SHI 3.27.19 – Why Inflation Matters

SHI 3.20.19 – Antifragile: Things that Gain from Disorder

March 20, 2019

SHI 4.3.19 — Inversion Reversion, Fear and Loathing

April 3, 2019

“We might as well nominate my cat for that other open spot …. ”

… commented Tim Duy in his latest ‘Fed Watch’ blog, speaking about President Trump’s nomination of Stephen Moore for a vacant FED board seat. I like cats. Works for me! 🙂

(Tim’s blog is worth a read, by the way: https://blogs.uoregon.edu/timduyfedwatch/2019/03/24/fed-needs-to-get-with-the-program/).

If Duy’s implication seems excessively harsh, you might want to check out this NewYork magazine article by Jonathan Chait entitled, “Trump Nominates Famous Idiot Stephen Moore to the Federal Reserve Board.” Ouch. Chait has no problem excoriating Moore: “He is capable of writing entire columns that contain no true facts at all.” Double ouch. (http://nymag.com/intelligencer/2019/03/stephen-moore-federal-reserve-trump.html)

One must wonder how well Mr. Moore could fit in at the FED, considering Mr. Moore’s December 2018 comments in the Wall Street Journal shortly after the FEDs December rate hike. Moore stated that FED Chairman Powell is “totally incompetent” and suggested Powell should resign. Yeah, call me a cynic, but I don’t think these two will be the best of buds. I think Tim’s cat may be a better choice.

Welcome to this week’s Steak House Index update.

If you are new to my blog, or you need a refresher on the SHI10, or its objective and methodology, I suggest you open and read the original BLOG: https://www.steakhouseindex.com/move-over-big-mac-index-here-comes-the-steak-house-index/

Why You Should Care: The US economy and US dollar are the bedrock of the world’s economy. This has been the case for decades … and will be true for years to come.

But is the US economy expanding or contracting?

According to the IMF (the ‘International Monetary Fund’), the world’s annual GDP is about $80 trillion today. US ‘current dollar’ GDP now exceeds $20.89 trillion. In Q4 of 2018, nominal GDP grew by 4.6%…following a 4.9% increase in Q3. We remain about 25% of global GDP. Other than China — a distant second at around $12 trillion — the GDP of no other country is close. We can’t forget about the EU — collectively their GDP almost equals the U.S. So, together, the U.S., the EU and China generate about 2/3 of the globe’s economic output. Worth watching, right?

The objective of the SHI10 and this blog is simple: To predict US GDP movement ahead of official economic releases — an important objective since BEA (the ‘Bureau of Economic Analysis’) gross domestic product data is outdated the day it’s released. Historically, ‘personal consumption expenditures,’ or PCE, has been the largest component of US GDP growth — typically about 2/3 of all GDP growth. In fact, the majority of all GDP increases (or declines) usually results from (increases or decreases in) consumer spending. Consumer spending is clearly a critical financial metric. In all likelihood, the most important financial metric. The Steak House Index focuses right here … on the “consumer spending” metric. I intend the SHI10 is to be predictive, anticipating where the economy is going – not where it’s been.

Taking action: Keep up with this weekly BLOG update. Not only will we cover the SHI and SHI10, but we’ll explore related items of economic importance.

If the SHI10 index moves appreciably -– either showing massive improvement or significant declines –- indicating growing economic strength or a potential recession, we’ll discuss possible actions at that time.

The BLOG:

For months I have suggested the December FED rate increase was a judgement error. On this one point, Stephen Moore and I agree. The FED has apparently come to the same conclusion. Before December, they were following the decades-old, deeply ingrained play-book that says the FED must have “room to cut” rates when the next recession arrives. And so, every three months, for several years, they added another .25% to the FED funds rate, so that rates could be cut when the next recession arrived. My concern, as you long-term readers know, was the stair-step FED rate increases were going to cause the very recession the FED feared.

