SHI 7.12.23 – A Gigantic Meal

SHI 7.5.23 — Rolling Along

July 5, 2023

SHI 7.26.23 – A Clash of Titans

July 26, 2023

Yes, that’s the Wolly Mammoth. The one on the left. 🙂

History suggests they roamed the earth for about half a million years, until vanishing about 5,000 years ago. They are gone. Extinct. And yet, in the near future, you might order a ‘Mammoth-Mac’ at MacDonalds. The Big, Super Big, GIANT, Big Mac is coming soon!

“

Is MacDonalds planning a ‘Wolly Burger?’“

“Is MacDonalds planning a ‘Wolly Burger?’“

No. They are not. I jest.

However, several companies across the globe are now sequencing Wolly Mammoth DNA to create ‘cultured meat’, recreating a protein that hasn’t existed for about 5,000 years. How’s it taste? No one knows: Scientists are not yet sure how the modern human immune system would react to this long extinct protein.

Regardless of your appetite to bite-down on a ‘Wolly Burger’, this revolution in evolution is a fascinating and somewhat important economic development.

Yep … once again, we’re talking burgers and economics. So sit back, relax, and sink your teeth into today’s blog.

Welcome to this week’s Steak House Index update.

If you are new to my blog, or you need a refresher on the SHI10, or its objective and methodology, I suggest you open and read the original BLOG: https://www.steakhouseindex.com/move-over-big-mac-index-here-comes-the-steak-house-index/

Why You Should Care: The US economy and US dollar are the bedrock of the world’s economy.

But is the US economy expanding or contracting?

Expanding. Even as the FED rapidly raises rates! At the end of Q1, 2023, in ‘current-dollar’ terms, US annual economic output rose to an annualized rate of $26.53 trillion. After enduring the fastest FED rate hike in over 40 years, America’s current-dollar GDP still increased at an annualized rate exceeding 6% during the first quarter of 2023. No wonder the FED is so concerned. The world’s annual GDP rose to over $100 trillion as 2022 began. And according to the IMF, in June of this year, current-dollar global GDP eclipsed $105 trillion! IMF forecasts call for global GDP to reach almost 135 trillion by 2028. America’s GDP remains around 25% of all global GDP. Collectively, the US, the euro zone, and China still generate about 70% of the global economic output. These are the 3 big, global players. They bear close scrutiny.

The objective of this blog is singular.

It attempts to predict the direction of our GDP ahead of official economic releases. Historically, ‘personal consumption expenditures,’ or PCE, has been the largest component of US GDP growth — typically about 2/3 of all GDP growth. In fact, the majority of all GDP increases (or declines) usually results from (increases or decreases in) consumer spending. Consumer spending is clearly a critical financial metric. In all likelihood, the most important financial metric. The Steak House Index focuses right here … on the “consumer spending” metric. I intend the SHI10 is to be predictive, anticipating where the economy is going – not where it’s been.

Taking action: Keep up with this weekly BLOG update. Not only will we cover the SHI and SHI10, but we’ll explore “fun” items of economic importance. Hopefully you find the discussion fun, too.

If the SHI10 index moves appreciably -– either showing massive improvement or significant declines –- indicating growing economic strength or a potential recession, we’ll discuss possible actions at that time.

The Blog:

Cultured meat has been trumpeted as a realistic and viable solution for climate change and a host of other man-made problems. With about 8 billion humans now occupying our planet, discussions like this are important, whether or not you agree with climate change theories. That discussion aside, it is an indisputable fact that more people means more demand for more stuff. Whether we’re discussing traffic on the freeways, frenzy for Taylor Swift concert tickets, or used cars, an ever increasing population in a wealthier world pushes up demand. Continuously. Relentlessly. Against that backdrop, land and water uses become a much larger part of the human ‘sustainability’ debate.

So regardless of what side of the debate you find yourself on, the simple fact is that DNA sequencing of extinct species might today be one technological key to open doors previously bolted closed, paving the way for new products and solutions, benefiting both capitalism and humanity.

Consider recent developments at the British cosmetics firm, Haeckles. They are experimenting in potential solutions to their expanding need for land and water to create fragrances. With the goal of cutting out farming completely, they are attempting to engineer scents from flowers lost to extinction by synthetically producing them from DNA. If successful, flower farming for use in fragrances could become a thing of the past. Extinct. ?

Ironic, right?

‘De-Extinction’ is the high-level term used to describe this movement. What is de-extinction? From one website promoting the concept:

“De-extinction, or resurrection biology, reverses plant and animal extinctions by creating new versions of previously lost species. Back-breeding, cloning, and genome editing are species restoration methods. The goal is to re-establish dynamic processes that produce healthy ecosystems and restore biodiversity.”

