SHI 6.2.21 – Where’s the Beef?

SHI 5.26.21 – The $8 Trillion Man

May 26, 2021

SHI10 6.9.21 – Quite a JOLT!

June 9, 2021

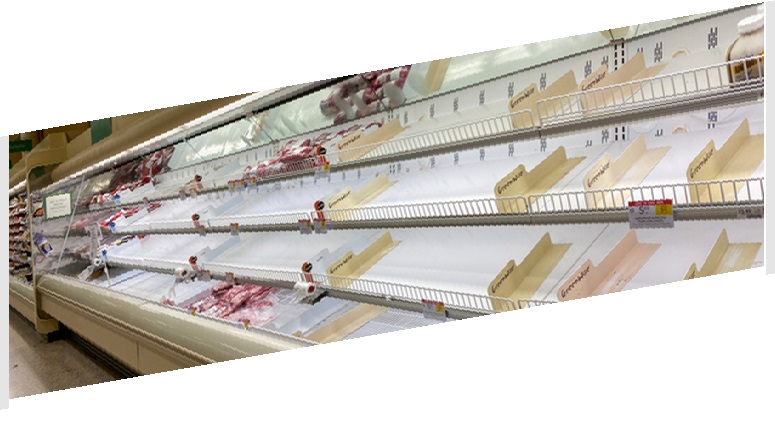

The shelves are empty ??? Where’s the beef?

Across the globe, cattle got a ‘stay of execution’ earlier this week when the digital and analog worlds collided in a ransomware attack on the largest beef producer in the world, Brazil-based JBS.

“

The price for Mastros T-Bones just jumped. A lot.“

“The price for Mastros T-Bones just jumped. A lot.“

Trust me. Our expensive eateries just got more expensive. Thanks to a ransomware attack on beef. What a world.

Welcome to this week’s Steak House Index update.

If you are new to my blog, or you need a refresher on the SHI10, or its objective and methodology, I suggest you open and read the original BLOG: https://www.steakhouseindex.com/move-over-big-mac-index-here-comes-the-steak-house-index/

Why You Should Care: The US economy and US dollar are the bedrock of the world’s economy.

But is the US economy expanding or contracting?

The short answer? Expanding. A lot. Forever more, COVID-19 will be mentioned concurrently with any discussion about 2020 GDP. Collectively, the world’s annual GDP was about $85 trillion by the end of 2020. But I am confident all 2021 GDP discussions will start with a nod to the blowout 1st quarter GDP growth number, because our ‘current dollar’ GDP grew at the annual rate of 10.7%! Annualized, America’s GDP blew past $22 trillion during the quarter, settling in at $22.0489 trillion. The US, the euro zone, and China continue to generate about 70% of the global economic output.

The objective of this blog is singular.

It attempts to predict the direction of our GDP ahead of official economic releases. Historically, ‘personal consumption expenditures,’ or PCE, has been the largest component of US GDP growth — typically about 2/3 of all GDP growth. In fact, the majority of all GDP increases (or declines) usually results from (increases or decreases in) consumer spending. Consumer spending is clearly a critical financial metric. In all likelihood, the most important financial metric. The Steak House Index focuses right here … on the “consumer spending” metric. I intend the SHI10 is to be predictive, anticipating where the economy is going – not where it’s been.

Taking action: Keep up with this weekly BLOG update. Not only will we cover the SHI and SHI10, but we’ll explore related items of economic importance.

If the SHI10 index moves appreciably -– either showing massive improvement or significant declines –- indicating growing economic strength or a potential recession, we’ll discuss possible actions at that time.

The Blog:

Because of the ransomware attack, JBS was forced to close beef processing facilities in Utah, Texas, Wisconsin and Nebraska and canceled shifts at plants in Iowa and Colorado on Tuesday, according to union officials and employees. “There are at least 10 plants I have knowledge of that have had operations suspended because of the cyberattack,” said Paula Schelling-Soldner, acting chairperson for the national council of locals representing food inspectors for the American Federation of Government Employees.

