SHI 5.19.21 – The Kinetic Inflation Roller Coaster

SHI 5.12.21 – US Household Debt JUMPS

May 12, 2021

SHI 5.26.21 – The $8 Trillion Man

May 26, 2021

Imagine you are riding a roller coaster. Your car has chugged and climbed, finally reaching the peak. The coaster ever-so-slowly comes to a near-stop. But moments later, you are plunging seemingly straight down, gaining speed at a rate you would not have believed physically possible, your heart in your throat.

“

All aboard the ‘Liquidity Trap’ roller coaster!“

“All aboard the ‘Liquidity Trap’ roller coaster!“

At the hill’s crest, your coaster has also reached peak gravitational ‘potential energy.’ And at the bottom of the next valley, along with your fear and anxiety, you and your car have now accumulated the maximum potential kinetic energy possible at that moment. It’s worth noting the two are equal (ignoring friction, absolute value).

OK, by now you’re probably asking, what the heck does this have to do with money supply, economics, and more specifically, inflation? Hold on … here we go!

Welcome to this week’s Steak House Index update.

If you are new to my blog, or you need a refresher on the SHI10, or its objective and methodology, I suggest you open and read the original BLOG: https://www.steakhouseindex.com/move-over-big-mac-index-here-comes-the-steak-house-index/

Why You Should Care: The US economy and US dollar are the bedrock of the world’s economy.

But is the US economy expanding or contracting?

The short answer? Expanding. A lot. Forever more, COVID-19 will be mentioned concurrently with any discussion about 2020 GDP. Collectively, the world’s annual GDP was about $85 trillion by the end of 2020. But I am confident all 2021 GDP discussions will start with a nod to the blowout 1st quarter GDP growth number, because our ‘current dollar’ GDP grew at the annual rate of 10.7%! Annualized, America’s GDP blew past $22 trillion during the quarter, settling in at $22.0489 trillion. The US, the euro zone, and China continue to generate about 70% of the global economic output.

The objective of this blog is singular.

It attempts to predict the direction of our GDP ahead of official economic releases. Historically, ‘personal consumption expenditures,’ or PCE, has been the largest component of US GDP growth — typically about 2/3 of all GDP growth. In fact, the majority of all GDP increases (or declines) usually results from (increases or decreases in) consumer spending. Consumer spending is clearly a critical financial metric. In all likelihood, the most important financial metric. The Steak House Index focuses right here … on the “consumer spending” metric. I intend the SHI10 is to be predictive, anticipating where the economy is going – not where it’s been.

Taking action: Keep up with this weekly BLOG update. Not only will we cover the SHI and SHI10, but we’ll explore related items of economic importance.

If the SHI10 index moves appreciably -– either showing massive improvement or significant declines –- indicating growing economic strength or a potential recession, we’ll discuss possible actions at that time.

The Blog:

Here’s our roller coaster. Our coaster has been named ‘Liquidity Trap‘ by Nobel prize winning economist Paul Krugman. We are all on board. We have no choice. Put on your seat belt.

Right. It’s not a real roller coaster … In this case, the coaster is a metaphor for money supply. More specifically, ‘M2 money stock’ and all the ups and downs we’ve seen over the past 70 or so years. That’s the blue line. What are the straight black lines? I added those to highlight periods of significant M2 money supply growth. You’ll see six (6) straight black lines in the graph above. All but one appear to be triggered by, or concurrent with, a recession. And, of course, the >26% M2 increase was part of the Coronavirus pandemic response.

The red line is the inflation rate. More specifically, it’s the ‘PCE‘ that the FED prefers over the CPI. Interestingly, in the graph above, before 1980 it appears that spikes in the PCE may have been triggered by earlier excessively large M2 growth episodes. But not in the recent past. I’ve highlighted 3 such episodes in the past 20 years (ignoring, for the moment, the 2020 spike) none of which triggered an inflationary response. Why? Finally, while recent M2 spikes didn’t trigger a robust increase in the PCE, will the 2020 HUGE spike trigger a different outcome?

Newton’s first law of motion tells us that an object set into motion will maintain its ‘speed’ unless acted upon by another ‘force.’ Like gravity. Or a concrete wall.

Economics is similar. GDP always changes when another ‘force’ is introduced into the equation. In the past year or so, the US pandemic response spiked money supply (M2) at grow rates never before seen. According to the St Louis FED, as of 1/1/21, Americans had $4.116 trillion in savings. That number has increased since then, as American ‘personal income’ saw a huge spike in April, alone, increasing by another $351 billion. In my roller coaster analogy, Americans now find themselves at the peak of the “money hill.” Right at the crest. But instead of potential energy, the potential here is spending. Americans have more money, for more potential spending, than ever before. Fascinating!

The fiscal and monetary stimulus of the past year or so have spurred our economy into frenetic motion. This “kinetic economic condition” is unprecedented. The spending potential is massive. Will Americans’ spend their money?