I believe the FED is operating in somewhat uncharted territory: ‘Real’ long-term interest rates, across the globe, are very close to zero today. And they’ve been at this level, I believe, for years. It’s impossible to say precisely on which side of zero they reside, but since the end of the ‘Great Recession’ in late 2009, “close to zero” is where they have settled in … where they now live. For almost ten years now, the central bank in every major developed economy has enjoyed near zero ‘real’ interest rates. This is not a U.S. issue … this is a global condition.

I used the word ‘enjoyed’ for a reason. Many U.S. economists and analysts would argue they have not “enjoyed” these low rates one bit. They would argue our current hyper-low level of interest rates is inherently corrosive, damaging the economy. Banks, insurance companies, pension funds, savings accounts, etc., all depend on a higher general level of interest rates to thrive … let alone, survive. Yes, these low rates are surely damaging these players.

But countries, if they were smart, could actually enjoy these absurdly low rates. Take Germany, for example. At the end of last week, their 10-year bond rates slipped below zero. Down to -0.02%. Not much below zero, to be sure, but below zero nonetheless. So my question for Germany’s central bank, the ‘Deutsche Bundesbank,’ is this: Why the heck don’t you refinance all your short-term debt into 10-year securities? I mean, for gosh sake guys, you can ‘enjoy’ 10 years of free money? Seems like a heck of a good deal to me! Imagine this: NO interest payments for 10 years! It’s like winning the lottery!

Maybe. But here’s the rub: What if current persistent levels of low inflation continue to the point where the globe begins to experience Japan-style deflation? Imagine what might happen to global economic activity if deflation became deeply ingrained, persistent, and expected?

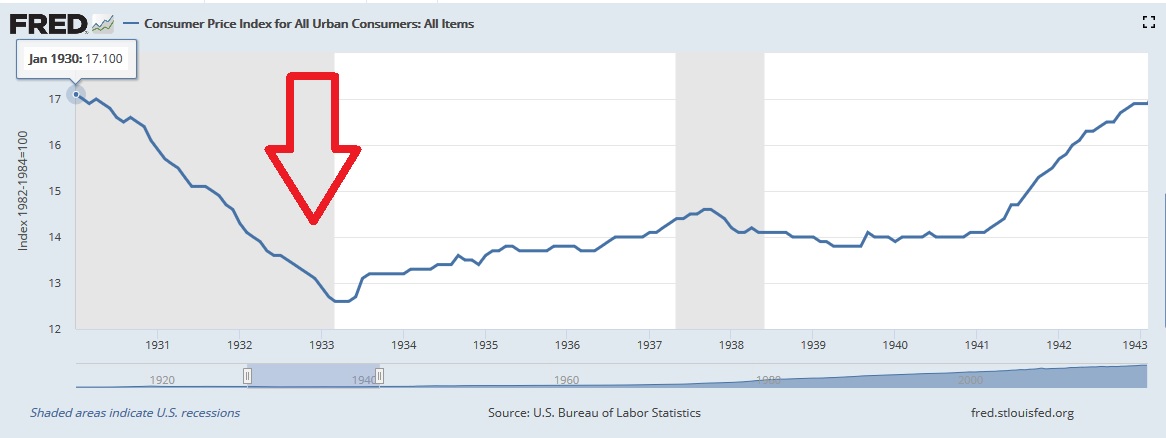

The U.S. experienced our last bout of protracted deflation in the 1930s. More than 80 years ago. Clearly, there are few — if any — living Americans who remember what deflation feels like. Here’s a CPI chart from that period, courtesy of our friends at FRED:

As you can see above, right after the Crash of ’29, prices began to slip. A lot. Above, we see a CPI reading of 17.1 in January of 1930. At its low-ebb in 1933, the CPI bottomed at 12.6 — a 36% reduction in general prices. General prices then danced around for years … reaching a near term high in 1937 before slipping again. It wasn’t until 1941 that inflation returned — more than 10 years later.

If the ‘real’ rate of interest is now zero, in a deflationary environment the ‘nominal’ rate would be less than zero. Negative. Which would mean that borrowing 10-year money at a zero percent interest rate might be overpaying. That’s a crazy idea, right?

