opine the THE END IS NIGH!

If we’re to believe these pundits:

- The US economy is doing great;

- The US labor force has reached full employment;

- The FED needs to step in – now – and cool down the economy before it overheats;

- Which means, a rate increase is imminent, and,

- If the FED fails to move soon, a bubble may form in both real and financial asset values.

Hmmm…let’s take a closer look. The rhetoric has certainly shaken the global bond markets. Here’s a great image from yesterday’s WSJ:

We see yields on Japanese sovereign debt have been moving UP since the beginning of August; in Germany, within the last week or so. As bond yield and bond value move inversely, investors in those bonds are getting crushed.

And yet, looking at the chart to the left, about $13 TRILLION of global debt (this sum now includes a bit of high-rated European corporate debt) continues to yield negative returns.

Let me repeat that: $13 trillion. Said another way, that’s about 29% of ALL sovereign debt on the planet. Investors owning 29% of this debt pay to own it. Sure, a lot of that is owned by the Bank of Japan (BOJ) and the ECB. But most is not. Most is in the hands of individual and institutional investors.

A few years ago, my kids bought me a book for Christmas: “The History of Interest Rates.” The book covers interest rates and lending practices since the birth of both, about 5,000 years ago. Sounds riveting, right? Well, I was happy with my present. On September 9th, the WSJ published an article entitled. “Hostage to a Bull Market” in which they questioned one of the authors of that book: “In the past 5,000 years, when was the last time we saw negative interest rates?” Their answer: Never. Not once in the past 5,000 years.

Before we move on, let’s be sure we understand the full scope of this historically unique event: While 29% of the approximate $45 trillion outstanding in sovereign debt is negative yielding, the other 71% is also at record-low yields. Yields the globe has not seen in the past 5,000 years. Not once. Without exception.

Which means, if global interest rates were to rise significantly or meaningfully, investors are likely to experience trillions of dollars in losses. Trillions. Are these investors wrong? Have they made a poor investment…certain to generate losses? Losses that may, in the aggregate, exceed $5 trillion or more?

Or are they making prudent choices? Intelligent choices?

We often assume that simply because something has never happened before, it’s an aberration, something that will self-correct soon. But here’s the the thing about things that have never happened before: Once they occur, so does a new reality. And, of course, we have no idea – until years into the future – if this new occurrence was simply an aberration, or if it is now the “new normal” if you will.

In statistics, there is a phenomenon called ‘regression to the mean’ which suggests over time a variable wildly divergent from its mean (norm) will return toward that norm over time. Many experts and economists believe that’s precisely what will happen here. Over time, rates will ‘normalize’ and return to their historic averages.

If they’re right, then, yes, the FED should raise short term rates now … moving the needle more toward that long-term ‘mean.’ A single move which will likely have little, if any, long-term impact on interest rates or asset values.

But if they’re wrong, unfortunately, we all know the series of cascading events a poorly timed rate lift might set into motion:

- The markets will assume this is the first of perhaps two or more rate increases;

- GDP growth will be adversely impacted, raising the possibility of a near-term recession;

- many asset values (equity and debt) will likely decline in response;

- fear and uncertainty will increase;

- consumer spending will likely decrease;

- jobs will likely be lost;

- etc.

Consider this: It’s entirely possible – even likely – current interest rate levels are the new normal. Isn’t it possible – perhaps even probable – the current interest rates reflect the new, low “natural” rate of interest? Sure, it’s not happened in the past 5,000 years … but could it be happening right now. $45 trillion of investment capital says yes, this is the new normal. I agree.

I’ll finish this portion of the BLOG with a few comments from Ben Bernanke, from his blog post yesterday entitled, “Modifying the Fed’s policy framework: Does a higher inflation target beat negative interest rates?” Here’s what Ben had to say:

“Nominal interest rates are very low, and in a world of excess global saving, low inflation, and high demand for safe assets like government debt, there’s a good chance that they will be low for a long time. That fact poses a potential problem for the Federal Reserve and other central banks: When the next recession arrives, there may be limited room for the interest-rate cuts that have traditionally been central banks’ primary tool for sustaining employment and keeping inflation near target.

Negative rates and higher inflation targets can be viewed as alternative methods for pushing the real interest rate further below zero. In that context, I am puzzled by the apparently strong preference for a higher inflation target over negative rates, at least based on what we know now. Y es, negative interest rates raise a variety of practical problems, as well as political and communications issues, but so does a higher inflation target.

In this post, I argue that it’s premature for policymakers to emphasize the option of raising the inflation target over the use of negative rates. Pending further study about the costs and benefits of both approaches, we should remain agnostic about whether either or both should be part of the Fed’s policy framework.”

(here’s the blog if you’d like to read Dr. Bernanke’s entire post: https://www.brookings.edu/blog/ben-bernanke/2016/09/13/modifying-the-feds-policy-framework-does-a-higher-inflation-target-beat-negative-interest-rates/)

Again, I tend to agree.

Phew, this is mentally exhausting, right? It’s DEFINITELY time for a steak! 🙂

OK…let’s head over to the Capital Grille because, hey, they need customers! But the other 3 do not: This week the SHI comes in at a recent high – a positive 9!

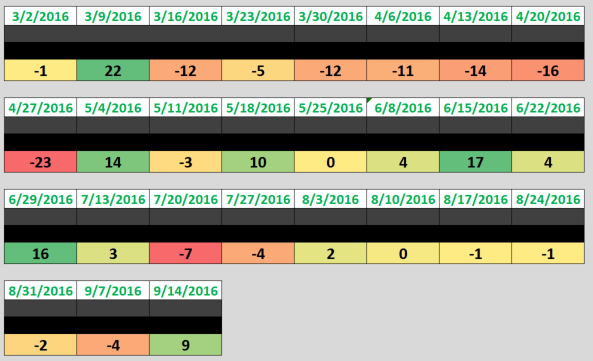

Here is the data:

Mastro’s is completely booked. Both Mortons (Santa Ana) and Ruth’s Chris (Irvine) are showing strength. Clearly, the consumer is feeling good … expensive steaks are flying off the shelf (or grill)!

Here’s the trend graphic:

While a positive 9 is a solid SHI reading, it does not indicate the US economy is overheating. (Remember, the possible weekly range of outcomes is (-44) to a positive 72. At a positive 9, we’re right in the middle. ) Like a beautiful, medium-rare filet, the temperature is just right!

We’ve been tracking the SHI since March 3rd. How has it been trending? Let’s take a look:

The blue line shows week-by-week movement; the red line is the long term linear trend. This week we see an up-tick. But when viewed in the macro, the SHI continues to report relative stability in consumer demand.

The market volatility is the natural results of conflicting future views. Everyone with ‘skin in the game’ so-to-speak is trying to read the tea leaves. Both here in the US and abroad.

The FED – and all the central banks of developed nations – have a difficult job today. Charged with growing GDP, while holding inflation in check and all-the-while maintaining full employment, they’re navigating choppy, turbulent waters.

Who’s right? Ben Bernanke? Or some of the current FED bank presidents? While we continue to seek the right path, I believe the FED will take action only when they firmly, and possibly near-unanimously, feel a rate hike is the correct policy.

All the rhetoric aside, they’re not there yet. Perhaps by year end. But not now. Until then, expect volatility and uncertainty…but little else will be different.

- Terry Liebman