Bottom Line: The other day, a friend asked, “Will prices increase?” I responded, “yes, many already have.” She then replied, “So inflation is coming?” To which I said, “not necessarily.” As I’ve said before, there is a mountain of difference between price increases in lumber or used cars and the PCE or CPI in the aggregate.

We are in uncharted territory. The global pandemic has disrupted many things. Supply chains, housing, materials, shipping, the list goes on and on. So we’ve seen serious price spikes, remote working, shortages, etc. Are these changes transitory?

We simply don’t know yet.

Economist Paul Krugman agrees with the FED: Yes is their answer. Paul believes all the inflation fears in today’s news result from old and outdated economic theory. He believes the Milton Friedman ‘Monetarists‘ of decades past should be dead and buried. He believes developed countries are now firmly entrenched in what he (and others) call a ‘Liquidity Trap’ and in this environment, increases in money supply do not translate directly into consumer spending spikes. (Theory suggests that a liquidity trap develops after interest rates fall to or below a certain level. <I would add that in addition, rates have to stay there for a protracted period, thus appearing ‘permanent’ as opposed to ‘transitory.’> Once that occurs, the argument goes, liquidity preference becomes virtually absolute in the sense that everyone prefers holding cash rather than holding a debt or financial instrument which yields so low an ROI as to render the return meaningless.)

Essentially, I interpret Paul’s comments to suggest that in a longer term, zero-bound interest rate environment, excess liquidity (cash) simply causes the unspent cash to be kinetic. Could it cause an inflationary spiral should everyone spend every dollar in a very short period of time? Sure. But people will elect to hold the cash. Not spend. His comment:

But when interest rates are very low — which they have been for years, basically because there’s a glut of savings relative to perceived investment opportunities — money is, at the margin, just another asset. When the Fed increases the money supply, people don’t feel any urgent need to put that cash to more lucrative uses, they just sit on it.

I agree with him. Cash in the bank is simply another asset. With few alternatives that offer attractive ROIs, cash in the bank is safer and yields about the same. Meaning nothing. And so it sits. Kinetically.

Prices of many goods — both consumables and durable — have increased. Some significantly. But I feel these changes are more the result of disruptions than inflation. Alternatively, the prices of assets that do, or may, generate an ROI have definitely increased. And they will continue to do so, over time, as ‘capital for investment’ and consumer cash at the margin are not fungible. Capital seeks a return. Cash just sits, kinetically, and looks pretty.

I believe the FED is right. I believe Krugman is right. Any PCE inflation we see, in the short run, will be transitory. Yes, consumers have a whole bunch of cash. But I don’t believe they will be inspired to spend it on consumables. Some will be used to reduce debt (read: credit cards) which is actually deflationary. Some will be invested. Some will be spent on necessities. But most will simply sit and dissipate slowly, over time. 🙂

But steak houses are here to stay. Once again, this week our grills are smoking hot and steak reservations are on fire!

