SHI: 10/11/17 Are Asset Values too High?

SHI 10/4/17: Their Own Set of Facts

October 4, 2017

SHI: 10/18/17 Rent or Buy, Prices are Steep

October 18, 2017

Well, they are certainly expensive.

Across the globe, stocks, bonds and real estate are all quite pricey from a historical perspective. But are they too high?

The answer, I believe, is no. But my answer is a bit fluid as it depends on another variable. On what, you ask? In my opinion, I believe the answer is interest rates. Or, more specifically, (1) the perceived level of long-term interest rates and (2) the actual, natural, level of long-term rates, for the foreseeable future. Something we call R-star.

Welcome to this week’s Steak House Index update.

If you are new to my blog, or you need a refresher on the SHI, or its objective and methodology, I suggest you open and read the original BLOG: https://www.steakhouseindex.com/move-over-big-mac-index-here-comes-the-steak-house-index/

Why You Should Care: The US economy and US dollar are the bedrock of the world’s economy. At present, is the US economy expanding or contracting? We need to know.

The world’s GDP is about $76 trillion. At last count, our ‘current dollar’ US GDP is now over $19 trillion — about 25% of the total. No other country is even close.

The objective of the SHI is simple: To help us predict US GDP movement ahead of official economic releases — important since BEA data is outdated the day they release it.

‘Personal consumption expenditures,’ or PCE, is the single largest component of US GDP — about 2/3 of the total. In fact, the majority of all US GDP increases (or declines) usually result from (increases or decreases in) consumer spending. Thus, this is clearly an important metric to track. The Steak House Index focuses right here … right on the “consumer spending” metric.

I intend the SHI is to be predictive, anticipating where the economy is going – not where it’s been. Thereby giving us the ability to take action early.

Taking action: Keep up with this weekly BLOG update.

If the SHI index moves appreciably -– either showing massive improvement or significant declines –- indicating expanding economic strength or a potential recession, we’ll discuss possible actions at that time.

The BLOG:

Unlike gold or diamonds, where value is determined by scarcity, the value of an “investment” asset is usually some function, or multiple, of its expected future income stream.

Robert Shiller, a well known economist and the father of the ‘Case-Shiller’ real estate index, believes the US stock market is “very expensive right now.” In an article published on April 16th, entitled “The Mystery of Lofty Stock Market Elevations,” Dr. Shiller expressed concern the CAPE ratio — a metric he helped develop — is at a “worrisome level.” The Economist Magazine is a bit concerned as well. On October 7th they published a piece titled, “The bubble without any fizz,” wherein they opined the S&P 500 is “uncommonly expensive,” European and emerging-market stockmarkets are “handily above their long-run average,” home values are “far above” their long-run averages in Canada, Australia and England. Here in the US, home prices (in nominal terms) have surpassed their prior 2008 peak. Further, they comment bond prices, and bond spreads, are abnormally frothy, and asset prices paid by private equity investors are “pushing up prices there, too.”

Is it time to move everything to cash and head for the hills?

No. Well, perhaps more accurately, we’ll know the correct answer in 3 or 4 years. But today, my opinion is ‘no.’ Why?

In the past, I’ve written numerous posts about low inflation rates, lack of correlation between the unemployment rate and wage growth, central bank borrowings, and today’s level of R-star — the “natural rate of interest.”

It is my opinion that values of three of the four major asset groups (stocks, bonds and real estate) are all highly inversely correlated with long-term interest rates. Only commodities — the fourth asset group — I believe, are predominantly uncorrelated. Long term rates are low … and so stocks, bonds and real estate values are high.

Long-term real interest rates have declined steadily since the early 1980s, and are now at or near historic lows. The ten-year Treasury bond yield was near 2% a month ago, and is likely now in a ‘trading range’ between that level and 2.5%. FED short-term rate increases may have some impact on this rate, in the short run; but, over the mid-range, central bank balance sheet downsizing could have a larger impact — if they were to downsize too quickly. Which I believe they will not.

The rate on US ten-year inflation-protected bonds — known as TIPS — is a paltry 0.5%. In Europe ‘real’ bond yields are negative. These rate conditions are not new: In February of 2014, Mervyn King and David Low wrote a paper for the NBER titled “Measuring the “World” Real Interest Rate” wherein they suggested:

Much of the “collapse,” in my opinion, has been more of a ‘reversion to the mean’ than an actual rate collapse. But make no mistake here: Rates are way, way down. And have been for an exceptionally long time. The King/Low paper is pretty dense with theory, but worth a read if you find this topic interesting.

These are conditions I believe to be the new normal. The new R-star. So, yes, asset prices are high. But are they too high? Again, I don’t think so. Today’s asset values reflect the new normal in rates.

Before I leave this topic, let me share something I found entertaining in a Bloomberg update from this morning. Again, the topic was asset values. And how both Richard Thaler — the most recent winner of the Nobel prize in Economics — and Rober Shiller are worried about asset value levels. The author commented,

“… maybe there’s a link between brilliance and skepticism that’s unhelpful for stock investing in the long run. Smart people can’t help but try to poke holes in things, and see the weaknesses in existing systems.”

