SHI 8/30/17: A Rising Tide …

SHI 8/23/17: Nowcasting GDP

August 23, 2017

SHI 9/6/17: Housing Redux

September 6, 2017

. . . lifts all boats . . .

is a commonly used aphorism, and suggests general economic improvement will ultimately benefit everyone within that economic system.

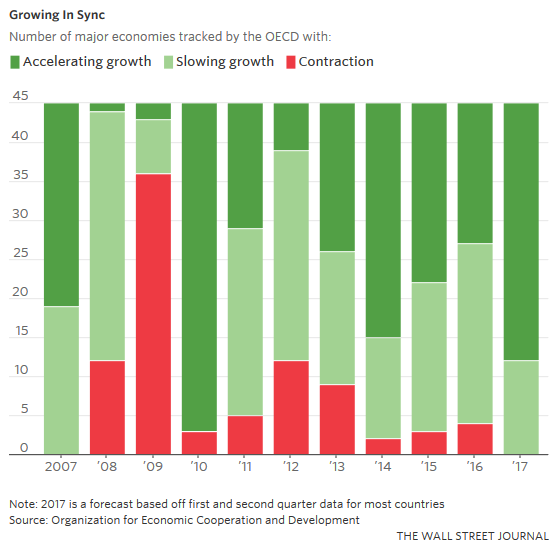

Well, everyone should be doing pretty well right about now since for the first time, according to the Organization for Economic Cooperation and Development (“OECD”), developed (‘major’) economies are all facing green lights and smooth sailing ahead:

For the first time since 2007 — the year that brought us the gift of the “Great Recession” — all major economies are growing in sync. Per the OECD, even little Greece should see 1% GDP growth this year. That’s quite a turn-around.

Hmmm…is this alignment a good thing or a bad thing … or a little of both?

Welcome to this week’s Steak House Index update.

As always, if you need a refresher on the SHI, or its objective and methodology, I suggest you open and read the original BLOG: https://www.steakhouseindex.com/move-over-big-mac-index-here-comes-the-steak-house-index/

Why You Should Care: The US economy and US dollar are the bedrock of the world’s economy. At present, is the US economy expanding or contracting? We need to know.

The world’s GDP is about $76 trillion. At last count, our ‘current dollar’ US GDP is now over $19 trillion — about 25% of the total. No other country is even close.

The objective of the SHI is simple: To help us predict US GDP movement ahead of official economic releases — important since BEA data is outdated the day they release it.

‘Personal consumption expenditures,’ or PCE, is the single largest component of US GDP — about 2/3 of the total. In fact, the majority of all US GDP increases (or declines) usually result from (increases or decreases in) consumer spending. Thus, this is clearly an important metric to track. The Steak House Index focuses right here … right on the “consumer spending” metric.

I intend the SHI is to be predictive, anticipating where the economy is going – not where it’s been. Thereby giving us the ability to take action early.

Taking action: Keep up with this weekly BLOG update.

If the SHI index moves appreciably -– either showing massive improvement or significant declines –- indicating expanding economic strength or a potential recession, we’ll discuss possible actions at that time.

The BLOG:

All 45 countries tracked by the Organization for Economic Cooperation and Development are on track to grow this year. This is a rare occurrence … the first time since 2007 that all are growing simultaneously.

Of course, forecast growth rates are very different — some economies are expected to show strong growth and others, well, much less. But all are expected to be positive.

