SHI 9/13/17: Inflation Accelerates!

SHI 9/6/17: Housing Redux

September 6, 2017

SHI 9/20/17: The Great, Golden State

September 20, 2017

The inflation rate is rising quickly, surprising economists.

No, no… not here in the US. Across the pond — in the UK. Just as I predicted in my October 15, 2016 SHI update. Take a look: https://www.steakhouseindex.com/this-just-got-real-and-by-real-i-mean-real-bad/

Here is a quote from that blog: “The UK is now importing inflation on a grand scale. The voters should have been warned. And this is just the beginning … if the pound continues to depreciate, <inflation> is going to get a lot worse.”

Ironically, the only thing that surprises me is the fact that many economists were surprised. 🙂

Economics can be quite opaque at times. This is not one of those times. If a country imports much of what it consumes, and its currency devalues against the currency of its trading partners, that country’s economy will experience a significant lift in its inflation rate. Simple.

Could this same thing happen here in the US?

Welcome to this week’s Steak House Index update.

If you are new to my blog, or you need a refresher on the SHI, or its objective and methodology, I suggest you open and read the original BLOG: https://www.steakhouseindex.com/move-over-big-mac-index-here-comes-the-steak-house-index/

Why You Should Care: The US economy and US dollar are the bedrock of the world’s economy. At present, is the US economy expanding or contracting? We need to know.

The world’s GDP is about $76 trillion. At last count, our ‘current dollar’ US GDP is now over $19 trillion — about 25% of the total. No other country is even close.

The objective of the SHI is simple: To help us predict US GDP movement ahead of official economic releases — important since BEA data is outdated the day they release it.

‘Personal consumption expenditures,’ or PCE, is the single largest component of US GDP — about 2/3 of the total. In fact, the majority of all US GDP increases (or declines) usually result from (increases or decreases in) consumer spending. Thus, this is clearly an important metric to track. The Steak House Index focuses right here … right on the “consumer spending” metric.

I intend the SHI is to be predictive, anticipating where the economy is going – not where it’s been. Thereby giving us the ability to take action early.

Taking action: Keep up with this weekly BLOG update.

If the SHI index moves appreciably -– either showing massive improvement or significant declines –- indicating expanding economic strength or a potential recession, we’ll discuss possible actions at that time.

The BLOG:

