SHI 11.29.23 – Sorting Thru The Tea Leaves

SHI 11.22.23 — Velocity: Money and Food

November 22, 2023

SHI 12.6.23 – ‘Tis the Season

December 6, 2023

Yes. Those are tea leaves.

Earlier today, two important economic reports came out.

First, the FED released their most recent Beige Book with comments on the current state of the US economy. The Bureau of Economic Analysis then added their “second” estimate of Q3, 2023 GDP growth. Interestingly, each tells a very different story about our economy today.

“

What’s up at the Steak Houses?”

“

What’s up at the Steak Houses?”

Restaurant reservations are also telling an interesting economic story today. And here is where we will start. At our expensive eateries.

Welcome to this week’s Steak House Index update.

If you are new to my blog, or you need a refresher on the SHI10, or its objective and methodology, I suggest you open and read the original BLOG: https://www.steakhouseindex.com/move-over-big-mac-index-here-comes-the-steak-house-index/

Why You Should Care: The US economy and US dollar are the bedrock of the world’s economy.

But is the US economy expanding or contracting?

Expanding … FED rate increases notwithstanding! At the end of Q3, 2023, in ‘current-dollar‘ terms, US annual economic output rose to an annualized rate of $27.64 trillion. America’s current-dollar GDP increased at an annualized rate of 8.9% during the third quarter of 2023. Even the ‘real’ GDP growth rate was hot… clocking in at the annual rate of 5.2% during Q3.

The world’s annual GDP first grew to over $100 trillion in 2022. According to the IMF, in June of this year, current-dollar global GDP eclipsed $105 trillion! IMF forecasts call for global GDP to reach almost $135 trillion by 2028 — an increase of more than 28% in just 5 years.

America’s GDP remains around 25% of all global GDP. Collectively, the US, the European Common Market, and China generate about 70% of the global economic output. These are the 3 big, global players. They bear close scrutiny.

The objective of this blog is singular.

It attempts to predict the direction of our GDP ahead of official economic releases. Historically, ‘personal consumption expenditures,’ or PCE, has been the largest component of US GDP growth — typically about 2/3 of all GDP growth. In fact, the majority of all GDP increases (or declines) usually results from (increases or decreases in) consumer spending. Consumer spending is clearly a critical financial metric. In all likelihood, the most important financial metric. The Steak House Index focuses right here … on the “consumer spending” metric. I intend the SHI10 is to be predictive, anticipating where the economy is going – not where it’s been.

Taking action: Keep up with this weekly BLOG update. Not only will we cover the SHI and SHI10, but we’ll explore “fun” items of economic importance. Hopefully you find the discussion fun, too.

If the SHI10 index moves appreciably -– either showing massive improvement or significant declines –- indicating growing economic strength or a potential recession, we’ll discuss possible actions at that time.

The Blog:

