SHI 12.12.18 – The Wealth Effect

SHI 12.5.18 – Inversion Aversion

December 5, 2018

SHI 12.19.18 – Spend Like There’s No Tomorrow

December 19, 2018

“Sir, the market price on the tomahawk is $189 … how would you like that prepared? ”

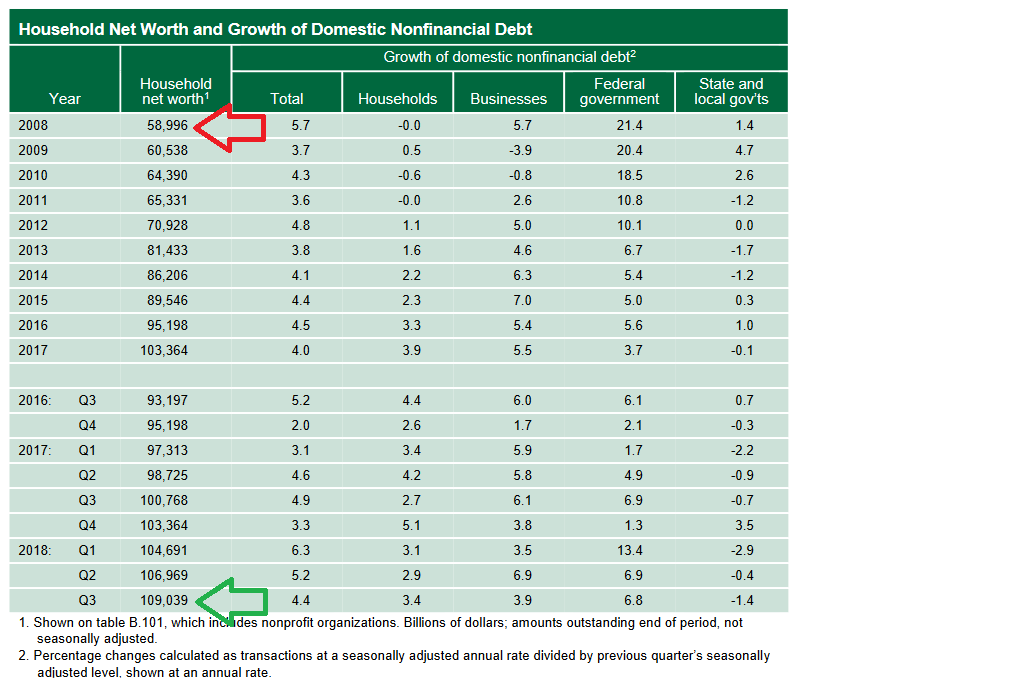

We’re rich! Maybe not you … and perhaps not me … but America is! Back in 2008, at the bottom of the “great recession,” U.S. household net worth was just under $59 trillion, according to the Federal Reserve’s “Financial Accounts of the United States” report known as the ‘Z.1.’ At the end of Q-3, 2018, that number had almost doubled — to over $109 trillion!

I’m sure our expensive steakhouses are pleased by this fact. Every day, they do their best to transfer some of that wealth into their cash registers.

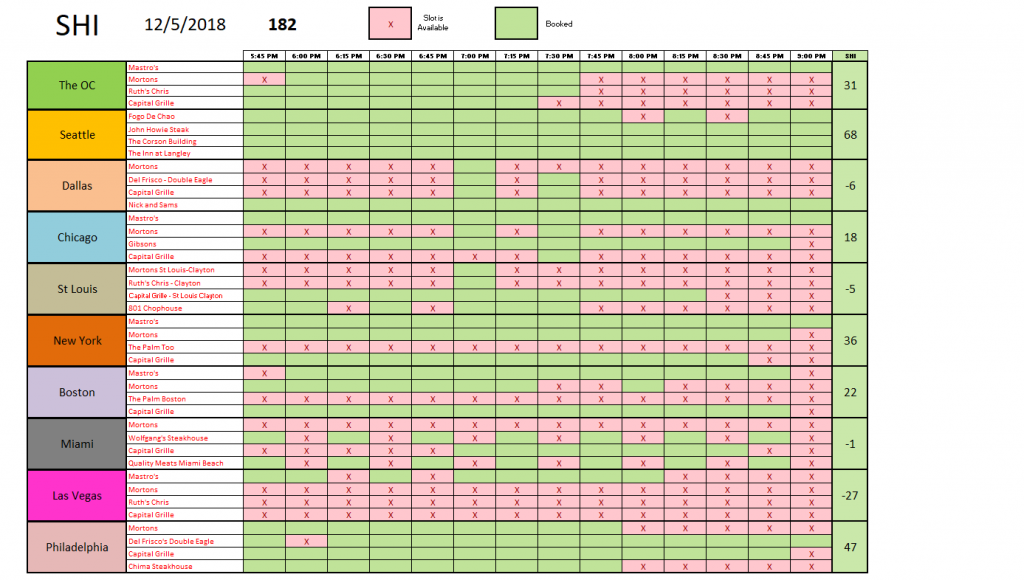

Welcome to this week’s Steak House Index update.

If you are new to my blog, or you need a refresher on the SHI10, or its objective and methodology, I suggest you open and read the original BLOG: https://www.steakhouseindex.com/move-over-big-mac-index-here-comes-the-steak-house-index/

Why You Should Care: The US economy and US dollar are the bedrock of the world’s economy. This has been the case for decades … and will continue to be true for years to come.

Is the US economy expanding or contracting?

According to the IMF (the ‘International Monetary Fund’), the world’s annual GDP is about $80 trillion today. US ‘current dollar’ GDP now exceeds $20.66 trillion. In Q3 of 2018, nominal GDP grew by 4.9%. We remain about 25% of global GDP. Other than China — a distant second at around $11 trillion — the GDP of no other country is close.

