SHI 3.6.19 – Gross Domestic Product

SHI 2.27.19 – Crosscurrents and Conflicting Signals

February 27, 2019

SHI 3.13.19 – A Serious Crisis

March 13, 2019

“Let’s talk GDP. We have Q4, 2018 numbers.”

America’s 2018 GDP finished strong. “Real” GDP grew 2.6 percent during Q4. For the entire year, America’s GDP grew by 2.9%. I suspect 2018 will prove to be a high water mark for GDP growth for years into the future. Why? Let’s dig in below.

Welcome to this week’s Steak House Index update.

If you are new to my blog, or you need a refresher on the SHI10, or its objective and methodology, I suggest you open and read the original BLOG: https://www.steakhouseindex.com/move-over-big-mac-index-here-comes-the-steak-house-index/

Why You Should Care: The US economy and US dollar are the bedrock of the world’s economy. This has been the case for decades … and will continue to be true for years to come.

Is the US economy expanding or contracting?

According to the IMF (the ‘International Monetary Fund’), the world’s annual GDP is about $80 trillion today. US ‘current dollar’ GDP now exceeds $20.89 trillion. In Q4 of 2018, nominal GDP grew by 4.6%…following a 4.9% increase in Q3. We remain about 25% of global GDP. Other than China — a distant second at around $12 trillion — the GDP of no other country is close.

The objective of the SHI10 and this blog is simple: To predict US GDP movement ahead of official economic releases — an important objective since BEA (the ‘Bureau of Economic Analysis’) gross domestic product data is outdated the day it’s released. Historically, ‘personal consumption expenditures,’ or PCE, has been the largest component of US GDP growth — typically about 2/3 of all GDP growth. In fact, the majority of all GDP increases (or declines) usually results from (increases or decreases in) consumer spending. Consumer spending is clearly a critical financial metric. In all likelihood, the most important financial metric. The Steak House Index focuses right here … on the “consumer spending” metric. I intend the SHI10 is to be predictive, anticipating where the economy is going – not where it’s been.

Taking action: Keep up with this weekly BLOG update. Not only will we cover the SHI and SHI10, but we’ll explore related items of economic importance.

If the SHI10 index moves appreciably -– either showing massive improvement or significant declines –- indicating growing economic strength or a potential recession, we’ll discuss possible actions at that time.

The BLOG:

You will recall that “real” GDP growth is adjusted for inflation. For the entire year of 2018, ‘current dollar’ GDP grew 5.2%. That’s a nominal increase of just over $1 trillion for the year. Impressive. And a bit surprising. At least to me.

Because, as I’ve said in numerous prior blog posts, the U.S. has a demographics problem. As a country, we’re getting old. I’m sorry to report that we just don’t have enough young people to (1) support the growing weight of benefits old folks require and (2) to grow the labor force enough to generate a 3%+ annual GDP growth rate. Only a significant increase in employee productivity, or immigration, can change this paradigm. This demographic roadblock is already firmly entrenched. It cannot change for decades.

So a 2.9% GDP growth rate is impressive. And I feel it’s unlikely to repeat. If you want to read more on this topic, direct from the source, click on this link: https://www.bea.gov/news/2019/initial-gross-domestic-product-4th-quarter-and-annual-2018