Can a real ‘Jurassic Park’ be very far behind? According to the folks at Colossal Laboratories and Biosciences, the answer is no:

“In 2016, The International Union for the Conservation of Nature (IUCN) drafted the IUCN SSC Guiding Principles on Creating Proxies of Extinct Species for Conservation Benefit. In addition to providing a framework for scientists and other stakeholders, the guidelines explain that the term de-extinction is somewhat misleading. It implies that it is possible to resurrect extinct species in their genetic, behavioral, and physiological entirety. This is not the case.”

Good. I really don’t want to wake up one morning to find a T-Rex at my front door, hoping to eat my cat. Or me for that matter. That would be bad. Perhaps I could convince him to eat a Wolly Burger instead? 🙂

Here’s the point … as I bring us back full circle to today’s economic discussion.

While fertility rates are down significantly in much of the world, aggregate global population levels still continue to increase, albeit at a slower rate. Remember, we recently eclipsed 8 billion. As population expands, most people hope to improve the lives of their families and children; often choosing to migrate from barren lands with limited opportunity, to geographic locations where their family might thrive and succeed financially. Which means there are discernible and definable geographies, around the globe, where human economic opportunities are the greatest. And conversely, there are those where the opportunities are the smallest. Fortunately for us, the United States is still perceived as one of the good places to be.

Against this backdrop, the post-pandemic world continues to change and evolve, implementing hard lessons learned since 2020.

And all of a sudden, this: Hardly a day goes by without another AI discussion in the media. Everywhere we see forecasts of humanity’s doom or salvation from Artificial Intelligence. And doom or salvation aside, it is widely believed that AI will significantly alter the future, in many, many ways. Ways we cannot even yet imagine. I agree. From the economic and financial viewpoint, the one likely conclusion we can draw is the benefits of AI to global businesses are significant. The potential operating cost savings and efficiencies from AI cannot be overstated. If anything, we yet under appreciate them.

Thru this lens, consider the pending US infrastructure expansion. To be clear: I am an “America Fan” … pretty much anything that makes the country better in the aggregate, I’m in favor of.

So when I make the following comments, know they are not political. The Infrastructure Investment & Jobs Act (“IIJA”) was approved in November of 2021. Less than 1 year later, in August of 2022, The CHIPS and Science Act (“CHIPS”) became law. The IIJA will pump up to $1.2 trillion into the economy. The CHIPS legislation adds another $280 billion. This almost $1.5 trillion will be spent over many years … and when passed, Congress hoped both would provide significant infrastructure and economic lift — far beyond the capital investment by the US government.

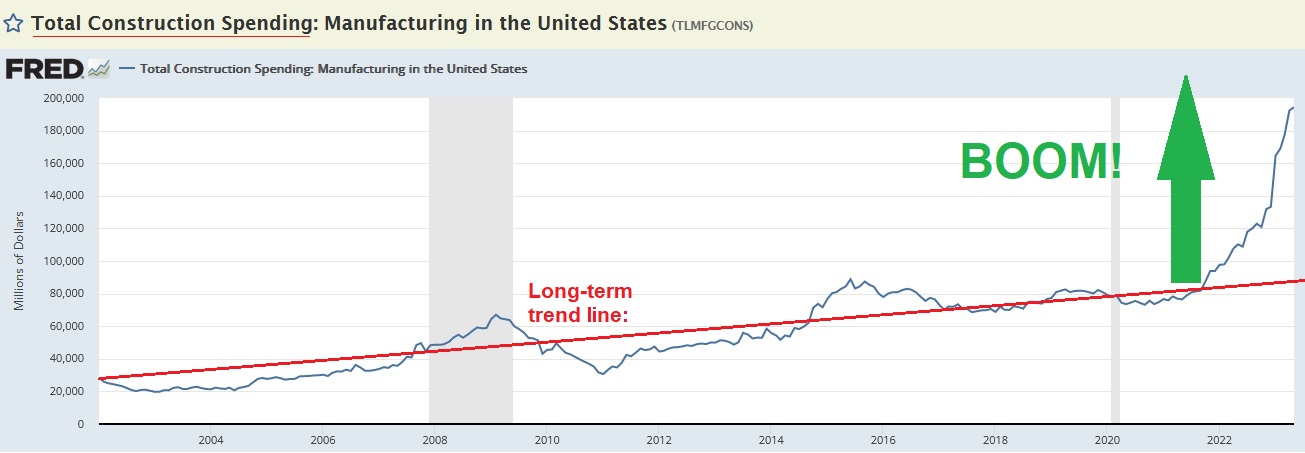

It looks like their dreams are coming true. Consider this image, courtesy of FRED (with modifications by me):

Boom indeed. New construction of US manufacturing facilities is BOOMING. The increase is nothing short of extraordinary. Consider these facts:

Total American construction spending in manufacturing has been fairly flat for decades. Primarily, in my opinion, due to the fact that since around 1990 America effectively outsourced manufacturing of pretty much everything to China. No longer. That ship has sailed.