The objective of the SHI10 and this blog is simple: To predict US GDP movement ahead of official economic releases — an important objective since BEA (the ‘Bureau of Economic Analysis’) gross domestic product data is outdated the day it’s released. Historically, ‘personal consumption expenditures,’ or PCE, has been the largest component of US GDP growth — typically about 2/3 of all GDP growth. In fact, the majority of all GDP increases (or declines) usually results from (increases or decreases in) consumer spending. Consumer spending is clearly a critical financial metric. In all likelihood, the most important financial metric. The Steak House Index focuses right here … on the “consumer spending” metric. I intend the SHI10 is to be predictive, anticipating where the economy is going – not where it’s been.

Taking action: Keep up with this weekly BLOG update. Not only will we cover the SHI and SHI10, but we’ll explore related items of economic importance.

If the SHI10 index moves appreciably -– either showing massive improvement or significant declines –- indicating growing economic strength or a potential recession, we’ll discuss possible actions at that time.

The BLOG:

In only 10 years, America’s net worth has just about doubled. This is unprecedented. Of course, that number took a big hit in 2008. Net worth declined by $10 billion from 2006 to 2008. This aside, the net worth growth since 2008 is staggering.

Of course, detractors would make two comments. First, the net worth gains have mostly filled the coffers of Americans who were rich already. The vast majority of Americans are no wealthier today than they were 10 years ago. And so while rich folks have become richer, most American’s have not. Most Americans still live pay-check to pay-check.

And second, they would likely tell you the assets on the balance sheet are significantly over-valued. The would probably add that protracted ultra-low FED short-term rates since 2009 have likely caused a bubble in asset values.

Here’s a summary of the Z.1 report:

Perhaps both statements are true. But I take exception with the second. Essentially, this claim suggests asset values are inversely correlated with interest rates. And since interest rates have been abnormally low for about a decade, asset values have ballooned … likely into bubble territory. My long-time readers already know I simply don’t believe current levels of interest rates are temporary or aberrational. In fact, I believe the opposite is true: The rates the U.S. experienced from 1980 thru 2000 were aberrational. Today’s rates, while perhaps a bit on the low side of normal, or ‘neutral’, are more representative of normal. My opinion. Time will tell.

One clear winner in all this, however, are the opulent steakhouses we’re watching each week in the SteakHouse Index. The ‘Wealth Effect’ is clear and present: When folks are feeling flush, they will spend. And the opposite is true as well.

Let’s see how the steakhouses are doing this week.

It’s starting to look a lot like Christmas! Check out these numbers!

We haven’t seen an SHI10 number this high since Mother’s Day back in February. Without exception, each of the 10 marketplaces has experienced significant increased reservation demand this Saturday. Even the vegans in Miami are making an exception this weekend! 🙂

Is this huge increase in the SHI10 a reflection of seasonality … the Wealth Effect … or strong consumer confidence? (Here’s a recent comment on ‘consumer confidence’ from the Conference Board: “Despite a small decline in November, Consumer Confidence remains at historically strong levels,” said Lynn Franco, Senior Director of Economic Indicators at The Conference Board. “Consumers’ assessment of current conditions increased slightly, with job growth the main driver of improvement. Expectations, on the other hand, weakened somewhat in November, primarily due to a less optimistic view of future business conditions and personal income prospects. Overall, consumers are still quite confident that economic growth will continue at a solid pace into early 2019. “)

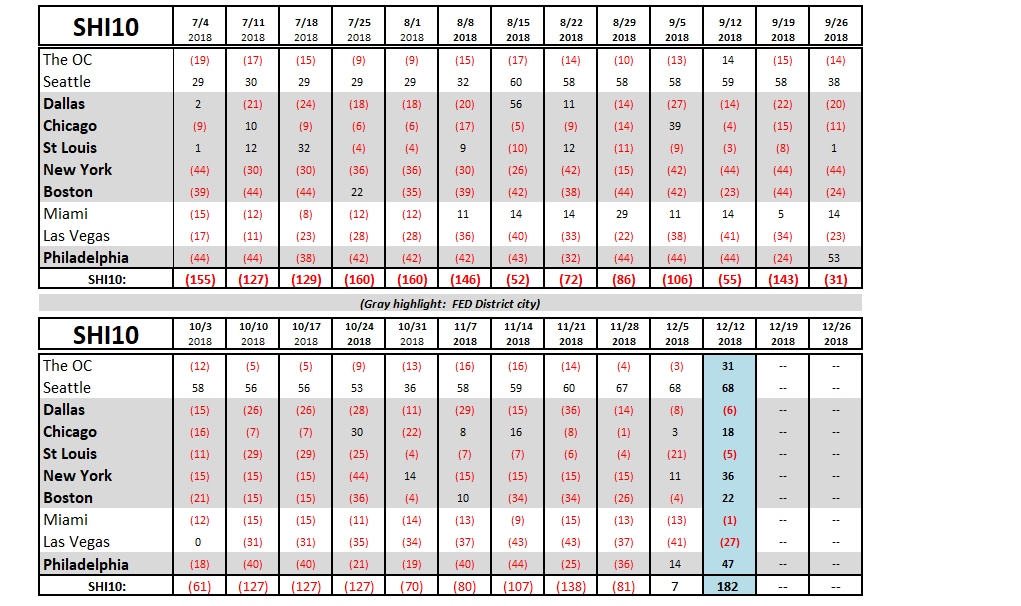

Or perhaps all 3? That would be my guess. This December, the U.S. economic engine is firing on all cylinders. Here’s our longer term trend:

Clearly a reading of 182 is WAAAAY above anything we’ve seen in months. Happy Holidays, Mastros!

- Terry Liebman