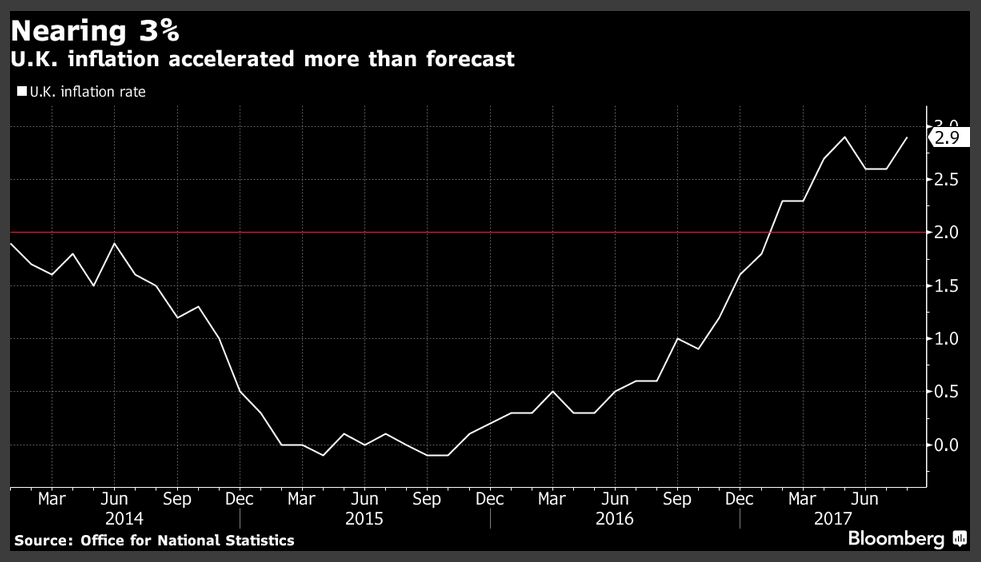

Per a Bloomberg article written yesterday, UK inflation accelerated “more than forecast” during August. The English pound value-slide is the culprit: The pound has fallen 11% against the dollar, and 14% against a “trade-weighted” metric, since the Brexit vote. Imports into the UK are much more expensive today. Per Bloomberg, “The inflation pickup in August was led by clothing and footwear, which surged 4.6 percent compared with a year earlier.” I am not surprised in the least.

By August of 2017, the UK inflation rate rapidly approached the 3% level:

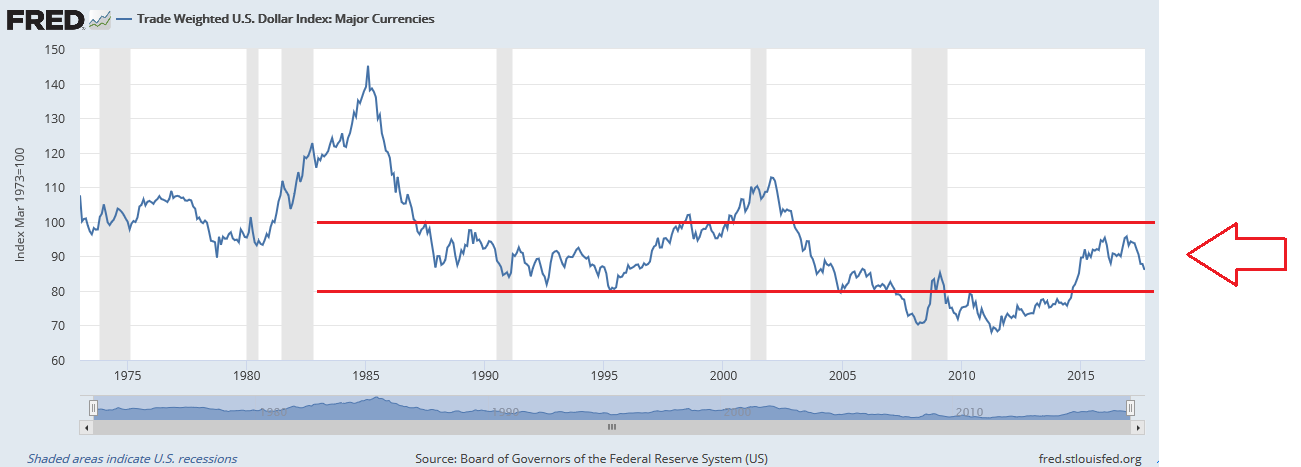

Here is something I didn’t see coming: This year, the US dollar — when compared to the currencies of countries we trade with — has also weakened significantly. Since January 2nd, the “trade weighted” US dollar has fallen more than 10%!

When asked to explain this huge decline, economists have been quick to chime in:

- Uncertainty over the US debt limit;

- North Korea;

- Declining long-term rates on Treasuries; and,

- The diminishing likelihood the FED will raise rates again in 2017.

None of which is completely on point. The true answer rests within a longer-term viewpoint. The fact is the US dollar was extremely strong — measured against other currencies — when our interest rates peaked in the 1980s. Remember: At no time in the 250-year history of the US have interest rates ever been higher than in the 1980s. Never.

Since around 1990 — the “dot-com” boom and the “Great Recession” periods being exceptions, the USD has been range-bound, as it remains today:

What’s odd about this year’s decline in the “trade weighted” dollar, however, is that its happening at all. Currencies always fluctuate. And their values, when measured against other currencies, is often a reflection of the perceived relative economic strength of that economy. Interest rates play a big part, too.

So when we look at this 10% dollar value decline through the ‘investor lens’ of US economic strength and interest rate levels — vs. those of our trading partners — one would expect the value of the dollar to be high. Yet it is not. What does this tell us?

