SHI 2.27.19 – Crosscurrents and Conflicting Signals

SHI 2.20.19 – Forget GDP … America Should Measure GNH!

February 20, 2019

SHI 3.6.19 – Gross Domestic Product

March 6, 2019

“While we view current economic conditions as healthy and the economic outlook as favorable, over the past few months we have seen some crosscurrents and conflicting signals…”

… said FED Chairman Powell speaking to Congress early Tuesday morning. “Crosscurrents?” “Conflicting signals?” Hmmm……….

Welcome to this week’s Steak House Index update.

If you are new to my blog, or you need a refresher on the SHI10, or its objective and methodology, I suggest you open and read the original BLOG: https://www.steakhouseindex.com/move-over-big-mac-index-here-comes-the-steak-house-index/

Why You Should Care: The US economy and US dollar are the bedrock of the world’s economy. This has been the case for decades … and will continue to be true for years to come.

Is the US economy expanding or contracting?

According to the IMF (the ‘International Monetary Fund’), the world’s annual GDP is about $80 trillion today. US ‘current dollar’ GDP now exceeds $20.66 trillion. In Q3 of 2018, nominal GDP grew by 4.9%. We remain about 25% of global GDP. Other than China — a distant second at around $12 trillion — the GDP of no other country is close.

The objective of the SHI10 and this blog is simple: To predict US GDP movement ahead of official economic releases — an important objective since BEA (the ‘Bureau of Economic Analysis’) gross domestic product data is outdated the day it’s released. Historically, ‘personal consumption expenditures,’ or PCE, has been the largest component of US GDP growth — typically about 2/3 of all GDP growth. In fact, the majority of all GDP increases (or declines) usually results from (increases or decreases in) consumer spending. Consumer spending is clearly a critical financial metric. In all likelihood, the most important financial metric. The Steak House Index focuses right here … on the “consumer spending” metric. I intend the SHI10 is to be predictive, anticipating where the economy is going – not where it’s been.

Taking action: Keep up with this weekly BLOG update. Not only will we cover the SHI and SHI10, but we’ll explore related items of economic importance.

If the SHI10 index moves appreciably -– either showing massive improvement or significant declines –- indicating growing economic strength or a potential recession, we’ll discuss possible actions at that time.

The BLOG:

Comedic actor Will Rogers had a quip I enjoy: “If you don’t like the weather in Oklahoma, wait a minute. It’ll change.”

FED policy seems to be following the same trajectory these days. Wait a minute … policy will change. Just like the weather. It wasn’t that long ago — December of 2018, in fact — that the FED raised interest rates. And, of course, just weeks ago, the FED became ‘patient’ … no longer following a pre-set pattern of rate increases. And now, just days later, our economy is facing crosscurrents. Gad-ZOOKS! What’s next? Rate cuts?

With Ben Bernanke at the helm, the FED became much more transparent. The idea was that if financial markets understood current FED philosophy, this understanding would foster more behavioral consistency and, ultimately, greater financial stability. Which is the FEDs mandate. Stability.

Well, transparency is one thing. Sea-sawing from ‘quantitative easing’ to ‘quantitative tightening,’ then neutral, and then possibly more easing in a few short months is … well … not very stable! One would surmise that with the mountains of high-quality financial and economic data at their fingertips, and an army of financial wizards and analysts pouring over that data, they would have a better grasp on current conditions. To me, frankly, their behavior appears exceptionally cavalier. My opinion.

Interestingly enough, consumers don’t appear to be feeling the same crosscurrents. At the same time the FED is growing concerned about economic headwinds, the consumer appears to be more confident — less worried — about the future.

The Conference Board Consumer Confidence Index® increased in February to an index reading of 131.4 (1985=100), up from 121.7 in January. That’s a big move.

Another index tracked by the Conference Board — the ‘Expectations Index‘ — increased at an even faster clip: Up from 89.4 last month to 103.4 this month. (This index is based on consumers’ short-term outlook for income, business and labor market conditions.)

“Consumer Confidence rebounded in February, following three months of consecutive declines,” said Lynn Franco, Senior Director of Economic Indicators at The Conference Board. “The Present Situation Index improved, as consumers continue to view both business and labor market conditions favorably. Looking ahead, consumers expect the economy to continue expanding.”

And so it would appear the FEDs expectations are in conflict with the consumer’s. Interesting, right? Why is this, you might ask?

The consumer, unfortunately, is often the last to feel a slowing economy. The financial markets tend to anticipate a slow-down first; the FED and economists seem to have a pretty good finger on the pulse; and the consumer, unfortunately, is often side-swiped by crosscurrents toward the “end of the beginning” (paraphrasing Mr. Churchill) of a recession. Consumer expectations tend to be a ‘lagging indicator.’ Which is why the Steakhouse Index is so important. If the FED is concerned about the economy, and the financial markets are showing fear and stress, we must monitor our ultimate lagging index — the consumer — the gauge how bad things really might become. As long as the consumer is happy … we’re probably in pretty good shape. And the consumer is happy. Maybe not as happy as the folks in Bhutan. But happy nonetheless!