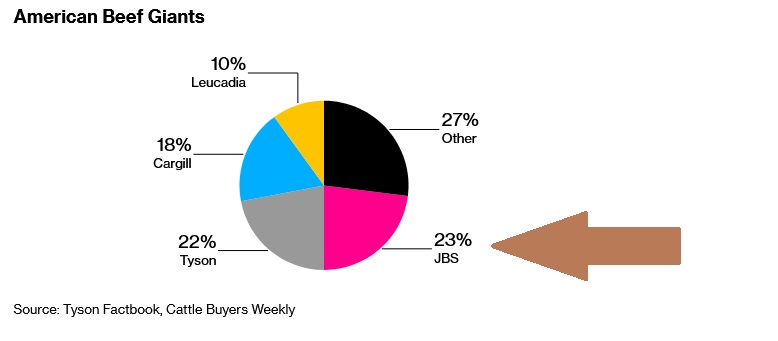

As a result of the cyber-attack, very much like the rain in Spain, cows remain mainly on the plain. Brazil-based JBS — the owner of the ‘Swift’ brand of beef and pork, as well as Pilgrim’s Pride — is a global producer responsible for almost 1/4 of all global beef supply. They own and operate facilities in 20 countries. This supply disruption will most assuredly impact the price everyone pays for a filet Mignon:

Shortages will push up steak prices. Is this inflation? Technically, no. It’s a supply-chain disruption. The price of beef will rise, but it may come back down later. Probably not. I suspect we will all soon be paying $75 or more for a beautifully prepared steak at our expensive eateries. More on the inflation debate, it’s worth noting that FED governors Lael Brainard, Raphael Bostic and James Bullard all said Monday that they wouldn’t be surprised if prices rise in the coming months, but they all again reiterated that most of those gains should be temporary.

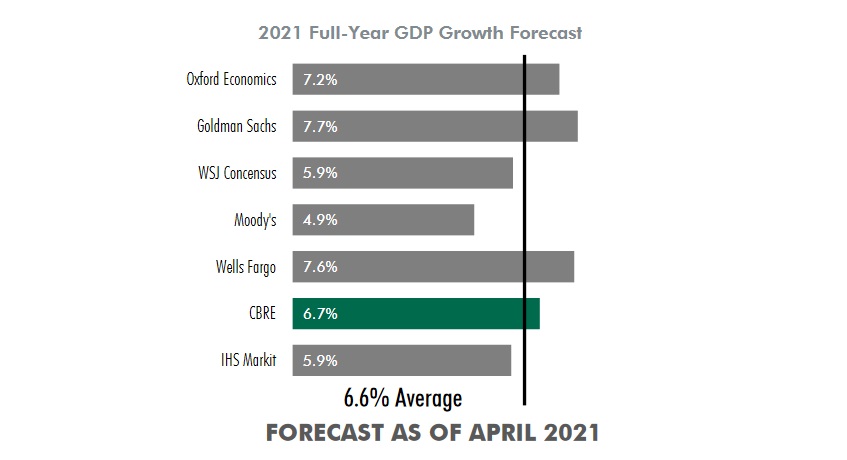

At the same time, 2021 GDP forecasts, too, continue to set new records. Back in January, the average GDP forecast for 2021 had already achieved the lofty level of 5.2% for the year. Three months later, the average is up to 6.6%:

Remember, these GDP numbers are ‘real.’ Which is to say that the nominal growth rate — or the ‘current dollar’ growth rates — for 2021 could easily top 10%. Staggering. 10% of $22 trillion is more than $2 trillion. And you may recall that federal tax collections tend to equal about 20% of GDP; thus, if 2021 generates an additional $2.2 trillion in GDP, tax collections on this portion alone could increase as much as $440 billion per year every year into the foreseeable future. Viewed thru another lens, in theory, the most recent Covid-inspired stimulus could be repaid to the US Treasury in just 5 years from the increased tax revenue. Assuming the government doesn’t spend it on something else. 🙂

It’s worth noting that the latest Q2 GDP forecast from the NY FED — their ‘nowcast’ — is 4.3%, and the 6/1/2021 ‘real’ GDP projection from the Atlanta FED is a staggering 10.3%!

https://www.atlantafed.org/cqer/research/gdpnow

Phew. Amazing. Let’s head to the steak houses and see if they agree.