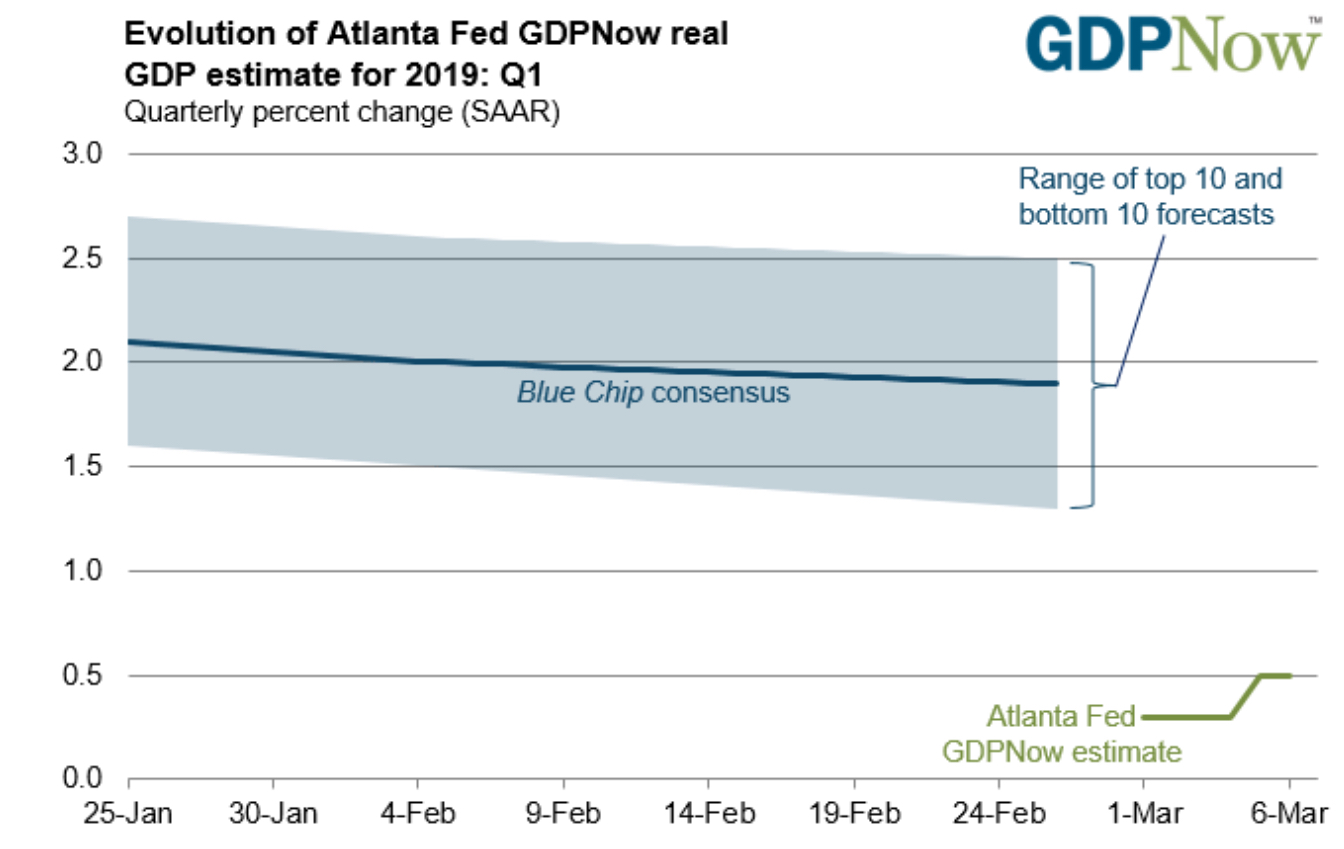

Enough looking back, it’s the mandate of the SHI to look forward … to be forward-looking. To that end, let’s see what the folks at the Atlanta and NYC FED have to say on the topic of Q1, 2019 growth.

With two of the first quarter months of 2019 behind us, the folks in Atlanta aren’t expecting a repeat of Q1, 2018 results. But remember: Q1 GDP growth — at least in recent years — has been the weakest of the four quarters. This was true in 2016, 2017 and 2018.

So perhaps 2019 is simply off to a slow start. As of this morning, March 6th, the economists at the Atlanta FED are forecasting an annualized growth rate for Q1 GDP at only 0.5%. Ouch. That’s a really slow start.

How accurate have the Atlanta folks been, you ask? Pretty good, frankly. For example, on January 3rd, 2019, they made their final Q4 forecast. They projected 2.6%. On the money. On October 1, 2018, they posted their final forecast for the third quarter: 4.1%. They were a bit high — actual “real” GDP growth clocked in at 3.4% in Q3. But they were close. If you wish to review past GDPNow forecasts, here the link: https://www.frbatlanta.org/cqer/research/gdpnow/archives.aspx

