SHI: 10/18/17 Rent or Buy, Prices are Steep

SHI: 10/11/17 Are Asset Values too High?

October 11, 2017

SHI: 10/25/14 Recession Talk

October 25, 2017

Whether one rents or owns, prices are high. And likely to get higher.

At its essence, economics usually boils down to ‘supply’ and ‘demand.’

If an item’s supply outstrips demand, prices fall. Sometimes far beyond expectation. And the opposite is true as well: If supply is not keeping up with demand, the price of that item can rise precipitously. The supply of American housing is not keeping up with demand…and, even worse, the challenge grows greater every year. And this trend might harm GDP growth.

Welcome to this week’s Steak House Index update.

If you are new to my blog, or you need a refresher on the SHI, or its objective and methodology, I suggest you open and read the original BLOG: https://www.steakhouseindex.com/move-over-big-mac-index-here-comes-the-steak-house-index/

Why You Should Care: The US economy and US dollar are the bedrock of the world’s economy. At present, is the US economy expanding or contracting? We need to know.

The world’s GDP is about $76 trillion. At last count, our ‘current dollar’ US GDP is now over $19 trillion — about 25% of the total. No other country is even close.

The objective of the SHI is simple: To help us predict US GDP movement ahead of official economic releases — important since BEA data is outdated the day they release it.

‘Personal consumption expenditures,’ or PCE, is the single largest component of US GDP — about 2/3 of the total. In fact, the majority of all US GDP increases (or declines) usually result from (increases or decreases in) consumer spending. Thus, this is clearly an important metric to track. The Steak House Index focuses right here … right on the “consumer spending” metric.

I intend the SHI is to be predictive, anticipating where the economy is going – not where it’s been. Thereby giving us the ability to take action early.

Taking action: Keep up with this weekly BLOG update.

If the SHI index moves appreciably -– either showing massive improvement or significant declines –- indicating expanding economic strength or a potential recession, we’ll discuss possible actions at that time.

The BLOG:

I’m concerned about the future of housing and its potential adverse impact on US GDP. If you are not, yet, you are likely join me by the time you’ve finished this blog.

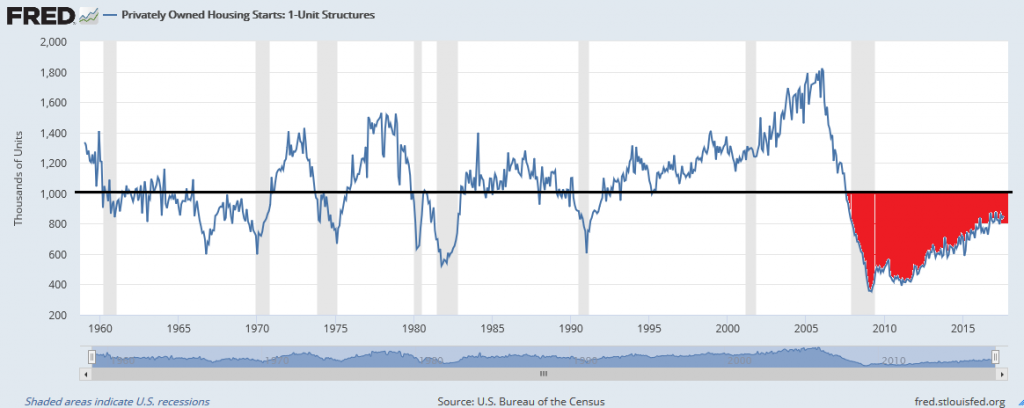

There are homes and apartments available to rent or buy, but year after year supply falls further behind. Causing both choices to be pretty darn expensive. What’s causing the problem? Take a look at the chart below, courtesy of the St. Louis FED and their research engine, FRED:

I added the black, horizontal line. And I added the red “fill.”

The black line is the average annual 1-unit (home) housing starts for the past 60 or so years. The number? Right around 1 million new 1-unit properties have been added, on the average, per year for about 60 years. The red “fill” shows the shortfall during the past 10 years. During the past 10 years, the “Seasonally Adjusted Annual Rate” — known as SAAR — has been closer to 600,000 per year. Meaning the United States, on the whole, has fallen far behind the 60-year average. Probably by about 400,000 homes per year — or 40% of the average.