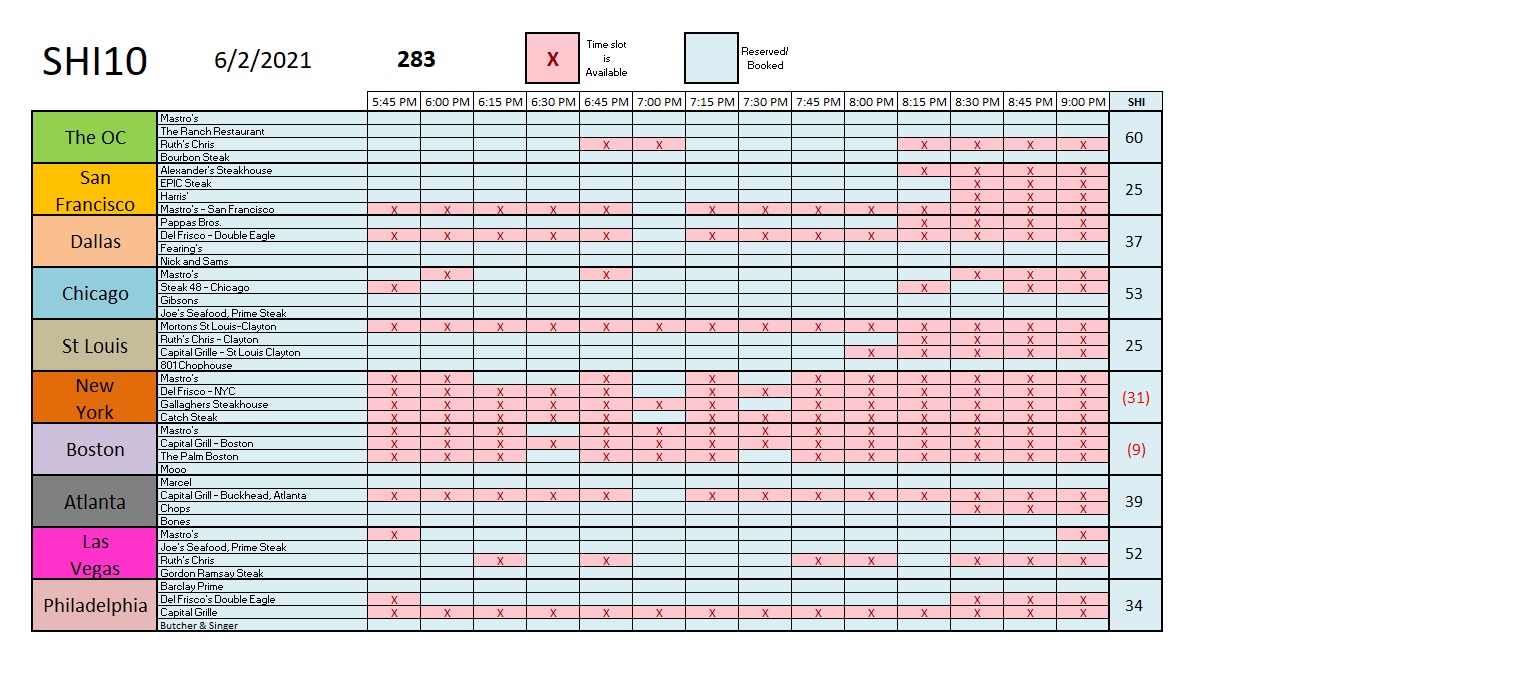

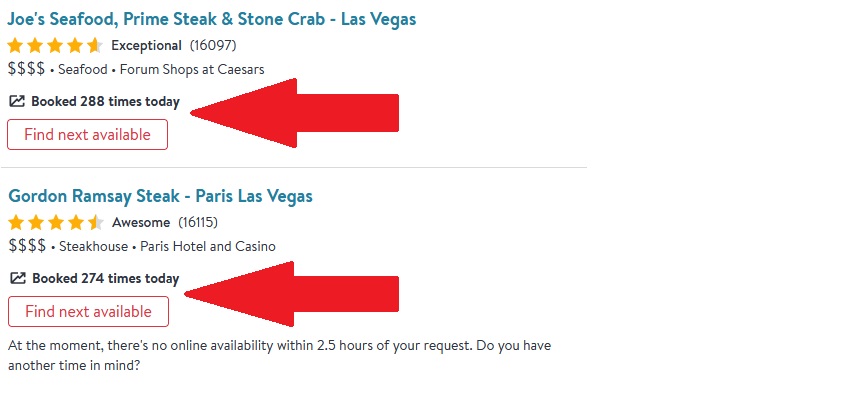

Hmmm….so so. This week our steak house grills are cooking at medium heat. Pricey steak houses in New York and Boston are having trouble filling their seats … while reservations in ‘The OC’ and ‘Vegas are flying off the shelf. You’ll remember that I pull this data off ‘Open Table’ at around 11 am. Take a look at the graphic below:

Joe’s and Gordon Ramsay, both of which are fully booked for this coming Saturday, were booked today 288 and 274 times, respectively. And that activity took place before 11 am! Economic activity in ‘Vegas is on fire.

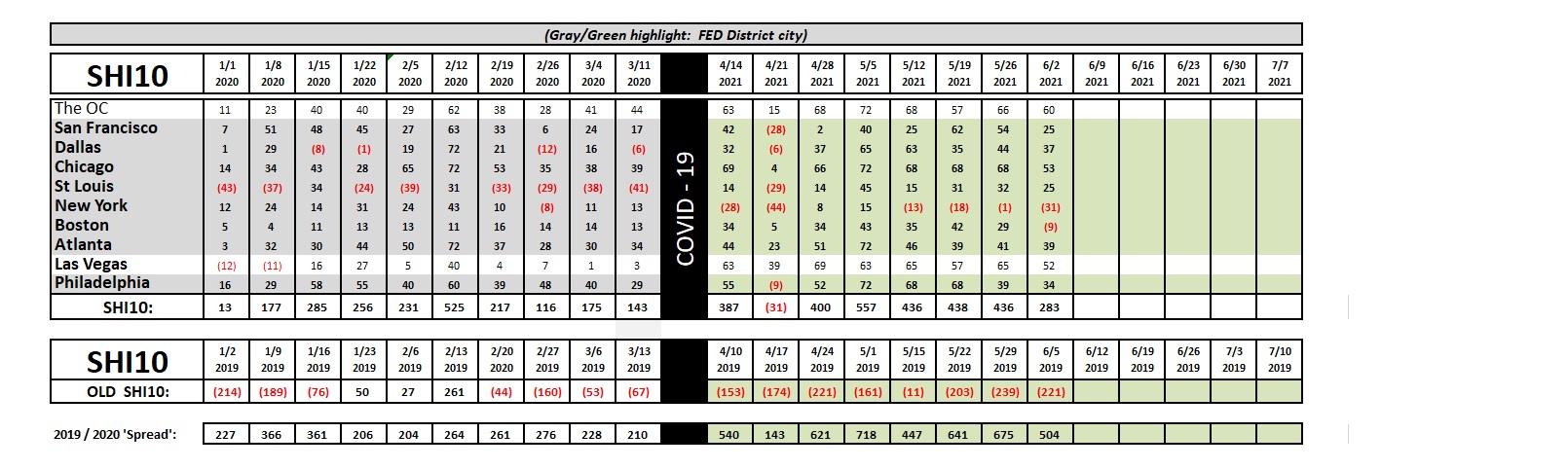

Here’s the longer term trend grid:

With a ‘spread’ reading of 504, today’s SHI10 still reflects much stronger reservation demand than 2019.