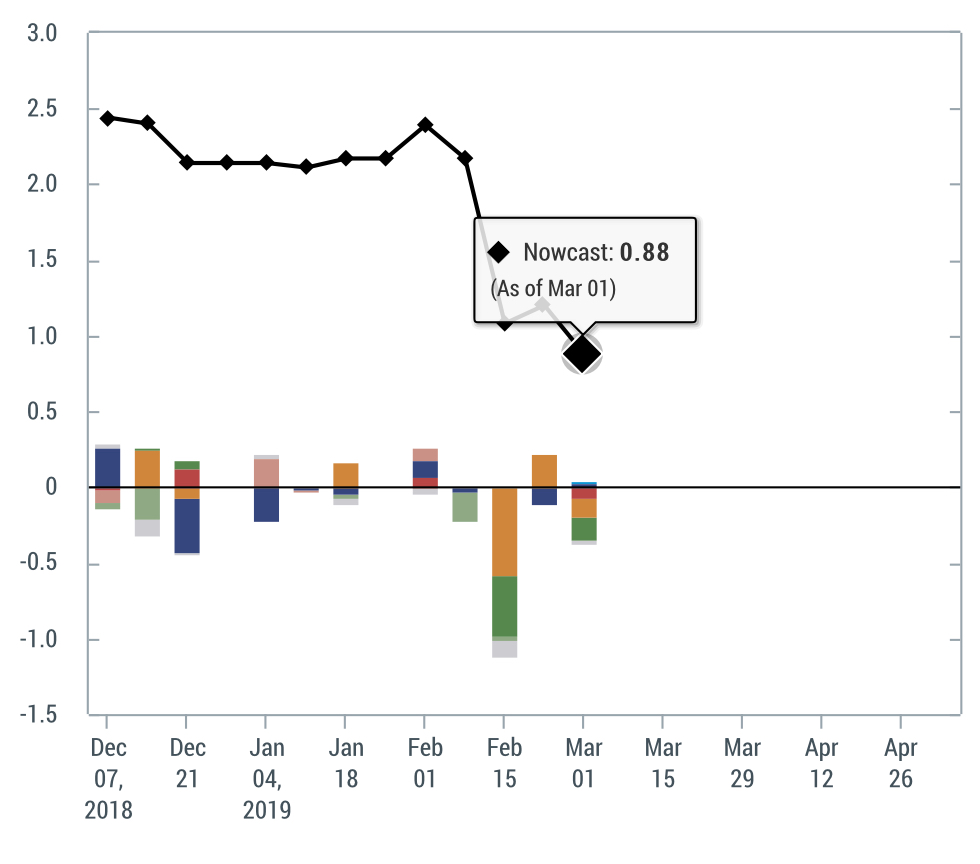

As you know, the NY FED also produces a forecast — called the “NowCast”. Here is their March 1st projection:

Hmmm, again, they are not very optimistic.

Take a look at the chart to the right. Do you notice the HUGE decline on February 15th? The ‘brown‘ and ‘green‘ data points were apparently quite negative. The brown data reflects large declines in ‘capacity utilization’ and ‘industrial production.’ Both data points track manufacturing activity.

But the negative ‘green‘ data strikes right at the heart: This is ‘retail sales and food services.’ The economists at the NY FED see this metric, all by itself, reducing Q1, 2019 GDP growth by 0.41%.

Both the Atlanta and NYC FED are not overly optimistic about the first quarter. It’s interesting to note that so far this quarter, the SHI is not showing the same weakness. Remember, across the country this has been a frigid and inclement winter. Sure, a piping hot ribeye sounds pretty good when it’s a negative 20 outside.

But if the roads are covered in snow, it’s tough to get to Ruths’ Chris! And the ‘government shut-down’ must have had some effect on economic activity.

These anecdotal issues notwithstanding so far, at least, the SHI has been tracking consistently with the first quarter of 2018 when GDP growth exceeded 2%. Let’s see what this week is telling us:

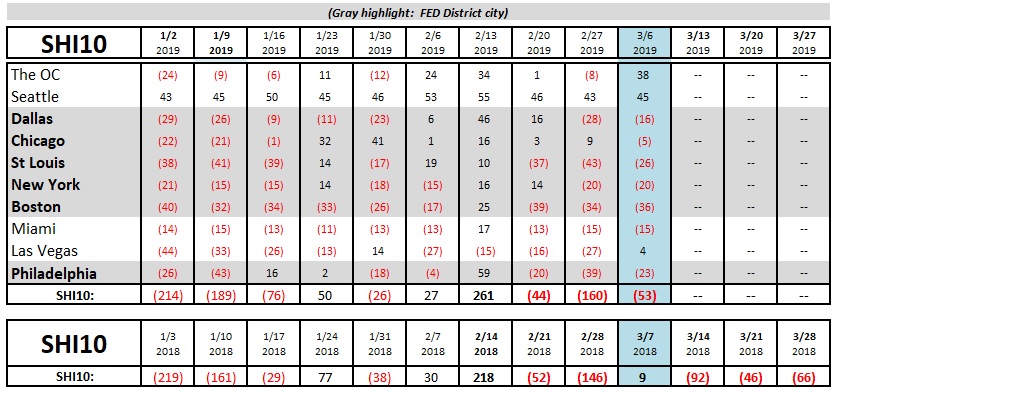

Well, restaurant reservation activity definitely improved. We’re seeing the same trend as last year. But this weeks SHI10 reading of a negative 53 is far weaker than the positive 9 from 2018. Is it meaningful?

