SHI 6.3.26 – A Stairway to Heaven

SHI 5.27.26 – GENIUS or Dumb?

May 27, 2026

SHI 5.10.26 — Should YOU Build a Data Center?

June 10, 2026

Led Zeppelin released “Stairway to Heaven” in November of 1971 — 55 years ago. Wow.

When they penned the lyrics, could Led Zepplin have known they were writing a theme song for AI data centers? Hmmm ….

“There’s a lady who’s sure all that glitters is gold

And she’s buying a stairway to Heaven

When she gets there she knows, if the stores are all closed

With a word she can get what she came for

Ooh, ooh, and she’s buying a stairway to Heaven”

“

Let’s talk bubbles.“

“

Let’s talk bubbles.“

Years ago, a good friend named Bill recommended a book. Titled“Finite and Infinite Games,” I found the book fascinating. You can read the the 200 or so pages if you’re intrigued, but I’ll summarize the central theme for you: Finite games are played to win — the players, the rules, and how it ends are all known before the game begins.

Infinite games are played to continue the play. The purpose is not to win. The purpose is simply to play perpetually. Of course, sometimes infinite games change and become finite. And when that happens, the game objective changes, and the players, rules and ending become factual. But unless and until that occurs, the players simply play.

In the years since reading the book, I’ve found this framework helpful in business. If a business “activity” is finite, then I play to win. If it is a never-ending cycle, I take a very different approach. So, if the AI data center boom is a “finite game” then it’s important that we understand — right now — the players, rules and ending goal. But if the boom is truly infinite, and after building out (to the extent possible) data centers on earth and then “AI data centers in space” become a thing, then SpaceX and the hyperscalers actually are building a Stairway to Heaven. One that will stretch to the heavens, never ending, never stopping.

Which is it? Is the AI boom in data center construction finite? Or infinite? Will we someday see data centers, as Buzz Lightyear might quip, “To Infinity and Beyond!”

The distinction is important: If the “game” is finite, then there is an end. If infinite, the game never ends and we are all simply players. Which is it?

Let’s chat.

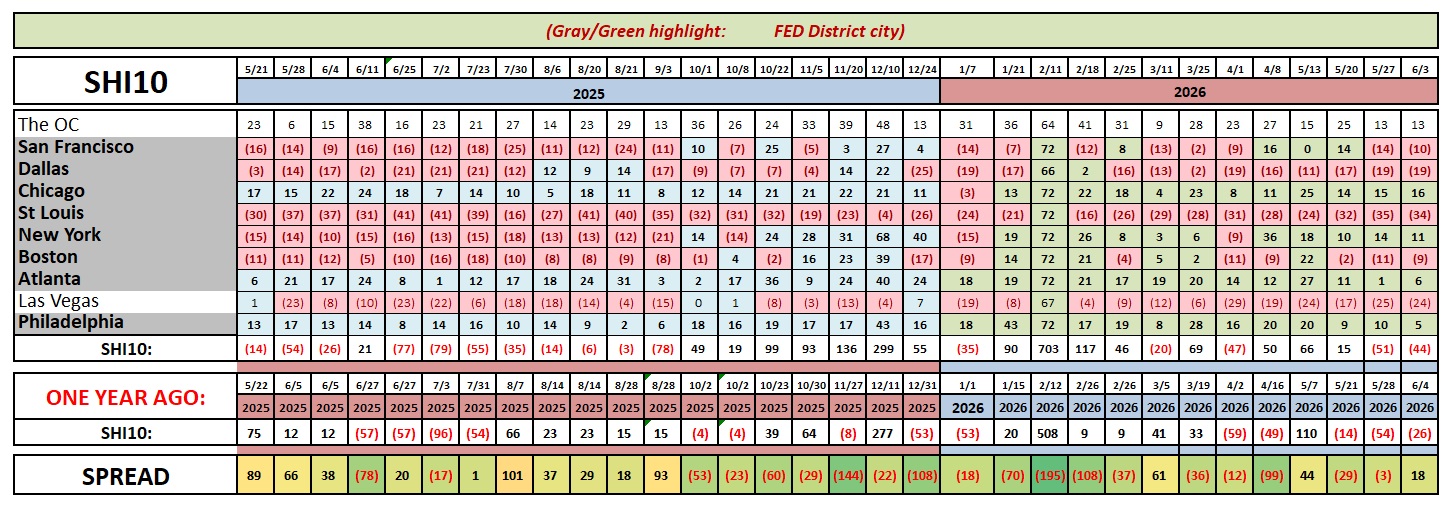

Welcome to this week’s Steak House Index update.

If you are new to my blog, or you need a refresher on the SHI10, or its objective and methodology, I suggest you open and read the original BLOG: https://www.steakhouseindex.com/move-over-big-mac-index-here-comes-the-steak-house-index/

Why You Should Care: The US economy and US dollar are the bedrock of the world’s economy. But is the US economy expanding or contracting?

Expanding … according the ‘advanced’ reading just released by the BEA, Q4, 2025 GDP grew — in ‘current-dollar‘ terms — at the annual rate of 5.1%.

The ‘real’ growth rate — the number most often touted in the mainstream media — was 1.40%. In current dollar terms, 2025 US annual economic output reached almost $31.50 trillion.

According to the IMF, the world’s annual GDP will expand to over $126 trillion in 2026. Of that amount, the US makes up over 25% — expected to reach $32.4 trillion by the end of 2026. Further, IMF expects global GDP to reach almost $135 trillion by 2028 — an increase of more than 28% in just 5 years.

