Move Over, Saudi Arabia!

January 8, 20172017 Forecast: The FUTURE is ….

January 17, 2017

Trump’s inauguration is a week from Friday. On January 20th. On January 21st his “First 100 days” begin.

Trump plans to run America like a business: “Under budget and ahead of schedule,” Trump assured us – perhaps somewhat metaphorically – back in October, making his case at a new Trump hotel. Can this be done – effectively?

Welcome to the first Steak House Index update of 2017. As this is BLOG 1 for January, today we will update both the SHI and the SHCI.

By the way, I think you know I’ve migrated this BLOG to a new URL – https://www.steakhouseindex.com/ The reading experience on the site is much better than in the email form. I suggest you click the preceding link and give it a try!

Why You Should Care: The US economy and US dollar are the foundation of global economics: our nominal GDP is over $18.5 trillion a year. Is it growing or shrinking? Is it possible to know – before the quarterly GDP releases from the BEA?

The objective of the SHI is simple: To predict the direction of this behemoth ahead of official economic releases. But while the objective is simple, the task is not.

BEA publishes GDP figures the instant they’re available. Unfortunately, it is a trailing index. The data is old news; it’s a lagging indicator.

‘Personal consumption expenditures,’ or PCE, is the single largest component of the GDP. In fact, the majority of all GDP increases (or declines) usually result from (increases or decreases in) consumer spending. Thus, this is clearly an important metric to track.

I intend the SHI is to be predictive, anticipating where the economy is going – not where it’s been. Thereby giving us the ability to take action early. Not when it’s too late.

Taking action: Keep up with this weekly BLOG update. If the SHI index moves appreciably – either showing massive improvement or significant declines – indicating expanding economic strength or a potential recession, we’ll discuss possible actions at that time.

The BLOG: Let’s fact facts: Making predictions is easy … making accurate predictions? Not so much. You may have heard the joke: “Why did God create economists?” Give up?

To make weathermen look good. 🙂

The new Trump administration makes forecasting even more difficult. I’m not complaining. Simply stating facts. Because even if America is “run like a business” in the upcoming 4 years, I have no idea what that means. What will the Trump administration and Congress focus on?

Changing corporate tax law? Individual tax cuts? Trade wars? Infrastructure spending? Walls? Quotas? International relations? Labor productivity? Import tariffs? Corporate profitability? Border taxes? Immigration restrictions? Fiscal stimulus? Creating new manufacturing strengths and jobs? Repatriation?

What will or will not be implemented? And when? How might our financial and political ‘adversaries’ react? And what might the unintended consequences be?

Or will we see ‘business as usual’ over the next 4 years? Has the campaign simply been, mostly, hype?

It will be interesting. And I suspect many of these questions will be answered in that first 100 days.

At least one strategic objective of the new Trump administration seems clear: An annual GDP growth of over 3%. After a decade at, or near, 2%, the new administration seems focused on a 3+ number. Can this be done? Is it possible? Great questions … and we’ll leave this discussion for another time. Sorry, but we have a lot to cover with the SHI and SHCI updates. Let’s get to it.