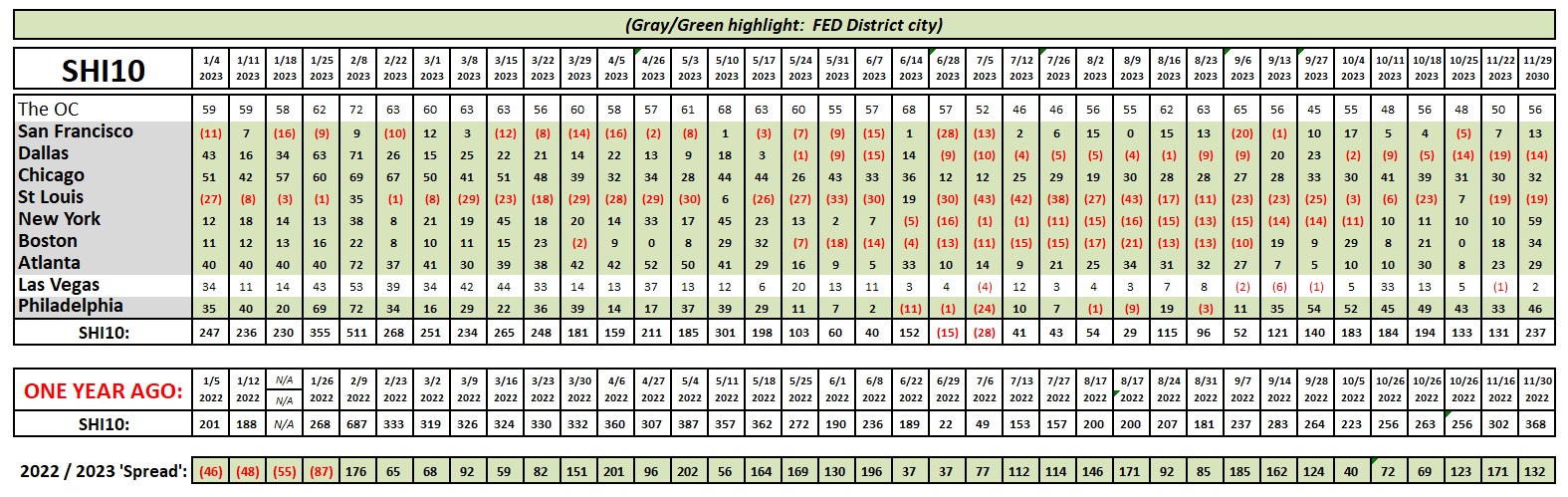

Here is today’s SHI40 trend analysis report:

Take a close look. You’ll see that reservation demand in “The OC” has been exceptionally consistent for the entire year. It’s the only SHI city with this experience. Every other city has ebbed … and flowed … and ebbed as the year unfolded. Not one of the other 9 cities have experienced the same result. Interesting.

Reservation demand at the most expensive restaurants in Philly started the year strong … then weakened mid-year … only to become strong once again in recent months. Then you have Las Vegas and Dallas. Two very different cities … with very similar SHI trajectories. Both began 2023 with strong restaurant reservation demand … and both have continuously softened during the year.

The ‘Vegas story might be easier to explain. One might surmise that as the “excess savings” balances continue to decline, Americans have less to spend, or are less willing to spend, on a ‘Vegas experience. Perhaps. The SHI certainly suggests this might be an explanation.

But how about Dallas? How did an early-January SHI reading of 43 slide all the way to a spate of negative readings over the past few weeks? Is Dallas still so excessively oil-price impacted that the decline in crude oil prices negatively impacted expensive eatery reservations?

Maybe. But the price of Crude Oil on the 1-year chart above really doesn’t correlate with that suggestion. So what’s the cause? Frankly, I couldn’t say. But Dallas expensive steak house reservation demand has softened week after week.

The widely divergent SHI readings across our ten markets is quite interesting. Clearly, as the SHI suggests, there are economic winners and losers across America. And today’s Beige Book reflects precisely the same theme.

According to the FED report, economic activity “was up slightly” in Chicago and Richmond, and only in Chicago and Richmond. In all other FED districts — 10 in all — the Beige Book described economic performance with words like contracted, down, slowed, decline, expanded slower, or softened.

And then, in complete contrast, today’s Gross Domestic Product report actually increased the Q3 reading up to a 5.2% ‘real’ growth rate and an absolutely sizzling ‘current-dollar’ GDP increase of 8.9% on an annualized basis. That is a staggering, red-hot achievement. It’s worth repeating.

CURRENT DOLLAR GDP GREW AT THE ANNUALIZED RATE OF 8.9% IN Q3.

Staggering.

But, I’m afraid to say, the most recent Beige Book suggests this outcome is unlikely to repeat in our current quarter. I would be shocked if Q4 results were even close. But the good news is this: GDP growth doesn’t have to be this strong again for the US economy to remain on solid footing.

Why is the Beige Book suggesting a slowing US economy while our economy in the GDP report is sizzling? That one is easier: Timing. Q3 was over on September 30th … and began on July 1st. Those economic results are far in the rear-view mirror. The Beige Book, on the other hand, is a very current survey.

The Q3 trajectory indicates the US economy is cooking. With gas. But clearly things are slowing. A bit. However, don’t let the naysayers convince you a recession is around the corner. It is not. Yes, the soaring rocket that has been the American economy is slowing … but that’s just fine. We’re good.

<:> Terry Liebman

{kind=link}

{kind=link}