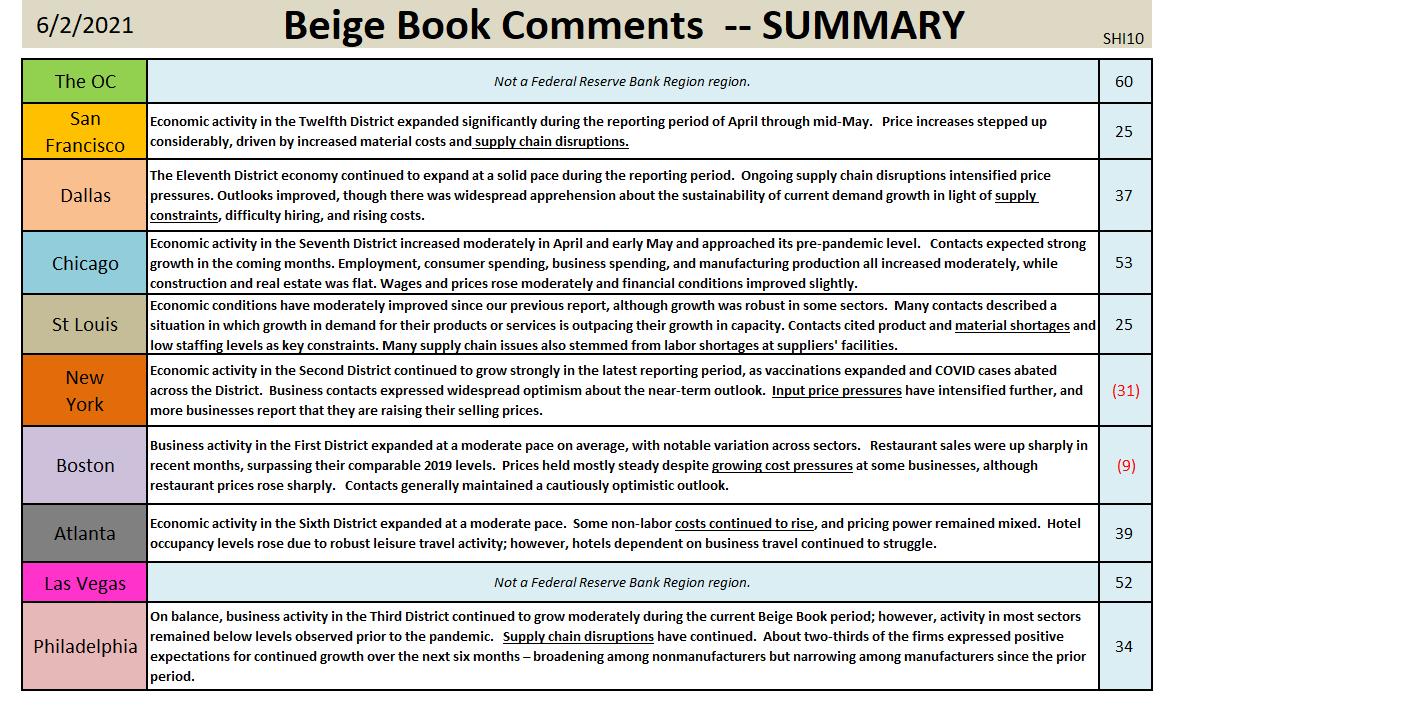

Speaking of beef, the Federal Reserve ‘Beige Book’ was released today. What is the Beige book, you ask? In the FEDs own words:

The Beige Book is a Federal Reserve System publication about current economic conditions across the 12 Federal Reserve Districts. It characterizes regional economic conditions and prospects based on a variety of mostly qualitative information, gathered directly from each District’s sources. Reports are published eight times per year.

Here is a brief summary that I have compiled (and edited for length) for the eight (8) SHI10 geographic areas that are overlap the FED districts:

Shortages and price pressures, as you can see, are quite commonplace. But, that aside, economic activity in all FED districts is brisk. Big picture, both the FED and SHI10 the data appear to support the strong GDP and economic forecasts as the economy recovers and heals from the long Covid disruption.

- <|> Terry Liebman