SHI 9.2.20 – With Little Fanfare, A New Era Arrives

SHI 8.26.20 – Halley’s Comet

August 26, 2020

SHI 9.9.20 – Ask the Big Mac

September 9, 2020

Today, the United States Federal Reserve Bank is arguably the most powerful institution on the planet. Of course, this depends on your definition of power. I define it as possessing the ability to take an action, or dictate policy, that directly impacts and changes people’s lives. Our myriad of government leaders have power. Presidents, Prime Ministers, dictators and theocrats have even more. But at this moment, the US FED has the most. Because the FEDs policies and actions directly impact the lives of almost 8 billion people.

” The FED has dominion over 8 billion people. “

Last month, the FED announced a monumental policy shift. This change is so huge, colossal in fact, that I expected to see significant commentary from the financial and economic press. But this did not happen. For some reason, comments were light. The moment seemed to have come and gone with a whimper when I expected to hear a roar. Quietly, and with little fanfare, the FED ushered in a new economic era … one that is sure to have far-reaching implications for years to come.

Welcome to this week’s Steak House Index update.

If you are new to my blog, or you need a refresher on the SHI10, or its objective and methodology, I suggest you open and read the original BLOG: https://www.steakhouseindex.com/move-over-big-mac-index-here-comes-the-steak-house-index/

Why You Should Care: The US economy and US dollar are the bedrock of the world’s economy.

But is the US economy expanding or contracting?

Before COVID-19, the world’s annual GDP was about $85 trillion. No longer. It will shrink thanks to ‘The Great Lockdown.’ I did not coin this phrase — the IMF did. The same folks who track global GDP. Until recently, annual US GDP exceeded $21.7 trillion. Again, no longer. But what has not changed is the fact that together, the U.S., the EU and China still generate about 70% of the global economic output.

The objective of this blog is singular.

It attempts to predict the direction of our GDP ahead of official economic releases. Historically, ‘personal consumption expenditures,’ or PCE, has been the largest component of US GDP growth — typically about 2/3 of all GDP growth. In fact, the majority of all GDP increases (or declines) usually results from (increases or decreases in) consumer spending. Consumer spending is clearly a critical financial metric. In all likelihood, the most important financial metric. The Steak House Index focuses right here … on the “consumer spending” metric. I intend the SHI10 is to be predictive, anticipating where the economy is going – not where it’s been.

Taking action: Keep up with this weekly BLOG update. Not only will we cover the SHI and SHI10, but we’ll explore related items of economic importance.

If the SHI10 index moves appreciably -– either showing massive improvement or significant declines –- indicating growing economic strength or a potential recession, we’ll discuss possible actions at that time.

The BLOG:

The Federal Reserve has had five (5) leaders in the past 50 years, people known as the “Chair of the FED” or simply the chair. Two (2) past chairs formulated and implemented significant monetary policy changes. Volcker, who became chair in 1979, waged the much-needed war against inflation. By lifting the FED funds rate in 1981 to over 19%, he triggered two (2) US recessions before he broke inflation’s back, seemingly vanquishing this enemy. His policies, never tried before, ended up doing the trick. Inflation and interest rates steadily declined over the next 30 years.

Bernanke, who took over as FED chair in 2006, also implemented massive policy changes when he was charged with navigating the US economy thru the ‘Great Recession’ of 2008. It was during Bernanke’s tenure that the FED finally, and completely, morphed from its lesser role as the central bank of the United States into the world’s central bank. Between 2008 and 2009, US monetary policy rescued the financial world. Since that time, the FED has remained firmly entrenched as the world’s lender of last resort.

In January of 2012, for the first time in history, the Bernanke and the FED established a de facto inflation target. Henceforth, the US inflation rate was to be 2.00%, the FED decreed. Of course, no one told inflation, because inflation has not cooperated, not one bit, stubbornly remaining well below this target level for more than a decade.