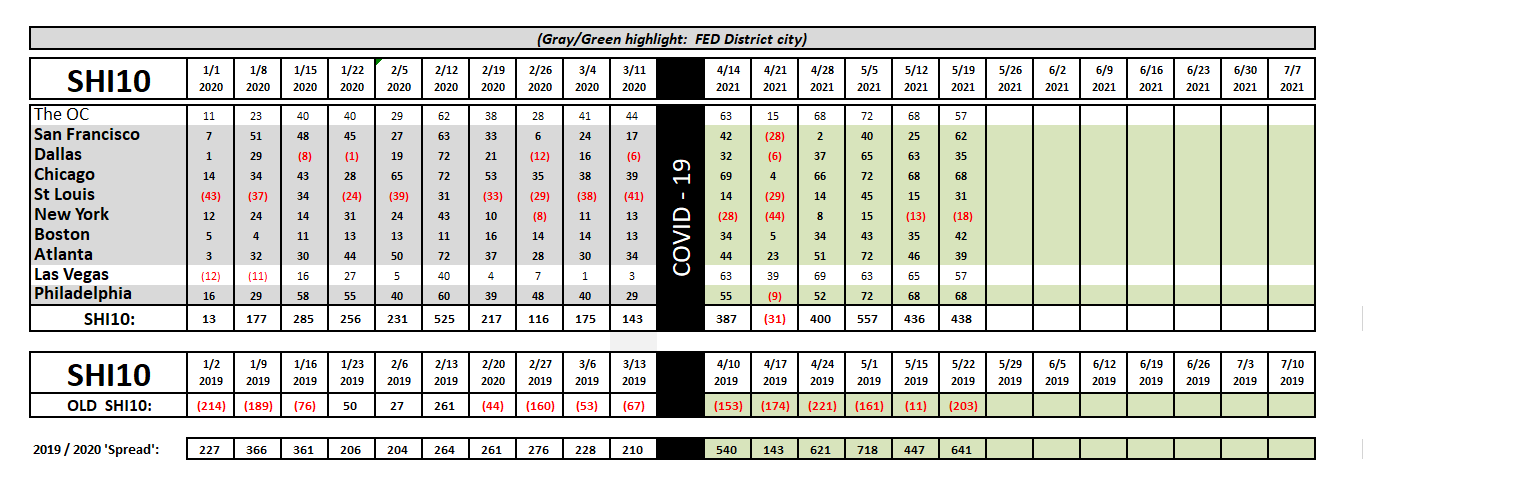

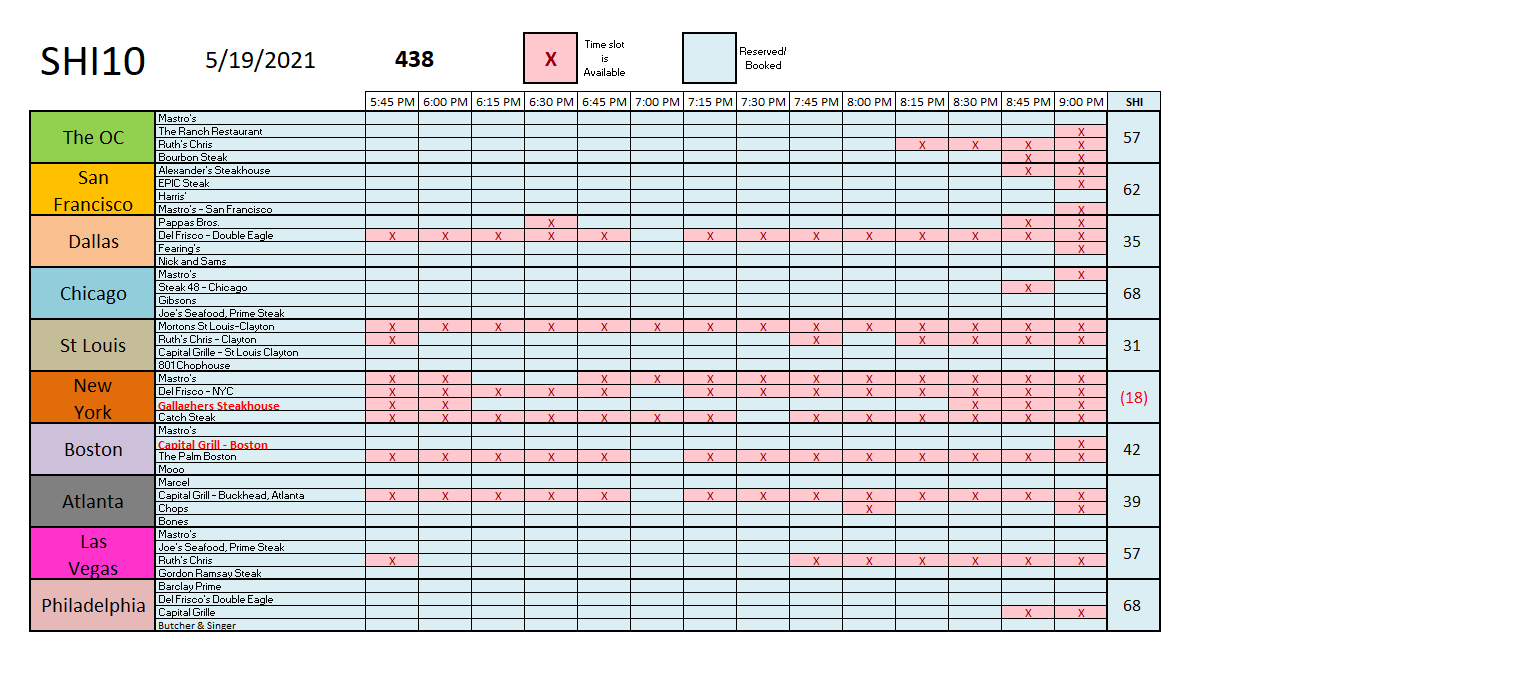

NYC continues to struggle, but Saturday evening steak reservations in expensive eateries in every other city are hard to come by. And the “reservation demand” spread in 2021 over 2019, once again, is monstrous. Steak house reservations in ‘Vegas, Chicago and Philly are almost impossible to find this Saturday. And look at the improvement in San Francisco. Interestingly enough, this improvement is before the ‘mask mandate’ is lifted! Wow. Here’s the city-by-city chart:

I will finish with these comments: I apologize if this blog is overly dense. I’ve edited, and removed, much of the content I had originally planned to share. It was too much, I concluded. Perhaps I was inspired by Mark Twain, or even Shakespeare, but I decided brevity, in this case, was best. Was I succinct enough? 🙂

Time for a steak and a great bottle of wine. 🙂

<> Terry Liebman