Simply this: Investors around the world (1) expect the US economy to remain somewhat weak, when compared to other developed nations; and, (2) expect the general level of US interest rates to remain low, or continue lower.

Which seems a bit odd to me since (1) most developed nation economies are certainly no stronger that ours and (2) the general level of their interest rates are much lower than ours. Take Italy, for example. Their economy remains is in very sad shape. Yet rates on Italian bonds are much lower than those on equivalent US bonds. It’s a crazy conundrum, likely caused by the ECB debt-purchase program.

No, more likely, the decline in the value of the dollar is related to changing investor expectations: As the year progresses, it seems more likely the FED will not raise rates again this year, and the highly anticipated US infrastructure and new corporate tax revisions have become unlikely as well. Investors appear to be voting “no confidence” in the Trump administration’s ability to break Washington grid-lock.

No currency discussion would be complete without a quick glance at the SHIs inspiration, the Big Mac Index. Open this link: http://www.economist.com/content/big-mac-index. The interactive graphic permits you to change the ‘base currency’ for comparison purposes. Give it a try. Substituting the euro for the US dollar, according to the Big Mac Index, the US dollar is still over-valued by 18.7%. and suggests the “implied exchange rate” is 1.36 dollars per euro. Hmmm … interesting.

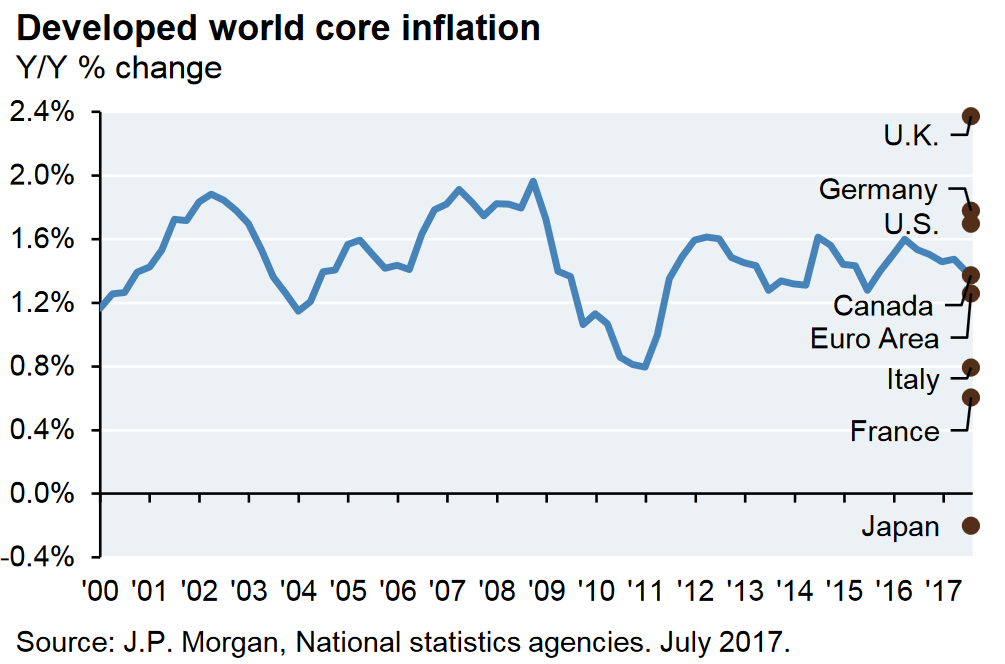

Beyond the UK, inflation in developed nation economies is tame. Here’s a great picture courtesy of JP Morgan:

Did you notice “core inflation” in Japan is negative? That’s another way of saying Japan’s economy remains in a deflationary state. Ouch. Not good. The economies of France, Italy, and the rest of the Euro area are close to a deflationary condition as well.