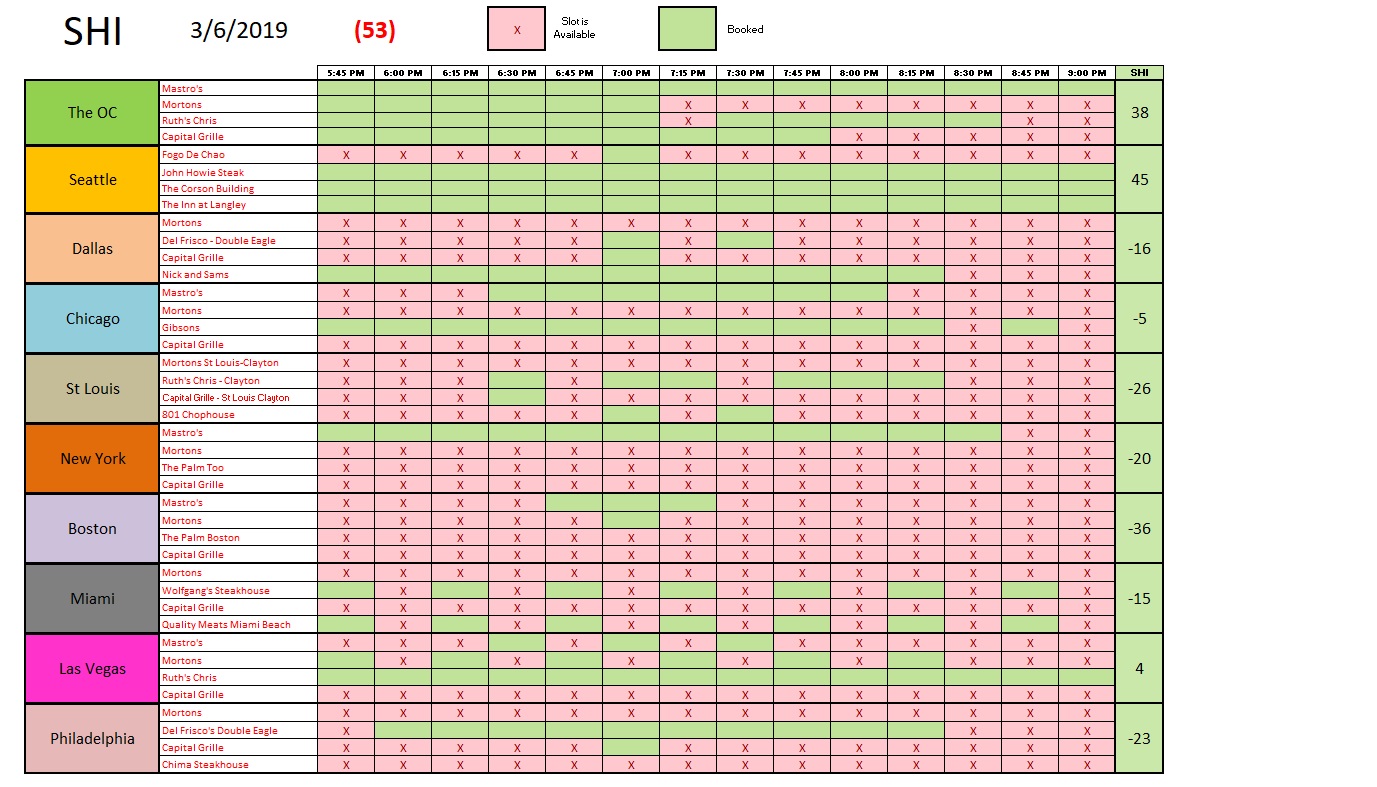

Here’s the weekly report from across the country:

The SHI10 — this week — reflects a slowdown in reservation demand at our pricey eateries. The Atlanta FED and the New York FED are both forecasting much weaker GDP growth numbers for the first quarter. Should we be worried yet? Is a recession on the horizon?

I’m not ready to cast that vote. Let’s be concerned … but let’s not overreact. I think the U.S. economy is slowing … and I think the folks at the Federal Reserve agree. But it’s too early to say by how much. Stay tuned.

- Terry Liebman

1 Comment

Love your Blog. Best, Rob Chandler