SHI 10.7.2020: Who’s Buying the Toilet Paper?

SHI 9.30.20: The Recession is Over!

September 30, 2020

SHI 10.14.20: How to Spend $2.2 Trillion

October 14, 2020

It was bound to happen: As the pandemic-inspired “work from home” movement grows long in the tooth, with no end in sight, questions are growing over costs that were previously borne by the employer at the office. Workers all over the world have been personally covering many of these costs for the past 6 months or so. So now it’s an issue. The debate over who pays for extra home utilities, office equipment, and printer supplies may be easier to settle … but who pays for coffee, tea and toilet paper when the office sends everyone home?

And you thought the SteakhouseIndex.com only delved deep into financial and economic questions. Hah!

“

Toilet paper? Who cares?”

“Toilet paper? Who cares?”

You should. Because it turns out our ‘who pays for toilet paper question’ does have meaningful financial and economic implications. For all of us.

Welcome to this week’s Steak House Index update.

If you are new to my blog, or you need a refresher on the SHI10, or its objective and methodology, I suggest you open and read the original BLOG: https://www.steakhouseindex.com/move-over-big-mac-index-here-comes-the-steak-house-index/

Why You Should Care: The US economy and US dollar are the bedrock of the world’s economy.

But is the US economy expanding or contracting?

Before COVID-19, the world’s annual GDP was about $85 trillion. No longer. It shrank. Until recently, annual US GDP exceeded $21.7 trillion. Again, no longer. According the the Q2 final numbers, annual US GDP is down to $19.5 trillion. We can thank the Great Lockdown for this one. But what has not changed is the fact that together, the U.S., the EU and China still generate about 70% of the global economic output.

The objective of this blog is singular.

It attempts to predict the direction of our GDP ahead of official economic releases. Historically, ‘personal consumption expenditures,’ or PCE, has been the largest component of US GDP growth — typically about 2/3 of all GDP growth. In fact, the majority of all GDP increases (or declines) usually results from (increases or decreases in) consumer spending. Consumer spending is clearly a critical financial metric. In all likelihood, the most important financial metric. The Steak House Index focuses right here … on the “consumer spending” metric. I intend the SHI10 is to be predictive, anticipating where the economy is going – not where it’s been.

Taking action: Keep up with this weekly BLOG update. Not only will we cover the SHI and SHI10, but we’ll explore related items of economic importance.

If the SHI10 index moves appreciably -– either showing massive improvement or significant declines –- indicating growing economic strength or a potential recession, we’ll discuss possible actions at that time.

The BLOG:

Working remotely. It began as short-term solution to keep workers working, and the economy humming, after the Great Lockdown began at the end of Q1, 2020. And leave it to the Dutch to first come to grips with the challenges this trend has created — at least for the Dutch households under their purview. Who pays in the Netherlands? The boss, they’ve decided.

Enter the National Institute for Family Financial Information, better known as “NIBUD“, in the Netherlands. Consider coffee and tea: “We have literally calculated down to how many teaspoons there are in an average household, so from there it’s not that difficult to establish the costs,” said Gabrielle Bettonville of NIBUD, who has researched the extra costs of remote working. NIBUD research has resulted in many Dutch companies offering each employee a 363 euro “COVID-19 work-from-home-bonus” for 2020. Effectively, NIBUD says, this translates to about 2 euro per day for the “average worker with average costs,” but is not intended to cover the specific costs of new home furniture or equipment, which NIBUD suggests each employee should take up with their boss.

The Netherlands is not alone in deciding to tackle this issue:

This all makes sense given the exigent conditions resulting from the Great Lockdown. Generally, I suspect, we would all agree the employee should not be burdened by the extra costs thrust upon them by the pandemic. Which brings us to our economic and financial issue of the day:

Who should pay the costs resulting from the mandatory shutdowns?

Isn’t this really the question we’re all asking, about so many money issues, all over the world? Should restaurant owners bear the huge “close/open/close/open” costs caused from the government mandated shutdown? Should the COVID-19 unemployed bear their burden alone? Should the apartment landlord bear the cost of unpaid rents? And what about the airlines? Who should cover their costs?

How about the San Francisco office building owner who’s vacant office space is not being leased? According to city real estate services firms, only 15% of the offices actually leased right now had people working in them last month. Which means all the local vendors and suppliers, who rely on office workers streaming into the city every day, aren’t selling their wares. The Golden Gate Restaurant Association estimates that half the city’s 3,900 restaurants are likely to fail, and go out of business, because of the shutdown. So it comes as no surprise that San Francisco office rents have fallen 4% since the end of March — and one consultant believes office rents may fall as much as 20%, a direct result of the remote working trend.

Who’s gonna pay for that?

The list goes on … and on … and on. And the answers, unfortunately, are much more elusive.

As the pandemic-inspired shutdowns ebb and flow, the impacts and implications reverberate around the globe. There are certainly some financial winners. Many companies are thriving under the “stay at home” trade. But many more are losing the battle. On a related topic, I am amazed at how resilient global supply chains have proven to be: After all, grocery stores still have toilet paper and cans of peas on the shelf every time I shop these days. And while there was a brief scare, a month or two ago, about an egg shortage, that appears to be a thing of the past, too. The majority of our ‘consumer goods’ supply chains are seemingly built from the strongest of iron.