Like me, JP Morgan believes central banks are in no hurry to shrink their balance sheets:

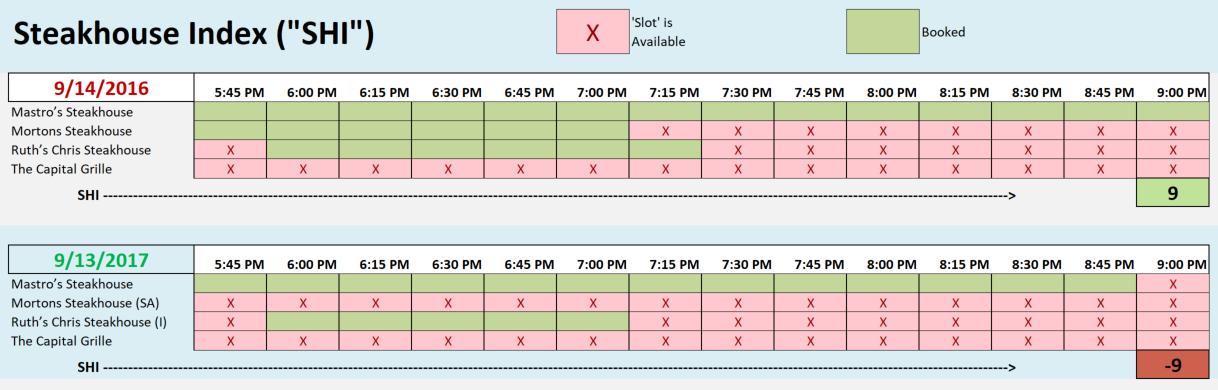

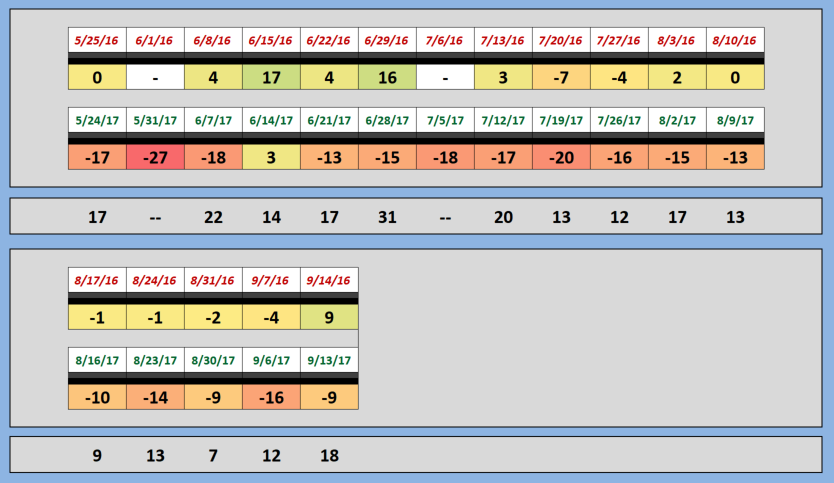

Ruths’ Chris has seen a small surge in popularity; but, our other two high-dollar steakhouses are completely available. This is quite different than a year ago when Mortons was booked until 7:00 pm. The long-term trend continues:

Last week, I commented, “If, for example, the contribution from PCE slides from the 2.3% Q2 rate to, say, 1.3% in Q3 — and assuming the contribution from all other components remains unchanged — our Q3 GDP growth rate will slip to an annual rate of 2.0%.”

Clearly, I was attributing an ‘average’ GDP reading resulting from PCE weakness. Unfortunately — at least for the SHI — this calculation has become more complicated.

Recently, as we all know, the US was struck by two record-setting hurricanes. Rainfall in Texas and wind in Florida have both wreaked devastation and havoc; Moody’s has estimated the damage/cost of both storms will range between $150 and $200 billion. Staggering. Goldman Sachs, as a result, has changed their Q3 GDP forecast to 2.0%. Economists at Moody’s and a number of other firms have also dramatically lowered their forecasts.

The cost of these storms in human suffering is incalculable. I wish everyone affected the best possible luck and a speedy recover.

- Terry Liebman