Back From the Grave!

Steak House Index UPDATE 6/29/16

June 29, 2016Nowcasting Update: July 1, 2106

July 1, 2016

Mark Twain was rumored to have become gravely ill while traveling in London in 1897.

The rumor spread rapidly across America and, according to legend, one US newspaper reported that he had died. When a reporter finally reached Twain for a comment, Twain supposedly replied, “The reports of my death are greatly exaggerated.”

I suppose we could say the same about home equity lines of credit, or HELOCs.

Why you should care: Simple: The HELOC is a great tool for money management. HELOC rates are quite low. Much lower than other types of debt (credit cards, auto loans, etc.), and judicious debt management is something we should all attempt.

Taking action: Explore your options…and get one!

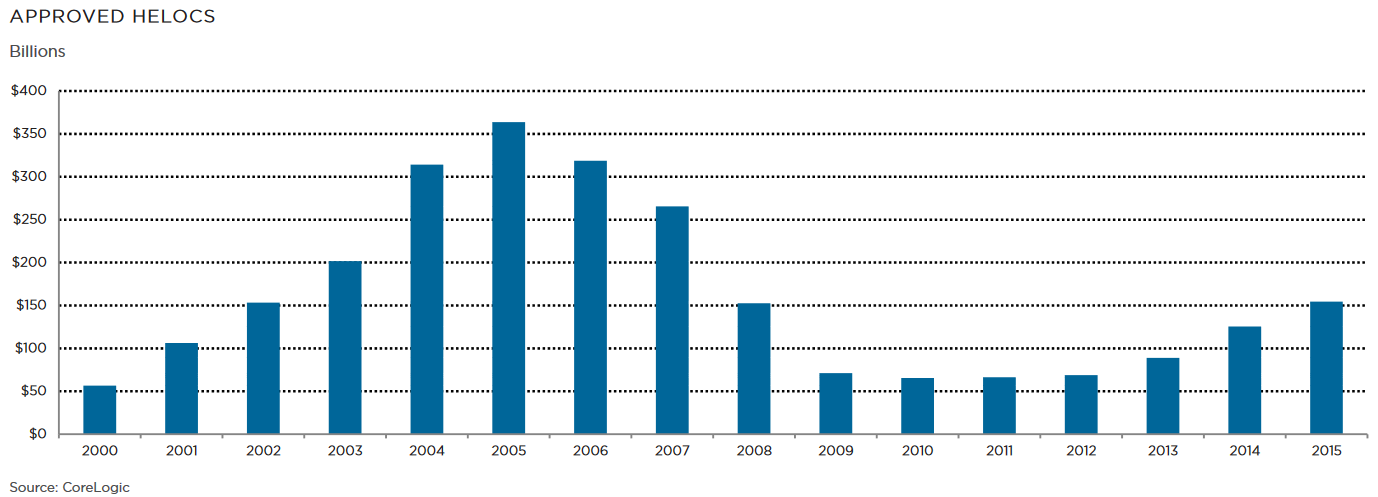

The BLOG: HELOCs are back! According to CoreLogic:

“During the first three quarters of 2015, lenders originated nearly 976,000 new home equity lines of credit (HELOCs) with combined limits in excess of $115.8 billion. Both of these figures were the highest for the January-through-September period since 2008 and represented year-over-year gains of 21 percent and 31 percent, respectively.”

Annualizing this number suggests HELOC origination exceeded $150 billion in 2015. Impressive. Because both borrower demand and lender willingness were almost, well, moribund in the past 5 or so years.

Of course, lenders today use very conservative underwriting standards. Combined loan-to-values (CLTV) are quite low…so the homeowner needs a bunch more equity than, say, back in 2005.

But equity is growing. Rapidly. Which suggests HELOC use will do the same in the years to come.

In their report, Corelogic opined that the “average interest rate on outstanding mortgage debt is now 3.8%” and, as a result, these low rates may change homeowner behavior somewhat. I agree. We’re already seeing this play out in the lower “for sale” inventories across the nation. Many homeowners are staying put.

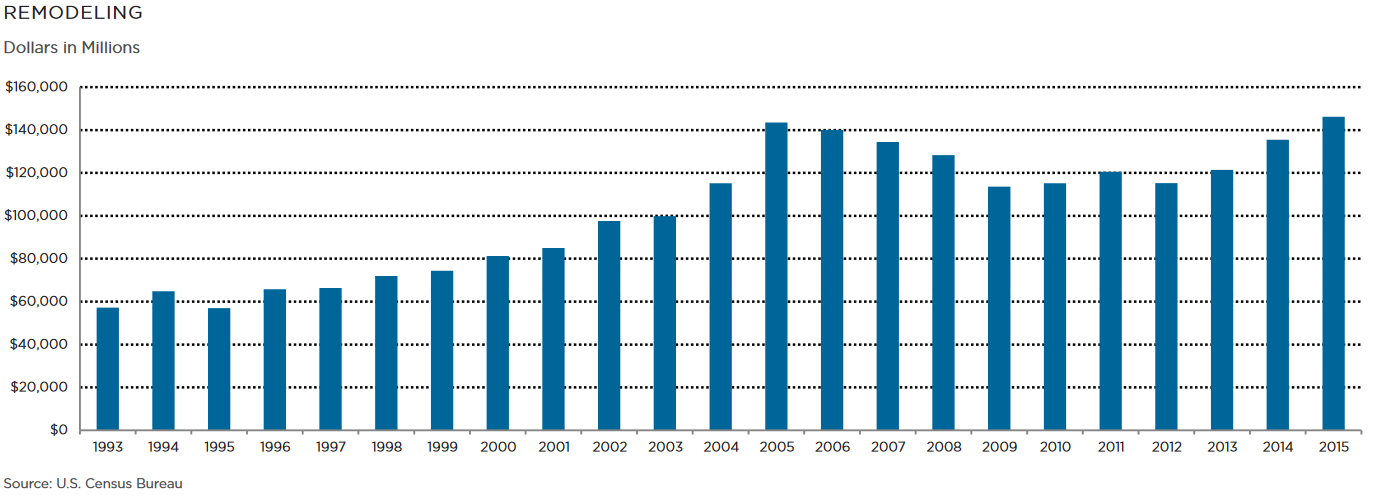

So what are HELOC funds being use for? Well, apparently many folks are deciding that if they’re going to stay put, they’re going to fix up the ole homestead!

Per CoreLogic and the US Census Bureau, home remodeling is at an all time high. About $150 billion in 2015.

In closing, let me make two suggestions: First, investigate HELOCs at your bank. Rates are low…timing might be right. Second, do what I did: buy Home Depot (NYSE: HD). Their stock price is down a bit…it has a nice dividend…and – who knows! – if the trend continues, and more people do more home improvements, it could be a nice little investment!

- Terry Liebman

2 Comments

The core of your writing while sounding agreeable at first, did not really settle well with me after some time. Someplace throughout the paragraphs you actually managed to make me a believer unfortunately only for a while. I however have a problem with your leaps in assumptions and one might do nicely to fill in those breaks. In the event you can accomplish that, I will certainly be fascinated.

A round of applause for your blog post.Thanks Again. Much obliged.