Before the pandemic, many American companies were beginning to question the wisdom of that choice. The pandemic simply pounded a wooden steak thru it’s heart. Finally, we realized outsourcing everything halfway across the world, connected only by brittle supply chains, was an exceptionally bad choice. One America is reversing today. With vigor and results, and with a little help from our Uncle in Washington D.C.

Take a look at the image above. Near term, as we see the ‘annual rate’ (in dollars) of ‘total construction spending’ in manufacturing peaked in 2009 at around ‘67,000 million’ – or $67 billion. By July of 2015, that run rate lifted to about $88 billion. And there it remained somewhat range-bound until May of 2021 – when construction spending in manufacturing exploded. From about $76 billion to over $194 billion just 2 years later. That is a 300% increase in just 2 years, folks.

Growth like that is massive and unheard of. Call it onshoring, reshoring, or (if just over the border) nearshoring, manufacturing is coming back to America in a big way. This new trend is downright exploding. We can thank the catalyst of the IIJA and CHIPS acts. In my opinion, they definitely lit the fuse. We can only speculate how much AI will play into these budding factories of the future … but the take-away here is easy: The timing is excellent. This accelerating trend could become the foundation for massive American economic growth for decades into the future.

Here’s a question for you: Did you know this fact before I shared it today? I suspect the answer is no. Because all we seem to get from media today is how horrible things are out there. And, yes, America faces real challenges. Many challenges. I do not want to minimize that fact. I won’t focus on them, but we all know they are out there. Such is life.

But it’s important to also balance the scales, when possible, and look for the things that might be going right. Not only does the massive expansion of manufacturing construction suggest the future of the American economy is bright, it employs a ton of people. In May of 2021, about 790,000 Americans were employed in “non-residential building construction.” By May of 2023, that number had increased to over 860,000 folks. That’s an increase of over 11%. In just 2 years. I am convinced the downstream implications promise even better results for America, Americans, and the US economy.

The FED has made short-term economic forecasting difficult. Their interest rate ‘hammer’ — if used indiscriminately or excessively — can easily derail everything. I’m hoping the hammer is now back in the tool shed. But short term fluctuations aside, the longer term economic view for America looks bright indeed.

Perhaps as bright as the grill at your local, expensive steak houses? Let’s take a look:

It IS looking a little brighter!