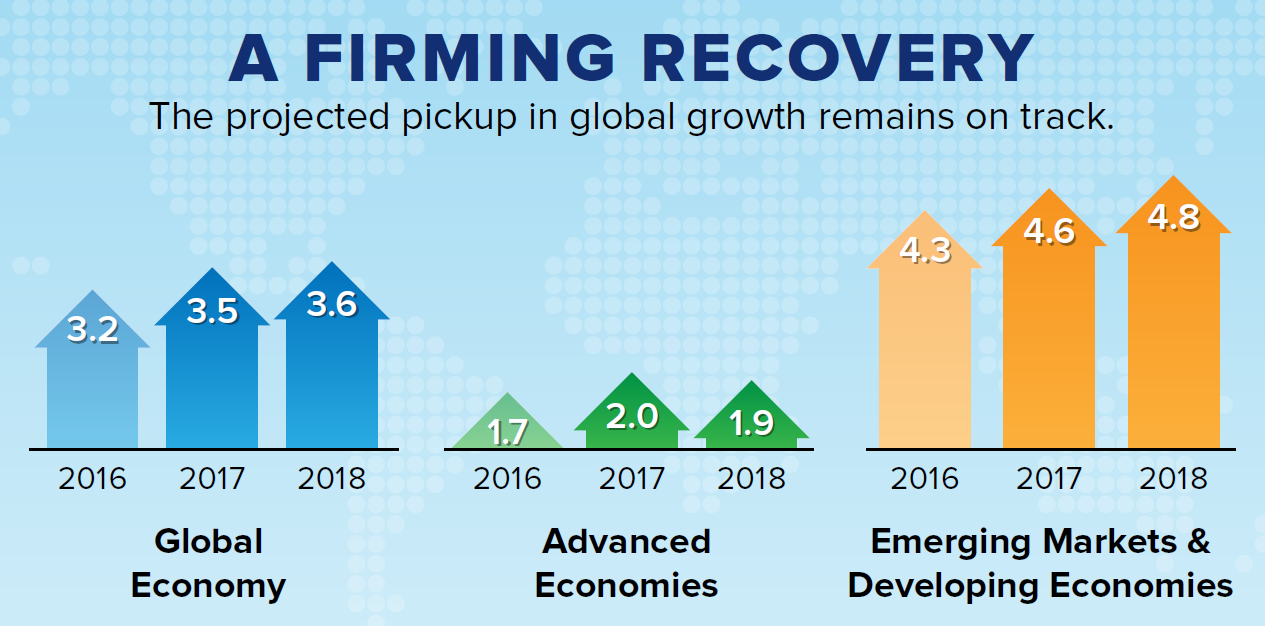

The International Monetary Fund agrees. In a recent update, they posted this graphic:

Note that 2017 and 2018 GDP growth in the ‘Advanced Economies’ is quite tame by comparison to ‘Emerging Markets’ and ‘Developing Economies.’

The IMF agrees with the SHI forecast: They expect 2017 and 2018 annual GDP growth of 2.1%. They expect Japan to continue under performing, with growth projected at 1.3% and 0.6%, respectively. And their EU GDP growth forecast is below that of the US: 1.9% and 1.7%, respectively.

The OECD is a bit more optimistic about US growth in 2018 (forecast: 2.38%), but agrees with the IMF in 2017. In summary, the international economic experts at the IMF and the OECD all seem to feel our boats are floating quite nicely.

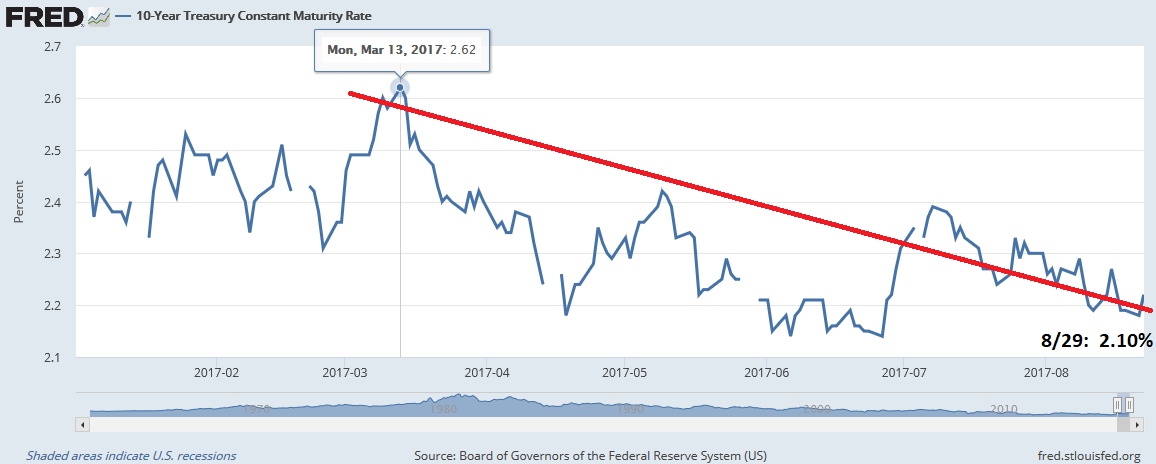

Then why, you might ask, are both short- and long-term rates falling? Specifically, here in the United States? Here’s a graph of the 10-year Treasury since January 1st:

Sure, the decline on 8/29 can be somewhat attributed to North Korea lobbing a missile over Japan. That’s a bit unnerving. More so if one lives in Japan.

But the 10-year has been sliding lower since peaking on March 13th of this year at a yield of 2.62% — and many economists opined it would continue higher. My favorite economist, however, predicted rates would likely head the opposite direction:

“I remain steadfast in my belief that we have already seen the 2017 peak for the 10-year Treasury. For the balance of the year, the 10-year T will fluctuate no higher than 2.50%. And likely much lower.” Of course, my favorite economist is me. 🙂

Back in January I shared my 2017 predictions with the world. Take another look: https://www.steakhouseindex.com/2017-forecast-the-future-is/

Over the past few months, I’ve written extensively on the topic of the “natural” or neutral rate of interest — and how it has declined significantly within the past 2 decades. I’m not alone in this belief: Many of the FED bank presidents either believe, or are starting to believe, this is factual. In my opinion, this is the underlying cause, the anchor, if you will, holding down all interest rates, here in the US and across the globe.

Of course, the massive central bank balance sheets are a huge anchor, too. If they were to shrink too quickly, throwing off all equilibrium, the equation would change quickly and dramatically. But I believe this is not a concern.

No, it’s likely that in spite of widespread positive global GDP growth, interest rates will remain at historic lows.