This wasn’t always the case. About a century and a half ago, when gold was first discovered in California, the small hamlet of San Francisco exploded almost overnight from only 800 hearty souls to over 200,000 within just a few years. As a result, chicken eggs became so scarce the price rose up to $1.00 apiece, the equivalent of $30 today. For one egg! The situation became so dire that grocery stores started placing “egg wanted” advertisements in newspapers. An 1857 advertisement in The Sonoma County Journal read: “Wanted. Butter and Eggs for which the highest price will be paid.” Supply chains have come a long way since the 1850s. Fortunately.

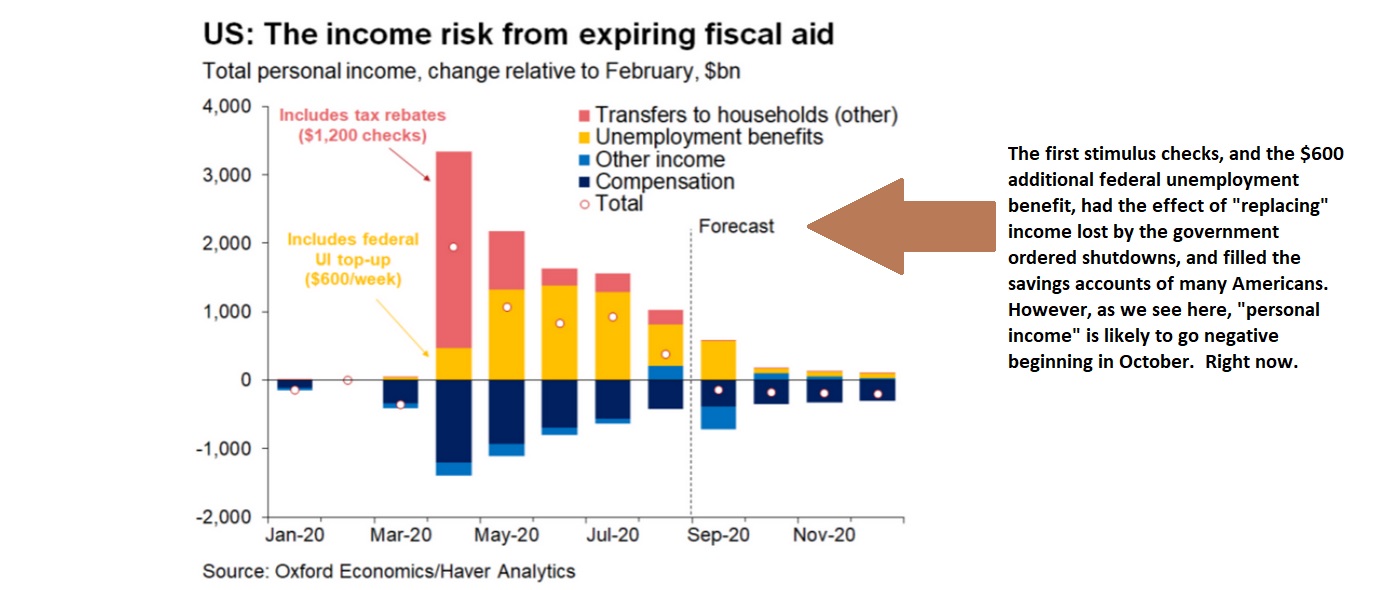

But the questions over COVID-19 costs remain and the participants in this complex equation are all looking for answers — and some help. Which is why the stimulus bills on the docket here in the US and around the world are both so important and so contentious — ignoring the politics for the moment. The question of who should pay remains the biggest of them all. But without further government fiscal stimulus — here and abroad — we all know who will bear the burden: Small businesses and the unemployed. You know it. I know it. And the FED knows it. Again yesterday, Chairman Powell reiterated his call upon US legislators for more fiscal stimulus aimed at supporting those most vulnerable, stating that the “burdens of this crisis” have been disproportionately distributed. Powell added, “The US federal budget is on an unsustainable path, has been for some time. But this is not the time to give priority to those concerns.”

It may surprise you, but I agree with Powell. Earlier stimulus programs fueled a huge ‘savings’ increase, replacing many months of lost income. (See my blog post from 8.26.2020: https://steakhouseindex.com/shi-8-26-20-halleys-comet/). But the savings will eventually run out:

In last week’s blog I declared the recession to be over. I believe it is. But this statement belies the fact that while the US economy may be expanding once again, the expansion will not be evenly felt or experienced. As Powell said above, the burdens of this crisis have not been distributed equally. Job losses have been concentrated in the lowest of the ‘low-wage sectors’ in our economy. Many of those unfortunates remain unemployed today, in most cases not due to any fault of their own. In the macro, at the highest levels, our economic expansion will continue. But for this group of unfortunates, current conditions will feel more like a depression than an economic recovery.

It is not the time to negotiate the price of water when your pants are on fire. Quickly use the water to put out the fire first. Negotiate how to pay for it later.

- Terry Liebman