Since 2012, the FED has assiduously focused and worked to push up, and peg, inflation at 2.00%. For a time, they believed they achieved their 2% goal toward the end of 2016, when the US unemployment rate fell to below 5%. As the unemployment rate continued to fall, suggesting higher inflation was just around the corner, the FED consistently increased interest rates over the next 2 years. This action was straight out of the FEDs current playbook — an action designed to “cool” the economy and prevent inflation from quickly rising above the 2% goal, possibly getting out of control.

You see, that was the fear. For decades, economists at the FED and around the globe have been ardent believers in an economic theory known as the Philips Curve (“PC”), which essentially establishes an “If/then” relationship between employment and inflation. The PC theory simply states that IF the unemployment rate falls below its “natural rate”, THEN inflation will begin to rise soon thereafter. This was the FEDs belief and expectation. This was why they quickly and significantly increased interest rates in 2016-2018.

But rampant inflation did not appear. In fact, as the unemployment rate continued to fall … all the way down to a 50-year low of 3.5% … inflation still remained stubbornly below the 2% target. Once again, the Philips Curve inaccurately predicted an inflation spike. Once again, economists were puzzled by the outcome.

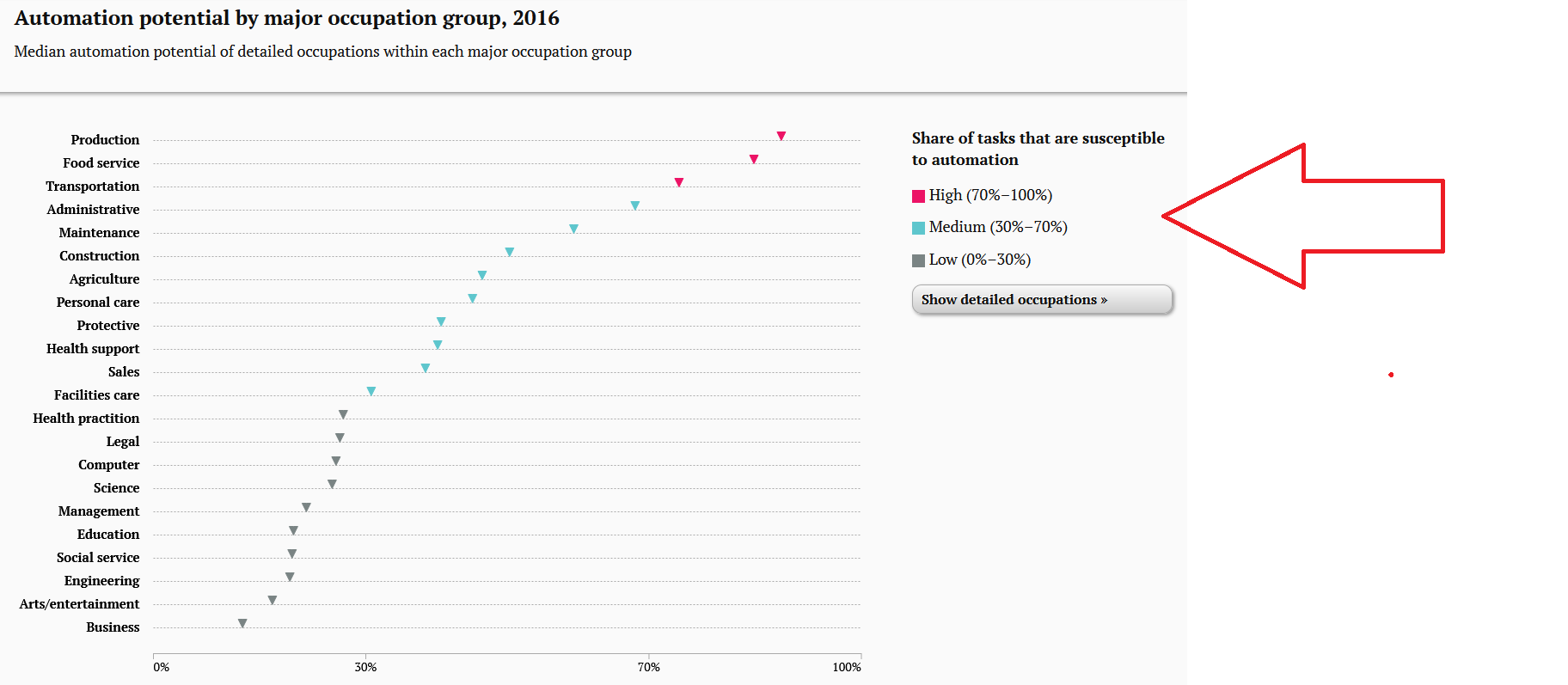

Fast forward to today: The FED now realizes they have consistently underestimated how strong the labor market could without triggering unwanted, excessive inflation. Finally, after many years of observation, the FED is finally acknowledging that the PC is no longer an accurate metric. Finally. Of course, for years now, long-time readers of this blog know I have suggested PC has not worked during 21st century. I believe the relationship broke down years ago, as the ‘industrial revolution’ waned and the ‘technology revolution’ took wings. Over the past 3 decades, across the globe, advances in technology have reduced human labor, as a percentage of production cost inputs, by almost 50%. Automation, both in hardware and software, has dramatically changed the labor landscape. Thus, in my opinion, today’s current definition of labor has changed. When Phillips made his observation between inflation and unemployment, and crafted his theory, ‘labor’ was implicitly defined as ‘human labor’. The word human was integral and assumed. Because in 1950, there was no alternative. Today, I believe the definition of labor must be expanded to include ‘non-human’ labor such as robotics, automation, AI, machine learning, etc. This is our present reality – and it is accelerating. As ‘non-human’ labor became available and cost-effective, the demand for ‘human labor’ has declined. And so, over the past 30 or so years, the demand for human labor, across the globe is down by about ½.