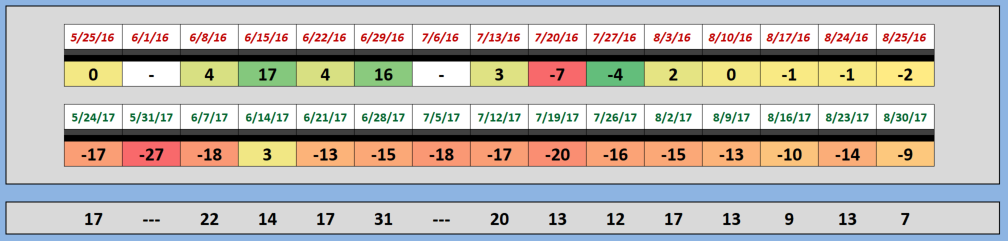

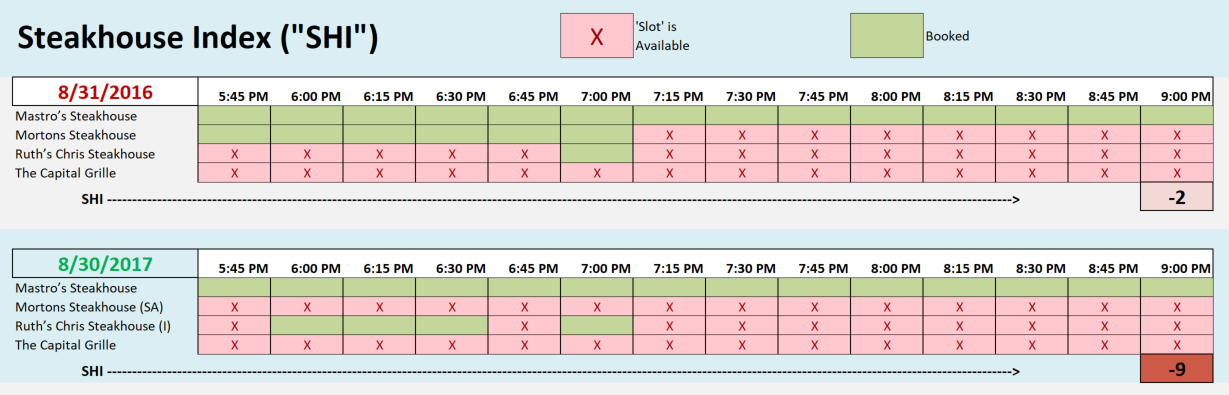

Opposite of interest rates, this week, the SHI is finally showing a bit of improvement! Here’s our trend report:

This is the best showing for the SHI in almost 2 months. Our ‘spread’ from the same week in 2016 is down to only 7 points. Of course, I would have trouble suggesting pricey steaks are once again back in vogue at our elegant eateries, but improvement is improvement. Here’s the SHI chart:

Mastros is certainly in vogue. Steaks are flying off the griddle. You can get a table at Mastros — but you’ll have to wait until 9:30 pm. Ruth’s Chris has made it’s best showing in months — with four (4) fully booked time slots.

You may have heard stock market investors speak of the “wall of worry.” The market, they claim, will ‘climb the wall of worry,’ a suggestion that financial markets have a common tendency to shake off, overcome, or ignore, negative news and keep ascending. Of late we’ve had plenty of economic, political and geopolitical issues to worry about. Whether the worry be US tax-cut legislation, hurricanes, neo-nazis, or North Korean missiles hurling over Japan, there’s definitely plenty to worry about.

Perhaps there always is. And maybe that’s the point. As different as today is, it’s just another day. More of the same. Perhaps.

A quick, final note: Earlier today, the BEA released their “second” estimate of Q2 GDP — now 3%. Averaging this number with Q1 — 1.2% — we have a GDP “run rate” for the first half of the year of 2.1%. This is a solid growth rate. Excellent.

For now, our boats continue to float … full speed ahead.

- Terry Liebman

2 Comments

Terry,

I ask you to consider two things this week for future blogs and SHI considerations.

1). How will the hurricane/tropical storm effect the economy? Also what nuggets of data do you think are appropriate to provide here for that? Insurance companies are definitely going to take a hit, and at the end of the year everyone’s premiums will inevitably go up to cover for this. I would be interested to hear your thoughts on the effect of natural disaster to the US economy.

2) Being from Chicago, I have considered the possibility that a steak house in each metropolitan city could be a good idea. Thoughts? My thinking is that across the nation, the appeal for a steakhouse (usually poorly lit) can vary. Being based in the SoCal area, you could be biased away from steakhouses. I see the counter argument that with enough data, trends in weather will be normalized. However, I think a national SHI in addition to the now localized SHI would be an interesting development. For example, Gibson’s in downtown Chicago will have a different feel than SoCal because people will be more inclined to go for more time of the year due to weather. Think cold weather 7 months of the year instead of 3. Thoughts?

Sincerely,

The steak house disciple

My brother suggested I might like this website. He was entirely right.

This post actually made my day. You cann’t imagine simply how much time I had

spent for this information! Thanks!