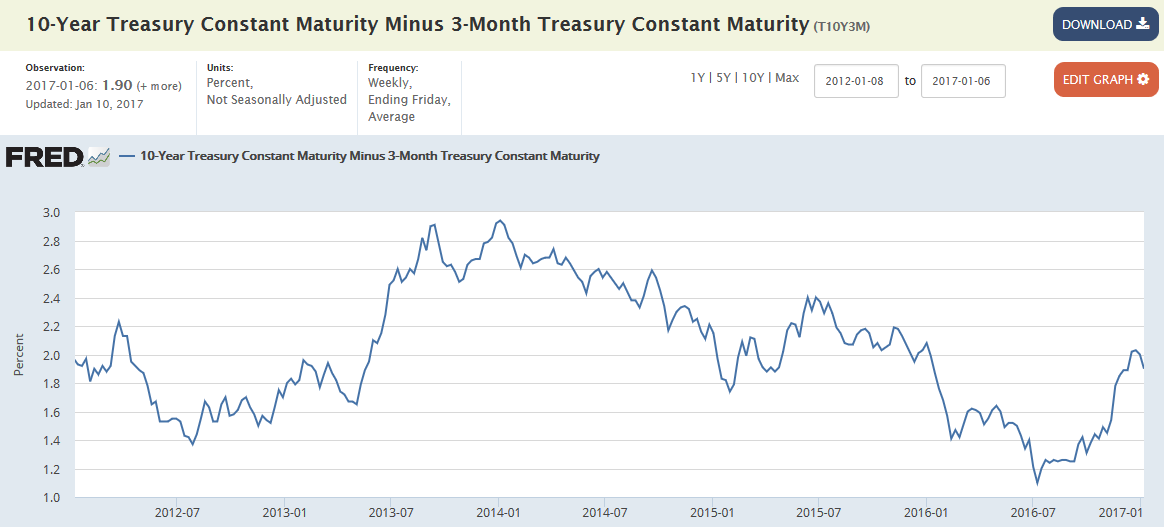

Here’s the graphic we use for our ‘Yield Spread’ discussion:

So the 10-year/3-month spread, last Friday, was 1.90% This suggests the probability of a near-term recession is less than 5%. Great.

On the other hand, the LMCI – the other metric we track for our composite index – has deteriorated. After 6 months of neutral or positive readings, the December LMCI fell below zero again, down to a negative (-.3). Here is a chart of all 2016 readings:

After 6 months of improvement, this favored FED index turned negative in December. But not significantly. A negative (.3) is fairly benign. Today’s JOLTs report, while a month behind, says pretty much the same thing: The job market condition is little changed. https://www.bls.gov/news.release/pdf/jolts.pdf

The BLS ‘non-farm’ employment survey, released on Friday the 6th, told us December added 156,000 new jobs. And the official unemployment rate was little changed at 4.7%. Both readings are solid, and again, benign. On the ‘better news’ side is the continued improvement in the U-6 unemployment rate: In December this “alternative measure” for the condition of the labor market again showed improvement:

The percentages above apply to the United States ‘civilian labor force’ (CLF). At the end of 2016, the CLF was about 160 million people. Meaning a U-6 decline from 9.9% in December of 2015 to 9.2% in December of 2016 tells us about 1.1 million Americans who were previously discouraged, ‘marginally attached,’ or working part-time when they didn’t want to … got the job they wanted. This is good news … however … if we subtract 4.7% (the official rate) from 9.2%, and then multiply the CLF by that percentage, we still have 7.2 million folks looking for a similar solution. We still have some distance to cover. But we’re moving in the right direction.

OK…once again, I’ve built up quite an appetite after lifting these heavy economic numbers. Shall we see how the Steak Houses are faring this week? This one might surprise you!

Here are the SHI charts for last week and today:

The first think you’ll notice is this week we have a positive 1 SHI reading. Great. But do you see anything else you find interesting?

YES! The Capital Grill is BOOKED AT 6:00 PM! Amazing! And you said it couldn’t happen! Hah! 🙂

Here’s our long-term trend report:

This SHI reading is the last metric we need to calculate the ‘Steak House Composite Index’ or SHCI.

You will recall our SHCI is a more comprehensive measure of the US economy. Beyond the SHI alone, which is designed to measure consumer spending, the SHCI weighs 3 components using a rigid, consistent methodology:

-

The SHI, as it taps directly into consumer spending, is weighted at 60%.

-

The LMCI, our labor market health barometer, is weighted at 20%.

-

The ’10/3 spread’ – a barometer of bond market confidence – will also be weighted at 20%. (However, to ‘right size’ the value in relation to the SHI and the LMCI, we will multiply a positive reading by 10X and a negative reading by 20X.)

As I said in the July 13th BLOG (https://terryliebman.wordpress.com/2016/07/13/steak-house-index-shci-update-7132016/) if all three of our metrics simultaneously achieved floor or peak values, the SHCI can range from a low of negative 22.1 to a positive 104. Here are today’s readings:

-

UST 10 Year/3 Month ‘spread’: Tracking the data, weekly ending Tuesday, our latest FRED reading (yesterday) is 1.90%. This reading is consistent with last month.

-

Labor Market Conditions Index: As discussed above, the LMCI released on Monday was a negative 0.3.

Our algorithm for the SHCI this month generates a reading of 11.44 – little changed from last month.

So, summarizing, 2017 begins, and a new US President takes office, on a solid economic foundation. The SHI and SHCI both reflect a consistent, medium-strength economy. We’ll continue to monitor developments and report changes as they occur.

Let the games begin!

1 Comment

Howdy very nice web site!! Guy .. Beautiful .. Amazing .. I will bookmark your site and take the feeds also…I’m glad to search out numerous useful information right here in the submit, we need develop extra techniques on this regard, thank you for sharing. . . . . .