Which creates a serious housing problem. Remember: When supply falls short of demand, prices rise. The recently released “USC Casden Forecast: 2017 Multifamily Report” discusses just this issue. Quoting the first two lines in the report:

Their answer: “The answer likely is the result of two forces: homeowner equity, and regulation.” Their “homeowner equity” discussion is interesting. They attribute insufficient equity to much of the problem:

“It is still the case that in 44 out of 100 of the largest US MSAs (cities), house prices have not yet returned to 2007 levels. In another 17 cities, prices, while higher, are only 10% higher or less than they were in 2007. ”

Here is their explanation of why this matters:

“To understand why this matters to new construction so much, consider the fact that most buyers of new homes are “trade-up” buyers: people who are moving out of a starter homes and into a newer, upgraded home. Between the end of World War II and the early 2000s, a typical first time homeowner could build equity by simply staying in their appreciating house, and then using that equity to buy up to a new home. But over the past ten years, many first time homeowners either lost equity, or built relatively little, meaning that they didn’t develop the wherewithal for a down-payment on a new house. This slowed the demand for new housing, even in a market where the overall demand for housing was increasing.”

This may not be as much of a problem here in California…or New York. For the “trade-up” buyer, at least. But it’s a serious issue in all markets between the coasts.

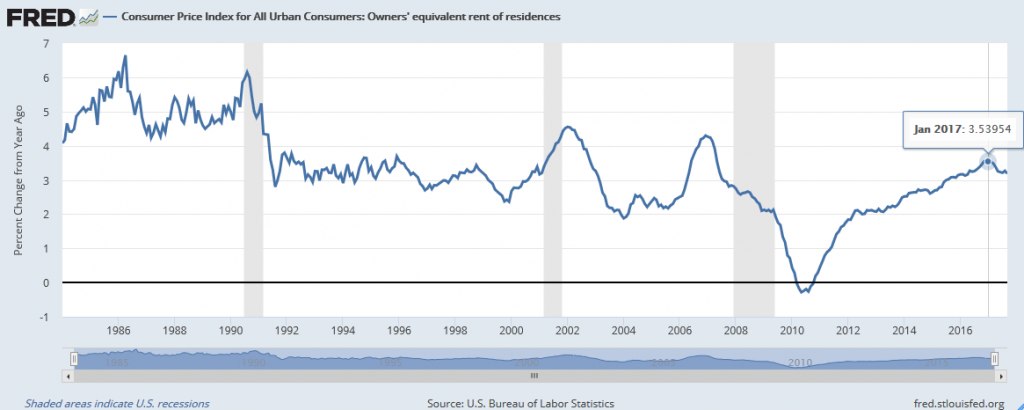

The bottom line: More people are renting … and rental rates have been rising. Significantly. Let’s ask FRED for another chart to see just how much rents have been increasing across the nation:

The answer: Since early in 2010, A LOT!

Even though the two most popular inflation gauges, the PCE and the CPI, have been far below 3.5% per year, the CPI rent metric (see above) — for the US as a whole — exceeded this figure back in January of this year. Increases in annual rental expense has been one of the largest contributors to both CPI and PCE increases in the past few years. The CPI more heavily weights rent in its calculation; the PCE, about 1/2 as much. As home or apartment rental rates are increasing faster than other components, this is one reason why CPI gains are usually higher than the PCE.

Rental rates in California have risen more rapidly than the nation as a whole. Making California an expensive place to rent or own. The Casden report continued:

“…because rents have risen so much, homeowning has become relatively attractive in many parts of the US.” Why might this fact be impactful to the SHI? The report offered this as a final thought: “The upshot of this is that after median rent is subtracted from median income, disposable income for median renters has fallen in the vast majority of MSAs around the country.” Ahhh….there we go: Consumers may have less disposable income.

Life basics include food, shelter and clothing. In theory, disposable income is what’s left. According to the Dictionary, ‘disposable income’ is “income remaining after deduction of taxes and other mandatory charges, available to be spent or saved as one wishes.” OK, therefore ‘disposable income,’ at least in theory, can be spent as the earner chooses.