If you are shocked by these comments, and find yourself having trouble believing the data, take a look at this (right click, open in a new window):

https://www.fastcompany.com/90483273/one-day-you-might-live-in-a-3d-printed-house

Still not convinced? Then consider this piece written by the Brookings Institution almost 2 years ago (again, right click, open in a new window):

… and consider this statement from the report: “The sharp segmentation of the labor market by educational attainment, gender, age, and racial-ethnic identity ensures that some demographic groups are likely to bear more of the burden of adjusting to the AI era than will others. The probable divides are clear: Men, youth, and less educated workers, along with underrepresented groups all appear likely to face significantly more acute challenges from automation in the coming years.”

Across the globe, we see continued erosion in the need for human labor. Automation has become a cost-effective alternative in many instances. And, perhaps even more concerning, at least when viewed thru a 2020 lens, the adverse impacts will be even greater on the young and minorities. The trends and data are incontrovertible.

By this policy change, the FED finally overtly acknowledges what has been apparent to many for years:

Labor conditions are evolving rapidly, and the changes are structural and permanent.

Powell’s policy shift is the 3rd major FED policy change in the past 50 years. You see, with this policy change, the FED is laying to rest the debate over the efficacy of the Phillips Curve. They are finally, and explicitly, stating that Philip’s methodology, validated in the 1950’s and in vogue for decades, no longer applies in today’s global economy. Thus, with this policy shift, the FED will not quickly react to low and falling unemployment levels, when they occur, and they will permit inflation to exceed 2% for long periods, with the expectation that the inflation rate will average 2% over time.

The bottom line: Ultra-low unemployment rates will no longer trigger FED interest rate increases designed to “cool” the economy. They will let it run … and run … and run. Possibly for years, until the inflation rate actually rises – possibly well above 2%. While they do, they will keep short-term interest rates at very, very low levels. And I believe the FED made this choice now, in August of 2020, for a very specific reason.

Historical fact is fact. To quote the late Senator Moynihan, “Everyone is entitled to his own opinion, but not his own facts.” Well, I still agree with the Senator even if others in politics and the media do not. ?