So if you’re really troubled about asset values … you must be a smart and brilliant investor! 🙂

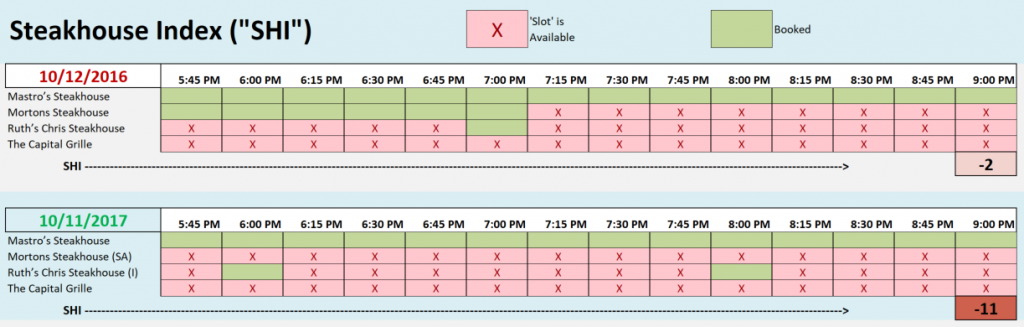

Are high steak prices keeping folks out of our steak houses? Or are consumer spending levels just a bit muted today? Here’s today’s SHI chart:

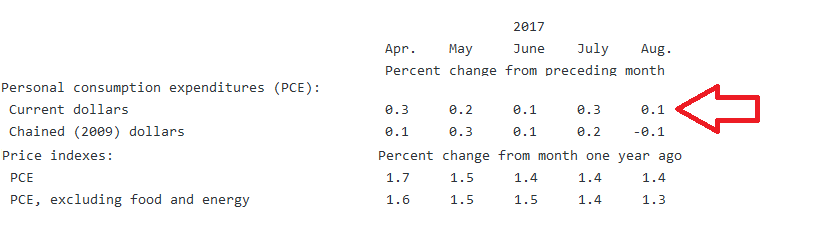

Once again, with the exception of Mastro’s, our other pricey eateries are not seeing much demand. This SHI result is consistent with numbers posted by the BEA in their “Personal Income and Outlays, August 2017” press release:

As can be seen above next to the red arrow, the increase in PCE slid dramatically from the prior month. I included the PCE ‘price index’ information, too. This Y-O-Y inflation index, as you can see, has been stuck at 1.4% — even lower if we exclude the volatile food and energy segments.

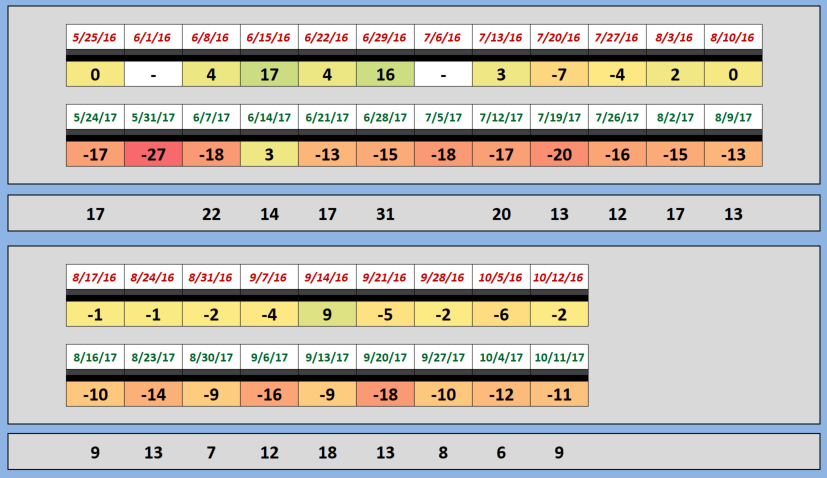

Here’s the longer term SHI trend chart:

By the way, I’m looking for more ‘votes’ on the idea to increase the SHI to cover a total of 10 or 15 cities — to expand our geographic footprint.

Yeah? Nay? Make your vote count! 🙂

- Terry Liebman

8 Comments

I think covering 5-7 large markets would be a better sample. Yes

Thanks John! – T

I agree that an increase in the number of markets used would be a good idea.

Unrelated question, what impact, if any, will all of the recent natural disasters our country (and others) have experienced have on the SHI & the US economy?

Thanks Kelly! Natural disasters are horrible for the poor folks impacted. We never want to lose sight of the human issues. Economically, they tend to have a short-term and a longer-term impact. Short-term: Negative. Job losses. Consumer spending down. Etc. But over the ‘rebuilding cycle’ – which emulates an infrastructure boost – the impacts are quite the opposite and very positive for the economy as a whole. – T

I vote Aye on expanding the geographic base for the SHI. I think it would be very interesting to see if there are regional variations in the data. Do “blue states”, for example, reflect a higher or lower degree of optimism over our economic future than “red states”; the coast vs the south vs the midwest; rural vs urban. A different picture might emerge. Or your current findings might be confirmed. Only the Shadow knows…..

Thanks Kevin! I appreciate the comment. – T

Thanks for your blog. I vote yes!!

I vote that your index should be broadened to include more cities and, in particular, some less affluent communities. I also think it may be beneficial to include some mid-priced restaurants that require reservations in your index.

I really enjoy reading your blog Terry and the fact you’re not afraid to take a stance…no surprise there!