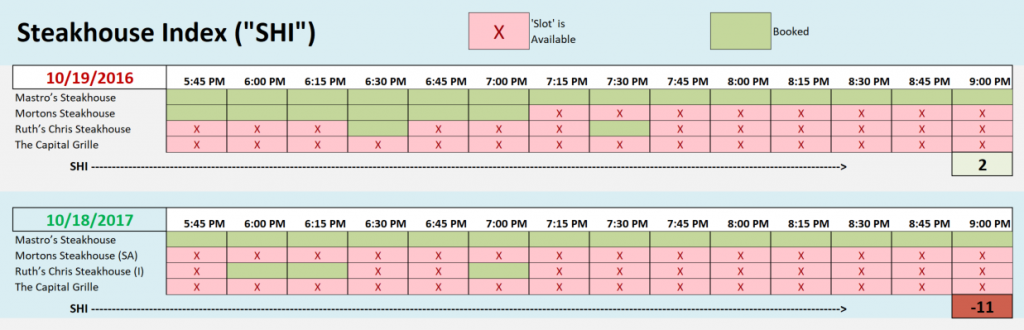

The SHI is intended as a proxy to measure increases or decreases in consumer spending. As housing costs are increasing across the nation, if wage gains don’t keep up, then a smaller “slice of the pie” is available for wage earners to spend on consumer goods. Thereby reducing GDP growth. Is this trend reflecting in our SHI results? Let’s take another look at the high-priced eatery reservations this week:

This week is quite consistent with the prior week. The SHI reading is a negative <-11> just as it was last week. Once again, Mastro’s Ocean Club is leading the pack — by a wide margin. This Saturday night, you can’t get a table for 4 at ANY time. Considering the lofty prices of their self-described “classic entrees, including steaks & seafood, star at this sophisticated spot with old-school charm,” this is an impressive feat. Only Ruths’ Chris also had booked time slots. Here’s our longer term SHI trend report:

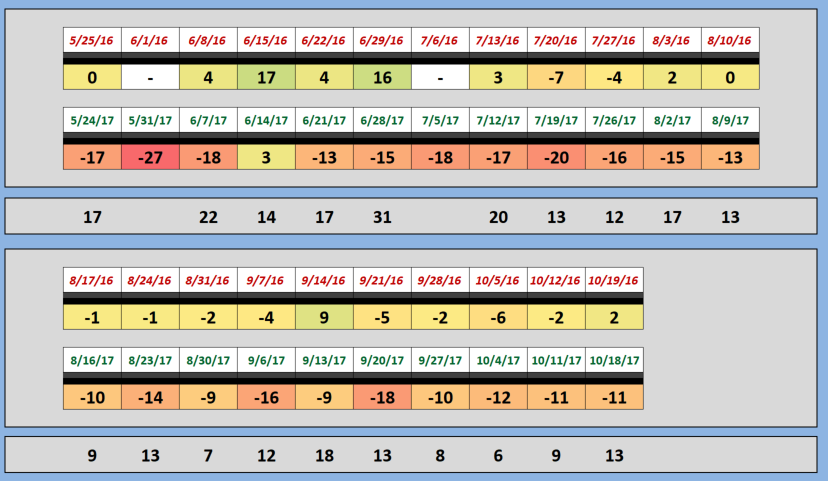

This week, the ‘spread’ is back in the double-digits: 13. But, once again, very consistent with the trend we’ve seen this quarter. Some of the weakness from the end of May thru the end of July seems to have moderated, and since that time, the SHI readings have been range-bound.

Steady as she goes.

- Terry Liebman

2 Comments

Steak House Master,

I don’t remember a blog (I might have missed it, or it might not have happened) where you discuss the possibility what effect the election last year had on the steakhouse index. We are nearing the date of the election and I am interested in seeing the data. Did it ramp up or did it decline heavily (or stay level)? How will that compare to this year? After looking at a quick graph of last year compared to last year, last year’s trendline shows a decline overall at this point and this year shows an increase. Granted neither have a great R-squared value, but interesting nonetheless.

Any thoughts on this?

The Steak House Disciple

Hello Disciple! In the final analysis, the SHI is focused on macro-economic outcomes. The biggest of which is the GDP. Did the presidential election result directly impact the economy…and thus GDP growth? In my opinion, no.

Now, alternatively, did the election result impact perceptions and future expectations? Absolutely. Which is one of the reasons the DOW closed above 23,000 today for the first time. And if those expectations change (tax cuts, increased corporate profits, streamlining business conditions), for any reason, or if some exogenous event changes expectations, that might be the reason the DOW once again closes below 20,000. We’ll have to see.

But, no, until the administration has some success actually changing the economic climate — something they have yet to do — it’s pretty much business as usual. Thanks for the question! – T