In a deflationary condition, repaying a debt far into the future is much more expensive than repaying today. Think of the dynamic this way: If inflation makes your cash less valuable over time, deflation makes your cash worth more. Meaning that in a deflationary cycle, cash you receive 10 years into the future is worth more then than it is now. Not less. Imagine trying to repay our $22 trillion national debt if deflation were persistent?

This is why interest rates would probably move far below zero if deflation were to take hold. The globe would be awash in trillions of dollars of negative-yielding bonds.

The mainstay U.S. unemployment rate (U3) reached about 10% in 2009. As it steadily slid, year after year, to a new low-water mark of 3.8% late last year, the FED believed the U.S. would begin to experience wage inflation. And they worried wage inflation would spread to the economy at large. As you long-term SHI readers know, for years now I’ve expressed my doubt this would happen. I’ve argued the ‘Philips Curve’ is less predictive today given the ‘substitution effect’ from international labor pools and automation. I’ve argued U.S. demographics — which closely align with those in Japan — play a big role in suppressing inflationary tendencies. And I’ve suggested that the scope and scale of global debt — both sovereign and household — are inherently deflationary.

I suspect the FED is coming around to the same mind. A bit. Their biggest concern in recent years appeared to be preparing for the next recession. Now, I suspect, they fear low inflation — or even worse, deflation — much more. And rightfully so. Because a solid economy can shake off a recession and grow again. But shaking off a deflationary spiral is much, much harder to do. In fact, the last time the U.S. had to face down this enemy, it took WW2 to stop our 1930’s deflationary spiral.

The bottom line? Goldilocks had it right. Whether the topic is beds, porridge or inflation, there is always ‘one’ that is “just right.” And on the topic of inflation, ‘just right’ for any developed economy is an inflation rate of about 2%. More or less. The “other two” — hyper-inflation and protracted deflation — are bad. Really, really bad.

Run-away, uncontrolled inflation is the worst of the 3. We’ve seen the deleterious effects of hyper-inflation in many economies — and we see it right now in Venezuela. There is no debate: If your economy is experiencing hyper-inflation, your country won’t be around much longer. Alternatively, while protracted deflation creates many problems for an economy “designed” to experience moderate inflation, it does not destroy the economy. It will destroy many business, but not the overall economy.

Moderate inflation — probably in the range between about 1.75% and 2.5% — is just right. Inflation is important.

And so are steaks. Expensive steaks. A piping hot, fresh-off-the-grill, aged New York isn’t getting any cheaper. Yet. Let’s see how reservation activity is this week.

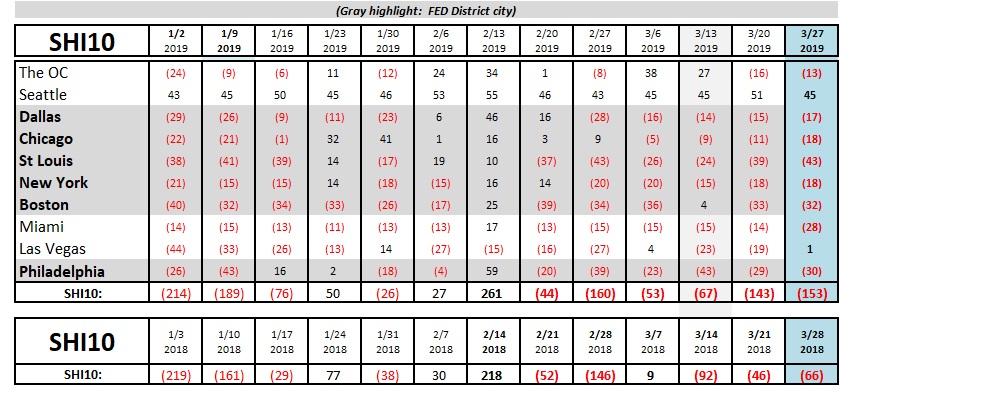

Not so hot. For the second week in a row, reservation activity is significantly lower than this same week in 2018. Take a look at the SHI10 ‘trend’ chart below:

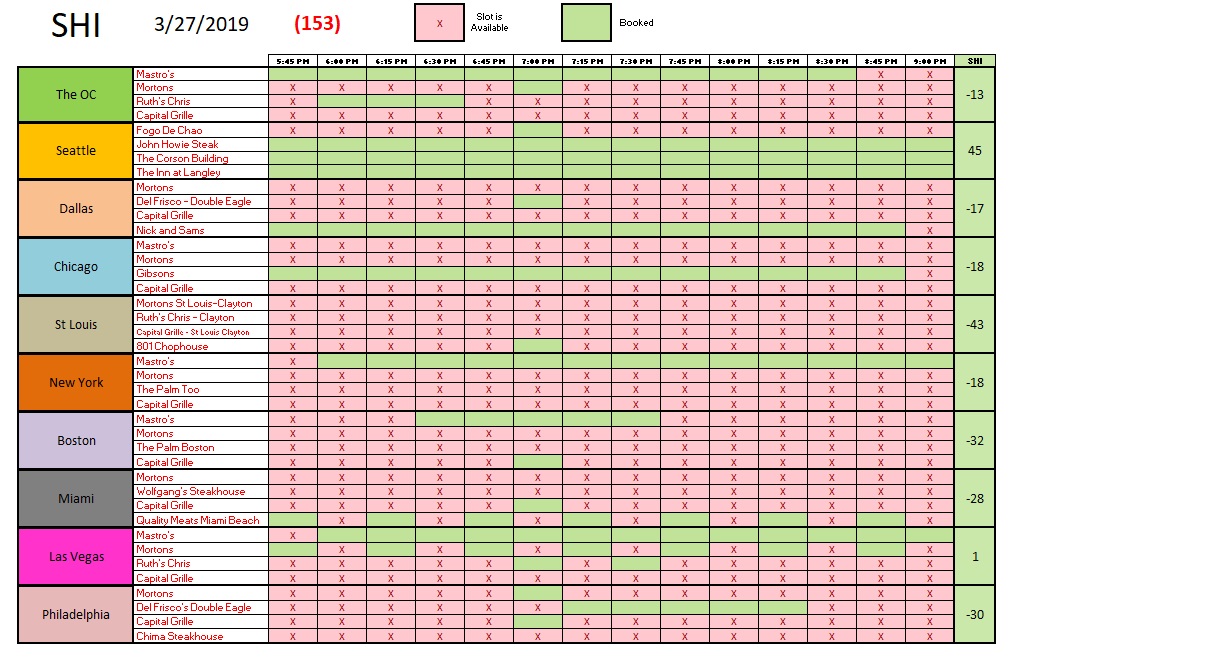

With the exception of the ‘Vegas pricey eateries, almost every other SHI marketplace is experiencing consistently weak or weaker reservation demand this week — and far weaker than this week, last year. Last year, the OC, Seattle and St Louis all had SHI readings ‘in the black.’ This year, only Seattle can make that claim. 60 points of the drop happened in St Louis alone: Last year, the SHI reading this week in St Louis was a positive 17. This week, a negative 43. Ouch. Here is the SHI chart:

The FED believes our economy is weakening. The economies in the EU, China and Japan, too, are slowing. Not falling into recession (Italy aside), mind you, just weakening.

The SHI numbers seem to agree. The well-heeled, expensive steak customers are making fewer reservations right now. For 2 weeks in a row. We are ending Q1, 2019 on a weak note. The next SHI update will be the first for Q2. Let’s see if the trend continues.

- Terry Liebman

{kind=link}

3 Comments

Informative as always.

Thank you!

“Inflation is important.”

Got it.

Thanks Terry.

We’re going out for a steak…and while we’re at it, we’ll pick up some inflation!

Choosing between Bearnaise, steak sauce or inflation, I prefer inflation on my steak!