So, here are the facts. The Bureau of Labor Statistics monthly labor report titled, “The Employment Situation,” contains an immense amount of data. Table A-2 is titled, “Employment status of the civilian population by race, sex and age,” and it tracks, among other things, unemployment levels by ethnicity. Below, I’ll share and compare the data from the BLS reports on ‘Whites’ and ‘Blacks’ (African American). This data was extracted directly from the reports, all of which are available on the internet.

- 2020, July: White unemployment rate – 8.3%; Black unemployment rate – 14.6%

- 2019, December: White unemployment rate – 3.2%; Black unemployment rate – 5.9%

- 2018, December: White unemployment rate – 3.3%; Black unemployment rate – 6.2%

- 2017, December: White unemployment rate – 3.7%; Black unemployment rate – 6.8%

- 2016, December: White unemployment rate – 4.1%; Black unemployment rate – 7.4%

- 2015, December: White unemployment rate – 4.5%; Black unemployment rate – 8.3%

- 2014, December: White unemployment rate – 4.6%; Black unemployment rate – 10.2%

- 2013, December: White unemployment rate – 5.9%; Black unemployment rate – 11.9%

- 2012, December: White unemployment rate – 6.6%; Black unemployment rate – 13.7%

- 2011, December: White unemployment rate – 7.5%; Black unemployment rate – 15.8%

As you can see, the data definitively shows that Black unemployment rates tend to be about double that of Whites. I make no social commentary here. These are the facts as compiled by the BLS. Thus, when the FED raises rates in order to slow the economy in response to low unemployment levels, African Americans are disproportionately adversely affected. Again, I’m not making a social statement. This data is factual.

I believe the FED has taken notice, too; and, I believe the FED has made a ‘social’ statement with their policy change: The FOMC statement stated “among the more significant changes to the framework” is “On maximum employment, the FOMC emphasized that maximum employment is a broad-based and inclusive goal ….” For the first time in the FEDs history, since the FEDs formation in 1913, I believe it has made a ‘nod’ to the inherent structural racial inequities within the employment and financial markets and models.

I believe this word choice was not accidental. It was intentional. Low levels of general unemployment, as seen in this last long-term economic expansion when general unemployment reached 3.5%, helped usher in low levels of non-white unemployment. The lowest in decades. In this policy statement, the FED is now accepting responsibility to achieve not only low levels of general unemployment, but, also, low levels of minority unemployment. They are specifically focusing on this issue … and with the word “inclusive” they are asking legislators to take up the issue in the appropriate regulatory bodies.

The FEDs new policy mandate to achieve an average 2% inflation target, over time, is a de facto policy statement telling us the FED is also targeting minority employment levels. In order to achieve both mandates, the FED will now maintain ‘quantitative easing’ conditions a much, much longer time than under prior mandates. Remember: The FED often triggers recessions when they chose to withdrew market and financial support. No longer. By their new policy, they want general unemployment levels to fall to, and remain at, very low levels. By their new policy, I feel they are also acknowledging the relatively new, and growing, challenges facing ‘human labor’ in the 21st century.

How does the new FED policy impact your assets and investment? Significantly, I believe. Over the next 3-5 years, I believe they will all increase significantly in value. In general, the protracted quantitative easing and ultra-low interest rates promised in the new policy will drive P/E ratios higher and capitalization rates lower. Whatever threshold you previously used to define a “good return” on invested capital will be redefined: Good is now lower. Whatever a “good return” used to be, it is now trending toward zero.

Whether intended by, or simply an unintended consequence of, current central bank policies across the globe, fiscal and monetary policies implemented to help the general population will have the effect of accelerating the financial trends that followed the Great Recession of 2008. The globe is more awash with capital than ever before. Of course, this condition definitely helps improve the lot of the general public, but it is helping the wealthy even more.

The “Great Financialization” that began with Nixon’s ‘Economic Stabilization Act of 1970’, which grew roots for decades thru 2007, and was then ratified in central bank monetary policies post-Great Recession, are accelerating in now 2020. The new FED policy has dumped gasoline on the already-burning fire. Hold on. It’s gonna be an interesting ride.

– Terry Liebman