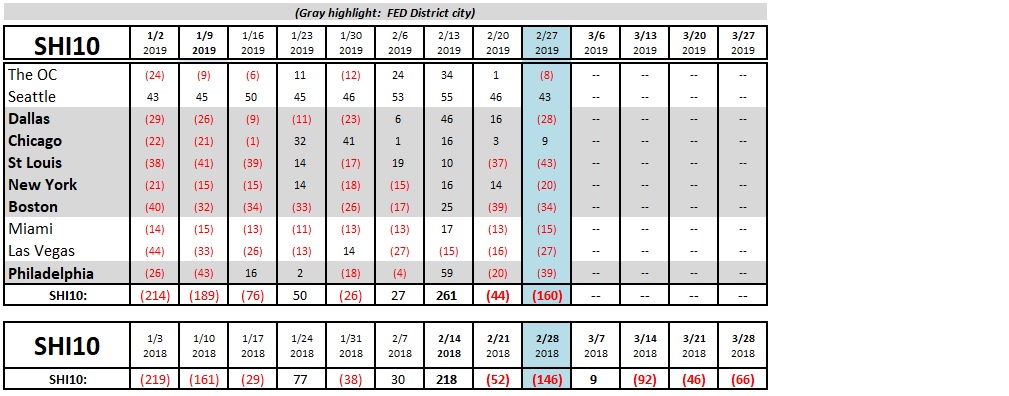

Restaurant reservations this week, I’m sorry to report, are more aligned with the FED state of mind than consumer expectations. Take a look:

With an SHI10 reading of a negative 160, our pricey eateries aren’t feeling the love this Saturday. On the other hand, this reading is fairly consistent with this week back in 2018. It’s interesting to see how closely this year’s SHI10 is tracking last year’s numbers. There’s the stability! 🙂

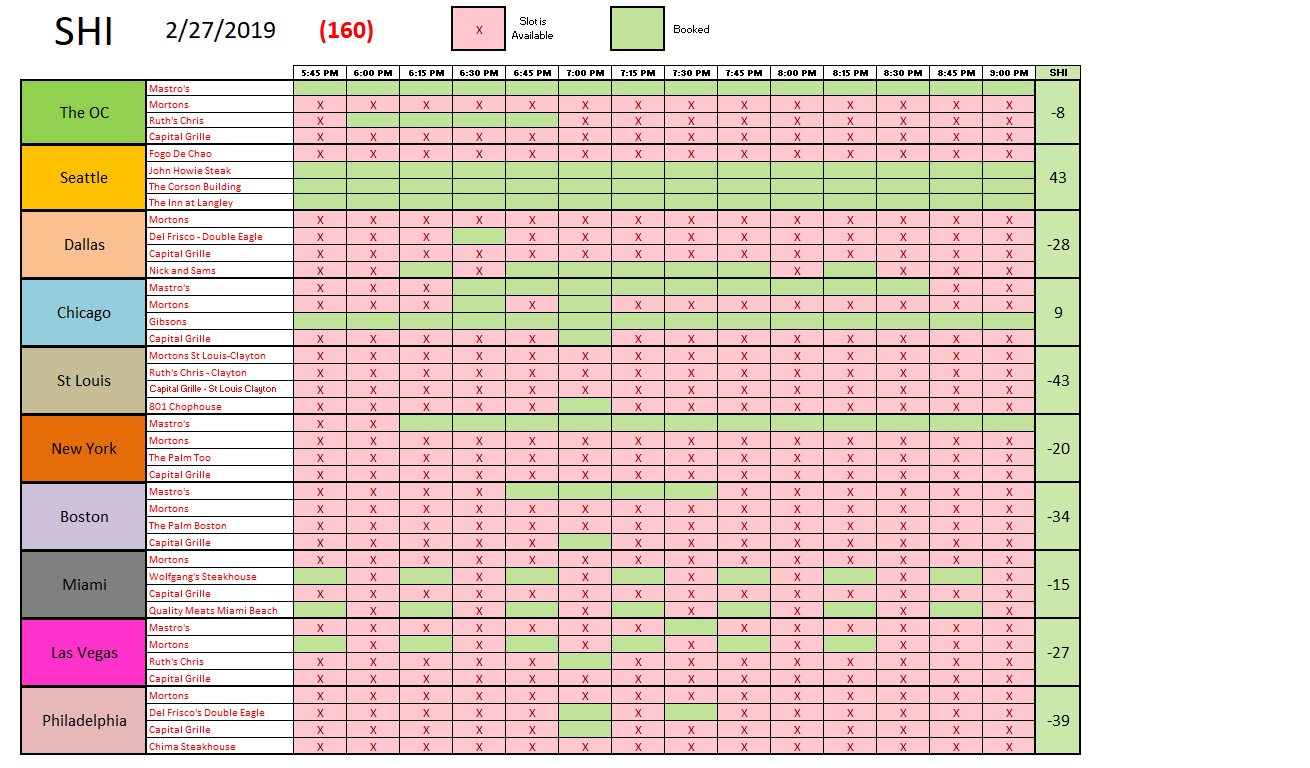

Here is the weekly chart:

If you were hankering for a beautifully grilled T-Bone this weekend, good news: Your local steakhouse is waiting for your call! Enjoy!

- Terry Liebman

{kind=link}