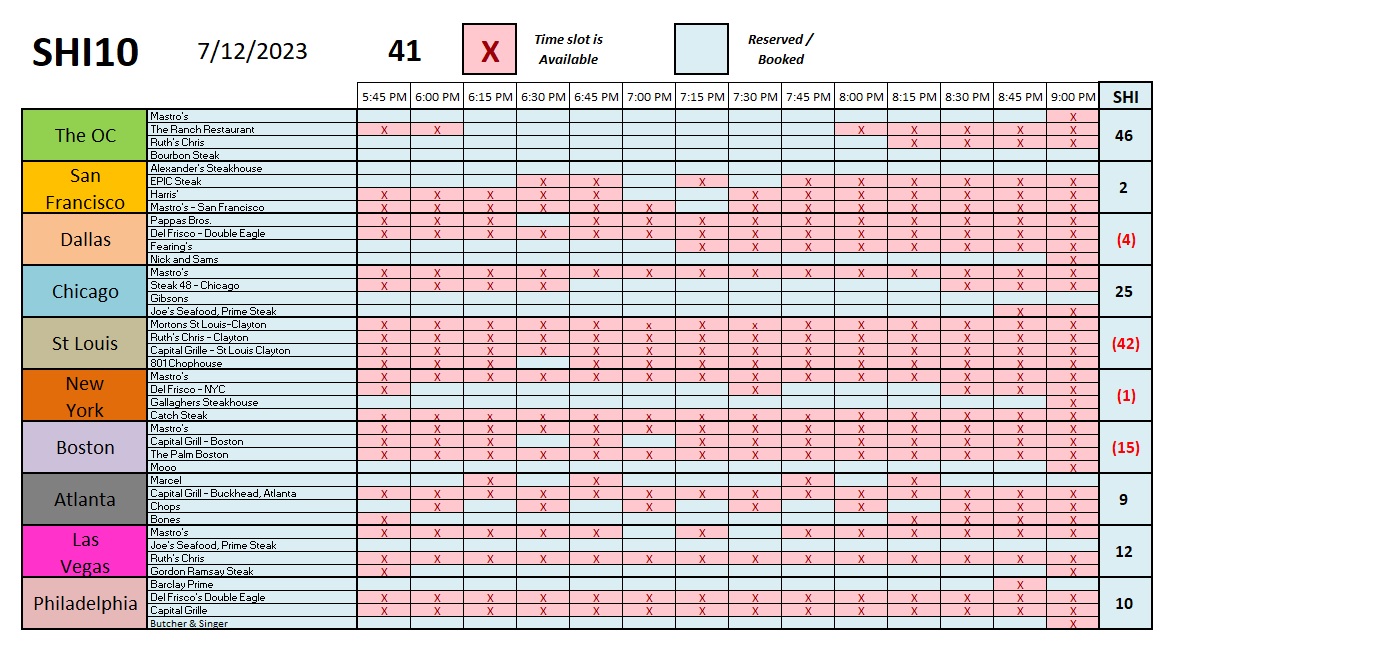

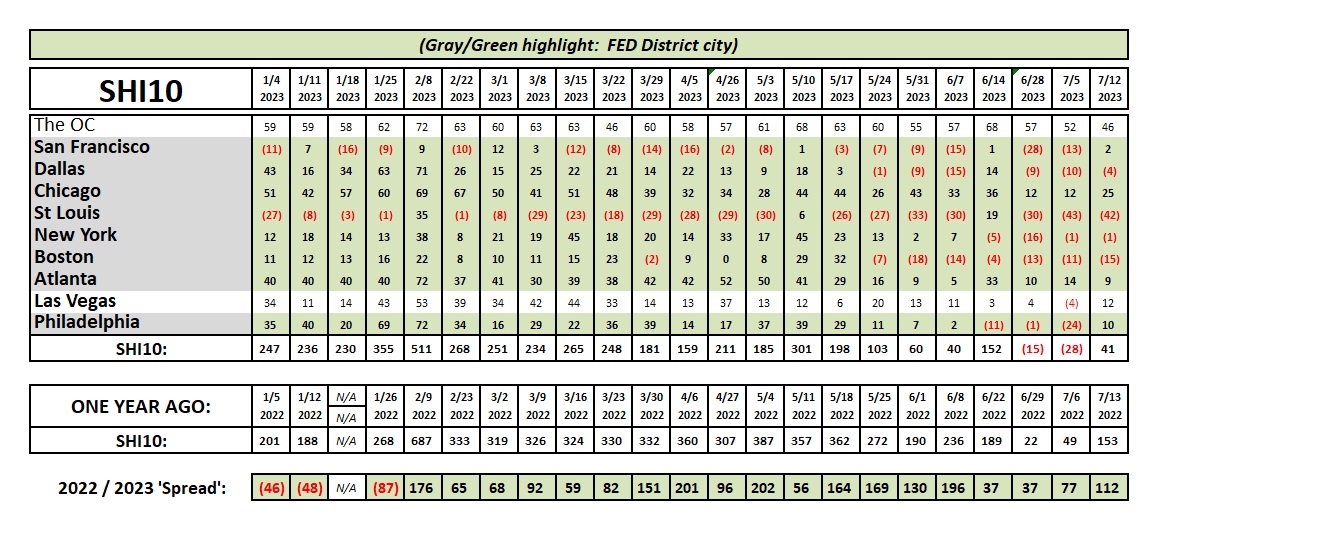

For the first time in 3 weeks, the SHI10 is positive. Reservation demand saw a general increase across the board, with the exception of here in the OC. Here’s the trend chart:

Improvement is improvement…but by any measure, expensive eatery reservation demand is muted across the US. Once again, the SHI confirms the US economy is softening slightly at present. At the same time, it’s interesting to note ‘Vegas is ‘out of the red’ this week.

Permit me one final comment on my blog topic from a couple weeks ago: the mythical recession, widely predicted by most economists for almost a year now, that never appeared.

SHI 6.28.23 — Here … Kitty, Kitty, Kitty! – The Steak House Index

In his blog from yesterday, Paul Krugman, the Nobel Prize-winning economist, asked the question:

“So it looks as if economists made a bad recession call. Why were they wrong?”

He starts the next paragraph: “One answer might be to ask why anyone would expect them to get it right.”

Funny. And spot on. The thing about the future is that it hasn’t happened yet. No one, at least no one I’ve met, has an effective, accurate crystal ball. So while we can forecast macro-economic, longer-term trends well founded in demographic, social, financial, and other conditions, accurate forecasting is far more of an art than a science.

Keep this in mind as you read my blog … and consider the advice given you by others thru a similar lens. 🙂

<:> Terry Liebman