America’s GDP remains around 25% of all global GDP. Just four countries—the United States, China, Germany, and Japan—generate roughly half of all economic activity worldwide. Collectively, the US, the European Common Market, and China generate about 70% of the global economic output. These are the 3 big, global players. They bear close scrutiny.

The objective of this blog is singular.

It attempts to predict the direction of our GDP ahead of official economic releases. Historically, ‘personal consumption expenditures,’ or PCE, has been the largest component of US GDP growth — typically about 2/3 of all GDP growth. In fact, the majority of all GDP increases (or declines) usually results from (increases or decreases in) consumer spending. Consumer spending is clearly a critical financial metric. In all likelihood, the most important financial metric. The Steak House Index focuses right here … on the “consumer spending” metric. I intend the SHI10 is to be predictive, anticipating where the economy is going – not where it’s been.

Taking action: Keep up with this weekly BLOG update. Not only will we cover the SHI and SHI10, but we’ll explore “fun” items of economic importance. Hopefully you find the discussion fun, too.

If the SHI10 index moves appreciably -– either showing massive improvement or significant declines –- indicating growing economic strength or a potential recession, we’ll discuss possible actions at that time.

The Blog:

There are days I feel like we’re watching the greatest game of “financial” musical chairs in history.

The AI spending numbers are staggering. The shift of resources to this market segment is unprecedented. The crowding-out of other, non-AI activities has also never happened before. I mean, try to find an electrical contractor to build your major commercial project today. Sure, you may find one, just expect the labor price to be 2X last year’s price. That assumes they can even find the electrical equipment to install in your new real estate project. And if you need a natural gas turbine for power generation, “behind-the-meter” at your new 1 gW AI data center, figure your going to wait for 3-5 years. Or longer.

Other days, watching the news, I think, “Hmmm….no, this is real. This AI boom is the most transformational event in human history.” We are truly building a stairway to heaven.

But both outcomes cannot be true. Either the AI boom in data center construction is a finite game, to borrow a phrase from the book; or, alternatively the AI data center boom is infinite. Never ending. To infinity and beyond?

Impossible. It must be, right? Which means this is a finite game. We know the players … but I’m struggling to understand the rules. And I don’t know about you, but I’m not sure what winning means.

But setting these concerns aside for the moment, I can envision how this game might end: A bottleneck caused by some macro-supply chain disruption. Think about it. I think the AI data center boom story has already morphed from “CAPITAL > LAND > APPROVALS > BUILDING > SERVERS/CHIPS” to “POWER (electric source) > POWER (components) > POWER (installation) > SERVERS/CHIPS. Apparently capital and land are no longer limitations. “Approval to build” might become the next limitation. Might this push future data centers into space? Hmmm ….

But power is a real hurdle today. Is this where the musical chairs game ends?

In a prior blog, I discussed the latest book by Andrew Ross Sorkin, “1929: Inside the Greatest Crash ….” It is a great read for any student of economics, finance and history. Sorkin is one of the talking-heads on CNBC, but recently he was interviewed on the show 60-Minutes, discussing his new book. When asked about parallels between today’s market and that of 1929, he commented,

“I think it’s hard to say we’re not in a bubble of some sort.”

He added: “I’m anxious that we are at prices that may not feel sustainable. And what I don’t know is we are either living through some kind of remarkable boom and part of that’s artificial intelligence and technology and all of that, or everything’s overpriced.”

I think Sorkin framed the issue perfectly. On one hand this could be a remarkable boom. On the other hand, the stock market could be overpriced. I think Sorkin would agree with the statement that both cannot co-exist, simultaneously, without end. Sure, we can certainly be inside a remarkable boom. I believe we are.

But as time passes, I fear that even if this is a remarkable boom the AI game must be finite. Remember: There are finite materials on earth. There is a finite supply of construction labor. There is finite capital, granted it’s a high bar these days. We definitely have finite power, although the hyperscalers have been extremely creative when solving this problem thus far. And finally, society has finite tolerance of the disruptive impacts from AI and the extraordinary allocation of resources to AI, away from and to the detriment of all other segments of society. Perhaps the game paradigm changes somewhat if near space becomes a realistic expansion arena for the AI hyperscalers. Certainly the upcoming SpaceX IPO believes that.

I simply wanted to introduce this thought exercise today. I will revisit this discussion with more data next week. But your take away from today is this:

While I believe AI is truly transformational, within the world of allocating capital and resources to the build-out of AI data centers, and away from other societal requirements, a crowding-out of sorts is growing. Supply chains are strained, a fact reflected in the parabolic price increases in many of the components required to build a data center, and this strain is becoming protracted. There is danger and froth out there. Be careful and thoughtful in your investment choices. Bubbles are forming.

Let’s head to the steakhouses where the only bubbles you’ll find are in the soft drinks!

Here’s the long-term chart. Yet again, not much has changed. I do find the trend in the OC to be kind of interesting. But, frankly, every SHI market is quite consistent at present.

Both the Atlanta FED and the NY FED forecasts for Q2 GDP growth remain quite robust. The FED Beige Book released earlier today highlighted the fact that “business investment” remains strong. AI data centers are business investments. Several of the FED districts reported that data-center construction is showing robust growth, and demand for steel, electrical equipment, power infrastructure, and transportation services are strong. Finally electricity demand was described as “insatiable” due in part to data-center expansion.

These are amazing times.

< Terry Liebman >